Link to report in Chinese Click here

- SenseTime (0020.HK) describes itself as “a leading AI software company,” however, we believe that in this case AI stands for Artificially Inflated revenue. Our research exposes SenseTime for what appears to be a pattern of falsifying revenue through employment of revenue fabrication schemes.

- Two court cases describe revenue fabrication and round-tripping schemes in which SenseTime either directly or through intermediaries provides funds to customers that in turn are used to purchase goods from SenseTime that might never have been delivered.

- The scheme was corroborated by the CEO of Capital Watch, a Chinese financial media company, who reported that SenseTime invests in third-party companies in exchange for revenue of an equal amount without real delivery of product.

- As unearthed in one of the court cases, SenseTime’s round-tripping scheme involved a counterparty who was detained by the police and never paid back the money. This implies to us that SenseTime either wilfully works with criminals or does not conduct risk management.

- We uncovered several undisclosed related parties controlled by SenseTime executives and senior employees – SenseTime appears to be hiding these entities off the balance sheet, reminiscent of the Philidor-Valeant relationship.

- SenseTime has deep ties to the Chinese government as reported by employees and media which has led to unprofitable (and seemingly unpaid) contracts.

- Chinese government ties also led SenseTime to being blacklisted by the United States Government since 2019 due to use of its facial recognition software in persecuting Uyghur Muslims – the blacklist cuts off SenseTime from U.S. technology markets.

- We believe that SenseTime’s cash burn will continue unabated despite attempts to stem losses via headcount reductions, while large (and growing) accounts receivables indicate, at best, an inability to collect payment and, at worst, fake revenue.

- Experts are skeptical of SenseTime’s future due to intense competition from larger and better funded peers such as Alibaba, Baidu, Huawei, Tencent, etc.

- Employee reviews online reflect dissatisfaction and dysfunction at a directionless and unprofitable business.

- Smart money is rushing for the exits with Alibaba and one co-founder reducing their respective stakes to zero.

Introduction

SenseTime Group Inc., listed on the Hong Kong Stock Exchange, primarily supplies its facial recognition technology to the Chinese government. The company loudly proclaims itself as the latest hot artificial intelligence (AI) company. Press releases and presentations that target the latest trends in AI include projects in the fields of “Smart City”, “Smart Traffic”, “Smart Auto”, “Smart Business”, “Industrial Quality Control”, “Smart Culture and Tourism”, “Smart Health”, “Smart Life” and “AI Education”. SenseTime repeatedly introduces itself as “the world’s leading AI platform company” or “leading AI algorithm provider”. This bull case, pushed by the company and sell-side analysts, is heavily reliant on SenseTime’s various AI technologies becoming growth drivers for the company. While these buzzwords might attract superficial interest from investors, our research reveals a drastically different picture.

Our research indicates that SenseTime has gone down the path of financial manipulation through a revenue round-tripping scheme and failing to disclose a tangle of related party businesses owned and controlled by company officers. Unfortunately, revenue round-tripping does not actually improve cash flow. SenseTime still finds itself losing billions of RMB per year.

We believe that SenseTime’s core facial recognition business has become notoriously unprofitable due to intense competition and the fact that the Chinese government simply does not make a practice of awarding highly profitable contracts to majority foreign owned businesses. This unfortunate position has led SenseTime to hype up their various AI endeavors in corporate communications, which actually describe a diffuse project-based business which is unlikely to scale like a true SaaS provider. The company appears to be devoid of a differentiated AI technology, as evidenced by the feedback of their own employees, and on its heels reacting to embarrassing gaffes such as showcasing an AI technology to investors that is later revealed to be a competitor’s product.

While insiders are selling their shares to the public, investors are cautioned to question the AI hype, and look deeper at a company that we believe is deeply dishonest.

Apparent Insider Exposes How the Revenue Round-tripping Scheme Works

The CEO of a financial media firm, Capital Watch, described the alleged SenseTime round-tripping scheme in detail. He seems to be intricately familiar with the process.

source:https://36kr.com/p/2223085043282952

The paraphrased translation of this WeChat post alleges SenseTime would invest 200 million RMB into 4 – 5 companies. The recipient companies pose as distributors of SenseTime, and then transfer their received 200 million RMB back to SenseTime, which books it as revenue. In the beginning, SenseTime would produce and deliver a couple of hundred units of the product. Later on, they simply waived production and logistics, rather [SenseTime and its distributors] just directly exchange invoices [without delivering any real products].

Further corroborating evidence strongly supports these allegations.

Local Court Cases Appear to Describe Revenue-Fabrication Schemes

Two of-record lawsuits in China courts involve SenseTime; both documents seem to suggest that SenseTime has been engaging in activities to fake revenues.

Court case 1: Beijing SenseTime Technology Development Co., Ltd. (“SenseTime Company” as Plaintiff; Chinese name: 北京市商汤科技开发有限公司) vs Jiangsu Jingyida Technology Co., Ltd. (“Jingyida Company” as Defendant, Chinese name: 江苏精仪达科技有限公司)

Considering the importance of this case, below is the more detailed illustration:

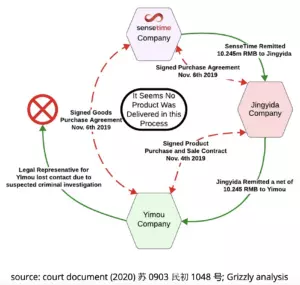

- SenseTime Company signed a purchase agreement with Jingyida Company on November 6, 2019 for a list of products (i.e., Toshiba mobile drives, Samsung Solid Hard drives, etc.) worth a total of 10.245 million RMB. Beijing SenseTime remitted a payment of 10.245 million RMB to Jingyida Company on November 17, 2019.

- Jingyida Company signed a product purchase and sale contract with Yimou Company on November 4, 2019 to purchase essentially the same products worth a total of 10.289 million RMB from Yimou Company. Jingyida Company remitted a payment of 10.289 million RMB to Yimou Company on November 18, 2019 (on the same day Yimou Company made a payment of 44,000 RMB back to Jingyida Company, resulting a net payment of 10.245 million RMB), one day after Jingyida Company received the 10.245 million RMB from SenseTime Company.

- In the meantime, Yimou Company also signed a goods purchase agreement with SenseTime Company on November 6, 2019, the same day SenseTime Company signed the purchase agreement with Jingyida Company. And the products under this agreement include essentially the same products that SenseTime were to allegedly purchase from Jingyida Company, plus certain SenseTime software.

