Scarce Flight Activity; Recycled Video material; Misleading DoD Contract; Partners bought with cheap Warrants

- Archer Aviation Inc (ACHR) is an eVTOL company that is seeking to be a leader in urban air mobility. Brought public through a SPAC, we believe the company has made a series of misrepresentations the latest of which being a contract award from the DoD which led a 40% run up in the stock.

- The DoD contracts ACHR received is a noncompetitive award with indefinite quantity and indefinite delivery, meaning the revenue could also be minimal and is also capped at $1.3m total revenue in 2023.

- The latest rise in the stock came after ACHR spun its last earnings announcement, which included the costly settlement of a legal dispute, as a big success: “ACHR secures $215M Investment from Stellantis, Boeing, United Airlines, ARK Invest …”. In reality, ACHR dished out $100M in free warrants for a $12,000,000 investment by Boeing, diluted shareholders by 25%, and must now purchase key tech from a competitor.

- ACHR’s CEO has stated that ACHR is conducting daily test flights, sometimes multiple times per day. ACHR frequently uploads new videos that showcase flight testing.

- Our investigators visited ACHR’s flight testing facilities in early August 2022 and late July 2023. Neighboring businesses and former employees reported seeing only a handful of flights conducted solely for special events, far fewer than the company’s statements claimed.

- Our analysis shows that ACHR is recycling heavily edited videos of their earlier test flights to portray longer flight performance, more frequent testing, and a generally more advanced product than reality.

- ACHR has bought credibility through partnerships with two big companies, United Airlines and Stellantis. In both cases, the company awarded millions of shares for questionable or no compensation. Worse yet, ACHR discreetly amended and/or activated clauses to vest warrants early.

- Archer’s stealthy divorce from one of its founders and co-CEO included accelerated vesting of a huge chunk of insider stock to permit selling sooner (which has commenced), while the circumstances of that breakup have never been fully disclosed for investors to evaluate its materiality.

- During 2022, ACHR announced that their lab and small-scale manufacturing facility in San Jose, CA would be operational by year end. Then the narrative changed to “right around May 2023”. An on-site visit in July found a very incomplete facility, not expected to be operational before October 2023, showing scant signs of anything approaching production readiness.

- ACHR has been spinning a media story that it is rapidly testing and certifying its prototype aircraft for FAA approval.

- As of this report publication date, ACHR only recently received its Special Airworthiness Certificate for its aircraft (non-conforming) Midnight-0 and has plans to start in-air testing only in a few weeks, despite management’s “matter of days” guidance of July 19th. ( Link )

- Even if Archer successfully begins flying Midnight, the path to earning Midnight a Production Certificate required to commence commercial sales seems years away.

- Grizzly consulted with former FAA Certification experts to evaluate the ACHR’s Certification path ahead for its Midnight program, based upon accomplishments so far. The experts we spoke to offered their opinions that for Production Certification (the permit ACHR would need to begin mass-producing aircraft for commercial use), 2028 was a very optimistic estimate and it might well take longer.

- In summary we believe ACHR is another SPAC that achieved a ridiculous valuation through unfounded projections and what we see as clear misrepresentations. Our conclusion is that, as an investment, ACHR seems set up for a metaphoric crash landing.

Background

Founded in 2018, Archer Aviation Inc (ACHR) designs and promises to manufacture an electric vertical take-off and landing (“eVTOL”) aircraft. The company came public through a reverse merger with a SPAC in 2021. Numerous competitors for similar form-factor aircraft appeared in the market prior to Archer’s emergence as a wannabe.

Like many other SPACs, ACHR has from its inception flown high on a vision spun of lofty projections: trillion dollar market-size projections that strain the most optimistic limits of credibility. They’ve indulged in numerous communication stunts involving video editing and recycling, which create misrepresentations. Careful inspection shows a pattern of misrepresentation, behind which is scant sign of operational accomplishment. This company is mostly a smoke-and-mirrors show.

ACHR pushes to be the among the first competitors positioned to bring a fully certified production aircraft (in FAA parlance, earned its “Type Certification”) to market. Through 2022, ACHR and its CEO specifically stated that the company was flying “daily test flights” with their first (non-conforming) prototype Maker (“often multiple flights daily”). It repeatedly uploaded videos of those flights to social media to support the perception of rapid testing progress. We believe management continues to promote its misleading story in social media because it can’t stop baiting investors with images of achieving FAA’s imprimatur well ahead of competition.

All of this is a lie. Ominous clues abound that ACHR’s actual flight path ahead is filled with looming storm clouds and a few brick walls.

This report presents Grizzly’s original on-the-ground due diligence, reported here for the first time. It probes ACHR’s progress toward its publicly stated goal, to be first to market with a commercially viable eVTOL (electric vertical takeoff and landing) aircraft suitable for piloted air taxi use. We cast grave doubt upon ACHR’s declared schedule of gaining this goal in 2024. FAA experts that Grizzly consulted with think 2028 is a more realistic estimate, and the company’s “optimism” has strayed far off course into material misrepresentation.

The only reasonable conclusion when discovering how vast the gap is between the company’s narrative and the hard on-the-ground facts is that ACHR management’s word cannot be trusted. For a development stage company with no revenues or profits, the only premise investors really have for their investment is the CEO’s credibility. In Grizzly’s opinion, based on the information provided by the FAA Certification experts we consulted with, the differences between ACHR’s communications to investors and the actual progress of its prototypes amounts to material misrepresentation.

Flying with the Air Force isn’t the Formation you’d Expect

On July 31st, 2023, Archer announced that they entered multiple contracts with the U.S. Air Force “Worth Up to $142 Million Representing Landmark Investment In eVTOL Technology by U.S. Military”. This news sent the stock to recent highs with an increase of more than 40% in the same day, spun up by momentum traders on over 40 million shares — 6 to 8 times daily average volume.

At least one of the contracts that Archer signed was awarded on July 27th, 2023 as a Small Business Innovative Research (SBIR) Phase III at a firm-fixed-price of $110,000,000 for “Midnight Based Advanced Vertical Lift”.

As usual, we believe the company communications have been placed squarely between opaque and misleading, and left out key information about the contract that seriously reduces the impact on the business as perceived by investors.

In short, nobody cared, until Archer’s PR and subsequent news reporting on the 31st caused the stock to take off, adding $500 million in market cap in one day. Note:

- SBIR Phase III are always by definition noncompetitive and nonbinding. The government issues large numbers of these periodically.

- This contract is also indefinite quantity and indefinite delivery, which could also mean that the DoD is not obligated to buy anything from Archer.

- Joby is also miles ahead by getting actual firm orders from the DOD, not the indefinite delivery boilerplate that might yield no revenue and is not a firm commitment. Joby is set to deliver two production aircrafts to the Air Force next year. ( Link ) Archer has nothing to deliver other than a non-conforming, untested unit. The DoD is also actually having manned flights with Air Force pilots and has already flown Joby aircraft. ACHR has never conducted even a single manned test flight on any of its aircrafts.

- ACHR’s press release seems hugely misleading given the above points. This contract is for a narrowly defined services and technology transfer, not large scale purchase of aircraft.

This SBIR Phase III contract, by definition, refers to work that derives from, extends, or completes an effort made under prior SBIR/STTR funding agreements, but is funded by sources other than the SBIR/STTR program. We checked the past projects under this program that Archer describes in its press release as “since 2021 on a series of projects through the Air Force’s AFWERX program with the goal of helping the AFWERX Agility Prime program assess the transformational potential of the vertical flight market and eVTOL technologies for DoD purposes”.

Moreover, that contract will be subject to milestones and achievements, with work that will be performed in San Jose, California, and is expected to be completed by July 31, 2028. In addition, it is indicated by the Air Force that for 2023, research, development, test, and evaluation funds in the amount of $1,293,077 are being obligated at time of award only. Note that this contract is for a narrowly defined services and technology transfer, not large-scale purchase of aircraft. The headline and language of ACHR’s PR create the appearance that ACHR is selling six aircraft to the Air Force for $142 million. The technology transfer and services committed in this contract are for a value up to $110 million. Our best understanding of the actual language of the award is: the Air Force has an option to buy up to 6 aircraft from ACHR, for the purpose of testing the technology being transferred, which would add the $32 million to get to the $142 million total.

Of the $110 million for services and technology, only $1.3 million is allotted for the balance of 2023, leaves $108.7 million disbursed over 5 years, (an average of $21.7 million per year if prorated, but the actual rate of expense is at the Air Force’s option) It is the option of the Air Force to determine how rapidly to draw down these services. It’s a nice plum, but hardly transformational.

Surprisingly, we found that the few Phase I and Phase II awards that Archer received were solely aimed at narrow aspects of their aircraft technology, in contrast to the award received by Joby, which was aimed at its whole aircraft “Electric Air Vehicle for Logistical Support”. Moreover, Joby has been a pioneer in the Air Force collaboration and has already had Air Force pilots flying their aircraft in the current year.

