Drug prospects dwindling, cash runway now drying up, abandoned by management, all while attempting to retain an investor base with false hopes driven by misleading statements

Bluebird bio (NASDAQ:BLUE), once a darling of the pre-revenue hot-biotech-money crowd, has entered its death spiral. Access to capital for bringing any product to market becomes increasingly dilutive and forces management into additional stock sales. Its core technology has been eclipsed by newer, safer, and more reliable treatment pathways. CEO Andrew Obenshain is now compelled to parrot a less and less credible portrayal of patient populations, treatment risks, and insurance reimbursement uptakes for his drug candidates. In this researcher’s view, Bluebird’s time for achieving escape velocity is past, and the forces of gravity pulling it toward a liquidation or dissolution scenario can no longer be escaped.

Key Takeaways:

- BlueBird also raised new funds in January only days after publicly stating that it had sufficient funds for the remainder of the year. The company also just recently filed a new shelf offering. We see BlueBird as a dilution machine.

- Considering BlueBird’s operational cash needs and dire prospects for commercial success, we believe the company will have to continue to dilute shareholders for the foreseeable future.

- Notably, almost the entire executive team and board of directors exited in late 2021, amidst the recent spin-off of BlueBird’s oncology division.

- We believe BlueBird is in a death spiral – foreseen by management who jumped at the chance to bail out during the oncology division spin-off after raking in piles of cash. We believe BlueBird will continue to dilute investors while putting forth false hopes and narratives.

- Projections made by BlueBird rely on old and inaccurate data, while some more recent data suggests a lower total addressable market for both the Zynteglo (Beta-Thalassemia) and the SCD (Sickle Cell Disease) treatment.

- BlueBird withdrew its Conditional Market Authorization from the European Union for “commercial reasons”. This is a strong indication that BlueBird’s treatments are simply commercially unviable outside the U.S., while its window of opportunity narrows within the U.S… The EMA (European Medicines Agency) had stricter guidelines and exclusion criteria for Zynteglo compared to the FDA (Food and Drug Administration); those policies considerably shrank the total addressable European market size. Moreover, BlueBird’s treatments are extraordinarily expensive: $3.0 for Skysona and $2.8 million for Zynteglo. These are among the highest priced treatments in the world. Even with the “adjustments” and “payment facilitation” offered by BlueBird, we doubt the treatment can ever be commercialized anywhere outside the U.S.A. This considerably reduces the economic prospects of these treatments and, most likely, for the future treatments as well. (See Pt 3 for the full story)

- Potentially eligible patients for BlueBird’s treatments “Zynteglo” and new lovo-cel, which are aiming to cure TDT (Transfusion Dependent Thalassemia) and SCD (Sickle Cell Disease), are, according to numerous experts we consulted, far fewer than the company portrays. (See Pt 3 for the full story)

- BlueBird’s recent Q4 2022 and Q1 2023 reports were filled with disappointing news, including a delay in their BLA submission for their SCD treatment and a very low number of patients that have initiated cell collections on both available treatments. Moreover, specifically for Zynteglo, 13 Qualified Treatment Centers (QTC) have been activated as of May 8th, 2023. According to the company, these were set up in the most prominent areas in terms of eligible patients, making these low numbers very alarming. We believe these early signs of non-adoption are very telling with regard to future market share. (See Pt 3 for the full story)

- Experts we consulted stressed that BlueBird has placed undue focus on parts of its clinical results data to make its treatment seem more beneficial than it actually is. Data cherry-picking and misrepresentation is, in our opinion, rampant in BlueBird’s disclosures. (See Pt 3 for the full story)

- We think management and the company have long realized that BlueBird is crashing and are trying to salvage the parts that might have more promise. But we also think there might be a more nefarious reason for management and board to abandon the company, which is to avoid legal liabilities. (See Pt 4 for the full story)

- The long-lasting legal battle that started in 2017 against San Rocco Therapeutics (SRT), which BlueBird attempted to de-emphasize in its disclosures, seems to have recently turned in SRT’s favor. Indeed, the Arbitrator Final Award dated February 7th, 2023 states that SRT has “exclusive, royalty-free commercial license” to patents that are indispensable to BlueBird’s technology. These patents appear to have been wrongfully used by BlueBird to develop their gene therapy treatments. (See Pt 4 for the full story)

- Following the recent Arbitrator Award, SRT filed a new lawsuit on April 27th, essentially trying to stop BlueBird’s alleged illegal use of SRT’s technology. We believe this suit poses an enormous risk to BlueBird’s future. The patents are essential to BlueBird’s technology, and the company is not in a position to afford a big penalty. The new lawsuit seeks $500 million in damages. (See Pt 4 for the full story)

- BlueBird’s technology is way less advanced and older than its competitors’. Most scientists we consulted agree that it also bears more risks. While direct competitors are using the CRISPR/CAS9 technology, which allows selecting only a specific DNA section to modify and limit the risk of oncogenesis, BlueBird’s treatment is a widespread injection with unknown potential inclusions and side effects more likely to develop. (See Pt 5 for the full story)

Guide to Contents

Key Takeaways

Introduction

Pt 1 Cash dwindling, dilutive financings …despite management protestations

Pt 2 Management actions no longer aligned with shareholders, at least not BLUE shareholders

Pt 3 CEO narrative increasingly a storyline, detached from actual data points, overstating prospects

Size of Addressable Markets, Total Number of Eligible Patients as Identified by Management Relies on Old, Inaccurate, Incomplete Data

European Market closed, company abandoned on-ramp

Unprecedented high-cost pricepoints appear increasingly impractical, insurance reimbursement far from certain

Cherry-picking clinical trial subsets to mislead investors about prospects

BlueBird has totally lost their “early mover” advantage in this treatment space

Pt 4 Longstanding legal battles over misappropriated /abused IP of other firms now coming to judgment, very unfavorably for BlueBird

We believe the company deliberately tried to understate its legal troubles To investors, which we believe could seriously affect the company’s future

Pt 5 BlueBird’s tech is now old, and has been eclipsed by competitors

BlueBird’s technology is outdated and competitor’s technology is way Safer and more precise

Pt 6 Changes to competitive landscape

Pt 7 Other uncategorized risks to future revenues

Appendix 1: Viral Vector Background Info

Therefore, the basis of the vector used by Bluebird has historically been and is still the same as the one used and developed by SRT

Introduction

BlueBird is a biotechnology company that has recently commercialized two gene therapy treatments in the U.S., the Zynteglo for Beta-Thalassemia and the Skysona for Cerebral Adrenoleukodystrophy.

As of May 9th 2023, only a single injection of each treatment, Skysona and Zynteglo, were administered. The company’s valuation relies on dubious future revenue projections, and present-day dilutive financings to keep the game going forward.

Through the company’s various investor presentations and press releases, investors might anticipate BlueBird’s promising future prospects and opportunities, but we believe these are drastically exaggerated. Multiple red flags lead us to conclude that BlueBird is desperately and actively trying to retain investor support for as long as possible while it slowly fades into oblivion.

- The company will obviously have to raise more cash to keep operating. We believe shareholders will suffer severe dilution sooner than expected. Indeed, it appears the company seems to have timed its January public offering quite well because we see the stock continuing to decline. Additionally, Bluebird recently filed an S-3 form for up to $350,000,000 mixed shelf offerings, which strengthens our beliefs. (See Pt 1 for the full story)

- Dilutive financing follows a very shady departure of the whole management team and board of directors to their oncology department spin-off, that took place in November 2021, where the whole leading team seems to have abandoned BlueBird. (See Pt 2 for the full story)

- Indeed, we believe that BlueBird has overstated and inflated its presented projections and total addressable market numbers to portray an exciting economic outlook for the next few years. In this report, we explain why we think this will not be fulfilled. (See Pt 3 for the full story)

- BlueBird has been presenting outdated and inaccurate key data to investors. (See Pt 3 for the full story)

- The ongoing uncertainty around the insurance coverage of their treatment, which are among the most expensive in the world, poses another ongoing risk. Even though the company is trying to reassure investors on this matter, we believe they remain suspiciously vague. The treatments start at $3.0 and 2.8 million for their Skysona and Zynteglo, respectively. (See Pt 3 for the full story)

- The sole advantage BlueBird enjoyed was that they were the first company to have commercialized their treatments, although we do not believe it will help them capture a relevant and sufficient market share. Their recent BLA submission delay and early signs of non-adoption are not encouraging. Patient interest in their treatments seems to be low, as announced in their latest earnings, with only 6 patients (as of May 9th 2023) across more than 13 Qualified Treatment Centers having initiated cell collection for Zynteglo, in areas of supposedly high prevalence. The real safety and efficacy of its treatments remain largely unknown. (See Pt 3 for the full story)

- The company is also in the middle of a fierce legal battle again San Rocco Therapeutics, which just filed another complaint against BlueBird, its spin-off 2SeventyBio, its former executives, and some other defendants affiliated with the company. This comes after SRT recently received a favorable arbitrator award in another lawsuit closely related to this one, in March 2023. (See Pt 4 for the full story)

- BlueBird’s technology is outdated compared to competitors. Moreover, we believe more exclusion criteria will be added to the already long list in the next few years. (See Pt 5 for the full story)

Pt 1 Cash dwindling, dilutive financings …despite management protestations

The Company will Remain in Dire Need of Cash Indefinitely as it Faces an Uncertain Future

We believe that BlueBird is actually in a much worse economic and financial situation than it portrays, and the recent Public Offering strengthens our opinion. BlueBird stated in its latest 10-K that:

“There is substantial doubt regarding our ability to continue as a going concern. We will need to raise additional funding, which may not be available on acceptable terms, or at all. Failure to obtain this necessary capital when needed may force us to delay, limit or terminate our commercial programs, product development efforts or other operations.”

And…

“The Company expects to continue to generate operating losses and negative operating cash flows for the next few years and will need additional funding to support its planned operating activities through profitability. The transition to profitability is dependent upon the successful development, approval, and commercialization of lovo-cel, the successful commercialization of ZYNTEGLO and SKYSONA and the achievement of a level of revenues adequate to support its cost structure.”

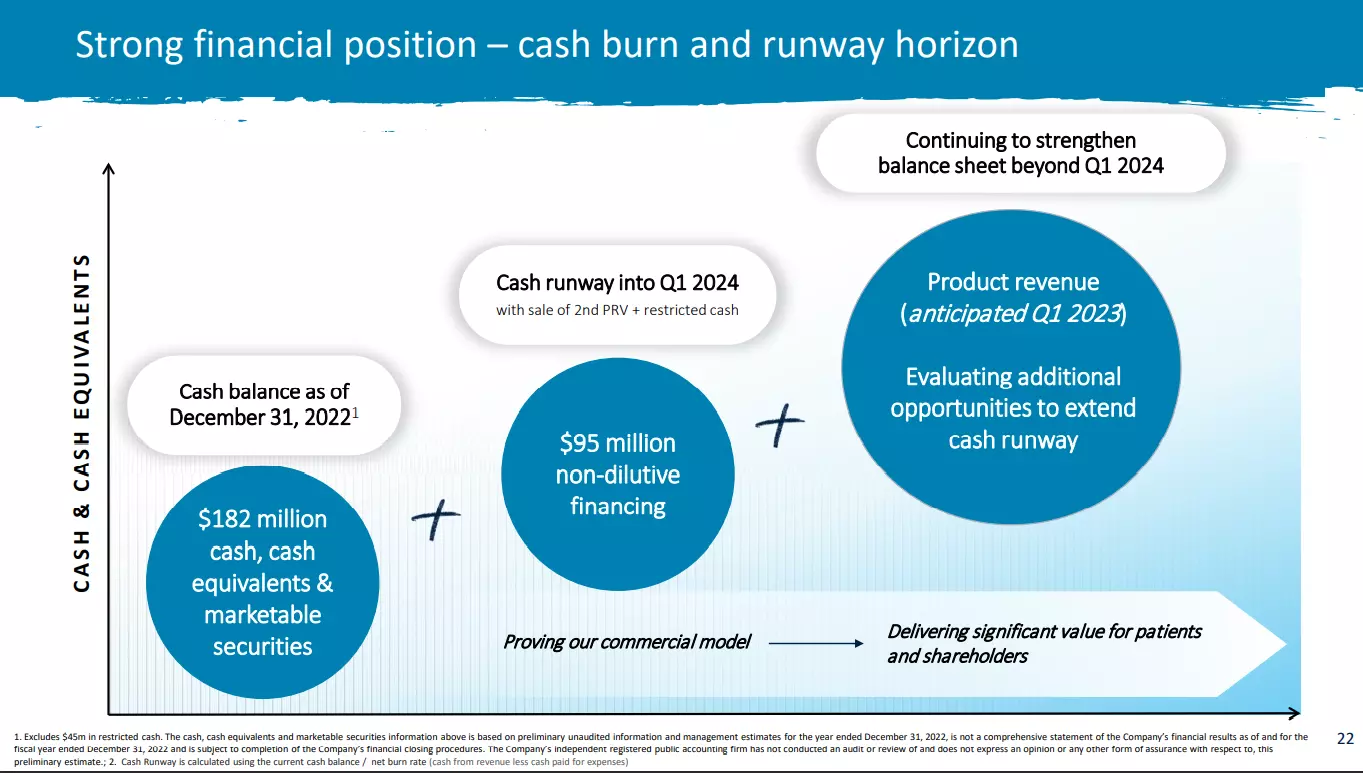

While BlueBird has been able to secure some cash through their recent stock issuance in January 2023 and the sales of its “Priority Review Vouchers”, we still believe that it will continue to heavily dilute its current shareholders in the near future. The company recently conducted a new Public Offering of Common Stock, 20,000,000 shares of its common stock for total gross proceeds of over $130 million, including the 30-day option for the underwriters got to purchase up to an additional 3,000,000 shares of its common stock.