In other words, during this three-party transaction, SenseTime Company were to purchase products from Jingyida Company, and Jingyida Company were to purchase the same products from Yimou Company, and lastly Yimou Company were to purchase essentially the same products from SenseTime Company, according to the multiple contracts/agreements referenced in the court documents. The payments were also meant to follow from SenseTime Company to Jingyida Company, and from Jingyida Company to Yimou Company, and lastly from Yimou Company back to SenseTime Company. This cycle was broken because Yimou Company’s legal representative Mr. Cai had lost contact due to suspected criminal investigation before this transaction was completed. By utilizing this kind of round-trip transaction, we believe SenseTime could artificially inflate its reported revenues.

We were lucky enough to catch this because the key person of one of the three parties, Yimou Company, had lost contact during the transaction, which resulted into this lawsuit between SenseTime Company and Jingyida Company. Imagine how many similar dealings could have gone unnoticed.

In this case, SenseTime Company sued Jingyida Company, alleging the reason for the lawsuit was Jingyida Company failing to fulfill the agreement by delivering the products under the agreement. However, the ruling of this case is that the court decided Jingyida Company fulfilled the agreement, and it is not required to pay back the 10.245 million RMB plus interest that SenseTime Company demanded to be repaid.

本院审查认为:人民法院审理经济纠纷案件,认为有经济犯罪嫌疑的,应当将相关材料移送公安机关或检察机关。本案中,原告商汤公司、被告精仪达公司及上海易华电子商务有限公司三方于2019年11月4日、6日签订了采购协议,三方之间为循环贸易。商汤公司于2019年11月17日将货款1024.5万元汇付给被告精仪达公司,精仪达公司于次日将该款项汇付给上海易华电子商务有限公司,现因上海易华电子商务有限公司及其法定代表人蔡某因涉嫌犯罪已被公安机关立案侦查。本院审查认为,上海易华电子商务有限公司及其法定代表人蔡某涉嫌犯罪,故本案应移送公安机关查处。依照《中华人民共和国民事诉讼法》第一百五十四条、最高人民法院《关于在审理经济纠纷案件中涉及经济犯罪嫌疑若干问题的规定》第十一条、《最高人民法院关于适用<中华人民共和国民事诉讼法>的解释》第二百零八条第三款规定,裁定如下:

驳回原告北京市商汤科技开发有限公司的起诉。

source: court document (2020) 苏0903民初3312号

Translation:

The court’s review concluded: When people’s courts hear economic dispute cases and suspect economic crimes, they should transfer the relevant materials to the public security organs or procuratorates. In this case, the plaintiff SenseTime Company, the defendant Jingyida Company, and Shanghai Yihua E-commerce Co., Ltd. signed a purchase agreement on November 4th and 6th, 2019, constituting round-trip trading among the three parties……

In addition, the court ruling also stated that the three parties: plaintiff SenseTime Company, defendant Jingyida Company, and Shanghai Yihua E-commerce Co., Ltd (“Yimou Company” as referenced above) are considered to be in a round-trip trading.

It was also reported that recently SenseTime’s Intellectual Property Executive Director, with the surname of Gao, was suspected of accepting “huge amount of” bribes from suppliers and criminal coercive measures have been implemented by the police.

Regardless of this transaction looking entirely fraudulent, it reflects terrible risk management by SenseTime to work with criminals.

Court case 2: Sichuan Changhong Jiahua Information Product Co., Ltd. (“Changhong Jiahua” as Plaintiff; Chinese name: 四川长虹佳华信息产品有限责任公司) vs Fujian Xinzeer Information Technology Co., Ltd (“Xinzeer Company”; Chinese name: 福建省新泽尔资讯科技有限公司) and its legal representative, Caitong Su, as Defendants

First a brief bit of background on this lawsuit: On December 3, 2019, Changhong Jiahua (seller) and Xinzeer Company (buyer) signed a purchase and sale contract involving SenseTime’s products worth a total of 3.27 million RMB.

1.2019年6月份,原告业务经理季世元和其合作伙伴上海商汤智能科技有限公司(以下简称商汤公司)业务经理李广得知被告有“人脸识别” 产品采购需要,多次到被告处走访推销商汤公司的“人脸识别”产品。但因被告已经采购并使用了深圳巨龙公司的“人脸识别”产品,便表示无需再购买。此时原告跟商汤公司的业务经理提出,由被告向原告采购一小部分“人脸识别”产品,原告向被告提供310万元的借款,利息按年利率11%计付,但要求以签订货物买卖合同的形式支付借款。被告当时业务因深受疫情影响,急需一笔资金用于生产经营,于是便答应了原告的借款方案。具体方案为:第一步,先由原告向商汤公司虚拟采购案涉产品并签订相应买卖合同和收货单,然后原告向商汤公司支付310万元虚拟货款;第二步,由商汤公司向被告的下游代理商福建坤骏公司科技有限公司(以下简称坤骏公司)虚拟采购案涉产品并签订相应买卖合同收货单,商汤公司将该310万元虚拟货款支付给坤骏公司;第三步,由坤骏公司将该310万元款项以同样方式付至被告子公司厦门市新泽尔信息科技有限公司账户;第四步,由厦门市新泽尔信息科技有限公司也以同样方式将该310万元付至被告银行账户;最后,由被告以同样方式向原告虚拟采购案涉产品并签订相应买卖合同和收货单,在形式上形成被告向原告购货310万元,货已收而款未付清的闭合式循环。

source: court document (2020) 京0106民初30115号

Translation:

In June 2019, the Plaintiff [Sichuan Changhong]’s business manager, Shiyuan Ji and his partner, the business manager of Shanghai SenseTime Intelligent Technology Co., Ltd. (“SenseTime Company” thereafter), Guang Li, learned that the defendant has product purchase needs for “facial recognition”. [They] visited the defendant multiple times to promote SenseTime Company’s “facial recognition” products. But [they] were told that the defendant had already purchased and was using the “facial recognition” products from Shenzhen Julong Company, and [the defendant] did not need to purchase [additional products]. At this point, the plaintiff proposed to the business manager of SenseTime Company that the defendant purchase a small portion of “facial recognition” products from the plaintiff, and the plaintiff would provide 3.1 million RMB worth of loan with an annual interest rate of 11%, but requesting that the loan be paid in the form of signing a goods purchase and sale contract. The defendant’s business at the time was severely impacted by the pandemic and urgently needed money for production operations, therefore the defendant agreed to the plaintiff’s loan proposal. First step: the plaintiff would virtually purchase the involved products from SenseTime Company and sign the corresponding sales contracts and receipts, then pay SenseTime Company a virtual payment of 3.1 million RMB……

In this transaction, despite the eventual ruling of the court, we found the defendants (Fujian Xinzeer and its legal representative)’s explanation of why this contract should be invalid is very helpful for outsiders to understand how the plaintiff (Changhong Jiahua) and SenseTime engaged with the defendants for this product sale. It appears that according to the defendants, they did not have the need to purchase SenseTime’s facial recognition products in the first place, as they had already purchased and were using similar products from another company. However, we suspect SenseTime recognized this kind of transaction as revenue. There seems to be no other point to this entire transaction but to create fake invoices/revenue for SenseTime.