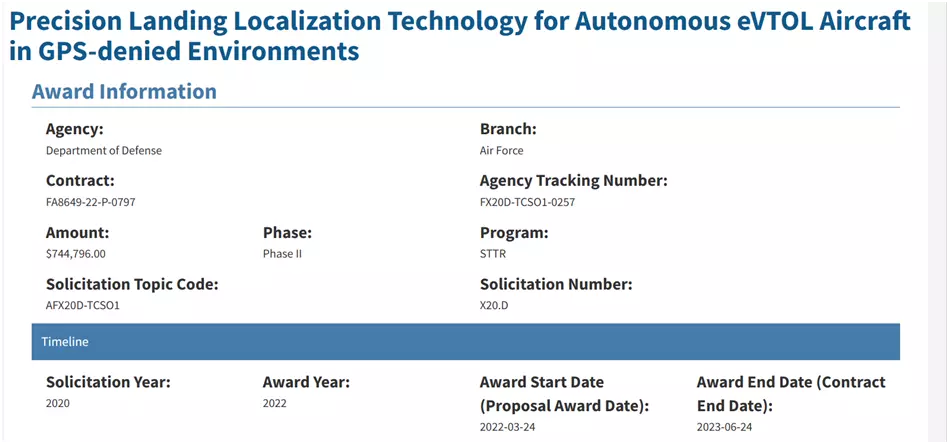

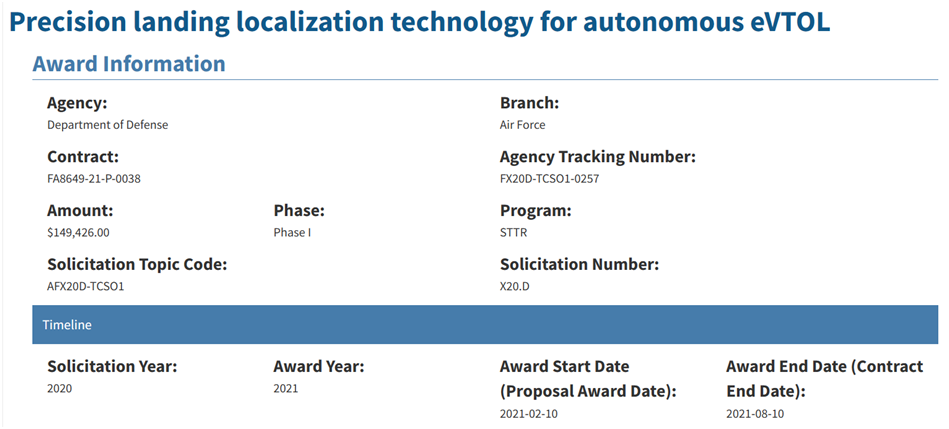

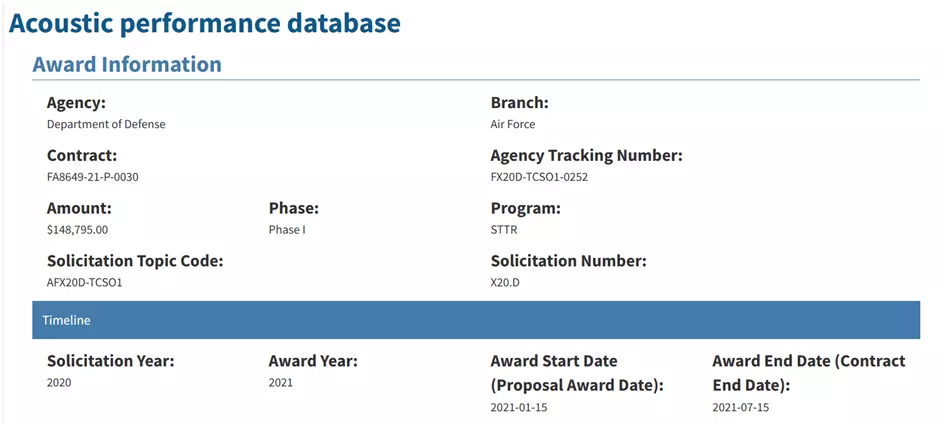

Archer was granted Phase I awards for the development of its “Precision Landing Localization Technology for Autonomous eVTOL” and “Acoustic Performance Database” in 2021. The following year, the company received a Phase II award to further develop its “Precision Landing Localization Technology for Autonomous eVTOL in GPS-denied Environments” where the goal was to “refine the vision-based navigation concept, develop a hardware prototype system and finally conduct flight tests with the prototype system on Archer’s full-scale Maker eVTOL vehicle.”

Note: Only Phase II Award that the company received.

Note: One of the two Phase I Awards that the company received.

Note: One of the two Phase I Awards that the company received.

In the more informative contracts press release from the Air Force, we found that the goal of that Phase III contract is to “iteratively conduct government operational experimentation on military installation for government-owned, government-operated flight operations to execute and experiment with key missions or mission elements to substantiate government use cases, concept of operations/mission design, and cost/benefit analyses of the Midnight aircraft that extend, derive, and complete previously awarded SBIR Phase I and II efforts.” That is what $110 million of the $142 million will be expended on.

In other words, these new contracts indicate an interest of the Air Force in some aspects of Archer’s technology in development, but do not seem yet to constitute a spelled out opportunity to sell any additional aircraft to the DoD in the future.

ACHR’s press release ends with this statement:

“The views expressed are those of the author and do not necessarily reflect the official policy or position of the Department of the Air Force, the Department of Defense, or the U.S. government.”

Moreover, in their last quarterly earnings press release published on August 10th, 2023 and the following earnings call, management announced that the company expects to deliver a non-conforming unit to the Air Force in Q4 2023 or early next year. First, this first delivery was inevitable as the Air Force needs an actual eVTOL to test its technology, it does not grant the company follow-on deliveries. Second, the delivery of a non-conforming aircraft substantially reduces the economic outlook of the sale. Third, this strengthens our belief that the Air Force is only interested in some aspects of the technology, and not in the aircraft itself, as at the time they will receive the first one, Archer would’ve barely or not even entered in the “real flights” part of its unmanned testing. This perfectly corroborates with what the Air Force has been contracting for in its “collaboration” with Archer, the technology.

Important Note Settlement Risk:

It is impossible to evaluate the future year revenues of this contract. While the lawsuit “Wisk Aero vs Archer Aviation” finally settled, Archer is now exclusively sourcing its autonomy technology from Wisk. In other words, if the Air Force is considering operating their aircrafts autonomously or is interested in that side of the technology, the IP is not held by Archer, placing the economic substance of the contracts in severe jeopardy.

Archer’s Communications About its Partnerships with Big Industry Companies Suggest a Bright Future, But we Believe the Win is Only One-Sided

The Last Quarter: Headline is a Winner, Reality Looks Dimmer

Following a long and expensive legal battle, Archer and Wisk, a Boeing company, finally reached a settlement announced jointly by both companies on August 10th, 2023. They also added that:

“the parties have entered into a collaboration that looks forward to the growth and development of the AAM industry. Archer has agreed to make Wisk its exclusive provider of autonomy technology for future variants of Archer’s aircraft. ”

To top it off, Boeing is also participating in Archer’s latest $215M funding round, alongside Stellantis, United and ARK Invest. All this was proudly announced in Archer’s last quarterly earnings release on August 10th. But looking closely at the matter, it appears that Archer simply accepted its defeat and found a way to sneakily compensate Wisk.

First of all, Archer announced in the separate 8-K filing that upon the closing of the Private Placement, they would issue Wisk a warrant to purchase up to 13,176,895 shares of Common Stock with an exercise price of $0.01 per share. At the time of issuance, this amounts to $73,000,000, which is close to what was left after deducting the investment amounts disclosed for some of the other participants in this Private Placement (Stellantis $70,000,000, United $25,000,000, Ark Invest $44,000,000, leaving $76,000,000 between the undisclosed Ken Moelis and Boeing investments, the only disclosed names prior to the newly filed S-3). However, it appears that Boeing only invested a measly $7,000,000 in Archer, and received close to 10 times its investment in free shares. In other words, besides the high-single digit discount provided to them via this Private Placement, Wisk/Boeing is also getting a gigantic amount of free shares, all of which will be fully vested in the next 6 months, while 4,512,636 were immediately vested. To us, this simply looks like a very expensive settlement for Archer and a big win for Boeing/Wisk.

If that was not already enough, it was specified by the company that if the value of the shares underlying the First Boeing Investment and the Initial Vested Share Tranche, plus any shares that become vested pursuant to the Second Tranche, have a combined value of less than a certain amount specified in the Agreement on the Specified Date, Archer will be required to pay the balance, if any, in cash. In other words, this is clearly a disguised settlement payment from Archer.