While it was common knowledge among investors that BlueBird would soon be in need of new financing, the timing is very unexpected to us, as the company had just sold its Priority Review Voucher and stated that:

“2023 Financial Outlook: The Company’s preliminary unaudited cash and cash equivalents and marketable securities balance was approximately $182 million, excluding restricted cash of approximately $45 million, as of December 31, 2022. As BlueBird bio launches two first-in-class gene therapies and readies its third investigational gene therapy for SCD for the commercial setting, full-year 2023 cash burn is expected to be in the range of $270-$300 million. BlueBird expects its cash, cash equivalents, restricted cash and marketable securities, including the proceeds from the sale of its second priority review voucher (PRV) for $95 million, will be sufficient to meet BlueBird’s planned operating expenses and capital expenditure requirements into the first quarter of 2024”

The above statement is from BlueBird’s Presentation at the 41st Annual J.P. Morgan Healthcare Conference in January 12th, 2023, only one week before the capital raise was announced.

Source: J.P. Morgan Presentation (BlueBirdbio.com) (January 2023)

Source: J.P. Morgan Presentation (BlueBirdbio.com) (January 2023)

The only reason that explains to us the timing of this public offering is that BlueBird management is well aware of its situation and did not foresee their stock price reaching any higher level anytime soon, despite all the positive catalysts that were supposedly on the way for Q1 2023. How could a company that will finally reach commercialization in a few weeks with a supposedly strong demand from a niche market and very appealing economic outlook raise money at that moment without supposedly needing it? Only a week after stating that the “Company enters 2023 with a cash runway into Q1 2024”? Perhaps it is in view of the BLA submission delay as well as the poor performance in terms of patients’ conversion.

In their latest 10-Q, the company affirmed that it has enough cash to fund its operation into the fourth quarter of 2024. Seeing their recent cash burn and revenue generation, we highly doubt that it will be the case, and expect additional capital raise in the next few quarters.

There is also a risk, pointed out by the company, that: “Without the release of our restricted cash, however, we estimate our cash, cash equivalents and marketable securities as of March 31, 2023 will be sufficient to fund our operations into the second quarter of 2024.”

Shelf Offering: Early May 2023, following a big run-up of more than 80% on their stock price the week before, the company filed an S-3 form. This allows the company to offer up to $350,000,000 in mixed securities over time, which could cause tremendous dilution of the stock price in the future, as we expect will happen. Once again, we believe this to be a huge red flag and a negative indicator for the future. The stock price dropped more than 50% following the latest offering.

Pt 2 Management actions no longer aligned with shareholders, at least not BLUE shareholders…

The company’s Management Had Already Decided to Abandon Ship

In November 2021, BlueBird spun off its oncology department, and it appears to be for the wrong reasons.

“BlueBird bio, Inc. (NASDAQ: BLUE) tax-free spin-off of its oncology programs and portfolio into 2seventy bio, Inc. (NASDAQ: TSVT), an independent, publicly-traded company. 2seventy launched with a cell therapy pipeline across a range of hematologic and solid tumors. 2seventy’s portfolio also includes a development and U.S. commercialization partnership with Bristol Myers Squibb for ABECMA, a BCMA-directed CAR T cell immunotherapy for multiple myeloma.” At its launch, 2seventy bio’s assets include BlueBird bio’s immune-oncology cell therapy products for solid tumors and hematologic malignancies, as well as $442m in cash to fund its operations into 2023.”

TSVT IPO’d at a price of $17.25 and quickly soared to above $40 per share in the few days following. It is currently trading at around $12 per share, with a market cap of around $600 million.

In our opinion, the spin-off’s main purpose was to save the potentially money-making oncology department from the doomed “BlueBird”. Not only did BlueBird fund the company with over $480m but also retained all the debt on its balance sheet while being drastically short on cash for the rest of its operations.

Moreover, management chose to convert the shares they acquired through generous stock based compensations into the spin-off. It seems that management is not interested in the remaining BlueBird entity.

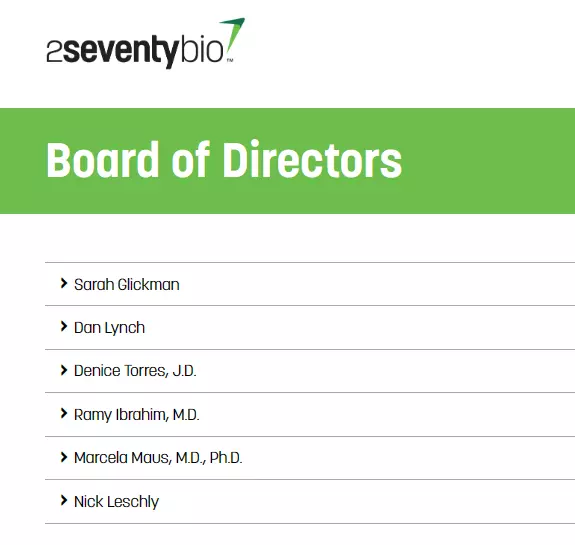

“On November 4, 2021, in connection with the Separation, Daniel Lynch, Sarah Glickman, Ramy Ibrahim, Denice Torres, Marcela Maus and William Sellers each resigned from BlueBird bio’s board of directors (the “Board”).”

Unsurprisingly, we found all of the directors who resigned are now forming the new spin-off’s board of directors:

Source: Company’s Website

Source: Company’s Website

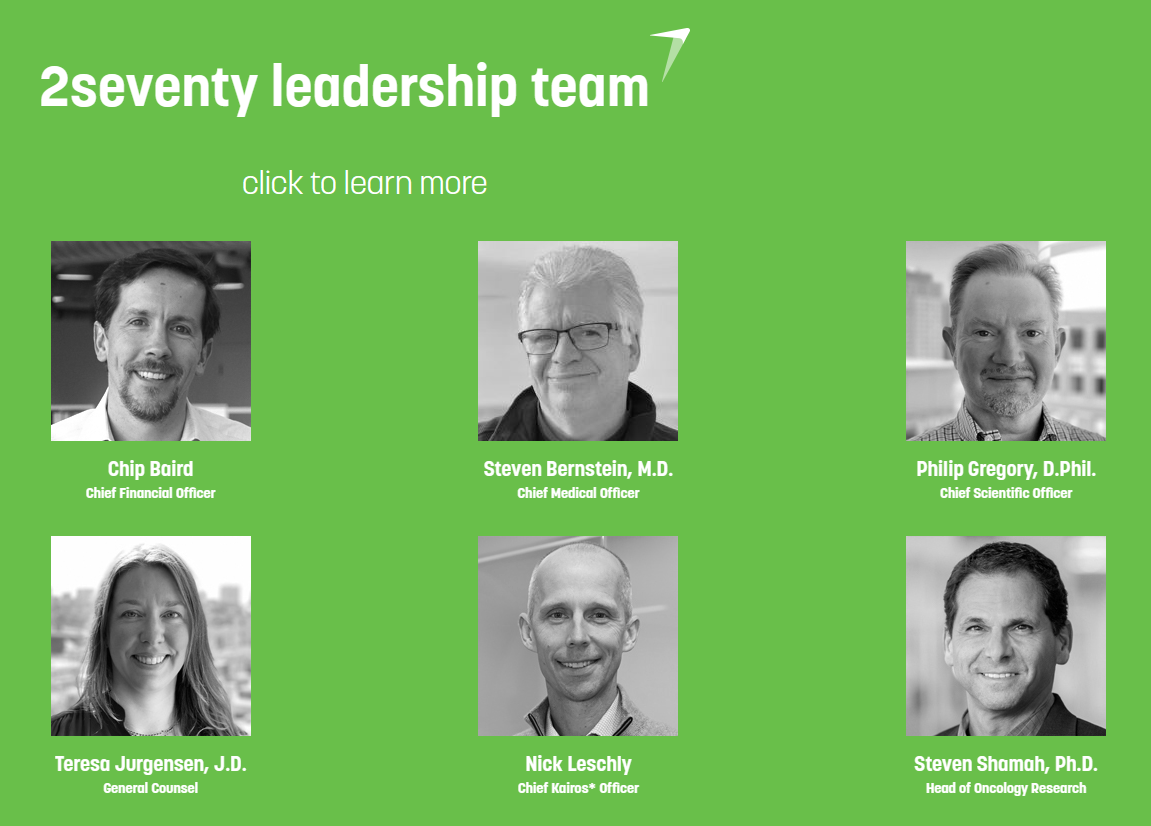

Way more worrying is the fact that BlueBird’s top management also resigned from their positions to take up lead roles at the spin-off, but with a twist:

“Additionally, on November 4, 2021, in connection with the Separation, Nick Leschly, William Baird and Philip Gregory resigned as BlueBird bio’s chief executive officer, chief financial officer and chief scientific officer, respectively.”

Source: Company’s Website

Source: Company’s Website

We observe very alarming quotes from the most recent lawsuit in which BlueBird as well as the spin-off and its directors are defendants:

“Defendants caused BlueBird to announce that they created 2seventy to spin off the oncology program; however, these statements were false and/or intentionally misleading and were part of Defendants Leschly’s, Reilly’s, Finer’s, Third Rock’s, and BlueBird’s fraudulent scheme to transfer their capital gains and investments out of BlueBird into another company as a way to avoid paying subsequent damages and liabilities owed to SRT.”

“Defendants caused BlueBird to announce that they created 2seventy to spin off the oncology program; however, these statements were false and/or intentionally misleading because, inter alia, BlueBird subsequently granted and transferred to 2seventy rights and/or ownership in the BB305 Vector.”

“In 2018, Leschly was the highest compensated CEO in biopharma, raking in $24,000,000; and between 2010 and 2021, Leschly sold over $100,000,000 in shares of BlueBird. Leschly currently owns substantial stock in 2seventy.”

Pt 3 CEO narrative increasingly a storyline, detached from actual data points, overstating prospects

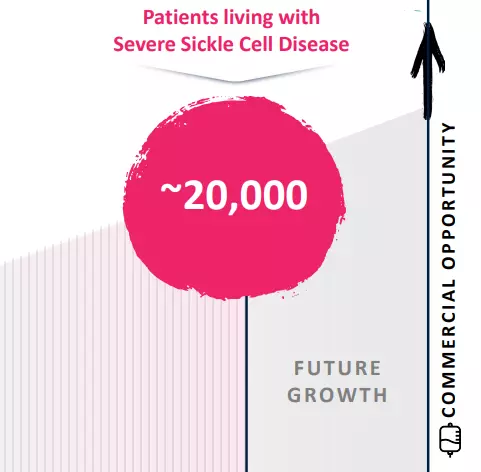

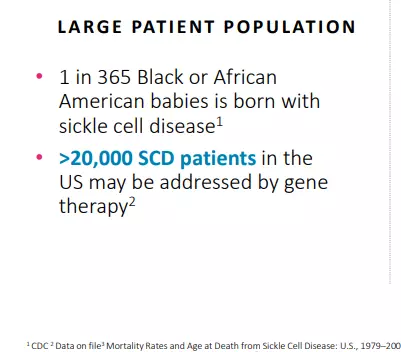

Size of Addressable Markets, Total Number of Eligible Patients as Identified by Management Relies on Old, Inaccurate, Incomplete Data.

BlueBird has been using exaggerated numbers which are of great importance, because they are used to generate financial projections. Their estimated number of eligible patients is almost a random number, given the fact that the data used is too old, inaccurate and in some cases even incomplete. In fact, there is currently no precise estimate available, as data still requires accumulation. For some reason, the company’s estimates are always higher than any sources we were able to find. As BlueBird is now relying solely on the U.S. market, these numbers are even more important for the company.

Beta Thalassemia (Zynteglo/Beti-Cel):

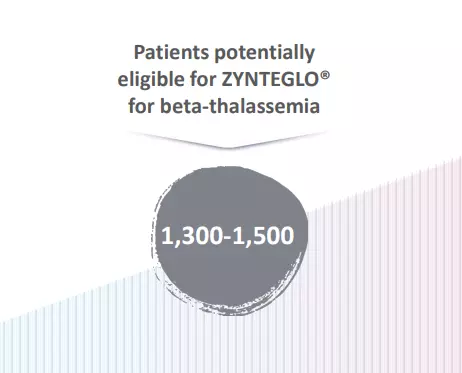

First, we believe that BlueBird has not put a lot of effort into determining its total number of eligible patients for its Beta-thalassemia, Zynteglo, which remains their most important currently commercialized treatment. We believe the reason is that the number BlueBird presents might be an optimistic overshoot for reality.

Even though BlueBird has been presenting various numbers when it comes to the total eligible patients for its Zynteglo treatment, most investors are basing their projections and expectations on the higher end of the estimation, which is 1500 “potentially eligible patients”. This estimation remains the most recent, as it is used in BlueBird’s latest investor presentation dated May 2023 as well as during the latest earnings call held in March 2023, where Thomas J. Klima, the company’s COO & CCO stated:

“Yes. So of the 1,500 patients in the U.S. who have — QTC — our initial Wave 1 QTC network we thought we could reach about 50 patients.”

Source: Company’s Latest Investor Presentation

Source: Company’s Latest Investor Presentation

It was disclosed by BlueBird that the supporting sources for this estimation are based on the CDC’s numbers and other sources that we will document below. But to do a proper assessment and estimation of a population affected by a disease, it is necessary to conduct what is called an “epidemiology” study.

An epidemiology is by definition “The study of the distribution and determinants of health-related states and events in specified populations”. It requires years to collect enough data in order for it to be relevant and accurate, especially when it comes to a rare disease.

We decided to interview an expert about the current available data on the beta-thalassemia epidemiology. This expert has 25 years of experience in bio-medicine has been involved countless times in drug design and development. His conclusion was unequivocal: There is no recent comprehensive data on this disease in the U.S.