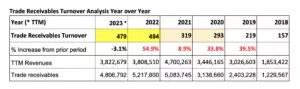

In both cases shown above, SenseTime seems to be involved in some form of revenue fabrication. It is impossible to comprehensively catch every instance of revenue fabrication, but when mistakes trickle through to the public eye such as court records, there are most likely many others that don’t surface. When unaccountable big-picture metrics, such as SenseTime’s off-the-charts 470+ day receivables turnover are posted, these are the kinds of suspicious details typically found in the shadows.

SenseTime’s Accounts Receivable Are Ballooning and Must be Written Off – Telltale Signs of Fake Revenues and Terrible Economics

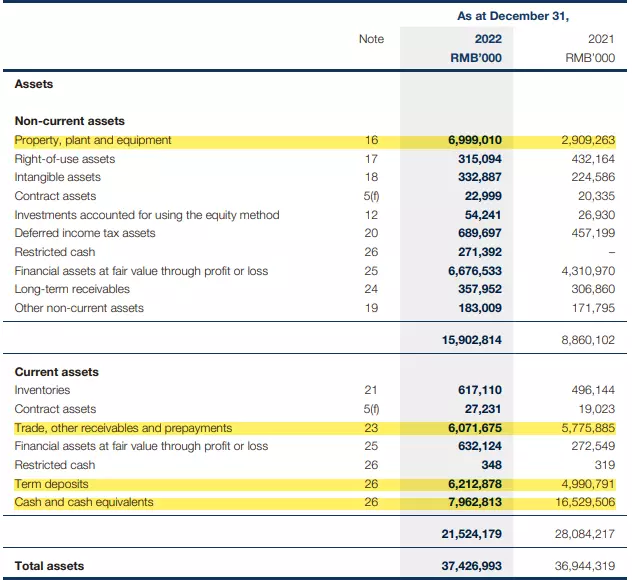

SenseTime’s financials are horrible and imply a failing core business. In the year 2022, SenseTime reported 3.8 billion RMB of revenues (a decline of 19.0% year over year as compared to 4.7 billion RMB in 2021) and it lost 6.1 billion RMB for the year. After certain adjustments, the company still recorded negative 4.2 billion Adjusted EBITDA and 4.7 billion RMB of Adjusted Net Loss. Both of these two adjusted metrics were far worse than in 2021. First half 2023 losses continue unabated.

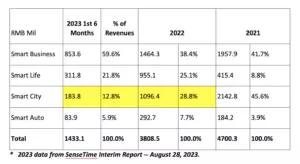

According to the company’s disclosure, it appears two major business segments (Smart Business and Smart City) are undergoing drastic decline year over year. For example, revenues from Smart Business were down from 1.96 billion RMB in 2021 to 1.46 billion RMB in 2022, and revenues from Smart City were down from 2.14 billion RMB in 2021 to 1.10 billion RMB in 2022. The Smart City business is cut almost in half year over year.

No meaningful improvement in 2023 half-year interim report

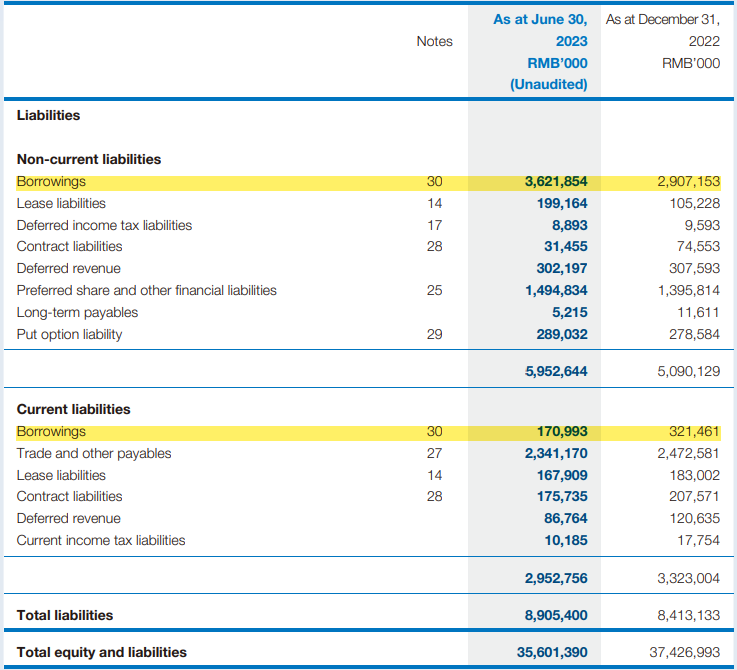

“Borrowings” is up 24% from EoY 2022 to June 2023 in interim report

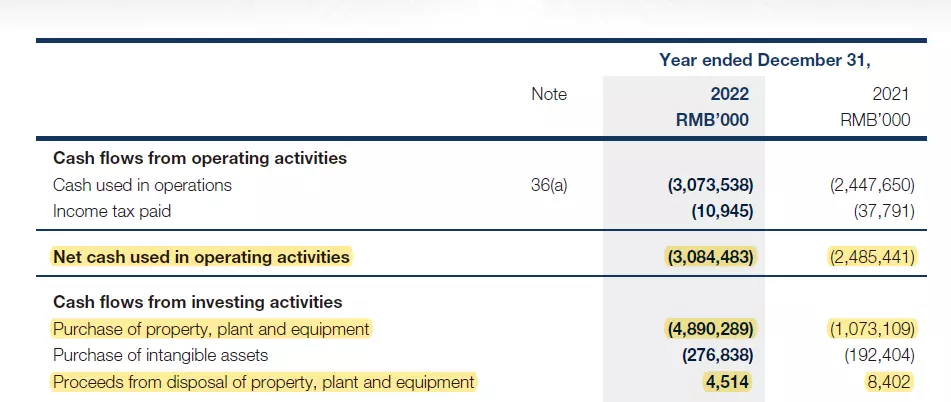

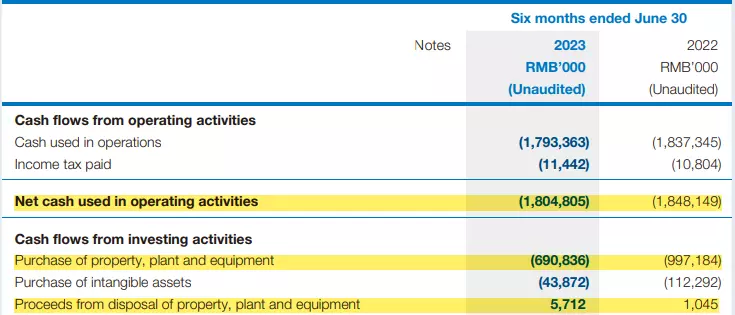

The company had 11.8 Bil RMB cash equivalents + term deposits, and it had 3.6 Bil of borrowings on its balance sheet as of June 30, 2023. SenseTime recorded a negative free cash flow of about 8.0 Bil RMB in 2022 (negative 3.5 Bil RMB in 2021) and reported another 2.5 Bil RMB outflow in the first half of 2023. This leaves the company with less than a two-year cash runway on hand.