We then noticed another paragraph below:

“In addition, at the Company’s election, Boeing has agreed to participate in a subsequent private placement of equity or equity-linked securities by the Company, if any, that occurs on or prior to the Specified Date (the “Second Boeing Investment”). Concurrently with the closing of the Second Boeing Investment, the Company would issue to Wisk a warrant to purchase a certain number of shares of Common Stock at an exercise price of $0.01 per share, in connection with Wisk’s autonomy insertion services into the Company’s aircraft.”

Unsurprisingly, Archer found another way to distract attention from the full compensation attributed to Wisk/Boeing. In the “Form of Registration Rights Agreement” included in the 8-K, we found that Archer is going to issue Wisk/Boeing even more warrants, as shown in this paragraph:

“(the “Second PIPE Financing”), up to such number of shares of Class A Common Stock with a fair value of $5,000,000 and (z) if the Company consummates the Second PIPE Financing, up to such number of shares of Class A Common Stock with a fair value of $15,000,000 pursuant to a warrant to purchase shares of Class A Common Stock to be issued to Boeing on the closing date of the Second PIPE Financing with an exercise price of $0.01 per share (all such issuances, the “Boeing Issuances”)”.

In other words, Boeing will receive an extra $15,000,000 worth of free shares for an additional $5,000,000 investment in a Second PIPE.

Once again, this situation, while being clearly a win for Wisk in all aspects, is being spun by Archer to appear as a fair and equal collaboration agreement. And once again, Archer is heavily diluting its investors to stay afloat.

The fact that Archer will now exclusively source its autonomous technology from Wisk could also imply that Archer did not either hold the Intellectual Property for it they claimed, or could not develop a reliable technology by themselves.

We strongly encourage investors to read the press release issued by Archer for its quarterly earnings release, and compare it to this section to measure how misleading and incomplete their communication strategy was.

Below is a table summarizing the current and future capital structure with regard to this new investment:

And if that’s not bad enough, they’re being two-timed — this alpha Drake has been courting another hen

ACHR has also been frequently and proudly name-dropping its two most prominent partnerships with United Airlines and Stellantis, as these are undoubtedly essential to the company’s credibility in this new sector. The company has been releasing press releases, videos and posts on social media about these partnerships, and even held or participated in events alongside some executives from both partnered companies. Similar to Wisk and Boeing, Archer has been trying to tell the story to investors that both sides are profiting from their relationships. But the reality is drastically different. It appears that Archer has been discreetly diluting investors to please both partners with tens of millions of free shares while releasing those shares from their vesting milestone schedule, and freeing the counterparty from its obligations along with that release.

Indeed, we found that the company used various stealthy night moves to activate agreement clauses, vesting and exercising more than 90% of all the warrants and free shares tied to its commercial success. The latest one happened on the exact day after ACHR’s stock jumped from $1.77 on April 25th, 2023 (or we can consider the low of $2.78 in June 2nd, 2023) and jumped to $4.89 on July 5th, 2023 and $6.87 on August 1st. In other words, both partners conveniently got all their free shares vested and exercisable already, and do not have remaining obligations to wait/help ACHR until it finally reaches commercial success.

To us, this is a big red flag, showing how the company is at the mercy of their partners which are the sole reason why they are maintaining their credibility, for now.

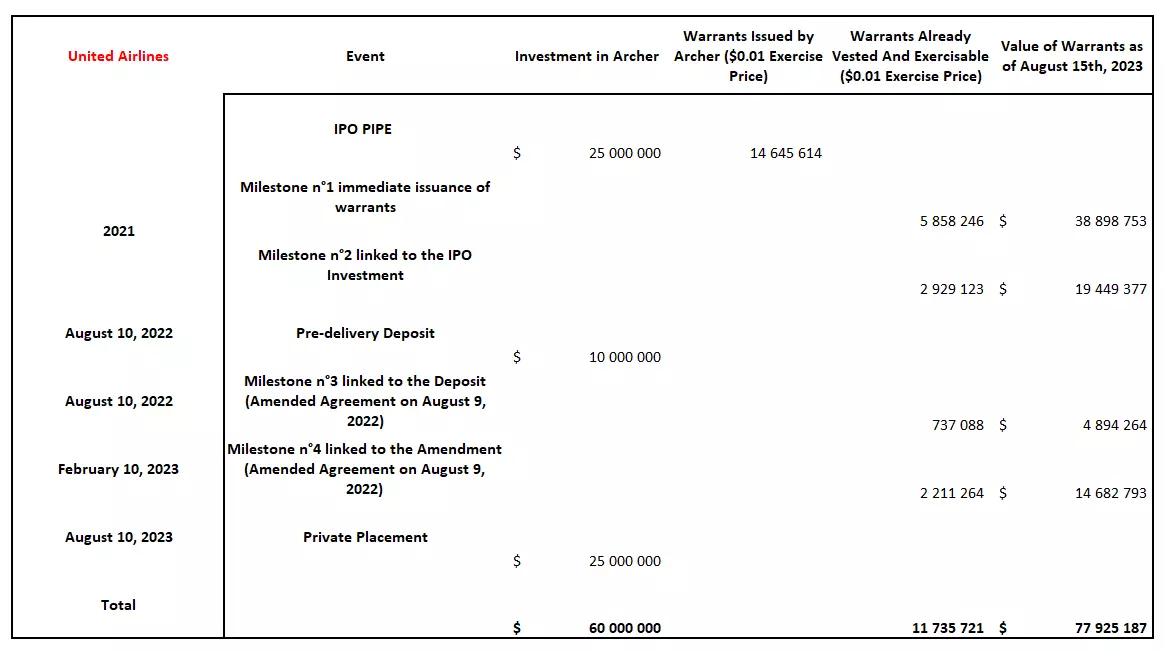

Last year, the company proudly announced the receipt of a $10 million pre-delivery payment by United for the first 100 eVTOLs to be produced. This was highlighted by the company as a major achievement, as, according to them, it shows how much confidence United Airlines has in ACHR. But the fine print of these written agreements tells a different story. United Airlines got a juicy reward for lending its name to ACHR.

As shown on the screenshot of the company’s website frontpage from September 2022, and on most of the company’s presentations almost a year later, the United Airlines partnership is one of the things that investors are most excited about. Indeed, the commercial partnership, along with a sizable purchase agreement for 200 eVTOLs with an estimated revenue of $1 billion, as well as an option to buy an additional 100 aircraft has been touted countless times by the company.

First, it is important to note that United Airlines is currently the first and unique ACHR “beta” customer, and also one of their shareholders. Upon signing the purchase agreement, “Archer issued 14,645,614 warrants to United Airlines to purchase shares of the Company’s common stock. “Each warrant provides United with the right to purchase one share of our Class A common stock at an exercise price of $0.01 per share.”

The warrants were granted with vesting in four equal installments in accordance with the following milestones:

- the execution of the Purchase and United Collaboration Agreements,

- completion of the Business Combination,

- the certification of the aircraft by the FAA, and

- the initial sale of aircraft to United.

At the time of issuance, the Company’s common stock price valuation, which was performed by itself, was at $13.35 which gives a total value of the warrants of approximately $196 million, or around 20% of the projected revenue of the total purchase agreement. At the current stock price, this is worth just below $100 million.

In a correspondence with the SEC dating back to July 2021, Archer confessed that they issued these warrants “to induce United to commit to a contingent purchase agreement for a new type of commercially viable aircraft from Archer, which provides valuable credibility to Archer to have such a prestigious customer and helps Archer achieve the announced merger with Atlas”, while for United Airlines, it was simply “to partner with an eVTOL company as part of its broader effort to invest in emerging technologies that reduce carbon emissions from air travel”.

Note that United has been partnering with numerous other aircraft companies in multiple different sectors as well. In other words, Archer gave United an opportunity, among others that United gladly took, to get some exposure in the eVTOL industry, while taking close to no risk and making profit from the millions of warrants. We believe that without such generous incentives, Archer would not have been able to get any credibility organically.

In particular, Grizzly notes United’s partnership with Eve Air Mobility ( Link ) , a division of Embraer, a highly successful Brazil-based commercial and business aircraft manufacturer, whose planes (close to 1000 in 2020) have been purchased and placed into service by many U.S. airlines. Clearly Eve Air Mobility does not need an auto manufacturer as a “partner” … they have a major aircraft manufacturer as a parent. But we digress…

After its business combination and IPO, Archer had already vested 8,787,369 warrants, completing the first two milestones. The two last vesting milestones were directly tied to Archer’s ability to achieve its final aircraft Type Certification by the FAA and its ability to manufacture and deliver the aircraft to United.

On August 10, 2022, ACHR announced the receipt of the $10 million pre-delivery payment from United Airlines. This announcement was well received by ACHR’s investor base and offered respite following a consistent decline in the stock throughout the year. But we believe this announcement was just another head fake from ACHR to fool its investors.