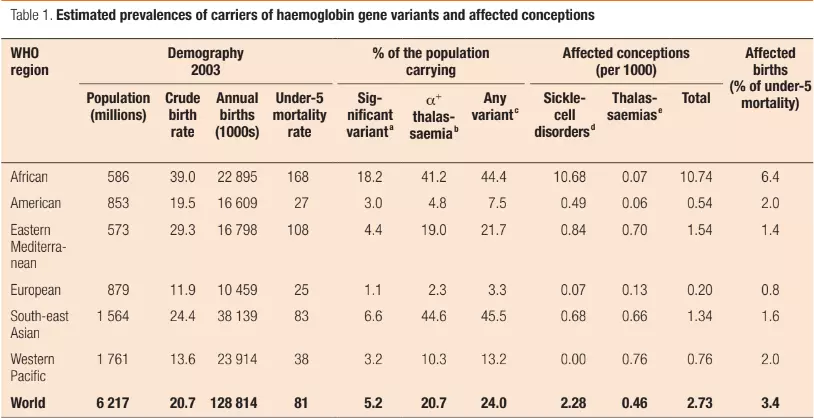

Recent research papers and scientific articles dated as early as 2021 clearly state that there is no current possibility of precisely determining the number of people with Beta-thalassemia in any part of the world. The latest relevant data points that the expert could identify as the ones used by the sources cited by the company date back to 2003 to 2008.

When we presented to him the estimate BlueBird was using in its various investor presentations, the expert was negatively surprised. He even stated that the company probably applied a simple “world estimate” of people carrying the disease to the total U.S. population, which would be unprofessional and inaccurate. Indeed, the main reason is that beta-thalassemia appears most commonly in certain regions of the world, including Eastern Mediterranean, African and South-East Asian regions. Therefore, because of these disparities, a world estimate cannot be accurate if applied to any of the individual regions. After digging deeper into the beta-thalassemia numbers, as guided by our expert, we could not reach a similar conclusion as BlueBird on the eligible patients estimate and we still wonder how they reached such high estimates. We present screenshots of the main data source used by BlueBird and its sources below:

Note and Source: “Epidemiology of β-thalassemia. Global epidemiological data including the percentages of populations carrying Hb variants, the number of newborns who have β-thalassemias per year, the number of patients who have TDT, and the percentage of TDT patients who are reached for blood transfusion, and the number of patients who died as a consequence of not receiving blood transfusion worldwide and in the individual sub-regions, according to the World Health Organization (WHO) as reported by Modell B and Darlison M published in the Bull World Health Organ 2008, 86, (6), 480–487”

We notice a few interesting points in this scientific article published in 2008. First of all, the article used 2003 as its “as of” date; such old data is not reliable when it comes to epidemiology. But more generally:

- The percentage of the population carrying an Hb variant in the American region is lower than the World average, with only 3% for the American region against 5.2% for the World.

- The American region is the area with the lowest number of annual deaths because of non-transfusion of patients, making it the region with the least urgent need for a treatment leading to transfusion independency.

- There was a number of 2,750 known patients in the American region, comprising of South America and North America. But the United States only accounts for around 30% of the total population.

After getting an approximate number of potential known patients in the United States, ineligible patients must be subtracted. Subsequent sections of this report are dedicated to this matter, but we will now provide a short and non-comprehensive list of ineligible patients:

- 4 years old or younger, carry some incompatible genotypes (extensive list still to be determined)

- not being transfusion dependent and where hematopoietic stem cell (HSC) transplantation is appropriate

- and a human leukocyte antigen (HLA)-matched related HSC donor is available (fewer than 25% of patients have compatible donors).

Moreover, Zynteglo has not been studied in multiple other instances, such as on patients older than 65 years old, pregnant women or with renal/hepatic impairment and more exclusion criteria are probably added in the future.

Additionally, it was mentioned in the 2022 ICER report (which BlueBird highlighted in this press release) that the number of TDT in the U.S. was around 1,000 – far below the estimated number BlueBird is using for its presentations and projections:

“Policy-makers and life science companies should consider that there are 300,000 people living with transfusion-dependent beta-thalassemia (TDT) worldwide, but only 1,000 of them reside in the U.S… Thus, the global burden of thalassemia lies predominantly outside of the U.S.. Unfortunately, the current business model for innovation will not offer easy options for making expensive treatments accessible to the vast majority of patients living with TDT. Long-range policy efforts should be directed at addressing this important ethical problem.”

However, more recent scientific papers tend to lean towards even lower estimates. Indeed, according to newer research, the Transfusion Dependent population in the U.S. would be around 900 patients, without including the exclusion criteria for the treatment administration, which would decrease that number:

“Surveys have shown that 10 large thalassemia centers in the country collectively follow about 1100 patients, while additional 1500 patients are estimated to receive care at other hospitals.”

(The transfusion management of beta thalassemia in the United States, Lal, 2021)

“The Thalassemia Western Consortium (TWC) study showed that of the 717 patients, 44% of patients had β thalassemia syndromes (including 15% with HbE β thalassemia) and 55% had various α thalassemia disorders. Transfusion-dependent patients comprised 35% of the population, 9% had received 1 or more life-time transfusions, and 56% had never been transfused.”

(The transfusion management of beta thalassemia in the United States, Lal, 2021)

In our opinion, all of the points mentioned suggest investors apply serious professional skepticism regarding BlueBird’s potential eligible patients estimates. As mentioned earlier, it appears that BlueBird simply used the CDC’s estimate coupled with a basic calculation. Perhaps that estimate would pass scrutiny of many investors given the credibility of the source, but we believe investors might fail to account for nuances in the data, especially about how old and inaccurate the data is. In this researcher’s opinion, a more credible estimate, based upon more recent data, would probably result in a substantial decrease in the number of potentially eligible patients for Zynteglo, and therefore its economic viability and outlooks as well.

Sickle-Cell Disease Treatment (SCD/Lovo-Cel):

Similarly, we noticed that BlueBird apparently followed the same process for its SCD (Sickle Cell Disease) treatment and the estimate of the potentially eligible patients. Indeed, the exact number of people living with SCD in the U.S. today is simply unknown. Currently working on it with various partners, the CDC supports projects to learn about the number of people living with SCD to better understand how the disease impacts their health.

Below is a table gathering the data currently available on SCD in the U.S. Note that it is also the only accurate data available, and that a number of state censuses are still ongoing:

| States | Numbers | Year Period | Birth Period | βS/βS or βS/β0 | βS/β+ | Total Severe scd | Number / Year |

| Colorado | 65 | 5 | 2017-2021 | 37 | 8 | 45 | 9 |

| California | 420 | 5 | 2014-2018 | 227 | 34 | 260 | 52 |

| Minnesota | 96 | 5 | 2016-2020 | 58 | 11 | 68 | 14 |

| Michigan | 294 | 5 | 2013-2017 | 162 | 29 | 191 | 38 |

| Indiana | 164 | 5 | 2015-2019 | 105 | 11 | 116 | 23 |

| Virginia | 321 | 5 | 2016-2020 | 189 | 16 | 205 | 41 |

| North Carolina | 624 | 5 | 2016-2020 | 306 | 25 | 331 | 66 |

| Tennessee | 221 | 5 | 2015-2019 | 137 | 18 | 155 | 31 |

| Georgia | 761 | 5 | 2014-2018 | 419 | 68 | 487 | 97 |

| βS/βS or βS/β0 | βS/β+ | Total Severe scd | Numbers / Year | ||||

| Total | 1639 | 220 | 1859 | 372 |

*(Source : CDC as of April 2023)

In summary, there is currently no accurate way to determine the number of potentially eligible patients for the SCD treatment. Once again, BlueBird has likely made projections based on rough estimates, extrapolating geographically specific data over the national population.

(Source: Company’s Latest Investor Presentation)

(Source: Company’s Latest Investor Presentation)

Moreover, it appears in the ICER report that, once again, there are some discrepancies regarding the number of eligible patients announced by BlueBird and by the ICER. Quoted from the latest SCD Draft Evidence Report published in April 2023:

“Generalizability outside of the trial setting was a concern raised by clinical experts who estimated that only small proportion (<15%) of people living with severe SCD might satisfy trial criteria.”

“In the United States (U.S.), it is estimated that approximately 100,000 people are living with SCD, although the exact prevalence is unknown.”

According to these numbers, the total eligible population for BlueBird’s SCD treatment is at least 25% less than the company’s estimates, which they strew liberally about their numerous press releases and presentations. Given a hypothetic $2,000,000+ treatment, similar to the ones already commercialized, this would reduce their future revenue prospects by more than $10 billion.

BlueBird’s sole source justification is “data on file”

Moreover, we found that this treatment also got a quite extensive and impactful exclusions criteria list which further shrinks the estimate. Here is one example below:

During the 64th ASH Annual Meeting, BlueBird bio exposed two cases of persistent anemia observed in an adult and a pediatric patient, in the pivotal cohort of the Sickle Cell Disease HGB-206 study of lovo-cel. Both patients had two α-globin gene deletions (−α3.7/−α3.7) and this alpha-thalassemia trait contributed to anemia after lovo-cel infusion. Thus, this genotype has been added to the exclusion criteria for the clinical trial. However, it was not specified if the excluding criteria of the α-globin gene deletion (−α3.7) is homozygous or also heterozygous.

As expected, the number of potentially eligible patients, which largely included African-Americans and Hispanic-Americans needs to be revised since the α-globin gene deletion (−α3.7) prevalence is 17% for Hispanic-Mexican individuals with the sickle cell trait and 16% of the Hispanic-Mexican subjects with beta-thalassemia.”

(María Paulina, Nava Bertha, Ibarra Bertha, Ibarra Maria, Teresa Magana, Torres Maria, Torres F, Javier Perea, Prevalence of −α3.7 and ααα anti3.7 alleles in sickle cell trait and β-thalassemia patients in Mexico. March 2006 Blood Cells Molecules and Diseases 36(2):255-8 DOI: 10.1016/j.bcmd.2005.12.003).

This also raises bigger concerns for the company, mostly that more gene deletion could lead to other medical conditions following the injection, and that would add to the list of exclusion criteria. With such a low number of patients in the clinical trials, insufficient data exists to determine all the profiles to exclude yet. We believe that with more treated patients, the list of exclusion criteria will become longer, which in turn shrinks the number of eligible patients.

We believe BlueBird has not been transparent enough to investors on these matters.

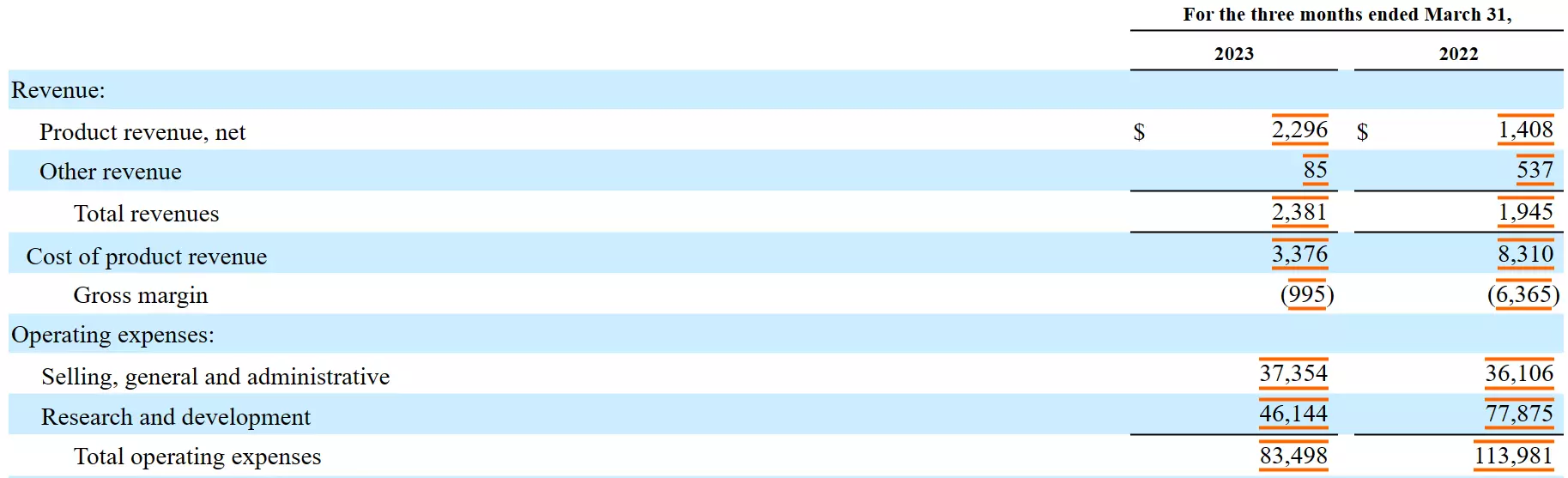

BlueBird’s releases cast doubt on its ability to capture the number of eligible patients on which most of their projections are based, which makes its ongoing cash burn even worse. During the past quarter, excluding the gain from sale of a priority review voucher, BlueBird burned more than $80 million of cash. With a very uncertain revenue generation future, gross margin uncertainty, which appears to be very low considering the currently available data on it, the outlook would require fiction to be encouraging.

(Source: Company’s filings, 1Q 10-Q 2023)

(Source: Company’s filings, 1Q 10-Q 2023)

European Market closed, company abandoned on-ramp

The European Market, the Entry Door to the Rest of the World Remains Closed For BlueBird

In a press release dated as of March 30th, 2022, the EMA (European Medicines Agency) stated that:

“On 24 March 2022, the European Commission withdrew the marketing authorization for Zynteglo (betibeglogene autotemcel) in the European Union (EU). The withdrawal was at the request of the marketing authorization holder, BlueBird bio (Netherlands) B.V, which notified the European Commission of its decision to permanently discontinue the marketing of the product for commercial reasons. Zynteglo was granted conditional marketing authorization in the EU on 29 May 2019 for treatment of transfusion-dependent β-thalassaemia (TDT). The marketing authorization was initially valid for a 1-year period. It was subsequently renewed for an additional 1-year period in 2020 and 2021. The European Public Assessment Report (EPAR) for Zynteglo will be updated to indicate that the marketing authorization is no longer valid”

While BlueBird tried to portray this move as insignificant for the company’s future prospects, we believe the failure to find arrangements for Zynteglo in the EU has in fact a way bigger impact on its future. The European Market contains many countries, some of which with the best healthcare systems and coverage in the world. By failing to reach an arrangement with any of these countries and by having to discontinue the marketing authorization in the EU, BlueBird has shown investors that its sole attainable market will remain the United States. This is confirmed by statements from the company’s CEO during their latest earnings call, when an analyst asked if they are thinking about the ex U.S. opportunities:

“On the ex U.S., we are focused on the U.S. only right now. We got this — we are getting the therapies launched, getting the therapy to patients in the U.S. It’s not on our radar screen for ex U.S. at the moment.”