The company has reportedly instituted layoffs across various departments this year ( Link ), not encouraging at a time when large and credible competition is committing massive resources to AI.

Worst of all, the disclosed trade receivables number and its allowance makes us doubt if the company has been cooking its books all along. With 40% of its revenue estimated to have been from Government contracts ( Link ), the sharp loss of principal revenue sources from urban and regional governments due to the real estate bubble suggests these receivables may never be collected. In other words, as bad as the current reported financials appear to be, the reality might be even worse at SenseTime.

Source: company findings; Grizzly analysis

Source: company findings; Grizzly analysis

For the Trade receivables item, the company’s gross trade receivable was 7.8 billion RMB as of December 31, 2022, and did not materially improve in the first half of 2023. However, the provision for impairment was set by the company at 2.58 billion RMB, which was about 33.1% of the gross trade receivables and raised yet another 13% as of June 2023. For the Other receivables item, the % of the provision for impairment as percentage of the gross other receivables is even higher (over 50%).

On one hand, the company is reporting 3.8 billion RMB in revenues with over 66% gross margin (FY 2022), but on the other hand, it appears that a preponderance of these reported revenues will never be collected from its customers. SenseTime itself attributes these impairments mainly to COVID, but such astronomical impairment numbers raise huge red flags and indicate further problems.

It is more probable that these high impairments are a direct result of the revenue fabrication schemes such as invoices for fictional transactions that SenseTime has been orchestrating, as well as government customers paying on their own timeline, that is, if they pay at all. (E.g. How many years will it take for the real estate bubble to deflate? The bad news isn’t yet all out.)

SenseTime’s financial and accounting team seem problematic at best. Investors should doubt the authenticity of the company’s reported financials. Even after massive impairments, the trade receivables turnover increased from 319 days in 2021 to 494 days in 2022. Receivables collection has worsened alarmingly every year since 2017, so this can be no surprise to management.

Source: company findings; Grizzly analysis

Source: company findings; Grizzly analysis

In the company’s own words:

“As of June 30, 2023, the aging of our gross trade receivables has worsened, compared to that as of December 31, 2022. A significant portion of our historical revenue was derived from Smart City, which typically features a long payment cycle as required by their internal financial management and payment approval processes. Although our overall cash collection amount has begun to improve year over year during the first half of 2023, cash collections for relatively long outstanding receivables remain challenging, as some of our customers, especially those in Smart City, face “temporary” budget constraints and uncertain macroeconomic environment.

From SenseTime 2023 interim report as of June 30, 2023

(bold and highlight by Grizzly Research):

SenseTime’s CFO, Zheng Wang, has plenty of investment experience in the capital markets. However, investors should notice Mr. Wang does not have much experience in the audit/accounting profession.

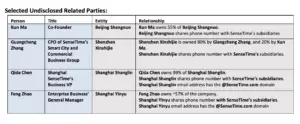

Cleverly Hidden Undisclosed Related Parties are Never a Good Sign

Our research uncovered numerous potential undisclosed related parties with SenseTime. Many instances were majority-owned by senior-titled officers of SenseTime or related to one another through publicly available sources. SenseTime’s conscious choice to keep these entities off the balance sheet is deeply worrying, especially in light of the revenue round-tripping described above.

Source: company findings; Grizzly analysis

Source: company findings; Grizzly analysis

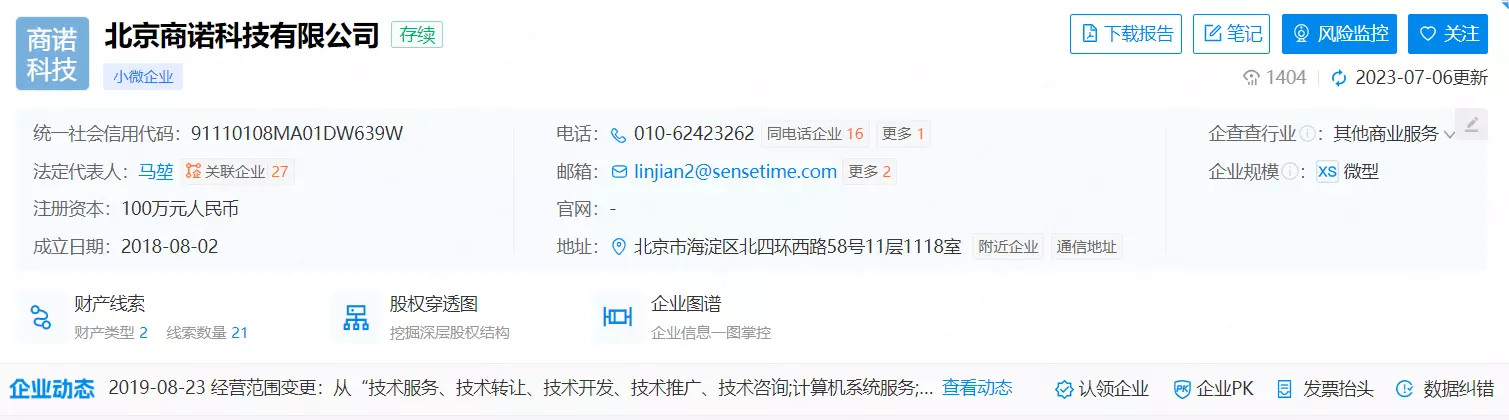

For example, Beijing Shangnuo Technology Co., Ltd. (“Beijing Shangnuo”; Chinese name: 北京商诺科技有限公司).

Source: Qichacha

According to Qichacha, Beijing Shangnuo was established on August 2, 2018 and lists Kun Ma as its 55% owner. Kun Ma is reported to be SenseTime’s co-founder. In other words, this company is majority owned by the individual Kun Ma, not by SenseTime. According to Qichacha, this company’s business includes internet information services, internet cultural activities, technology service and consulting, etc.

One company named Shenzhen Xinshijie Digital Technology Development Co., Ltd. (“Shenzhen Xinshijie”, Chinese name: 深圳市新视界数码科技开发有限公司) has its 20% owner as Kun Ma, who is the co-founder of SenseTime as mentioned above. Its other 80% owner is an individual named Guangcheng Zhang. According to Qichacha, this company’s business includes facial recognition technology development, applied electronic information system’s technology development, etc.