Indeed, one day prior to the announcement, on August 9th 2022, the company had without fanfare amended its warrant vesting terms with United as follows:

“1. Amendment to Exhibit B, Vesting Terms. Pursuant to the “Vesting Terms” contained in Exhibit B to the Warrant, Milestone IV applies to 4,422,529 Shares underlying the unvested portion of the Warrant, of which 884,506 Shares (the “Mesa Shares”) are reserved for and subject to deduction from the Warrant in the event certain warrants are issued to Mesa Airlines, Inc. (“Mesa”) pursuant to the Assignment and Assumption Agreement by and among Mesa, United Airlines, Inc., Mesa Air Group, Inc., and the Company dated February 26, 2021 (the “Assignment Agreement”), and Milestone IV shall be amended and restated to read in its entirety as follows:

- “A. PDP Advance Payment: Of the remaining 4,422,529 Shares (collectively, the “Condition IV Shares”) underlying the unvested portion of the Warrant, the Warrant shall vest and become exercisable with respect to 737,088 Shares (the “Bucket A Shares”) upon the payment by United to the Company of $10,000,000 in accordance with the proviso set forth in Section 5.2 of the Purchase Agreement (as amended by Amendment 1 thereto);

- B. Route Collaboration Agreement: The Warrant shall vest and become exercisable with respect to 2,211,264 Shares of the Condition IV Shares (the “Bucket B Shares”) upon the six-month anniversary of the Amendment Effective Date, during which six-month period the parties intend to negotiate toward the completion and effectiveness of a comprehensive collaboration agreement pertaining to the Company’s aircraft route development, site selection and related logistics.

- C. Acceptance and Delivery of Firm Aircraft: The Warrant with respect to 589,671 Shares of the Condition IV Shares (the “Bucket C Shares”) shall vest and become exercisable as follows: 1/160th (or 3,685.45) of the Bucket C Shares shall vest and become exercisable upon the acceptance of delivery and final purchase by United (or its nominee as permitted under the Purchase Agreement) of each Firm Aircraft (as defined in the Purchase Agreement) as set forth in the Purchase Agreement; provided, however, that notwithstanding the foregoing, if the Company is unable to deliver all Firm Aircraft on the date agreed pursuant to the Purchase Agreement (the “Outside Delivery Date”), and (x) either of the Purchase Agreement or the Collaboration Agreement is still in full force and effect, or (y) either such agreement is no longer in full force and effect due to the Company’s uncured material breach, then the Warrant as to all such remaining unvested Bucket C Shares underlying the Warrant as of such date shall automatically vest and become exercisable upon such Outside Delivery Date.

- D. Acceptance and Delivery of Firm Aircraft on United Purchase Option Exercise: If United elects to exercise a United Purchase Option with respect to any Mesa Aircraft pursuant to Section 2.01(c) of the Assignment Agreement, the Warrant with respect to 884,506 shares (the “Bucket D Shares”) shall vest and become exercisable as follows: 1/40th of the Bucket D Shares (or 22,112.65 shares) underlying the Warrant shall vest and become exercisable by United upon the acceptance of delivery and final purchase by United (or its nominee as permitted under the Purchase Agreement) of each such Mesa Aircraft.”

In other words, Archer amended its warrant vesting terms effective ONE DAY before United Airlines announced its $10 million pre-payment for the first 100 aircraft, who thereafter immediately received 737,088 shares (around $3.2 million as of August 9th, 2022) after its pre-payment and received an extra 2,211,264 shares after 6 months (now totaling close to $20 million at ACHR latest opening price), where “the parties intend to negotiate toward the completion and effectiveness of a comprehensive collaboration agreement pertaining to the Company’s aircraft route development, site selection and related logistics.”

Following this amendment, United Airlines does not need to wait until Archer successfully enters commercialization and delivers the aircrafts, as only fewer than 1.5 million free shares out of the initial 4.4 million are now still contingent upon that milestone.

The only winner we see in this purchase agreement, even after the pre-delivery payment, is United Airlines. United Airlines was basically given millions of free shares (11,735,721 shares have been vested as of today, worth over $78 million at latest opening price) to place an order in exchange for a token $10,000,000 prepayment, subject to several important conditions and requirements, such as “further negotiation and reaching of mutual agreement on certain material terms related to the purchases” that are still to be determined and unknown to investors.

In their most recent earnings call, management stated that:

“As we progress further through the aircraft certification program, we expect that we will agree upon and receive additional pre delivery payments from United. Beyond these previously announced arrangements, Stellantis and United remain committed to helping Archer get to commercial operations in 2025. We are very fortunate to have the continued support of these 2 strategic partners and investors.”

We wonder what other magic Archer will use to incentivize United sufficient to earn more pre-delivery payments, which will most probably not happen out of thin air, and how much more dilution the company will place upon its shareholders.

If ACHR gets more “good news” to show its investors and its stock price increases, United Airlines will profit from this increase through its millions of shares. On the other hand, if ACHR fails to fully develop its eVTOL, United has no liabilities to ACHR, and will still be able to profit from its millions of shares on the way down. Note that United’s $10 million pre-payment will be refunded in full if ACHR never delivers any aircraft. We believe ACHR signed a ridiculous purchase agreement with United Airlines to keep its investors excited by the prestige of United’s name, but adding risks only on its own side.

Finally, ACHR and United announced a “route collaboration” agreement on March 23, 2023 about “the next point to point route” from downtown Chicago to O’Hare. ( Link ) No announcement from Archer when United and Eve Air Mobility partnered up on the route from downtown San Francisco to SFO International on June 14, 2023 … ( Link )

But when you’re the one “paying for your partnership”, you may find that your partner thinks it’s a non-exclusive arrangement.

Partnership with Stellantis is also Paid For with Stock

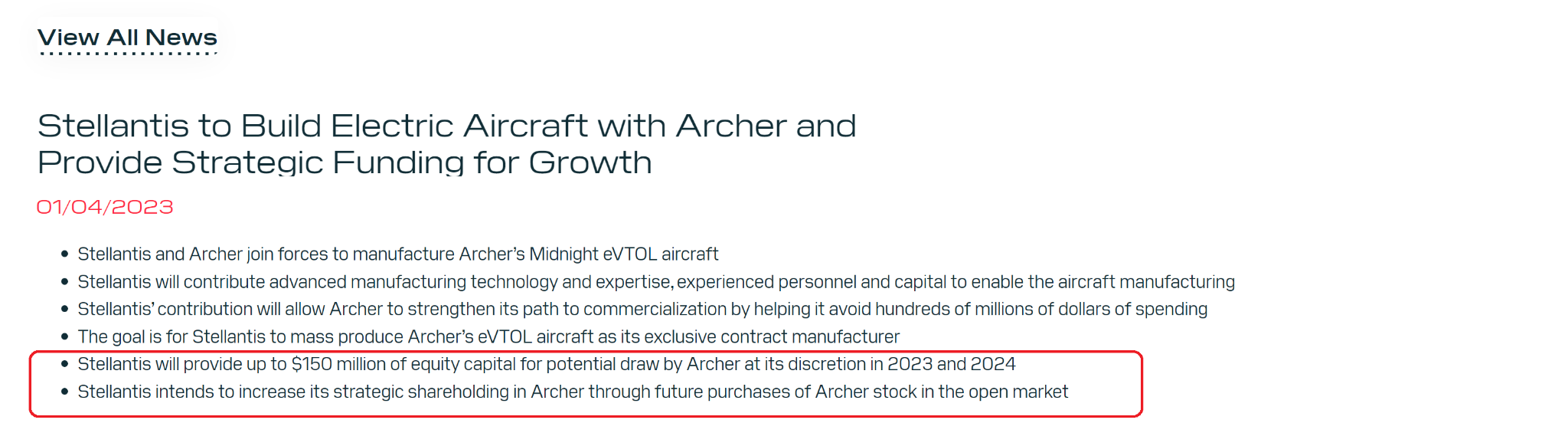

We find a similar dynamic with the more recent highly touted partnership with Stellantis. Indeed, on January 4, 2023, Archer announced its deeper collaboration with the company:

In their Q1 2023 earnings call, the company stated:

“Stellantis initially became an investor in Archer in 2021. And as part of the recent expansion of our strategic relationship in addition to our manufacturing partnership, they have committed up to an additional $150 million in equity capital for Archer to draw upon at our option between now and the end of 2024.”

However, when looking deeper into the agreements, we find that Archer submitted an equity line of up to $150,000,000 worth of stocks at a 10% discount with high contingency milestones. The colorful feathers of this deal portray not just passing interest, but Stellantis’ deep involvement with Archer. But under the feathers, they only had to buy $25 million worth of stock at a discount as the other $125 million are contingent upon milestones linked to the ACHR obtaining its Airworthiness Certificate for their final conforming aircraft Midnight and the full transition flight of their non-conforming or conforming version, which, if it happens, would be much later next year. We found the management quote to be misleading, as Archer did not have the option to draw upon that equity capital for a rather long period.