Only the U.S. healthcare system can potentially be suited for the range of prices that BlueBird is seeking for its products. As we have shown earlier, the regions that are the most affected by the targeted disease are South East Asia and Africa, which logically, are also the regions with the most potential patients. Historically, these regions saw the lowest percentage of patients having access to regular transfusions, drastically increasing the number of patients in need of another treatment. But these regions are also not as developed as the European Union or the United States, whether economically or healthcare system and coverage. Thus, we believe there is little to no chance that BlueBird can access these markets in the foreseeable future, even if the company tries to adapt its price while staying economically viable.

Apart from the economic repercussions from the EU withdrawal, BlueBird’s treatment is not suitable for more conservative and strict countries and areas when it comes to medical restrictions and policies.

The following statement is from the EMA (European Medicines Agency):

“Zynteglo is indicated for the treatment of patients 12 years and older with transfusion-dependent β-thalassemia (TDT) who do not have a β0 /β0 genotype, for whom hematopoietic stem cell (HSC) transplantation is appropriate but a human leukocyte antigen (HLA)-matched related HSC donor is not available (see sections 4.4 and 5.1).”

Surprisingly, when looking into the BLA (Biologics License Application) report for the Zynteglo in the U.S., we found out that the population included in the Phase 3 studies conducted by BlueBird showed profiles that were counter-indicated by the EMA’s guidelines. Indeed, more than 29% were of the β0 /β0 genotype and almost 40% were less than 12 years old.

Moreover, there are other contraindications that we mentioned earlier in the report, making the EU exclusion list for the Zynteglo substantially longer, and thus shrinking the number of eligible patients.

Not only does the withdrawal from the EU market drastically decrease the future economic prospects of the company, but it also gives competitors a comfortable way to gain more credibility and build a stronger global track record.

Additionally, while the company might be thinking of re-entering the European Market in the future, other competitors are soon to access it with multiple treatments. We believe competitors are using a more robust, more promising, more recent and most probably safer technology than BlueBird. We believe this withdrawal crushed any chances for the company to capture some market share, past, present and future, by being the earliest player.

Unprecedented high cost price points appear increasingly impractical, insurance reimbursement far from certain

We consulted with insurance experts and expect at least around 10% of patients to be refunded up to 80% of the treatment cost, according to the data presented from the latest clinical trials and BlueBird’s announced refund policy on Zynteglo, as they will not reach Transfusion Independence at all. Moreover, as discussed earlier in the report, ICER suggested a policy where BlueBird would refund patients failing to achieve TI during 5 years following the injection. It turns out that BlueBird only mentioned the price alignment with ICER with pride, but omitted to mention that they did not follow their guidance on the refund policy, taking it down to 2 years of achieving TI following the treatment. To us, this does not show confidence from BlueBird’s side, medically and economically.

We expect a revenue drag with the lovo-cel treatment for SCD, where the clinical data is still very small. The company also did not disclose any details in terms of pricing or reimbursement so far.

BlueBird has also been making very evasive and questionable claims around its Zynteglo treatment’s coverage by public and private insurances. Earlier in their development, one of the main concerns that investors had around the treatment was its price, already set to be very expensive. With the announcement of a price way over the general estimates and the ICER recommendation, the next challenge for the company would be to find agreements with insurers.

While trying to reassure investors through various presentations and press releases, the company made statements and claims that we found to be questionable and without real substance. The first step towards this was to ensure that most potentially eligible patients would be covered by insurance. But after discussing with experts in the healthcare insurance industry, our thoughts were confirmed and the general feedback after presenting these claims to them was: “These statements do not give any useful information or precision on the current situation whatsoever, they are too general and vague.” We present these statements and claims below:

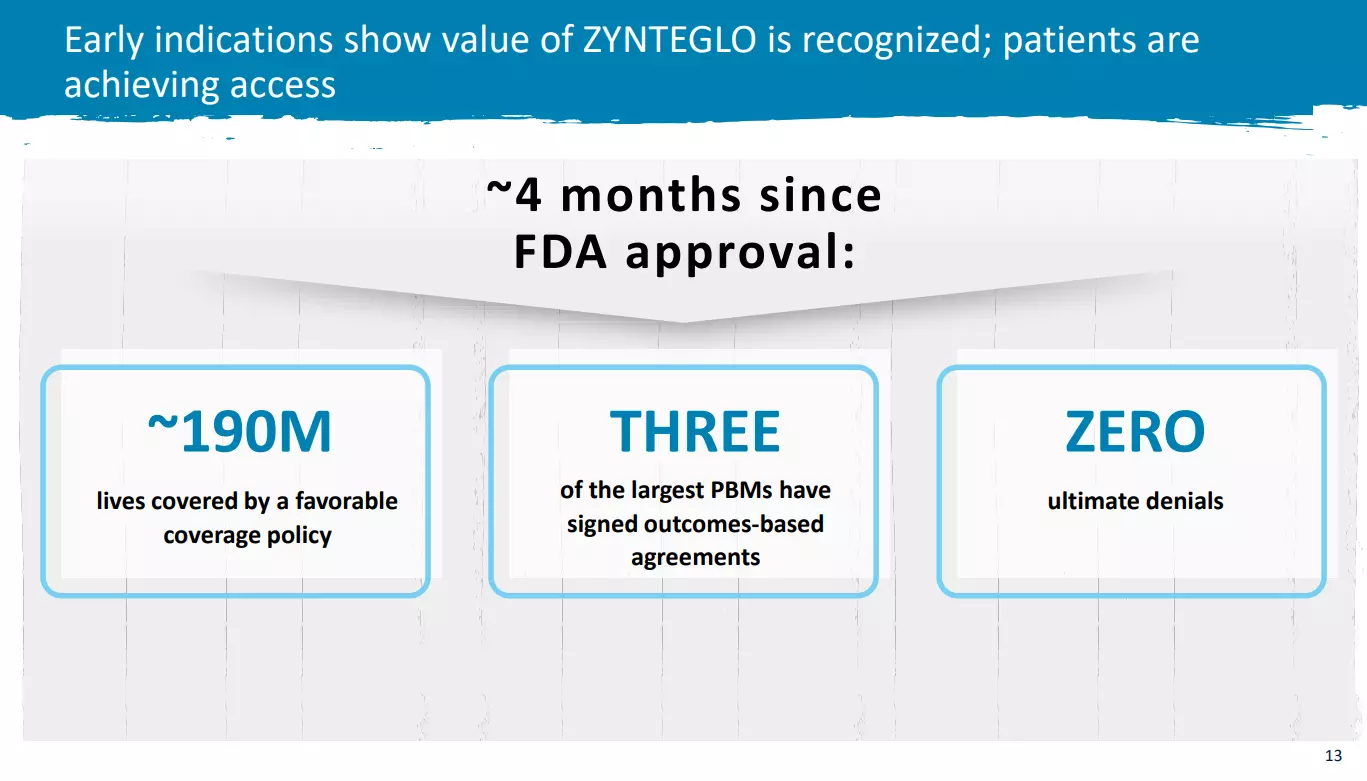

1. “Payers have expressed a deep understanding of the unmet need in transfusion-dependent beta-thalassemia, and the value of ZYNTEGLO. Approximately 70-75% of patients with transfusion-dependent beta-thalassemia are covered by commercial insurance, and BlueBird is currently in late-stage negotiations with leading commercial payers including national Pharmacy Benefit Managers (PBMs) with the potential to represent dozens of plans. Additionally, we are engaging with state Medicaid agencies representing approximately 80% of publicly insured thalassemia patients.” – Quote from BlueBird

In the first part of the paragraph, BlueBird states that most of its patients are covered by either a commercial insurance or by Medicaid agencies, as well as being in late-stage negotiations with leading commercial payers (PBMs). This is an almost useless set of information, as it is does not give any indication on the portion of potential patients actually covered for the treatment. Almost any other medical company could make a similar statement. The trick here is that BlueBird knows very well how hard it will be to reach an agreement with most insurers, whether it is public or private, and the current portion that is in reality covered is probably shockingly smaller. We reached the same conclusion with PBMs, which are really just intermediaries, having all the benefits without taking much risk, it is not surprising nor a big achievement to reach an agreement with them.

2.  Source: Latest Investor Presentation.

Source: Latest Investor Presentation.

We find the statements on the screenshot above to be even more laughable and void of meaning. In our opinion, they constitute a prime example of how BlueBird is desperately trying to come up with positive statements to keep investors hopeful in their slowly fading company. First of all, the statement “around 190M lives covered by a favorable coverage policy” is either an outright lie or a misleading statement. Indeed, the word “favorable”, here given without any context, might lead investors to believe that around 190M people have insurances that would cover Zynteglo. This is simply not true and not possible to determine at present. Further, the statement “Zero ultimate denials” is a total farce, as negotiations around the coverage of a treatment, especially treatment with a high price tag and covering rare diseases, can take months to years. BlueBird could easily “appeal” final decisions and offer alternatives in the future, putting the negotiations on hold, resulting in “zero ultimate denials” when in fact, they are just playing for time.

Uptake in trial enrollments very low

Source: January 2023 Investors Presentation

Source: January 2023 Investors Presentation

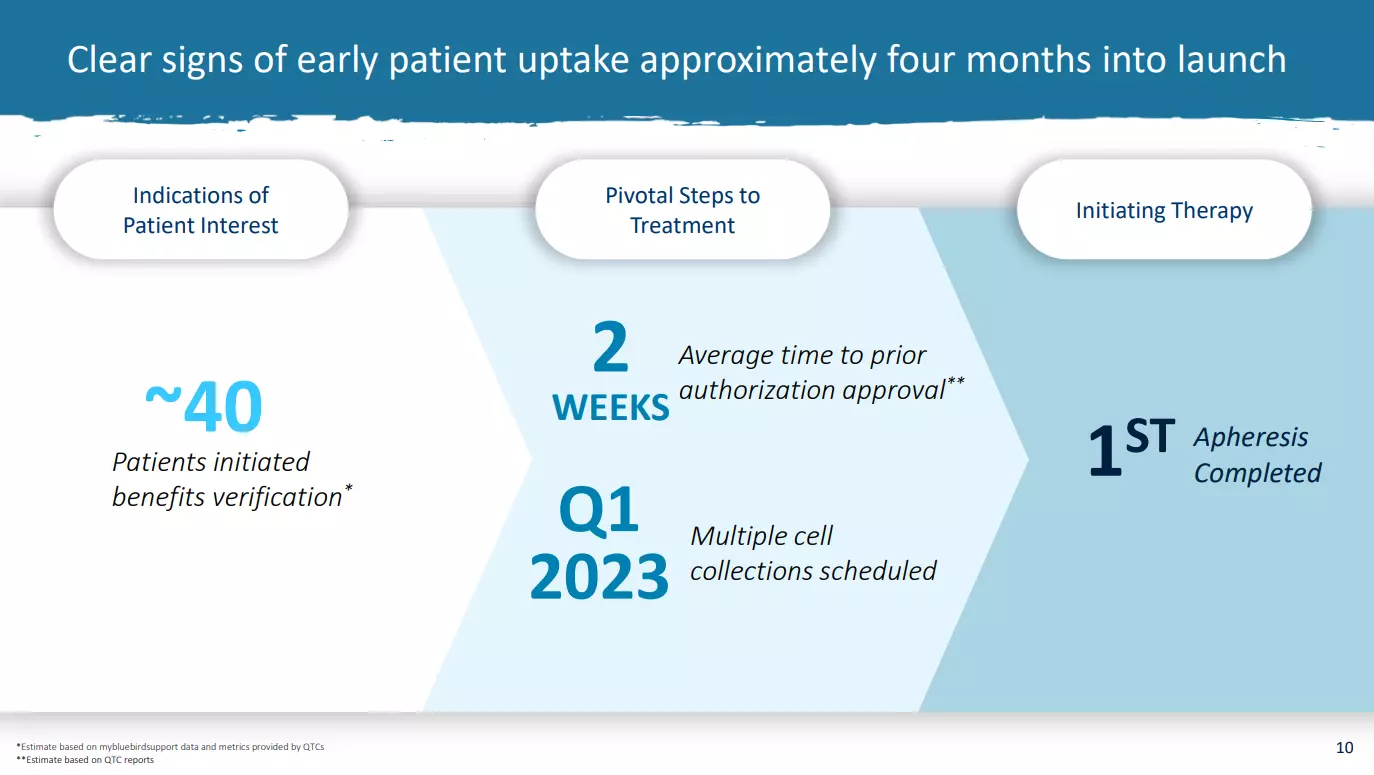

BlueBird told investors that there was “early indications of patient interest” when 40 patients “initiated benefits verification”. We view this statement and conclusion as simply ridiculous. First of all, we want to point out that benefits verification is a non-binding, very simple process for a person to get some information about the coverage of a treatment.

The Zynteglo treatment is supposedly “life-changing” for patients as it aims to cure a deadly and burdensome disease. Out of the supposedly 1500 patients, only around 2.5 to 3% initiated this simple verification process in 4 months? While, at the time, the company announced that their QTC network at the time could reach 50 patients, we still find it very odd and we wonder how BlueBird is even daring to present this number to investors.

Moreover, in their latest earnings call, the CCO & COO stated that:

“Yes. We really are pleased with how the launch is going, and we continue to see consistent volume of patients who are initiating benefits verification and moving through to the prior authorization phase. We at launch provided that as a metric because it was really the only thing that we had that was the indicator of demand. We’ve moved now to focusing on the number of patient starts. So those that have moved through that process and actually started therapy with the cell collection process. So we aren’t providing any updates. I will just say that we feel very strong about how things are going, and that number continues to increase and be steady.”