Source: Qichacha

According to this article, this individual Guangcheng Zhang is the chief product officer of SenseTime’s Smart City and commercial business group.

Another two examples are Shanghai Yinyu Enterprise Management and Consulting Partnership (Limited Partner) (“Shanghai Yinyu”, Chinese name: 上海寅愉企业管理咨询合伙企业(有限合伙)) and Shanghai Shanglin Enterprise Consulting Co., Ltd. (“Shanghai Shanglin”, Chinese name: 上海商临企业咨询有限公司). According to Qichacha, Shanghai Yinyu’s business includes enterprise management and consulting, and Shanghai Shanglin’s business also includes enterprise management and consulting.

Source: Shanghai Yinyu (Qichacha)

Shanghai Yinyu shares the same phone number with many of SenseTime’s subsidiaries and has registered email address ends with @sensetime.com. However, its majority-owner is an individual named Feng Zhao (57.14%). According this article, Feng Zhao is SenseTime’s enterprise business’ general manager.

Source: Shanghai Shanglin (Qichacha)

Shanghai Shanglin also shares phone number with many of SenseTime’s subsidiaries and has registered email address ends with @sensetime.com. According to Qichacha, Shanghai Shanglin is 99% owned by an individual named Qida Chen. According to this article, Qida Chen is Shanghai SenseTime’s business VP.

The table above is representative, but there are likely many more. Our researched connections, mostly sourced from Qichacha and Chinese news and articles, are extensive but probably not exhaustive. Multiple entities are owned and/or controlled by SenseTime officers and senior employees, and they are connected to SenseTime through shared phone numbers and/or email domains.

This creates every possibility for related party transactions which have not been disclosed to outside investors, and facilitation of possible revenue fabrication schemes.

Businesses connected via senior officers to undisclosed related parties cast a dark shadow over financial statements. Investors face the risks that even the company’s poor financial results are less than a trustworthy representation of the company’s true financial picture.

SenseTime Has been Blacklisted in the U.S. since 2019 due to their Involvement in the Persecution of Uyghur Muslims

SenseTime’s worsening accounts receivable issue is worsened by the fact that the company has a severely limited target market and therefore no outlook for any real improvement. Obviously, the facial recognition software that SenseTime is selling to the Chinese government is an integral pillar of the company although SenseTime fails to disclose the exact revenue percentage attributable to government contracts. The fact that accounts receivable days keep ballooning clearly shows that customers are not paying on time or not paying at all. SenseTime seems to have no real outlook for improvement because the company has been banned from key markets.

In October 2019, SenseTime was added to the Entity List of U.S.’s Department of Commerce, ( Link ) and ( Link ) which essentially prohibits the company from doing business with or buying technology from U.S. companies.

“On Monday, the Department of Commerce announced that 28 Chinese companies and government entities had been added to a blacklist for their roles in human rights violations in Xinjiang, an autonomous region in northwest China that’s home to millions of Uighurs, a Turkic Muslim minority. Among the ventures banned are the Chinese startups SenseTime, Megvii, and Yitu, which, combined, have raised billions of dollars to develop commercial facial recognition technology.

Those three companies, which have flourished amid the Chinese government’s push for investments into artificial intelligence, have faced mounting criticism over perceived misuse of their technology by government agencies, particularly in Xinjiang, where it is believed to have played a role in the arrest and detention of more than a million Uighur Muslims and other ethnic minorities. While SenseTime and Megvii have denied working with state entities in the region, researchers and academics have uncovered troubling connections between their facial recognition tech and the surveillance and imprisonment of minorities in China.”

The companies that are on the entity list are facing technology backlash because the U.S. government will be “prohibiting them from purchasing U.S. products or maintaining relationships with American entities.”

In December 2021, SenseTime was also added ( Link ) to the investment blacklist by the U.S. Treasury Department due to its involvement in the suppression of ethnic minorities. This event actually delayed SenseTime’s IPO. ( Link )

“OFAC is also identifying a Chinese firm, SenseTime Group Limited (SenseTime), as a Non-SDN Chinese Military-Industrial Complex Company (NS-CMIC) pursuant to E.O. 13959, as amended by E.O. 14032. SenseTime owns or controls, directly or indirectly, a person who operates or has operated in the surveillance technology sector of the PRC’s economy. SenseTime 100 percent owns Shenzhen SenseTime Technology Co. Ltd., which has developed facial recognition programs that can determine a target’s ethnicity, with a particular focus on identifying ethnic Uyghurs. When applying for patent applications, Shenzhen SenseTime Technology Co. Ltd. has highlighted its ability to identify Uyghurs wearing beards, sunglasses, and masks.”

According to this article, after being added into the blacklist, “U.S. persons are prohibited from trading the securities of the designated companies.” SenseTime is listed at the Hong Kong stock exchange, which is supported by enormous liquidity coming from international investors including U.S. investors. With U.S. investors being banned from investing in the stock, the demand for the company’s stock has been negatively impacted. We do not think the company will be removed from this blacklist anytime soon.

On August 10, 2023, President Biden signed an executive order to block and regulate U.S.’s capital investment in China ( Link ), which primarily targets high-tech industries including chips, micro-electronics, quantum technology and artificial intelligence. It is expected that AI companies such as SenseTime would have greater obstacles advancing its AI technology in the future without technology and business cooperation with the U.S. and other western countries.

Experts say SenseTime has no Competitive Moat in AI, and no Access to Western Markets for their Future Offerings. Thus, SenseTime lacks any Convincing Investment Thesis.

We spoke with several industry experts who were in direct contact with SenseTime’s business offerings or are active clients. Also numerous former SenseTime technical employee interviews align with these conclusions. No one had a positive view of SenseTime’s outlook. Here is a summary of the main findings.

Before its IPO in December 2021, SenseTime established their SenseME solution for facial recognition as a leading competitor in the field of personal identification and security. Its solution has been implemented by banks and other payment providers. One expert summarized that “SenseMe was a break-through, but they [SenseTime] can’t come off their high horse.” Another expert emphasizes that SenseME’s success is a testament to the talent in the company that must be taken seriously by our analysis.

However, the big caveat is that AI solutions for recognition and generation of graphical or written content, including competitors to SenseME, are plentiful and rapidly becoming commoditized today, with strong competition from U.S. tech giants and Asian competitors. In May 2023, a leaked document from a senior engineer at Google Alphabet, published in “The Guardian” ( Link ) described how openly available open source software is already undermining the business model of the corporate generative AI models (i.e. services like ChatGPT, Bard, Midjourney, Stable Diffusion) . In other words, open source developers program generative AI solutions for everyone to use free of charge are making the entire business model of generative AI development unprofitable.