First, the company changed its speech, as in their earnings call from the Q4 2022, management said:

“The remaining balance is available over 2 tranches of $70 million and $55 million based on achieving certain business milestones, which we expect to occur in 2023. This construct allows us to be opportunistic to draw on that capital, if needed, but also allows us to do so by taking market conditions into account.”

We believe this to be completely delusional. The milestone tied to the Airworthiness Certificate did not involve its non-conforming aircraft but its final “Type Certification” Midnight aircraft as described in the filing: “Midnight” means the Company’s planned production eVTOL aircraft referred to as “Midnight” or “Midnight-1” by the Company, and “M001” by the FAA.” This aircraft is promised to be assembled by the end of this year, thus, it is a long way from receiving its Airworthiness Certificate.

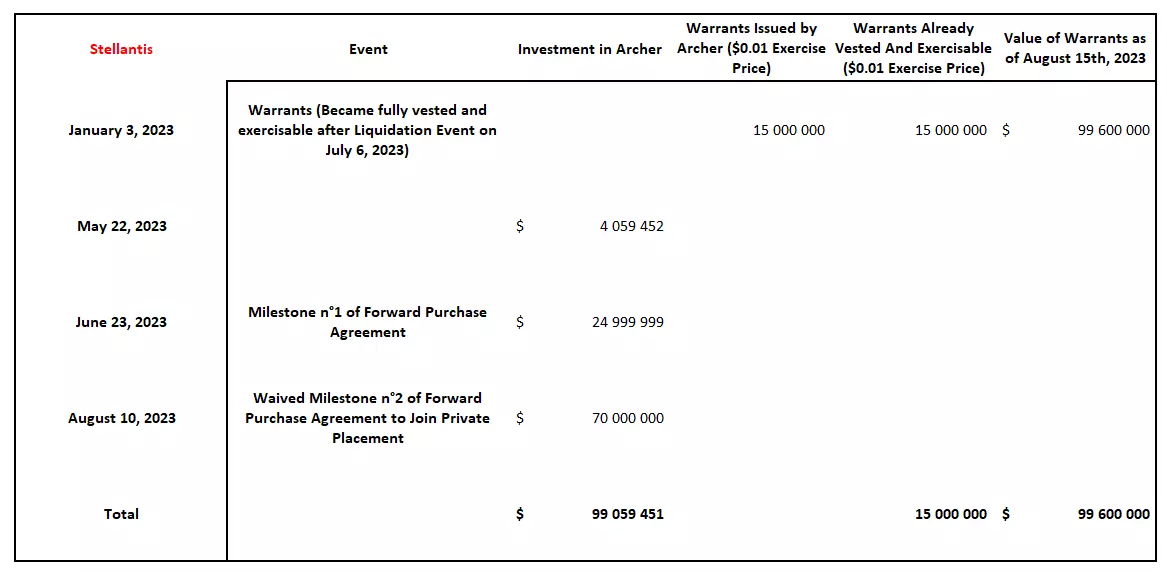

Stellantis had to waive this milestone in order to participate in the latest financing round. We believe the language that Archer uses implies that milestones have once again been shifted, because the previous milestones like Air Worthiness for the conforming aircraft seem utterly unachievable within 2023. We suspect that Stellantis was only willing to commit to further financing because they just received the 15,000,000 warrants from Archer as we explain later in this section.

The other milestone is based on the company’s ability to conduct a “Full Transition to Wing-Borne Flight with respect to either Midnight-0 (non-conforming) or Midnight (conforming)”. As a reminder, it took Archer a full year to take Maker from hover to full transition flight as stated in their Q4 2022 earnings call. At the moment, we are still waiting for Midnight-0 to simply take off. Therefore, we highly doubt that the company gets access to the rest of this capital anytime soon. Moreover, the agreement has multiple other clauses that could prevent Archer from drawing this equity capital at all. The only positive point is some minor balance sheet relief for investors before the next dilution wave.

Moreover, the sentence “Stellantis initially became an investor in Archer in 2021” is misleading, as well. Indeed, the company received millions of free shares from two manufacturing agreements with their subsidiaries in Italy and in the US, for simple consulting projects on designing parts. This marks the beginning of Archer heavily incentivizing Stellantis.

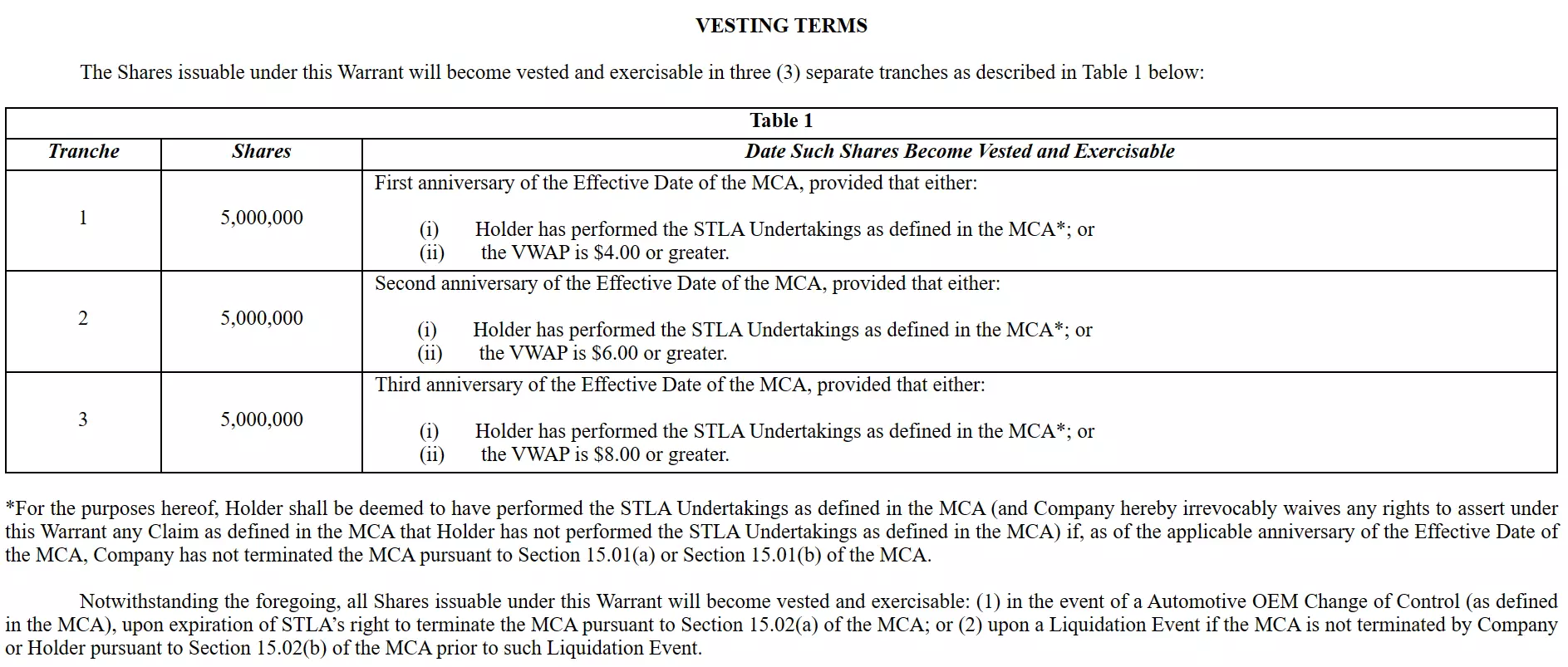

Besides this equity line, Archer provided Stellantis with 15,000,000 additional $0.01 shares vested upon very vague milestones, and appears to have purposely activated one of the clauses of the agreement under which all the shares should immediately be vested and exercisable, way before investors would have assumed.

Indeed, here is a screenshot of the “Warrant to Purchase Shares” documents, showing the vesting milestones for the warrants:

Note the last sentence visible on the screenshot: “Notwithstanding the foregoing, all Shares issuable under this Warrant will become vested and exercisable: (1) in the event of a Automotive OEM Change of Control (as defined in the MCA), upon expiration of STLA’s right to terminate the MCA pursuant to Section 15.02(a) of the MCA; or (2) upon a Liquidation Event if the MCA is not terminated by Company or Holder pursuant to Section 15.02(b) of the MCA prior to such Liquidation Event.”

One of the liquidation events description is:

“(iii) the consummation of any transaction (including, without limitation, any merger or consolidation) the result of which is that any “person” becomes the “beneficial owner” directly or indirectly, of more than 50% of the Voting Shares of the Company (measured by voting power rather than number of shares) provided that for the purposes of this clause (iii), any outstanding shares of the Company’s Class B Common Stock shall be treated as shares of Common Stock on an as-converted basis and no effect shall be given to the voting power of outstanding shares of the Company’s Class B Common Stock in excess of the voting power of such Common Stock”.