After announcing the very disappointing number of 40 having initiated benefits verification and finally converting only a handful of patients to initiate cell collection, the company decided to stop providing updates on that number, even though it is said to be consistent and increasing. We believe this is nothing but a ridiculous excuse to divert investors’ attention from the launch failure and the weak interest of patients in the two treatments.

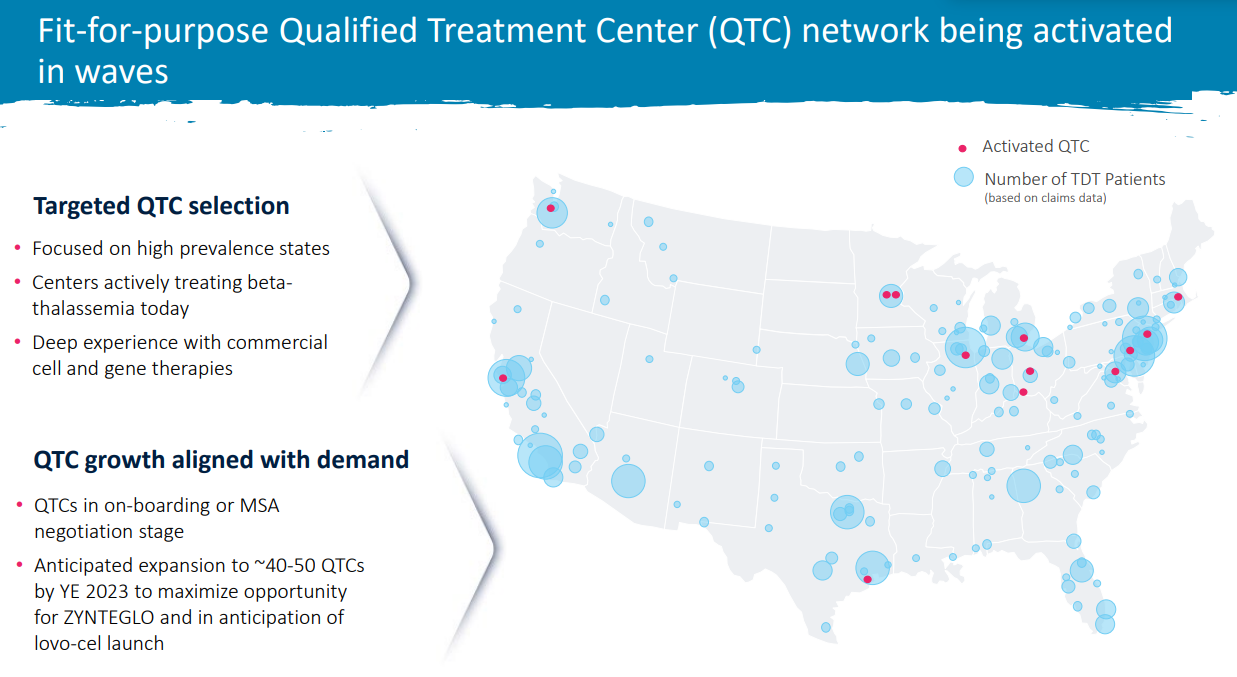

In addition, the screenshot below shows a map of the 13 activated QTCs locations along with the number of TDT patients, potentially eligible to receive Zynteglo. The company clearly shows and states that these early Qualified Treatment Centers are located near the areas with the most patients. Therefore, it makes sense to assume that the company is currently able to reach more than the 50 patients of the “Wave 1 of 5 QTCs” announced in their latest earnings call. Nevertheless, even though management stated during the BofA 2023 Healthcare Conference that the adoption curve would be linear with a current strong momentum, we do not see this happening. Moreover, why would the company not provide any numbers on patients having initiated benefits verification anymore? This would be the most relevant metric, as it allows tracking the adoption and conversion rate, which would strengthen the investors’ confidence in the insurance coverage and real patient interest.

Source: Company’s Investor Presentation

Source: Company’s Investor Presentation

- The market penetration for a first treatment that bears such high risks and costs for the patients, while there is an incoming better competition, will most likely keep being small, as people might want to have multiple options before being comfortable enough to make a decision. We already notice early signs of this scenario happening, with only 9 patients having started and/or completed cell collection as of May 9th 2023, across two treatments, with a very highly touted QTC network.

Cherry-picking clinical trial subsets to mislead investors about prospects

BlueBird Has Been Cherry-Picking and Arranging Its Clinical Trials Data to Portray a Brighter Truth than is reflected by Reality

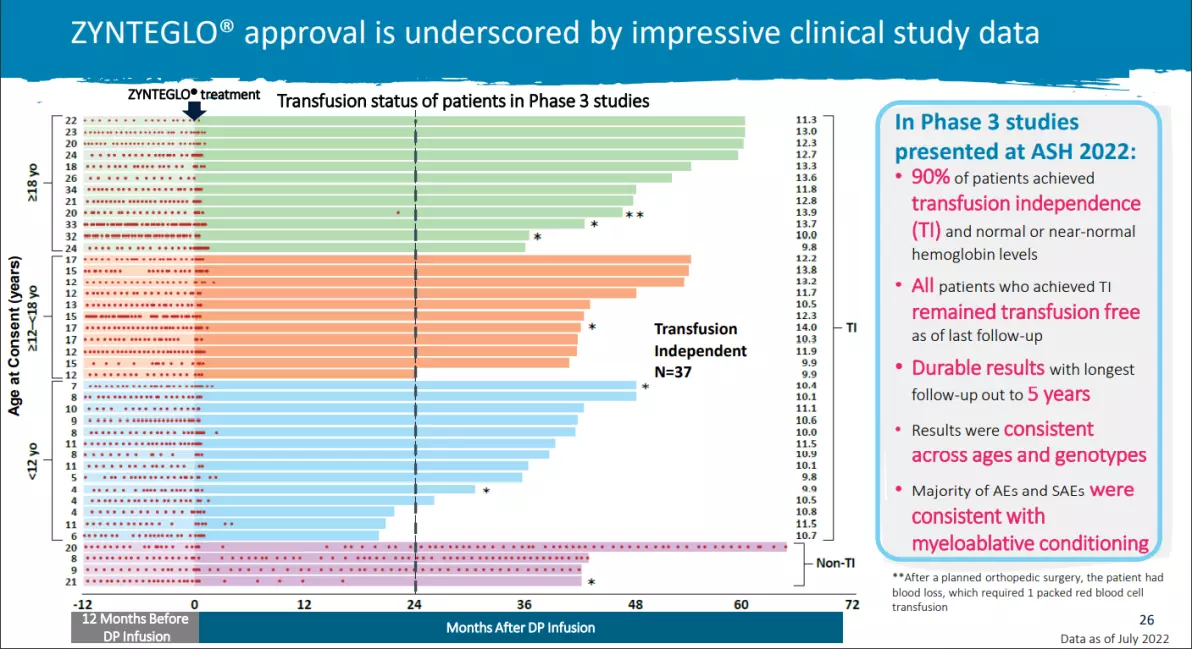

Discrepancies and inconsistencies abound in the company’s latest presentation, in which BlueBird showed “impressive clinical study data” of 41 patients across its two Phase 3 studies, with 90% of them achieving Transfusion Independence (TI). Note that the data is as of July 2022, where multiple patients were not evaluable as they did not reach the 24 months follow up required to achieve TI under BlueBird’s requirements. BlueBird still chose to include them in the 90% of patients that achieved it. As of May 2023, the same data is from July 2022 is still presented.

(Source: BlueBird’s Latest Investor Presentation)

(Source: BlueBird’s Latest Investor Presentation)

When it comes to the hemoglobin levels, BlueBird is boasting that 90% of patients achieved “normal or near-normal” levels. This is simply not true given the fact that BlueBird takes “11.5 g/dL” as their reference level. The median (11.5 g/dL) reached by patients following the Phase III studies and used as the reference level is actually the lower range of hemoglobin level for children aged 2 to 9 years old, as shown in the footnotes put by BlueBird’s themselves:

“Normal Hb ranges for healthy individuals from the American College of Clinical Pharmacy:

-

-

2–9 years: 11.5–14.5 g/dL

-

Males 10–17 years: 12.5–16.1 g/dL

-

Females 10–17 years: 12–15 g/dL

-

Male adults (≥18 years): 13.5–18 g/dL

-

Female adults (≥18 years): 12.5–16 g/dL”

-

Moreover, Transfusion Independence is defined by BlueBird as:

“A weighted average hemoglobin greater than or equal to 9 g/dL without any blood transfusions for a continuous period greater than or equal to 12 months.”

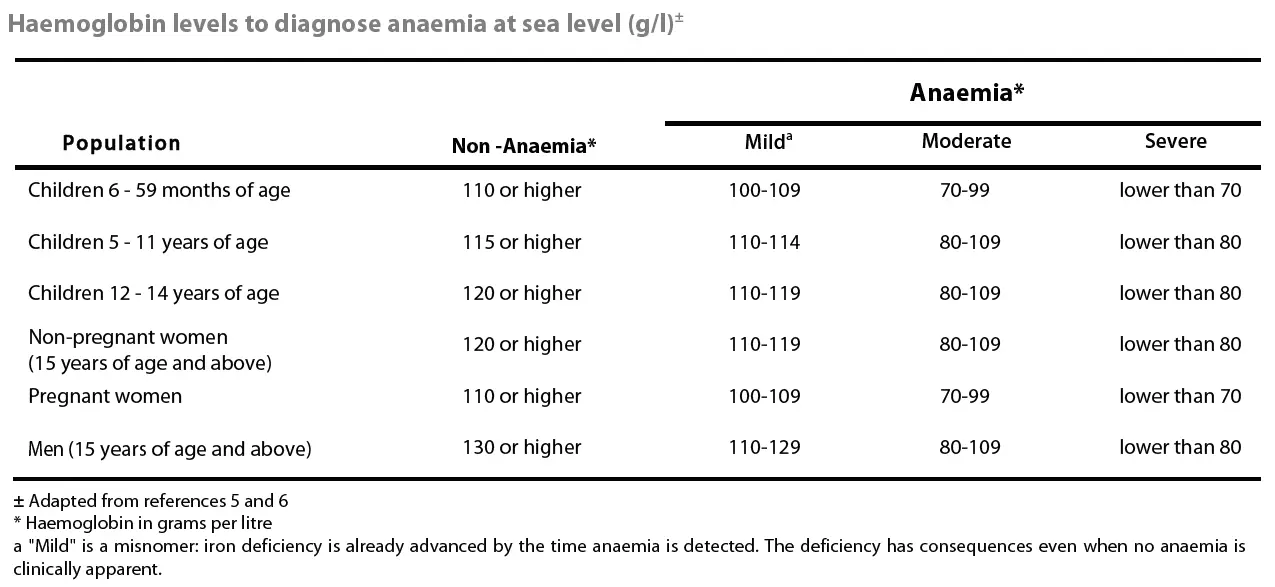

In reality, any person with this hemoglobin level, especially adult men, would be considered in severe anemia. Indeed, the WHO definitions of hemoglobin levels below 12 g/dL in nonpregnant women 15 years of age or older, below 11 g/dL in pregnant woman, and below 13 g/dL in men 15 years of age or older are widely used for diagnosis of anemia worldwide (Red Blood Cell Disorders. Amer Wahed MD, Amitava Dasgupta PhD, DABCC, in Hematology and Coagulation, 2015).

(Source: Haemoglobin concentrations for the diagnosis of anaemia and assessment of severity WHO/NMH/NHD/MNM/11.1.)

(Source: Haemoglobin concentrations for the diagnosis of anaemia and assessment of severity WHO/NMH/NHD/MNM/11.1.)

Anemia has a wide range of symptoms, including fatigue, increased or irregular heartbeat, feeling dizzy or light-headed, being short of breath, even when doing things you could usually do easily, etc.

We find it very misleading that BlueBird decided to take such a low level of hemoglobin as “near-normal” when it is definitely not the case, as patients are still in an anemic state.

Moreover, according to Drs Renzo Galanello and Raffaella Origa, Beta-thalassemia major form is characterized by reduced Hb level (<7 g/dl), and intermediate form is characterized by Hb level between 7 and 10 g/dl

(Renzo Galanello and Raffaella Origa, Beta-thalassemia, Orphanet J Rare Dis. 2010; 5: 11. Published online 2010 May 21. doi: 10.1186/1750-1172-5-11).

In the case where a person would go from 7 to 9 g/dL, which cannot be considered as very significant or life-changing, the patient would still be reaching TI according to BlueBird, but would still be considered in severe anemia by the medical consensus.

The patients’ genotypes also have to be taken into account because there are different severity levels of beta-thalassemia. While some patients treated with Zynteglo show acceptable levels of hemoglobin, BlueBird chose not to disclose their genotype or hemoglobin level prior to the clinical trials, which makes it impossible to assess whether the patients saw a significant increase in their hemoglobin level or not. As mentioned earlier, intermediate forms of beta-thalassemia are considered when the Hb level is between 7 and 10 g/dl, which could have been the starting point to a very low increase following the injection, but still considered a patient reaching TI.

Given the facts mentioned above, we believe that BlueBird chose to use clinical endpoints as well as a narrative that deflects the attention of the investors from the fact that patients treated with Zynteglo will not completely get rid of their disease, but will more likely have a “less aggressive and less inconvenient” one. According to the “normal levels of hemoglobin” given by BlueBird and from our other sources, it appears that more than 55% of the Phase III trial patients can still be considered in anemia state after receiving a Zynteglo injection. This also comes with uncertainty around the follow-up treatments, costs, and side effects. An example of this, which was stated by the company, is that some patients received phlebotomy and/or iron chelation following the treatment. We believe there are simply better solutions for patients.

BlueBird has lost their “early mover” advantage in this treatment space

The company has also recently submitted its BLA for the SCD treatment after the FDA requested additional information on vector and product analytical comparability. This severely impacted BlueBird’s sole advantage, which was to be ahead of the commercialization race. This drastically decreases the company’s future ability to capture the minor market share it could have hoped for.