That is why SenseTime is forced to venture into Internet-of-Things and big data solutions that make use of specialized system networks and mass databases. In this context, SenseTime aggressively pursued pilot projects in the field of Smart City, Smart Traffic, Smart Auto, Smart Business, Industrial Quality Control, Smart Culture and Tourism, Smart Health, Smart Life and AI Education. (see sensetime.com)

For the following reasons, none of the experts we talked to had a positive outlook on SenseTime’s strategy:

-

- The variety and goals of these “smart” projects are de facto complex technology consulting services that are impossible to replicate as packages. They require expert consulting, software developers, and big data experts to build specific client solutions. That is why this strategy cannot scale profitability, despite the company being valued as a SaaS provider. The former employee quotes below consistently support this point.

- As a China-domiciled company, SenseTime must cooperate with the Chinese Communist Party (“CCP”) on all matters. One expert emphasized that ”there is always a way to send customer data back to China“. That is why SenseTime will never have access to Western markets to sell solutions for smart city surveillance, smart industry production and logistics, smart auto, smart health or life. All these lines of business are structurally relevant to the productive functioning of a country. Western prospects will not choose software solutions built upon a data foundation that is presumed shared with Chinese State security agencies. SenseTime’s addressable market can never grow beyond that of its own country and China’s few very close allies.

- Given SenseTime’s global shareholder base, China has no incentive to provide SenseTime with very profitable contracts that would create windfall shareholder earnings. Instead, China is more likely to use its grip on the company to “develop technology and let it barely survive”, as one expert commented. “It might even be the most advantageous strategy for China to force SenseTime into bankruptcy, if the CCP sees good reasons to take full control of SenseTime’s assets.” In any case, shareholders will likely end up disappointed.

We asked our experts specifically if they are optimistic or pessimistic with regard to the stock. All answered they were pessimistic based on the business and tech analysis alone.

Two Chinese investment banks cover SenseTime’s stock with elaborate analyst reports. Both of them changed their narrative about SenseTime with several hard pivots in the last three years alone. This is alarming and a sign of lack of any convincing long-term business strategy.

In their latest report, Chinese Merchants Bank International (“CMB”) writes in August 2023, SenseTime will “focus on Generative AI business development”, and Bank of China International (“BOCI”) writes on the same day “Only generative AI matters”.

In May 2022, BOCI was describing SenseTime as “leading Chinese AI software company engaging in city management, business optimisation, IoT, healthcare and automotive businesses.” These “smart” projects, however, are complex and heavily customer-tailored applications, which is a completely different business model than the much narrower business case of generative AI. In March 2022 CMB focused on SenseTime’s future strategy in the AI-as-a-Service Cloud business. This is, again, a completely different business strategy where AI solutions are not tailored to clients but server performance is rented out to the customers’ developers. In February 2022, CMB praised SenseTime as the “Unrivaled computer vision leader in China”. This statement might not have been wrong at the time, but the analysts’ succeeding hard pivots now appear as fiction, futile efforts undertaken with SenseTime to invent ever new growth narratives. Informed commentary is noticing:

This critique is sharply framed by trade publication “KR Asia” (10/17/2023) ( Link ) :

… major shareholders continue to frequently cash out. This sends a signal: there are still doubts about how long the generative AI trend will last, and there is even more skepticism about SenseTime’s ability to monetize it”

This scathing assessment is repeated by blogger “Tao is right”: (10/09/2023) ( Link )

“One of the major advantages of SenseTime is that it can tell stories. Wherever there is an outlet, it will go there and use hot concepts to continuously describe a larger business picture for capital.”

“as early as the IPO of SenseTime Technology, the “Metaverse” was mentioned 47 times in its prospectus; after talking about the concept in vain, the trend of digital collections has emerged, and SenseTime Technology has also made great efforts in digital collections”

“If you ask what the main business of SenseTime is, many people may not be able to tell clearly, because chasing the trend again and again makes SenseTime’s business look diverse and dazzling… SenseTime continues to enter new tracks. On the one hand, each business line is facing relatively strong opponents, and its current technical strength is not enough to make the company”

“these overly complicated business lines distract SenseTime’s resources and energy, making it difficult for the company to focus on business exploration, and to a certain extent, will also prevent the company from forming a stable business structure”

A former SenseTime technical program manager’s candid comments mirror the same issues — warning flags “from the trenches”, describing explicitly how SenseTime’s AI is really a string of one-off “pilot” and consulting projects, and its claim to AI-as-a-Service is failing to live up to the hype.

A former SenseTime technical program manager stated:

“First of all, there is no recurring profit because … although this is a fixed price project, SenseTime is trying to make it recurring by following the model of the SaaS company by software as a subscription, right? So this is what the company is trying to do to follow the model of the SaaS, software as a subscription model and through the AI cloud solution to provide the software upgrade year-by-year to have recurring profits.

But unfortunately, I think that project is still a fixed price. And the model to follow the SaaS subscription model and the productization is not as what is expected and planned. And this is a highly customized project. So that is my view, yes. The model is still not as built at the time after I leave, yes.”

“So this whole project is a pilot AI project … right? No one has done it before. … But because of this, it requires a high, high customization because there’s no predecessor can be learned before.

All things need to learn from scratch. I really see on what sense that it’s trying to do is that use it as a pilot, although there are a lot of customization, but transform this customization into the productization, but it is still very hard because the magnitude and the requirement from different company, it’s very different from the different industries, from different companies. It varies a lot, yes.

I see the productization is over time because again, for this project, you spend across a few years, and then you need to put a lot of researchers, software developers, hardware engineers, test QAs, long years. So eventually, this project will make some profit at this period of time, like for example, in one or two years. But because of the productization is taking longer, longer time, so this profit is just temporary.”

So previously, this project is built by [ _ competitor X _ ] [another ] … AI company from China. So it is beat by this company, but it was given up by [them]. Why? Because it is highly customized, and no one has done it before.

Did SenseTime get a huge amount of ROI for this? … Not really. It is considerable, but not as expected because the project spend is actually considered worse planned for one to two years… but now it’s three to four years, okay? And however, this is a fixed project. It’s not a target material. So more unexpected investment is going in to complete this project. So not much ROI, .. because it’s still a huge pioneer amount, and second question, whether it leads to more similar projects?

So to many industry at a great breadth is one of the core strategy from SenseTime … this is the reflection of not having a right business direction. Or the whole AI industry is not ready to be landed based on the adaptability from other industry.