Surprisingly, on July 6th, 2023, Adam Goldstein, Founder, Chief Executive Officer and Director of Archer Aviation Inc. (the “Company”), became the beneficial owner of approximately 50.1% of the total voting power of the Company’s outstanding capital stock as of July 6, 2023. Mr. Goldstein’s voting power increased to over 50% of the total voting power of the Company as a result of sales and/or transfers by other stockholders of the Company’s Class B common stock”.

This happened right after a big stock price pump, where the stock rebirthed from $1.77 on April 25th, 2023 (or we can consider the low of $2.78 in June 2nd, 2023) and jumped to $4.89 on July 5th, 2023, one day before the warrants were miraculously vested under the liquidation event.

In other words, Archer deliberately gave Stellantis all the free shares that were linked to their performance regarding the “Manufacturing Collaboration Agreement”, where none of those free shares should have been vested as of today, right after its stock price quadrupled in less than four months. Moreover, the latest clause of the agreement stipulates that “In no event will termination of the MCA for any reason have any effect on Shares issuable under this Warrant that have become vested and exercisable on or prior to the date of such termination” meaning that Stellantis now holds 15,000,000 shares for free and does not have any obligation to perform according to the agreement anymore.

In conclusion, we see Archer discreetly pleasing its “very much needed to stay credible” “partner” companies at the expense of its own shareholders. Such accommodating behavior only shows that Archer is signing partnerships solely because it gives millions of free shares at the demand of such companies, and could not negotiate to commit these partners organically.

We want to end this section with a funny quote from management during the company’s Q1 2023 earnings call:

“As you can see, we are being very thoughtful about how we manage our liquidity and potential shareholder dilution.”

Note: This does not include the 15,000,000+ exercisable $0.01 warrants that Stellantis possesses.

Co-founder Ducks Out the Back

ACHR underwent a sudden rupture in the relationship amongst its two founders, college friends, we’re told. Of course, investors will never benefit by knowing “the real story” about this fact materially affecting their investment. We do know there was significant legal effort made to avoid the appearance of conflict, as reflected in a huge tranche of founder’s shares forfeited, and a much larger portion being assigned accelerated vesting with the stroke of a pen.

A couple of months later, this bromance was over, and Adcock was selling his Founders shares hand over fist. What happened? ( Video Link )

The disaffected founder, Brett Adcock, recently (end of May thru end of June, 2023) sold a large tranche (over 14 million shares) at approximately $3.00 to $4.80 per share ( Link ) We are left wondering if Adcock’s abrupt departure from his previously close buddy on the ACHR gravy train was due to tensions over the strategic “bet the farm” direction Adam Goldstein has taken in defending Wisk Aero vs Archer Aviation.

No discussion of dilution can be complete without mentioning Marc Lore, who appears in ACHR’s recent filings as holding 28,086,358 shares, appx 15.2% of ACHR’s common stock, by far the largest individual shareholder, except for CEO Goldstein. (Note that Goldstein’s voting control is absolute, by virtue of his holdings of Class B shares with 10x voting rights.) Lore owns the Minnesota Timberwolves and is an experienced entrepreneur. Potential momentum traders in ACHR must wonder if they’re buying Lore’s shares in the market. Once he evaluates the reputational risk this position might represent, his change of heart would inflict enormous de facto dilution for shareholders.

Is Archer Flying Its Prototypes Intensely, as they Claim, or Are They Only Coming Out For The Show?

Aggressive Video Editing and Reposting to Fool Investors;

but ACHR Can’t Earn FAA Certification from Videos

The first and biggest red flag we encountered, when starting our investigation, was how Archer is using heavily edited and recycled promotional videos to portray a very active flight test campaign and operational progress. Indeed, the eVTOL developer is promoting itself on Instagram, TikTok, YouTube, and many other platforms where they frequently post videos and images. The company posts a wide range of content documenting its operations including Midnight showcase and events, employee stories, Maker test flight videos, as well as “behind the scenes” videos of the “control unit” interior, aircraft manufacturing and data analysis by engineers.

Such marketing is not uncommon and can be a positive way to update investors about corporate developments and technological, operational progress. However, in ACHR’s case, we found the company has been aggressively manipulating and editing media content to portray a story which misrepresents the actual activity and progress at the company.

One way in which ACHR manipulates its content is through the recycling of clips and images which are often completely unchanged from previous versions, in some instances more than a year after it was shot. The company simply modifies colors and adds visual effects to give viewers the impression that the content is new and/or different. While acceptable in some cases, several examples point out that ACHR has not employed this practice innocently. In the current state of the eVTOL industry, showing technological progress and achievements – especially through test flights – is crucial to keep investors interested and portray progress.

The most recent videos posted by the company showing Maker flying does not break the rule. Indeed, Archer has recently been heavily communicating regarding President Joe Biden’s Federal AAM Interagency Working Group visit at their Flight Test Facility. The company published a video where they show members of the group looking around the facility. The Midnight prototype was prominently displayed, as it could not fly at the time. Later on, a purported flight demonstration of Maker was conducted. We are really dubious of that flight demonstration. Indeed, we found that ACHR has been recycling its old footage, adding some filters to it and splicing it into the recent event video to make investors believe there was an extensive flight demonstration that day.

Below are two screenshots comparing the images from the recent event from July 3rd, 2023 and the “Phase Three of Flight Test Program” video from October 31st, 2022.

Note: This video was published on July 3rd, 2023. (Biden’s group visit)

Note: This video was published on October 31st, 2022.

To us, this raises serious doubts about the capabilities and flight frequency of ACHR’s older prototype Maker. There is simply no logical reason why the company did not film its flight demonstration for the interagency working group, except it couldn’t go that day, or would have made an unimpressive demo for other reasons.

But this example is only the most recent. Indeed, we compiled multiple instances of ACHR re-using its old footage by modifying their aspect. Below are a few more examples:

Note: This video was published on December 20th, 2021.

Note: This video was published on August 17th, 2022.

Note: This video was published on December 7th, 2021.

Note: This video was published on August 17th, 2022.

Time expansion or miraculous weather change?

In another video, the company tried to combine videos from several days into one with seamless transitions. However, one detail caught our attention: in one frame, the sky is cloudy and then suddenly becomes totally clear in the next instant. While this video is a “recap”, ACHR is using this technique to make the maneuvers and flight seem longer than it actually is.

Astonishing weather change?

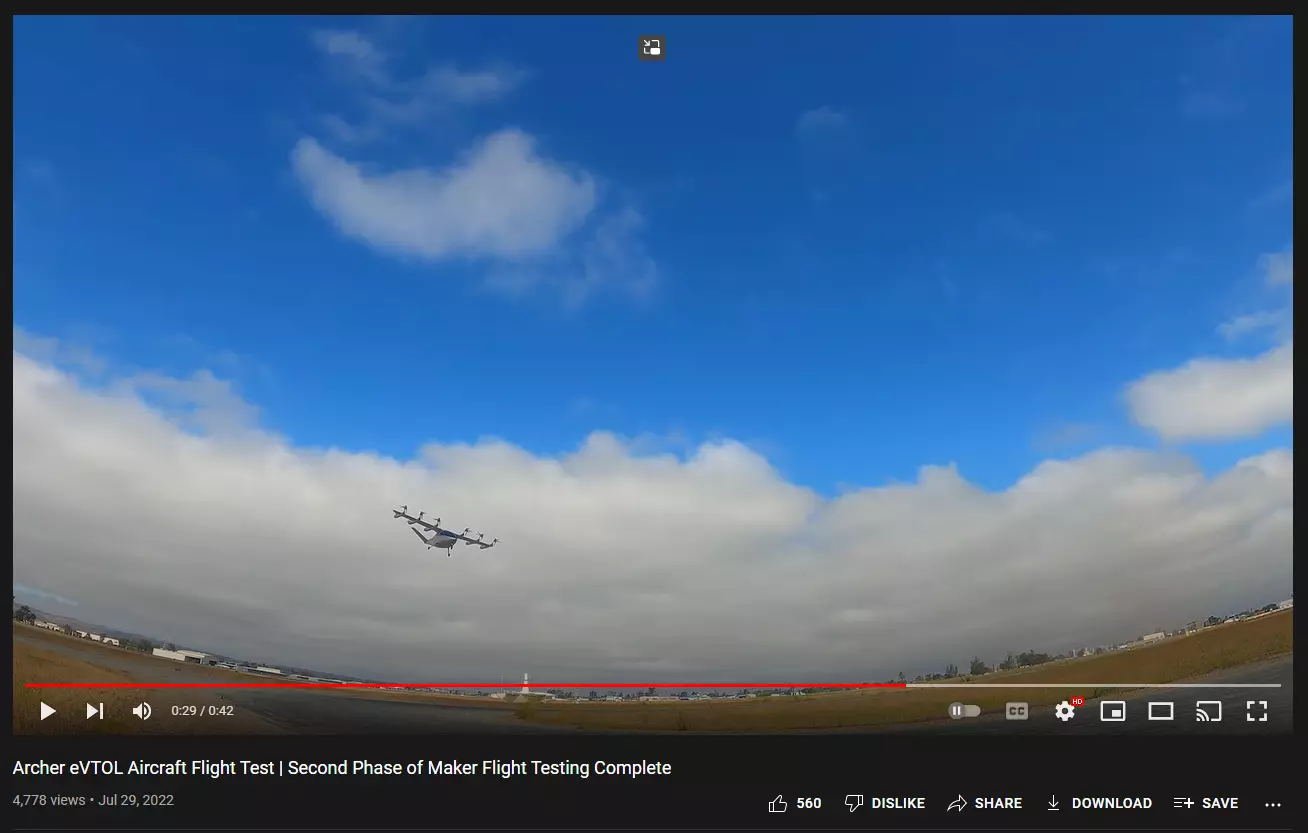

Regardless of the obvious different days’ flights spliced together, Archer titles this video:

“Archer eVTOL Aircraft Flight Test | Second Phase of Maker Flight Testing Complete”. Grizzly says “Hmmmm…that headline sounds like a lie, and looks like a lie … ”

We suggest investors have a look with their own eyes. Indeed, we did not compile all the instances in which footage is being re-used, as it would take too much space in this report.