The sole advantage BlueBird enjoyed was that they were the first company to have commercialized their treatments, although we do not believe it will help them capture a relevant and sufficient market share.

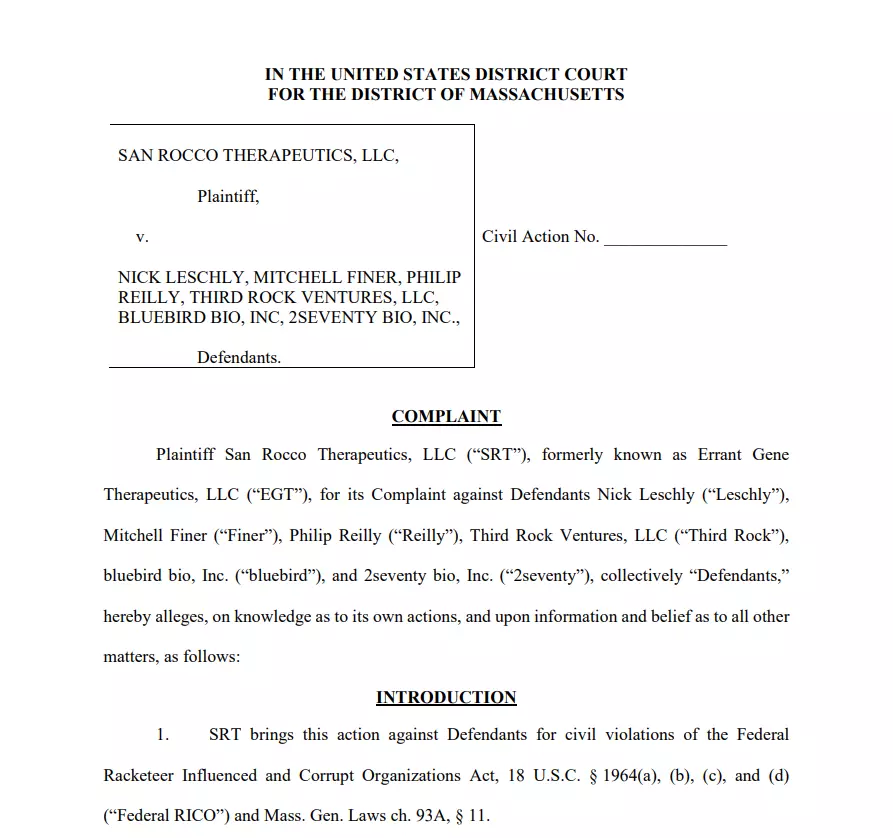

Pt 4 Longstanding legal battles over misappropriated /abused IP of other firms now coming to judgment, very unfavorably for BlueBird

We Believe the Company Deliberately Tried to Understate Its Legal Troubles to Investors, Which We Believe Could Seriously Impact the Company’s Future

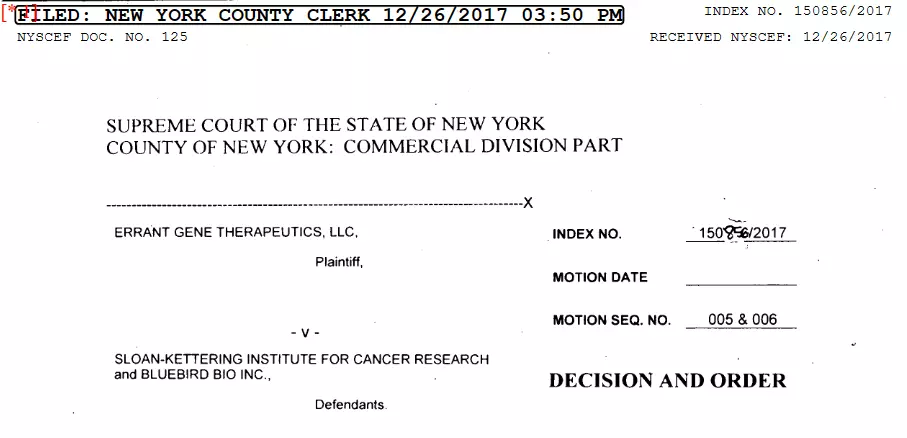

We found several red flags within BlueBird’s disclosure on its legal proceedings which lead us to think the company is not as confident on the matter as it appears to be. In fact, until the company released its 2021 10-K filing in March 2022, investors were not given any information about the fierce ongoing legal battle against San Rocco Therapeutics (SRT) that started in 2017. With multiple ongoing lawsuits and recent Arbitrator Award in favor of SRT, we believe BlueBird and its investors are facing enormous risks that could completely change and possibly end the company’s operations.

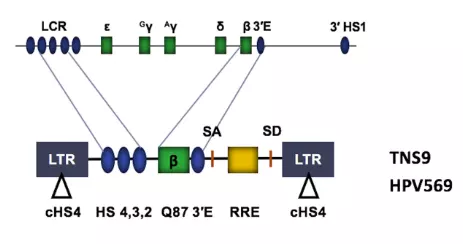

The lawsuits address patent claims. These patents specifically cover a vector (a target of drug delivery to specific intracellular structures), which are indispensable to the therapies developed by the company. We asked some experts to explain how important these vectors are, to find a more extensive explanation. (See Appendix 1 at end of this report for a more detailed explanation.) First and foremost, without the vector protected by these patents, BlueBird simply could not have developed these therapies. Indeed, the vector used such a key factor in the therapy that without it, as developed for the targeted pathology, the simplest flaw in the vector would make the therapy inefficient and therefore, completely useless.

2017 First Lawsuit and 2020 Settlement Agreement

In 2017, San Rocco Therapeutics (formerly Errant Gene Therapeutics) commenced a civil action against Sloan Kettering Institute (SKI) and BlueBird in the Supreme Court of the State of New York, entitled Errant Gene Therapeutics, LLC v. Sloan Kettering Institute for Cancer Research and BlueBird Bio, Inc., Index No. 150856/2017, alleging the following causes of action: fraud against SKI; breach of contract against SKI based on their 2011 Agreement; breach of contract against SKI based on their 2005 Agreement; civil conspiracy to defraud against SKI and BlueBird; unfair competition against BlueBird; injunctive relief against BlueBird; and unjust enrichment against BlueBird.

San Rocco Therapeutics is a biotechnology/biopharmaceutical research company and a worldwide leader in gene therapy. In 2000, SRT began financially supporting the research of Drs. Michel Sadelain and Stefano Rivella, both of whom were medical researchers and scientists at Memorial Sloan Kettering Cancer Center (“MSKCC”) and the Sloan Kettering Institute for Cancer Research (“SKI”), collectively “MSK”.

As a result of SRT’s unyielding commitment, it has successfully developed recombinant vectors that can be used in gene therapy treatment of rare genetic diseases, such as Sickle Cell Disease and Beta Thalassemia.

According to the lawsuit:

“In 2005 SRT signed with MSK for the worldwide commercial rights to, and purchased, Michel Sadelain’s gene therapy project for Sickle Cell Disease and Thalassemia, which afflicts Mr. Girondi’s son, Rocco. Under the 2005 Agreement, MSK granted SRT an exclusive license agreement to the intellectual property related to the lentiviral vectors invented by Drs. Sadelain and Rivella. SRT’s tireless efforts and work with Drs. Sadelain, Rivella and others, resulted in the development of the SRT’s TNS9 Vector for the treatment of Beta Thalassemia.

55. From 2005 to 2010 SRT invested several million dollars and, together with MSK,

improved the TNS9 Vector. From 2005–2009, SRT commandeered and paid for 55 iterations and modifications of lentiviral vectors that led to SRT’s TNS9 Vector.

56. SRT’s Director of Gene Therapy, Dr. Christopher Ballas, created an innovative and proprietary vector production and formulation process, which is worth in excess of hundreds of millions of dollars.”

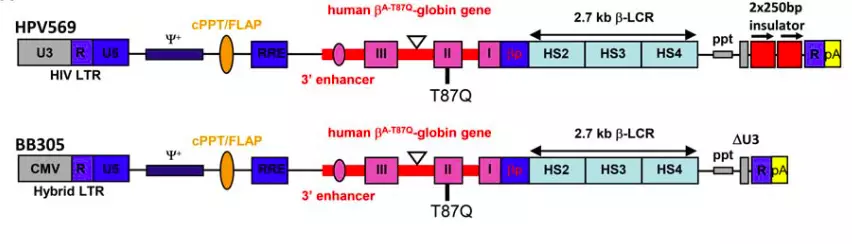

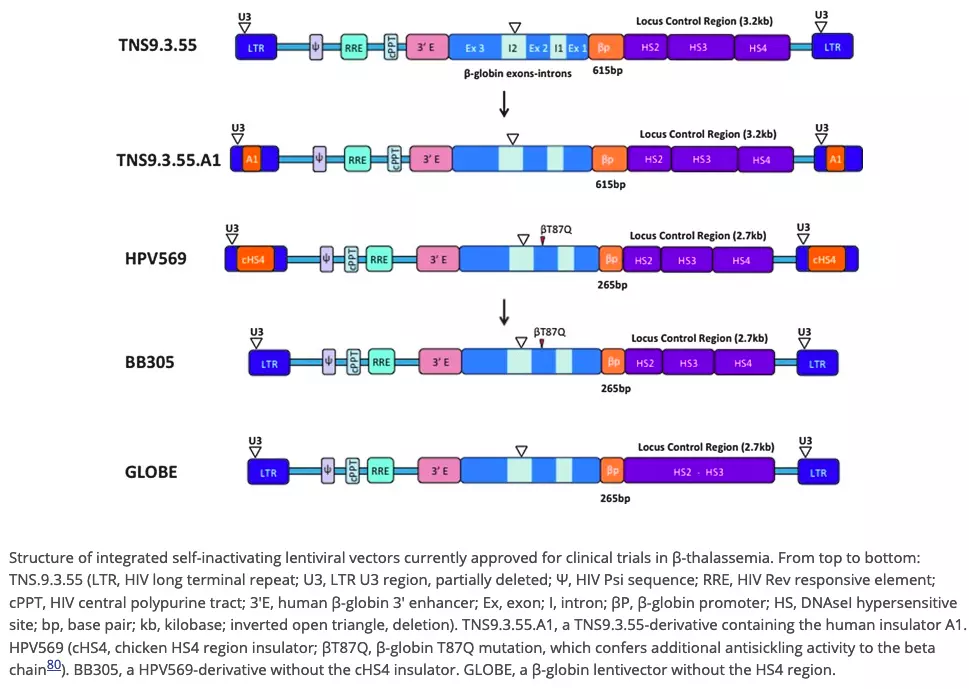

Like SRT’s TNS9 Vector, BlueBird’s (formerly Genetix’s) gene therapy relied on a vector delivery system. SRT and BlueBird are direct competitors. SRT’s TNS9 Vector was years ahead of the purported BB305 Vector in terms of development.

Unable to acquire the TNS9 Vector directly from SRT, Defendants BlueBird, Third Rock, Leschly, Finer, and Reilly entered into and engaged in a conspiracy to fraudulently induce SKI into an agreement where they fraudulently obtained samples of SRT’s clinical grade TNS9 Vector, which was part of their scheme to eliminate BlueBird’s only competitor and obtain FDA approval with market exclusivity ahead of SRT. (in 2011)”

On November 2020, SRT and BlueBird executed the “Settlement Agreement” in order to resolve all and any disputes between them. Following the execution of this agreement, SRT dismissed its complaint and stated that it received an “exclusive, royalty-free commercial license” to both U.S. patents related to the vector with exclusionary rights and all substantial rights. Moreover, SRT also stated that, “BlueBird was not granted any type of license, including, without limitation, a commercial license to the Patents. BlueBird has never had or has never been granted a commercial license to the Patents.”

However, the following year, SRT claimed that BlueBird started engaging in commercial activities with the “BB305 lentiviral vector” that infringe SRT’s Licensed Patents and therefore breached the agreement. In addition, this would mean that in September 2021, BlueBird completed the submission of its Biologics License Application to the FDA for its Infringing Drug Product, involving perjured testimony and concealing the correct identity of BlueBird’s purported “BB305 vector” approved by the FDA with orphan drug market exclusivity.

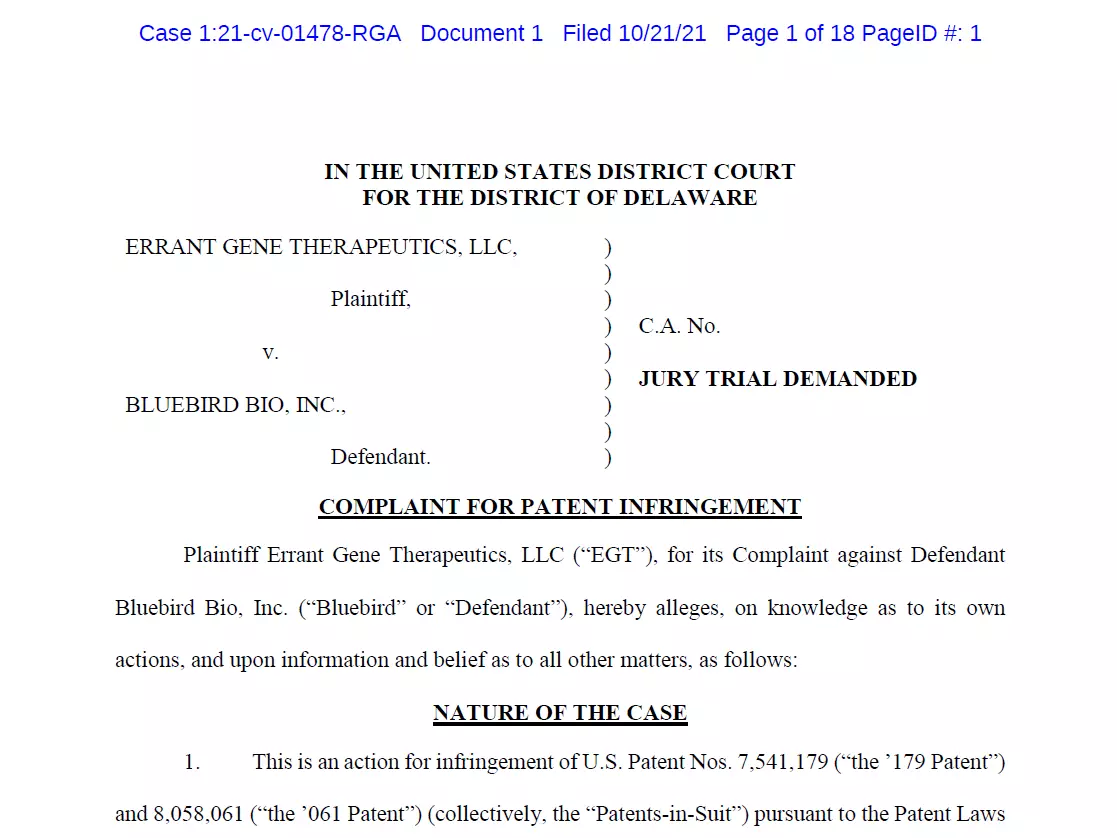

2021 Patent Infringement/Breach of Agreement Lawsuit

On October 21, 2021, SRT filed a complaint in the United States District Court for

the District of Delaware against BlueBird alleging willful infringement of the Licensed Patents, San Rocco Therapeutics, LLC v. BlueBird Bio, No. 21-1478 RGA (D. Del. Jul. 26, 2022) (the “Delaware Action”).