The same former employee’s quote speaks to the vast gulf between the company’s marketing story about AI as a SaaS when contrasted with the reality of customer needs:

“But ultimately, we are just making a joke that, hey, you’re just like paying money to make a show to those companies, but nothing. So this is what is not being changed. … I’m not sure whether the investment will be five years or ten years, but in my opinion, at least for the two years, companies will become more conservative about AI. And they would not be willing to pay more money for it until they see this is really getting returns from the project.”

“… the leadership or the management from SenseTime needs to be refreshed because it is still led by a bunch of scholars, and they don’t have the business experience”

“the leadership structure for me is still scholars but the business vision … it’s not as clear and defined in long term”

“in terms of the integration, in terms of the applications, Baidu and Alibaba wins far more and much better than SenseTime.”

SenseTime Embarrasses Itself by Taking Results of their Supposedly Original AI Technology from Another Company’s Platform

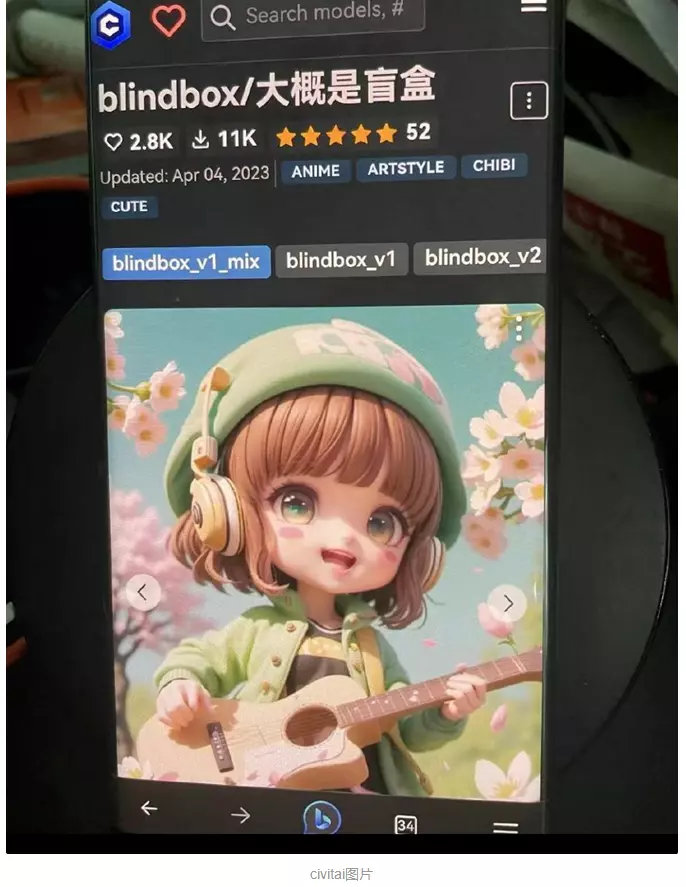

On April 10, 2023, SenseTime held a conference to demo for investors and media its AI technology and product. SenseTime showed one picture that created a wave of media scrutiny and controversy. The inclusion of an image from Civitai in SenseTime’s presentation led to questions about the origins and capabilities of their AI model.

This is the picture that is originally from another AI site called Civitai!

This situation was widely reported in the Chinese media at the time. Later it was reported (Link) that the company responded to this incident, stating that its technology SenseMirage includes both SenseTime’s own AIGC big model and it also provides third-party open-source models and user-uploaded local models. This is not a convincing excuse in our opinion. It appears the company tried to explain away the incident, when it was called out by the public and media.

In the Words of Current and Former Employees: Lack of Compelling Technology, and a Toxic Work Culture

Maimai is a very popular employee communication forum (similar to LinkedIn) in China. Sometimes the communication/chat from a company’s current or former employees give a glimpse of the culture of a company’s work environment. A sample of SenseTime’s voices appears below. The consistent feedback from too many employees is that in their view, SenseTime is a smoke and mirrors company lacking both its own compelling technology and a clear management-led direction. Here are a few threads from Maimai about SenseTime.

Q: Is SenseTime in the top level on the Artificial Intelligence sector?

A [from a former SenseTime employee]: [SenseTime] is considered on the top level when using PowerPoint to tell stories.

On November 18, 2022, a person with the tag of being a SenseTime employee stated: SenseTime had already cut 1,000 employees, decreased from over 7,000 to over 6,000 employees and the headcount cut is still in process.

One reviewer of SenseTime states his/her impression that the overall planning of the company is chaotic and directionless.

[The company] does not know to focus its core business. Too many trials resulted in too many failed projects.

[The company] does everything and wants to profit from everything, but it will give up when it finds out it is not easy.

We find similar anonymous comments by current and former employees on Glassdoor ( Link ), and the situation is not improving over time. If anything, the working environment is reported to be worsening more recently.

An Assistant Supply Chain Manager wrote on October 15, 2023, about “layoff and chaos”.

A product manager wrote on February 16, 2023, it’s “hard [for SenseTime] to make profit by product”.

Another Product manager wrote on November 10, 2020 “bad product environment and no guidene [guidance].”

On October 27, 2022, a former director of sales and business development described SenseTime as “early stage with no clear direction to market”.

A research engineer on January 18, 2021, claims the company has “no product”.

Another senior engineer summarizes on August 29, 2023: “low salary poor profitability frequent re-org and layoff”.

On November 17, 2022, an algorithm researcher writes: “Company is not making profit (…) keep changing directions.”

A machine learning engineer complained on November 10, 2022: “No good product and Tech-orientation.”

Even more vocal in Glassdoor reviews are descriptions by many different employees describing a hyper-toxic and exploitative work environment, as well as harassment against non-Chinese employees and underpaid staff. Here are a few instances:

“No job security, disrespectful behavior, and no processes to manage the team or work. Professional harassment is one of the finest qualities at the SenseTime Abu Dhabi Office”.

Threatening everyday environment to fire you if you don’t obey their orders. Make you work on weekends and holidays without any overtime incentive and not even a single appreciation. Even if you have a proven record in previous companies they will make you feel that you are dumb and pathetic for the job so that you work under constant job fear. (…) Don’t mentally and professionally harass your employees who are not Chinese.” ( Link )

“There is no work life balance. Extended working hours, Weekend work, Leaves are not granted. There is no bonus for over working. Any voice raised is answered with termination. (…) it is a very unstable place to work under harassment conditions with a zero job reliability” ( Link )

“Cons: Work and company culture, long working hours, mobbing” ( Link )

“Terrible Cheap Startup trying to be Multinational: cheap pay, terrible benefits, long hours, management are the worst – nepotism is serious” ( Link )

“Management will not bat an eyelid when firing staff even though they have put in a lot of effort.” ( Link )

“Toxic culture: Perform not rewarded. Top down approach. Company culture it’s inside the trash bin. Mico management and picking out needles out for the sake of driving ego-ness.” ( Link )