Last year, in December 1st 2022, ACHR released a video to announce with much fanfare their “biggest” technical achievement and the finalization of years of work and development, the “Archer Full Transition Flight/Maker eVTOL Aircraft”, their first flying prototype.

Unsurprisingly, and similar to our previous comments on the other videos, this video is less than a minute long, and shows scarcely 10 seconds of actual flight footage. The rest of the reel is still pictures, pre-flight videos, and embedded camera footage with weird angles, barely showing anything. Among the comments, we can sense a huge disappointment from the investors, some of them even arguing that it did not really happen.

To us, it does not make sense that a company publishing so many videos on their supposed “progress” is not capable of shooting a properly transparent video showing clearly their biggest technological and operational achievement in a clear unambiguous single “take” from takeoff to landing. To this day, investors do not have publicly accessible material showing even a single unedited full flight or proof that their first prototype is capable of doing so.

Since then, ACHR conveniently released videos solely on their non-conforming commercial prototype Midnight-0. Indeed, even though the company stated in their earnings call that Maker is still flying regularly to collect additional precious data, investors are left with videos of a non-flying prototype, where they could only see its rotors turning at best, during the Paris Air Show. The company states it was conducting some ground testing with Midnight at that moment, but still, no videos have been released yet. Note that they did release short ground testing videos for their Maker prototype.

The main reason ACHR may be employing this sleight-of-hand is they seem to be trailing their competitors’ progress. Indeed, Archer is not only not showing much on its progress and actual demonstrator aircraft capacities, but what they show is not impressive compared to other companies such as Joby or Lilium. ACHR has not demonstrated yet that its aircraft operates and flies at the speed and distance they are promising investors.

Screenshot of a video showing a complete flight at high altitude and speed

by ACHR competitor Joby Aviation.

This simple 2.5 minute video is a single take. Note how it is thoughtfully overlaid with labels to point out the phases of vertical takeoff, transition, forward flight, transition and vertical landing without interrupting the continuity of visuals of the aircraft during its flight. Note its publication date is two years ago! Is that too much to ask of ACHR?

Transparency: We can’t hear you!!!

One of Archer’s videos aimed especially at noise levels fails to actually convey the answer to the question about noise levels. It is heavily edited and overlayed by another soundtrack to mask the sound of the aircraft. By comparison, Joby Aviation posted a comprehensive and clear video addressing the noise level of their aircraft in partnership with NASA (posted 1 year ago, plenty of time to copy its format), as well as a video comparing the noise level among various aircraft, including their own, with a clear audio segment for each aircraft (also posted a year ago).

You don’t have to be a rocket scientist to see and hear the point of this JOBY video

Which causes us to raise this question with regard to ACHR: Can they even spell “transparency”?

Test Flight Location Shows No Activity Matching Company Statements — This Duck Don’t Fly

During the Q3 2022 earnings call, Archer disclosed the location where they were purportedly conducting an active flight test program for their demonstrator aircraft, Maker. Brimming with curiosity, we sent a representative to learn about activities at their site. To get some context, here are several announcements the company made about test flight activity at the site:

During their Q2 2022 earnings call, ACHR management explained:

“As we announced two weeks ago, we have completed the first two phases of our Maker flight test program, hover and critical azimuth. We are regularly flying many times per week and sometimes multiple times per day. We are now shifting into the third phase of Maker’s flight test program, during which we will evaluate its system performance at increasing forward speeds.”

Screenshot showing the flight testing facility at Salinas Municipal Airport.

Additionally, in this YouTube video from August 2022 CEO Adam Goldstein says, “So even though we are flying every day, sometimes multiple times a day, every time I come out here, I just get so excited”.

The test flight facility location is 37 Mortensen Avenue in Salinas, CA, a small municipal airport where ACHR shares the main warehouse with several other companies, as disclosed in the exhibit from their 10-K filing.

Observing videos published on ACHR’s YouTube channel, here is the exact location where Archer conducted its few demonstration flights within the airport boundary (a single flight indicates a flight path over a patch of uninhabited contiguous farmland).

The blue and red outlines correspond to the exact position of the Maker during the flights shown on the videos. Even though the airport is a small municipal one, we didn’t want any stray events to escape our investigator’s view.

Our investigator spent a week monitoring the facility as well as inquiring about ACHR’s activities with people and companies operating and working at the airport.

Despite monitoring the exact location where the Maker purportedly flies regularly, our investigator was unable to identify the aircraft at all. We inquired with employees from other companies at the airport, who informed us they had only seen the aircraft once. The employees said this single instance was a long time ago, probably around December 2021 – January 2022 (statement offered, August 2022). Most people told us they had no idea about the company or the aircraft. Considering the airport’s small scale, all workers at the site would have been able to see an aircraft of the Maker’s size, especially if it was flying every day as reported.

Shown below, we also spotted a truck in the videos which ACHR calls their “mobile control unit” and is supposed to be engaged in test flight activities. Engineers are supposed to be controlling and monitoring the aircraft from the vehicle which would have to be set up before the Maker is taken out of the warehouse and reparked after it is done flying. Again, our investigator had no luck in observing this vehicle deployed even once, given the duration of the period we spent at the site.

ACHR’s “Mobile Control Unit” showed in a video posted August 2022.

ACHR shares the interior of the “Mobile Control Unit”

from a video of activity while Maker is operating.

We spoke to ACHR’s employees working in areas related to the site. This confirmed our findings. One of ACHR’s engineers told our investigator that if he wants to see the aircraft flying, he would have to “wait for a while” and that the aircraft “had not been flying for a few months”.

More recently, in July 2023, we decided to repeat our week of observation, when both Midnight and Maker should have been out there undergoing tests in the Municipal Airport. Obviously, Midnight couldn’t fly during that time, as it was waiting for its Special Airworthiness Certificate, but the company was supposedly already doing some ground testing, as stated in this press release from May 2023 and Maker should still be flying regularly, as stated by the management during their Q1 2023 earnings call from May 11th, 2023:

“Today, we don’t talk about it much, but we still fly Maker on a very regular basis with our very professional flight test team, and that’s the same team that’s going to be executing flight tests with Midnight going forward.”

Moreover, during that same call, management also confirmed that Midnight had been reassembled and was undergoing ground testing:

“Just last week, the aircraft was delivered to our flight test facility in Salinas and reassembled. You can see a picture of the aircraft in Salinas on the cover of our shareholder letter. This is right on schedule and means we are on track to begin flight testing of this aircraft this summer once it completes all its necessary ground tests.”

Below is a picture sent by our investigator, reporting accurately our observations from the entire monitoring period week. The hangar door on Archer’s side, with the aircrafts inside, remained closed.

Indeed, despite our week of observation, this time our investigator could not spot any activity either. Moreover, when speaking again to some nearby businesses, including one with a direct view of Archer’s warehouse door, they all affirmed to us that activity is very rare and that the aircraft only flies “sometimes, but really not often”. Our representative also spoke with engineers working in the same warehouse as Archer, (but not directly with them), who confirmed that they did not witness regular activity from Archer’s section. These people are the most precious witnesses we could hope to find, having the closest and most frequent contact and view on the company’s operations. Their statements were not surprising considering our other findings around the company’s messaging, especially with regard to other communication distortions we will show later in this report.

Moreover, as shown in the picture below, the other section’s door, adjacent to Archer’s section, was opened during one of our days of observation and we could clearly observe that both aircraft Maker and Midnight are just sitting in the warehouse that we monitored.

Note: Picture taken by our investigator showing rotors from Archer’s aircraft stored in the airport’s warehouse.

Given the recent statements made by management on their flight testing plan, we believe we have caught them in an outright lie. Could it be that Archer is struggling with its testing and needs weeks of preparation in the intervals between each short flight?