It appears that BlueBird has been cherry-picking some parts of the lawsuit progress. Indeed, in their past and recent filings, the company only mentioned having filed a motion to dismiss in April 2022 but omitted to mention the one they filed in January 2022, which was countered and granted to SRT:

January 2022 motion, not disclosed: “Following the initial complaint, on January 14, 2022, BlueBird and Third Rock filed a motion to dismiss or, alternatively, compel arbitration and stay the Delaware Action. SRT filed an unopposed motion for leave to file a Second Amended Complaint, on March 4, 2022, which was granted on March 7, 2022.”

April 2022 motion, disclosed: “On April 6, 2022, we—along with Third Rock Ventures, LLC—filed a motion seeking various relief including to stay the proceedings and compel arbitration on two threshold issues, which we argued warranted complete dismissal of the action as a matter of law, regardless of the merits of SRT’s underlying infringement claims.” This motion resulted in the recent Arbitrator Award in favor of SRT, mentioned below.

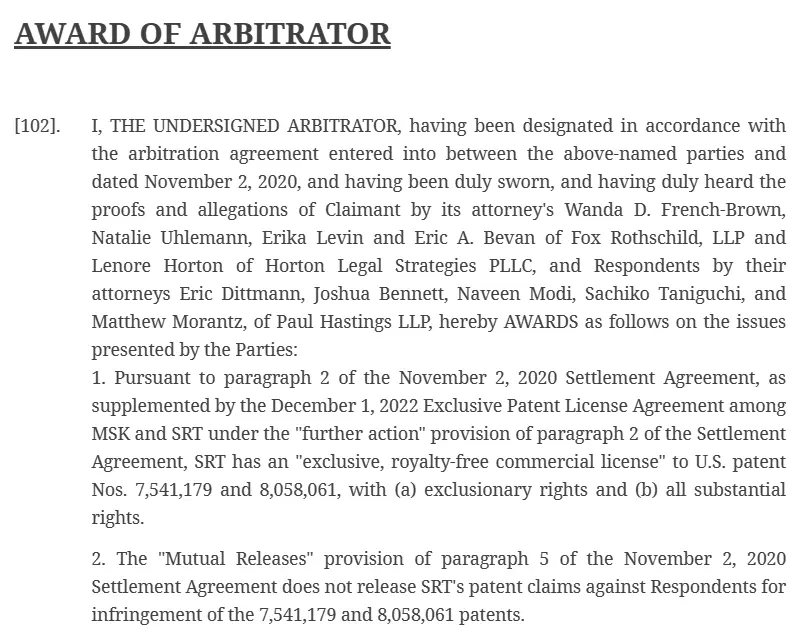

Below is a screenshot of the recent Arbitrator Award, in favor of SRT, stating that SRT has indeed an “exclusive, royalty-free commercial license” to both U.S. patents with exclusionary rights and all substantial rights. Note that this was filed recently, in February 7th, 2023. We believe this gives a substantial advantage to SRT in this legal battle.

In what we see as a final desperate move, BlueBird tried to invalidate the patents by filing petitions for inter party reviews with the PTAB, which was accepted last month. In our opinion, this seems to be BlueBird’s last straw.

2023 RICO Lawsuit

Following this award and the previous lawsuits, on April 27th, 2023, SRT filed an action for violations of federal RICO (Federal Racketeering and Corrupt Organizations Act), fraudulent inducement and unfair business practices in the United States District court for the District of Massachusetts against multiple defendants including the former CEO Nick Leschly, BlueBird Bio Inc., their spin-off and 2seventy Bio Inc. SRT is seeking “recoverable damages “business or property,” which is an amount in excess of $500 million or an amount otherwise determined at trial; and (iv) an amount to be decided at trial in the form of punitive damages for Defendants’ illegal and fraudulent actions.”

Source: United States District Court for the District of Massachusetts

Source: United States District Court for the District of Massachusetts

“After November 2, 2020, Defendants Leschly, Third Rock, Reilly, Finer, BlueBird, and 2seventy committed additional fraudulent and unlawful acts against SRT as part of their ongoing scheme involving fraudulent inducement of SRT in connection with the Settlement Agreement and the fraudulent spin-off of 2seventy — all of which were committed in furtherance of their objectives to shut down SRT, get ahead of BlueBird’s only competitor, and protect financial interests and earnings that resulted from Defendants’ predicate acts of racketeering activities.”

“In furtherance of their objectives, Defendants engaged in mail and wire fraud involving a scheme based on (i) theft of SRT’s trade secrets; (ii) fraudulent inducement of SRT in connection with the Settlement Agreement; and (iii) the fraudulent spin-off of 2seventy in order to protect financial gains and profits that resulted from their scheme to eliminate SRT as a competitor and obtain FDA approval with market exclusivity based on stolen unlawful competitive intelligence (confidential information).”

Again, we want to remind investors that this lawsuit was filed shortly after SRT got a favorable arbitrator award on its other lawsuit against BlueBird.

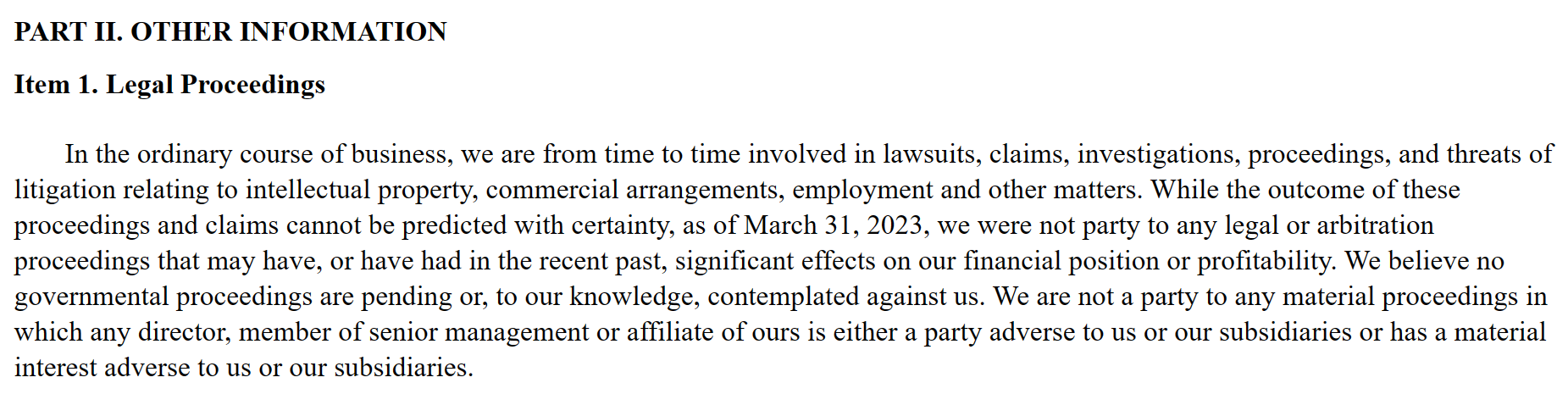

Disclosure Issues

Given the severity of the situation, we believe that any investor would want to understand this situation more clearly. But it is only briefly mentioned by BlueBird in its quarterly and annual filings. Moreover, we believe the company makes misleading statements in its latest 10-Q filings, given the current situation:

“While the outcome of these proceedings and claims cannot be predicted with certainty, as of March 31, 2023, we were not party to any legal or arbitration proceedings that may have, or have had in the recent past, significant effects on our financial position or profitability.”

For reference, the first instance where the legal proceedings against SRT appear in BlueBird’s filings is in March 2022 10-K, reporting for the year ended December 31, 2021. The company, for some unknown reason, did not, and still does not mention anything about the 2017 Lawsuit and the 2020 Settlement Agreement:

(Source: BlueBird SEC filings, 2021 10-K)

(Source: BlueBird SEC filings, 2021 10-K)

In the following quarterly and annual reports, the company gives a very simplified summary of the legal proceedings progress, mostly softening the narrative.

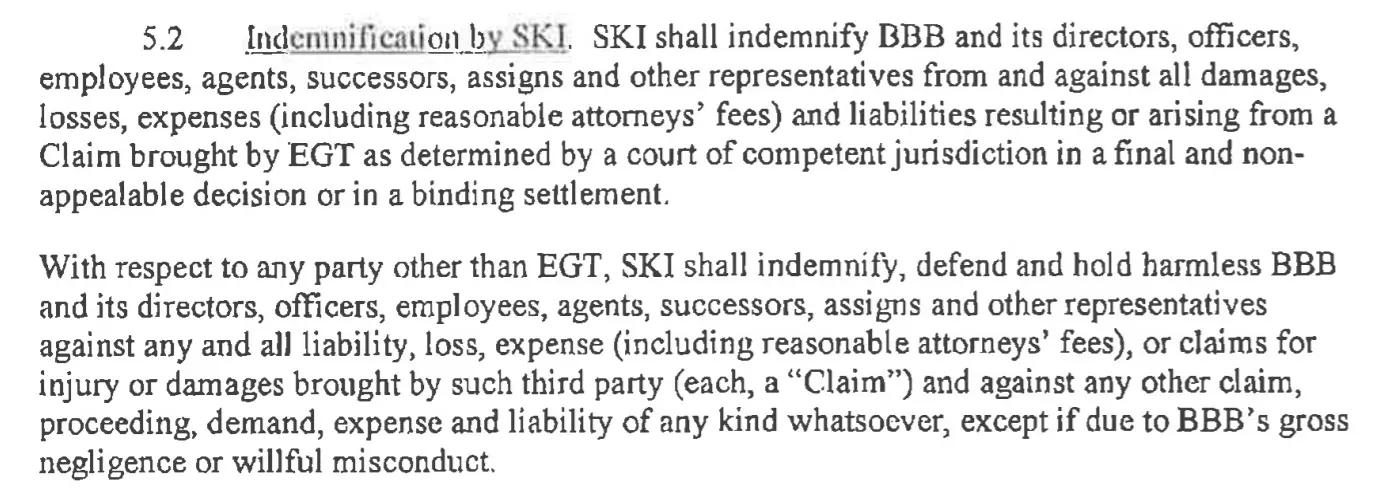

Perhaps BlueBird chose not to disclose this matter until now because they think they found themselves a loophole. It appears that there is, in the collaboration agreement signed in 2011 by BlueBird and Sloan Kettering Institute, a clause ordering Sloan Kettering Institute (a non-profit organization) to indemnify BlueBird from and against all damages arising from the case against EGT (former name of SRT). We find this extremely odd and believe this to be a huge red flag:

Source: Agreement Document

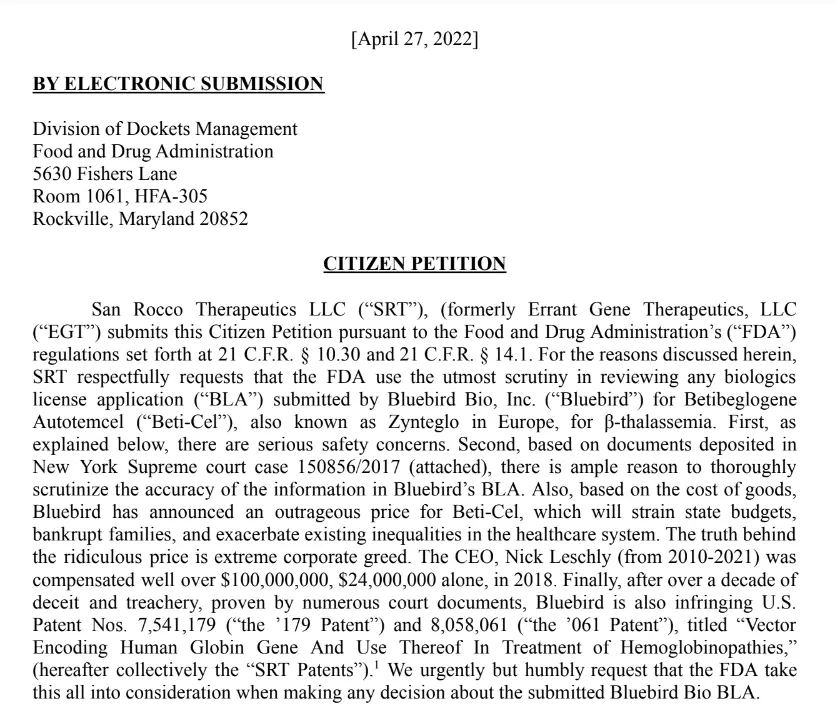

The company also omitted to mention that SRT submitted a Citizen Petition pursuant to the FDA regulations on April 17th, 2022.

Given the situation, we believe this to be a huge red flag, as investors should be more informed about what we consider to be an enormous risk. We advise investors to closely follow the progress of the lawsuits.