“A decaying company: working env is becoming harsher” ( Link )

“Long OT time. Very harsh working environment” ( Link )

“Learn things but painful to work up to 16h a day. (…) Snacks are bad. Too long to work. Changing aim. Target not clear.” ( Link )

“bad work life balance” ( Link ) “Internal management is chaotic and there is no room for development.” ( Link )

“Don’t dream about work life balance. Endless work. Need to communicate closely with China company” ( Link )

“Poor work-life balance, impractical workload. Poor mid-level management, under-skill but very confident in their decisions that you must have to follow, a mess of managing the R&D procedures, causing lots of extra workloads” ( Link )

“Cons: Culture, unbelievably long working hours, and substandard staff benefit” ( Link )

“Bad food, low salary. Many Overtime.” ( Link )

“Layoffs & high staff turnover rate” ( Link )

“hard work, bad management, relatively low salary” ( Link )

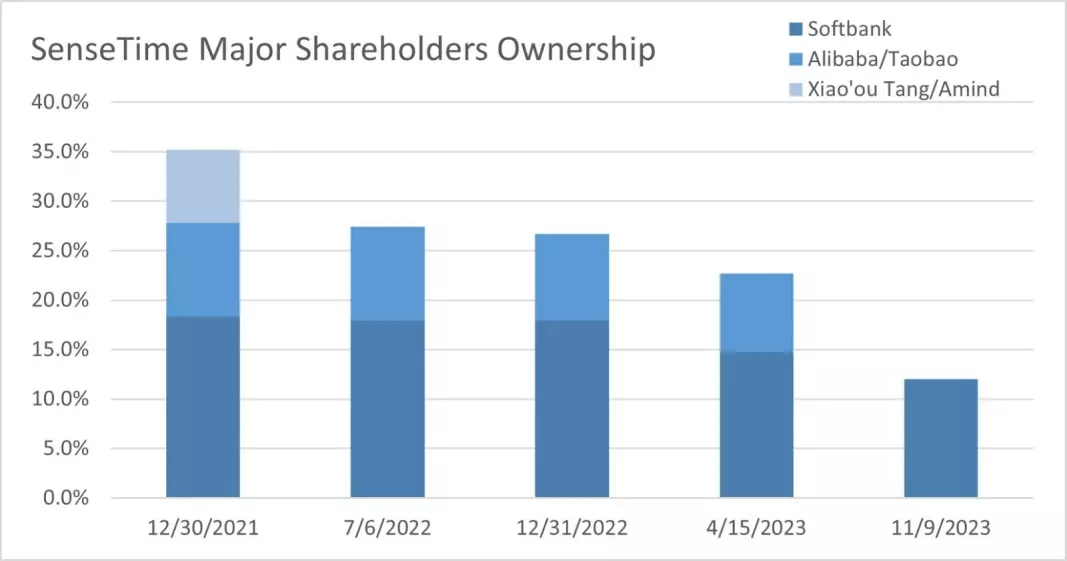

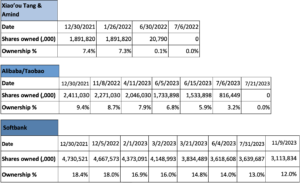

Insiders and Big Shareholders are Dumping Shares

According to the disclosure in the HK Stock Exchange, SenseTime’s controller, Xiao’ou Tang and his holding company Amind disposed of 1.87 billion shares of the company which leaves them without a single share of SenseTime since July 6, 2022.

Starting November 8, 2022, Alibaba began to sell its SenseTime shares. The system shows that Alibaba owned 2.271 billion shares of SenseTime after Alibaba sold 80 million shares at an average price of HKD 1.819. As of June 15, 2023, Alibaba had sold 50 million shares of SenseTime at an average price of HKD 2.267, and owned roughly 1.5 billion shares of SenseTime after the sale, amounting to 5.91% of the total shares outstanding. On July 21, SenseTime issued a PR ( Link ) stating that the company has been informed by Taobao (Alibaba’s subsidiary) “has disposed of all the Class B shares of the Company held by it in an orderly manner, and that as at the date of this announcement, the arrangements for such disposal have been completed.” In other words, Alibaba has sold all its SenseTime shares.

Softbank, an even bigger shareholder than Alibaba, started to sell SenseTime in December 2022. For example, Softbank sold 12.948 million shares at an average price of HKD 1.9769 and it continues to hold 4.67 billion shares after that sale. As recently as July 31, 2023, Softbank sold 14.9 million shares of SenseTime at an average price of HKD 1.7919, and it still holds 3.37 billion shares after the sale, accounting for 12.99% of the total shares outstanding.

The fact that the company’s controller and its two biggest shareholders have either already sold or continue to sell their shares aggressively is not a vote of confidence.

We note that Alibaba and SoftBank were initial investors from prior to SenseTime’s IPO, and also disclosed as engaged in transacting products and services with SenseTime as related parties in IPO disclosures. But transactions with these two giants have dwindled off significantly, while both parties have been relentless sellers of their IPO shares. This demonstrates loss of faith and interest by these large, credible counterparties in SenseTime’s “products” (which, as described above, aren’t really products, and are apparently not very effective “pilot projects”) plus follow-on integration going forward. These giants had much to gain by value-add collaboration, and would know the most about why they bailed.

Smart Money Senses it’s Time to Head for the Exits

Source HKEx News: (Link); FactSet; Grizzly Analysis

Conclusion

We believe SenseTime is operating a fundamentally dead-ended facial recognition software business, plus some additional AI R&D projects with almost no chance of scalable future profits. Political issues severely limit the company’s expansion potential. The Chinese Government is unlikely to award highly profitable contracts to majority foreign owned companies, and Western governments will not entrust sensitive infrastructure data to an entity which is likely compelled to share all data with China State Security Services. This unfortunate position seems to have driven SenseTime to embark down a dark path. We believe all its talk about AI technologies is just that — a smoke and mirrors show to lure in investors. The industry’s most respected experts are setting expectations that there will not be an array of profitable AI engines. The most powerful tools are now open-source. Of course there will be consulting and configuration work to apply them to specific solutions, but pie-in-the-sky valuations for SaaS companies claiming AI engines to be their “holy grail of revenues” will not bear fruit. SenseTime’s financial results already support the unavoidable conclusion that SenseTime’s AI technology is not gaining scalable revenue traction.

Worse yet, the evidence gathered above regarding SenseTime’s revenue fabrication schemes paint an image of deep dishonesty and financial manipulation. Unfortunately for SenseTime, reality seems to be catching up quickly. Caught between its dwindling cash balance and continuously worsening cash flow, with business offerings unlikely to scale to match its SaaS valuation, its largest shareholders clearly Sense it’s Time to leave the premises.