ACHR is Struggling to Build its Manufacturing Facilities on Time

The Lab Space/Low-Scale Production Facility Appear Way Behind Schedule

During their Q1 2022 earnings call on May 12th, 2022, ACHR announced:

“On the pilot line side, we are building out a new lab space here in North San Jose, and we will be [*inaudible*] in that lab space, we will be manufacturing our low-rate initial production facility there, where we will produce ten vehicles to really start to be used in the certification process. So, that lab will be built out through this year, and we will start the production of those vehicles next year.”

To continue our research, we analyzed the advancement of the construction for this “lab space and low-rate initial production facility” which was projected to be operational at the end of the year. A quick search in the company’s filings provided us with more information about this facility.

“On March 9, 2022, the Company entered into a lease agreement with SIR Properties Trust. The lease is for approximately 68,000 rentable square feet of building space in the building located at 77 Rio Robles, San Jose, California. The Company intends that the premises will be used for lab space and a low-rate initial production facility. The term of the lease commences 210 days after the landlord delivers possession of the premises to the Company, subject to certain demolition work being completed, and will expire 90 months thereafter, with an option for the Company to extend the term for one additional five-year period. Base rent payments due under the lease are expected to be approximately $15.0 million in the aggregate over the term of the lease.”

Consistent with our previous observations, we found a completely empty facility and parking lot. Our investigator bumped into some people who also described the building as empty and unoccupied. We peaked into the facility and found no signs of progress inside. We take this undeveloped facility to mean ACHR has either lied to investors or is way behind the announced schedule. In either case, this is very concerning. Here are the pictures of the facility we got from our investigator:

Picture of the building’s parking lot.

Picture of the building’s empty interior.

During the company’s last earnings call held on May 11th, 2023, management stated that some equipment was being installed in the facility:

“As we speak, lab and manufacturing equipment such as robots for our battery pack production line are being installed and commissioned. Lastly, there’s an aircraft final assembly area that can support the production of tens of aircraft per year.”

Two weeks later, during the J.P. Morgan conference, they announced that the facility was finally ready:

“With respect to our strategy, we are building out our San Jose test lab and pilot manufacturing facility. It’s actually coming online as we speak. It’s right around the corner from us.”

Therefore, we decided to pay another visit to the facilities in the area a few weeks ago. This facility is, as management said, “right around the corner” from their headquarters, although the headquarters seem to be only used for management and administration purposes. We then went to verify their claims on the lab & manufacturing facility following all the red flags and misrepresentations we previously presented in this report. The results are consistent with everything else.

Indeed, while we noticed some improvements, a conversation with people working at the facility along with a short walk inside confirmed that it is not as operational and ready as management is stating. We were told by these people that the facility will be operational around October this year and that a few people have been coming here for about a month. Moreover, we heard that the facility is not equipped with a specialized fire suppression system, a concerning indicator when they are working with lithium batteries, which have historically caused a number of difficult-to-extinguish fires. Moreover, we noticed electric wires coming out of the walls almost everywhere, another sign that the job is not finished.

In terms of activity, we observed a couple dozen cars in the parking lot. But inside, we could only see one person working in a rudimentary looking lab while all the employee break seating was totally empty.

Picture of the lab, we could only see one person working inside.

Picture of the facility’s parking lot.

In conclusion, while Archer has been making some progress on the construction of this lab & small-scale manufacturing facility, we believe they are misrepresenting the progress to investors. The facility is still far from operational and needs a lot more work before they can achieve anything meaningful there.

Five Months Later, Archer Only Removed Trees For Its “High-Volume Manufacturing Facility” Due in H1 2024

In March 7th, 2023, Archer proudly announced that it had begun the construction of the “First of its Kind High-Volume eVTOL Manufacturing Facility in Covington, GA” in partnership with Stellantis, their “manufacturing partner” to whom they gave millions of shares for free.

In more detail, the planned approximately 350,000 square-foot facility would be capable of producing up to 650 aircraft per year. The company added that this type of high-volume manufacturing facility is believed to be a first for the eVTOL industry. The Covington facility “should be capable of being expanded by an additional 800,000 square feet”, which is estimated to support long-term production targets of up to 2,300 aircraft per year.

To be exact, the company stated that the construction had begun on March 2nd, 2023. Also note that the goal is to get the facility up and running by mid-2024 and plans to spend $118 million for its construction, but gave away almost $70 million worth of stock to Stellantis before reaching any of the planned construction milestones. The timeline was softly pushed back into 2025 during the last earnings call where COO Thomas Muniz admitted that they have yet to pour any foundation.

Thanks to some local articles giving more information about the facility’s future location, we were able to find it. The facility will be built on a few parcels owned by the State of Georgia. The details of these parcels can be found on this website (Parcels IDs: C061000000017000 – C061000000014000 – C061000000018000.).

Using satellite images services, we were able to get a rough idea of how the terrain looked right after the company announced that the Phase 1 of the construction had begun:

According to the company, the beginning of the construction was intended to be marked with a ceremonial event in April. No event has been held or covered by any media so far. Analysts had seemed excited about it, as it was a means to get more attention on this new manufacturing facility project.

After three months of waiting and no ceremonial event on sight, in June 19th, 2023, the company stated that the construction was well underway, along with a YouTube video showcasing a rendering of the future facility, as shown below:

More than four months following the beginning of the construction, during July 2023, we decided to see for ourselves, and sent one of our investigators to look at the construction site. What we found is consistent with the rest of our findings. Indeed, as shown in the photos below, the company has only removed trees and flattened the ground. There was no building, no concrete slab poured, and no sign of rough-in utilities. This aligns with the company’s commentary during their last earnings call where Archer mentioned that they so far cleared the area and are getting ready to lay the foundation.

Moreover, we find a very interesting quote on this manufacturing facility project from management during the conference held by J.P. Morgan where Archer participated on May 23rd:

“Sure. I think there’s 2 different phases to that relationship. The relationship that we have — is desired between us two is for them to be a contract manufacturer for us at scale. And clearly, in that relationship, the contract manufacturer would own the assets, would own the technology around producing those assets, and we would enter into a sort of like a cost-plus relationship with them. So that — I think that’s — we haven’t defined on when that, what exactly that cutover point is.

Currently, they are contributing IP and people to help us think through the first phase and how that scales into the second phase. So the first phase, the Georgia factory, the San Jose factory, et cetera, those are — the cost of those are generally being borne by Archer by design. We’ve always had it in our plan. When and if we cut over to that new paradigm where they’re our contract manufacturer, when that happens, we’ll figure out who owns what at that point. But the good news is that we’ve come to an agreement that our goal is for them to be our contract manufacturer at scale. So we will get out of that business and just turn it over to them.”

In other words, Archer will bear most of the costs associated with the construction of the manufacturing facility while Stellantis simply assists them with IP and specialized workforce. In the end, Archer will probably leave all the assets to Stellantis, as the goal is to get out of the manufacturing business and get Stellantis to perform as their contract manufacturer.

Given the incentives from Archer to Stellantis we previously highlighted, under what conditions and price will Archer transfer the assets to them? Could it be that Stellantis will receive millions of free shares, discounted assets, and bear close to no risk? We see this situation as being a win-win for the partner once again, and a higher risk for ACHR’s shareholders.

Conclusion

Grizzly consulted with multiple FAA experts and the conclusion is that the most optimistic timeline to commercial launch of Midnight-1 is not next year, it is 4-5 years at the earliest, or most likely 2028 or beyond.

- Upon commencing test flights, it will take a year for Midnight-0 to be able to complete a nominally complete vertical takeoff, transition, substantive horizontal flight, transition, and vertical landing.

- As a one-off manufactured (non-conforming) aircraft, Midnight-0 cannot be Type Certified. That burden will have to be carried by Midnight-1 or aircraft currently unbuilt that follow.

- Rigorous FAA inspection of the manufacturing facility, including certification of all the subsystems manufacturing to FAA production standards, will be required.

- That certification activity cannot commence until a production facility is production ready.

- Some of the rules of the FAA certification process are not expected to be finalized before the end of 2024.

… and that’s if everything goes right. If one of the birds of any of the competitors, manned or unmanned, goes down (of course we hope not…), add another 18 months or two years for the investigation and consequences.

The demands of this timeline are not all ACHR’s fault; the competitors have to accomplish them as well. It’s just that ACHR has been spinning a yarn since inception, to the point we consider material misrepresentation.

We believe that investors have been misled by the standard tricks that have been employed by a generation of what we consider dirty companies, that came public through reverse merger with a SPAC. The projections seem utterly unreasonable, insiders are bailing left and right, and investors seem to be consciously misled with new videos and statements that we view as bordering on outright lies.

We also note that the pattern of handing out cheap shares to big name partners in order to gain credibility is something that we also observed with our last critical campaign where Ark Invest was a significant shareholder on the other side – TuSimple holdings. You want to go back for yourself and see how this situation played out. Our estimate is that Ark’s investment in Archer will be equally as successful.