Pt 5 BlueBird’s tech is now old, and has been eclipsed by competitors

BlueBird’s Technology is Outdated and Competitor’s Technology is Way Safer and More Precise

Among the risks of technology eclipsed by direct competitors includes higher patient risks, due to broader scope of inclusions and more unpredictable side effects

Pt 5 Takeaways

- More side effects and exclusion criteria will arise over time. We see absolutely no upside in the treatment follow-ups, but rather increased financial and economic risks for the company

- The market penetration for a first treatment that bears such high risks and costs for the patients, while there is incoming better competition, will most likely continue to stress BlueBird’s uptake, as patients and their caregivers might want to consider multiple options before being confident enough to make a decision. We already notice early signs of this scenario happening, with only 9 patients having started and/or completed cell collection as of May 9th 2023, across two treatments, within a very highly touted QTC network.

Last year, after suffering a clinical hold amidst concerns of oncogenesis in patients that had received a Zynteglo injection, BlueBird attempted to reassure its investors by stating:

“In addition to our earlier findings of several well-known genetic mutations and gross chromosomal abnormalities commonly observed in AML in this patient, our latest analyses identified the integration site for the vector within a gene called VAMP4. VAMP4 has no known association with the development of AML nor with processes such as cellular proliferation or genome stability. Moreover, we see no significant gene misregulation attributable to the insertion event,” said Philip Gregory, chief scientific officer, BlueBird bio. “In totality, the data from our assessments provide important evidence demonstrating that it is very unlikely our BB305 lentiviral vector played a role in this case and we have shared with the FDA that we believe these results support lifting the clinical holds on our β-thalassemia and sickle cell disease programs.”

Even though the two patient deaths were not associated at this time with BlueBird’s treatment, because the integration in VAMP4 gene is not related to cancer development, this integration is not a rare event since at least 50% of patients exerted unspecific integration in the VAMP4 location. But it was not the unique unspecific integration since oncogenesis including BCR, XPO7, and CBFB have also been reported

(FDA Briefing Document. Cellular, Tissue, and Gene Therapies Advisory Committee Meeting June 9-10, 2022 BLA 125717 betibeglogene autotemcel Applicant: BlueBird bio, Inc.).”

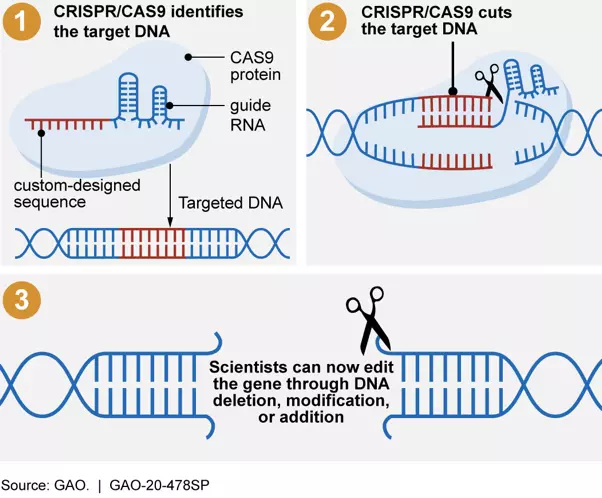

These results reflected the unspecific and uncontrolled integration site using old lentivirus technologies in contrast to the newer technology Crispr-Cas. The development of a targeted gene-drug insertion system nevertheless remains an essential objective for patient safety.

(FDA report)

The first gene therapies targeting humans, appeared in the 1990s, and use virus vector (i.e. Adenovirus or lentivirus) to deliver genes safely into cells. Based on this old process, BlueBird bio developed lentivirus gene transfer to treat rare diseases, however this technique did not allow specific gene integration into cells as demonstrated in the illustrations below (i.e. VAMP4 and BCR, XPO7, CBFB oncogenes)

(FDA Briefing Document. Cellular, Tissue, and Gene Therapies Advisory Committee Meeting June 9-10, 2022 BLA 125717 betibeglogene autotemcel Applicant: BlueBird bio, Inc.).

This uncontrolled integration may cause several unknown side effects to occur.

In contrast, BlueBird’s competitors targeting similar rare diseases are using the newest technology of gene editing called “CRISPR (-cas9, -cas12)” or “genetic scissor”. This CRISPR-Cas9 technology cuts the DNA strands to repair it. This approach, which requires two close cuts, consequently increases the specificity of the method and the integration.

(Fu Y, Sander JD, Reyon D, et al. Improving CRISPR-Cas nuclease specificity using truncated guide RNAs. Nat Biotechnology 2014; 32: 279–284).

This CRISPR/Cas system allows precise targeting of a gene, which greatly reduces off-target mutations and uncontrolled gene integration into cells compared to BlueBird’s technology foundation.

(Tan EP, Li Y, Velasco-Herrera Mdel C, et al. Off-target assessment of CRISPR-Cas9 guiding RNAs in human iPS and mouse ES cells. Genesis 2015 ; 53 : 225–236.).

Figure: At the Top – Illustration showing the Lentiviral gene integration process. At the Bottom- Illustration showing how CRISPR/CAS9 systems allow scientists to make targeted changes to an organism’s DNA.

Source: At the Top – (Lentiviral Vectors–the Promise of Gene Therapy Within Reach? Rafael G. Amado and Irvin S. Y. Chen Authors Info & Affiliations Science 30 Jul 1999 Vol 285, Issue 5428 pp. 674-676 DOI: 10.1126/science.285.5428.674)

At the Bottom – (Science & Tech Spotlight: CRISPR Gene Editing GAO-20-478SP Published: Apr 07, 2020).

The oncogenesis risk is not unknown to medical regulators and authorities, as mentioned in Zynteglo’s BLA review:

“11.6 Recommendations on Postmarketing Actions

The sponsor will conduct a PMR safety study. Upon consideration of the risks of LVV-based therapy, the previously considered registry-based analysis of spontaneous postmarketing adverse events reported under section 505(k)(1) of the Federal Food, Drug, and Cosmetic Act (FDCA) will not suffice. The pharmacovigilance system under section 505(k)(3) of the FDCA is also considered insufficient to assess this serious risk. Therefore, the Applicant will be required to conduct a postmarketing, prospective, multi-center, observational study to assess the long-term safety of betibeglogene autotemcel and the risk of secondary malignancies post ZYNTEGLO. This PMR study under Section 505(o) of FDCA will enroll at least 150 patients TDT, to be followed for 15 years after product administration. The study design will specify regular monitoring for clonal expansion with adequate testing methods.”

“Patients should be monitored at least annually for myelodysplasia, leukaemia, or lymphoma (including with a complete blood count) for 15 years post treatment with Zynteglo. If myelodysplasia, leukaemia, or lymphoma is detected in any patient who received Zynteglo, blood samples should be collected for integration site analysis.”

This exacerbated risk, while being the most important and concerning, is not the only aspect about the treatment that is worrying, as there are a lot of missing data around the post-treatment reactions and side-effects. These follow-up treatments will also mean extra risks and costs that patients will incur following the treatment.

The following statements were made by BlueBird themselves and are not extensive; we believe that more side-effects and exclusion criteria will arise with time:

“There are no data on the effects of Zynteglo on human fertility. Effects on male and female fertility have not been evaluated in animal studies. Data are available on the risk of infertility with myeloablative conditioning. It is therefore advised to cryopreserve semen or ova before treatment if possible.”

“No clinical data on exposed pregnancies are available. Reproductive and developmental toxicity studies with Zynteglo were not performed. Zynteglo must not be used during pregnancy because of myeloablative conditioning. It is unknown whether Zynteglo transduced cells have the potential to be transferred in utero to a fetus. There is no opportunity for germline transmission of the βA-T87Q -globin gene after treatment with Zynteglo, therefore the likelihood that an offspring would have general somatic expression of the β A-T87Q -globin gene is considered negligible.”

“Elderly Zynteglo has not been studied in patients >65 years of age. HSC transplantation must be appropriate for a patient with TDT to be treated with Zynteglo. No dose adjustment is required.”

“Renal impairment Zynteglo has not been studied in patients with renal impairment. Patients should be assessed for renal impairment defined as creatinine clearance ≤70 mL/min/1.73 m2 to ensure HSC transplantation is appropriate. No dose adjustment is required.”

“Hepatic impairment Zynteglo has not been studied in patients with hepatic impairment. Patients should be assessed for hepatic impairment to ensure HSC transplantation is appropriate. No dose adjustment is required.”

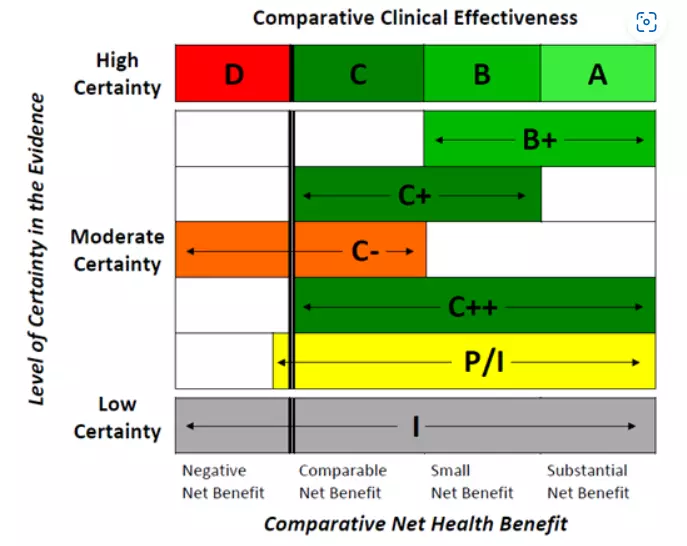

More recently, ICER published their preliminary report on the gene therapies targeting Sickle Cell Disease. The institute rated BlueBird’s lovo-cel a B+, while Vertex/CRISPR’s treatment got a C++ rating. While we respect and value their opinion, we believe the reasons for these ratings do not completely portray a “real-world” reality.

Indeed, BlueBird’s better rating mostly relies on the fact that it has a longer track record thanks to the two previous treatments that they got over the line (Zynteglo & Skysona). Moreover, while being less promising, the technology they use is older and thus, there is more data available. In reality, the clinical trials from both companies are relatively small, and still need long follow-ups to really prove their efficacy. Most experts and scientists in the industry agree on the fact that Vertex/CRISPR’s technology clearly outperforms BlueBird’s old technology.

We consulted multiple experts, including some who have been working for the French Institute Pasteur, which invented the technology BlueBird uses. The vast majority agreed that Bluebird’s technology only benefits from the fact that it has been around for longer, and thus is receiving a more favorable view and rating from the authorities, while in reality, CRISPR technology is far more promising. We believe doctors and patients will not blindly follow the ICER rating, and will most likely prefer CRISPR over BlueBird. The very low adoption of BlueBird’s current commercialized treatments is one of the most prominent indications confirming our belief.

Moreover, we uncover certain unsettling truths regarding ICER’s ratings for both treatments (Zynteglo and SCD). First of all, it is disclosed in the first few pages that some of the examiners received compensation or have had direct ties with BlueBird:

“Reviewer expert:

Sujit Sheth, MD

Professor Weill Cornell Medicine

Dr. Sheth has received salary or other payments for services such as consulting fees or honoraria in excess of $5,000 from BlueBird Bio, Bristol Myers Squibb (BMS), and Agios. Dr. Sheth has also received manufacturer support of research in thalassemia clinical trials conducted by BMS, Agios, Forma, and Imara.”

“Director, University of Alabama at Birmingham Adult Sickle Cell Clinic

Co-Director, Lifespan Comprehensive SCD Center, University of Alabama at Birmingham Associate Professor, Division of Hematology and Oncology

University of Alabama at Birmingham Medicine

Dr. Julie Kanter has consultancy relationships with Guide Point Global, GLG, Novartis, BlueBird Bio, GlaxoSmithKline, Graphite bio, Glycomimetics, and Johnson and Johnson.”

Moreover, for some reasons, the chart displaying the interpretation of the ratings, C++ (Vertex/CRISPR’s rating) is appearing below C-, while being in fact, superior:

Source: ICER website

Source: ICER website

When looking at the footnote, the ratings read as follows:

- C+ = “Comparable or Incremental” – Moderate certainty of a comparable or small net health benefit, with high certainty of at least a comparable net health benefit”

- C- = “Comparable or Inferior” – Moderate certainty that the net health benefit is either comparable or inferior, with high certainty of at best a comparable net health benefit “

- C++ = “Comparable or Better” – Moderate certainty of a comparable, small, or substantial net health benefit, with high certainty of at least a comparable net health benefit “

- P/I = “Promising but Inconclusive” – Moderate certainty of a small or substantial net health benefit, small likelihood of a negative net health benefit”

This might induce confusion in the appreciation of certain companies that would receive this newer “C++” rating, which would be Vertex/CRISPR’s case here. Logically, C++ should appear right under B+ on this chart, but appears just above “P/I”.

Pt 6 Changes to competitive landscape

There is every reason to expect a decrease in patient interests, who might turn towards more conventional medicine, such as Reblozyl (Bristol Myers Squibb), which received approval by the FDA in November 2019 for the treatment of anemia in adult patients with beta thalassemia who require RBC transfusions. There are also other more recent treatments targeting the diseases treated by BlueBird such as Endari (Emmaus Life Sciences), Oxbryta (Pfizer) or Adakveo (Novartis) for SCD.

We could argue that patients want to take their time for such an important decision and that some of them would also want to get more data and results from the treatment. But this is even more problematic for the company when multiple competitors are close to also obtaining the final authorization from the FDA, coming with better quality treatments. We strongly believe that BlueBird will not be able to capture as much market share as they assume.

Pt 7 Other uncategorized risks to future revenues

BlueBird is also using patents and technologies from many medical institutions and medical companies where they will have to pay some royalties upon commercialization of their treatments, based on their net sales. There are multiple agreements which all require “low single digits” royalties, we can assume around 10% of the net sales will be extracted from BlueBird’s revenue stream, another economic hit for the company.