- Sigma Lithium Corp. (NASDAQ: SGML) is a development-stage lithium mining company focused on advancing its Grota do Cirilo Project to production in Minas Gerais, Brazil. SGML has coasted a boom in lithium prices to a >26x return over the last 3 years, with the stock surging another 200% over last 12 months on speculation of a buyout ahead of production commencing.

- Though several large mining players have been rumored with an SGML takeover, reported interest from Tesla has generated the most investor enthusiasm. We believe a Tesla bid is highly unlikely given Elon’s focus on refining and preference for clay minerals available in Nevada over conventional spodumene, as well as the availability of less risky offtake agreements which are standard for OEMs.

- Amongst other misrepresentations, we find SGML’s claims of “Greentech” and “Green Mining” to be fickle. SGML has allocated minimal capital to R&D over the years. The Company lacks innovation Elon so often searches for in acquisitions.

- We agree there may be suitors for SGML but not at the current price. We consulted experts who all considered a $2-3B acquisition price more realistic. Trading at a ~56% premium to this target, the current stock price is unsupported by demand from leading mining companies. For example, despite prioritizing the purchase of a producing lithium mine, Rio Tinto supposedly passed on SGML due to the company’s outrageous asking price.

- Rio Tinto passed, then Tesla dodged, but that hasn’t broken the rumor mill. As recently as yesterday, SGML shares jumped ~9% on a reports that Tianqi Lithium (SHE: 002466) and Gangfeng Lithium (SHE: 002460), which also has ties to Tesla, were mulling a bid for the company. This strikes us as more misplaced speculation. Last year the Canadian government clamped down on Chinese investment in its companies in critical sectors. In one highly comparable case, this policy resulted in Lithium Chile (TSXV: LITH), a Canadian company operating entirely in South America, losing its major shareholder, Chengze Lithium.

- Even ignoring the low likelihood of the Company being sold, we seriously doubt SGML has the resources required to deliver on the project which has already been delayed multiple times. Our report timelines SGML’s history of production delays with production originally slated to begin in 2019!

- In January 2023, SGML lost Japanese industry giant Mitsui & Co. as a client when Mitsui terminated a 2019 pre-agreement and investment deal in January 2023. Mitsui promptly signed a deal with Atlas Lithium Corp. (NASDAQ: ATLX), another pre-production lithium miner with a much smaller market cap. We find it telling that large companies keep ducking SGML.

- We engaged local Brazilian mining experts to review SGML’s permits and licenses. These professionals identified SGML is still missing key environmental licenses which it must secure to meet its April 2023 production deadline. How can SGML be so confident in its production schedule if it has yet to secure all required licenses?

- Our conversations with industry experts and company insiders suggest SGML lacks leadership and technical expertise required to effectively run the mine. Insiders told us SGML is “lacking PhDs” and its Toronto executives are actually “investment promoters”. We are also concerned that SGML’s co-CEOs are a divorced couple and CEO Ana Cabral has no background in mining.

- SGML’s valuation has been buoyed by feasibility studies which assume lithium prices ~87% above figures in reputable industry studies. We question these studies which have been repeatedly updated to include even more aggressive assumptions. SGML’s investor materials are deliberately vague on prices used in calculations.

- At Tesla’s March 2023 Investor Day, Elon described lithium as one of Earth’s most abundant minerals. With this in mind, we’d characterize lithium mining as a “race to production” during the short years in which supply remains constrained. Against this reality, we believe SGML has intentionally overstated the speed at which it can ramp production to convince investors they can be an early mover.

- We see many underappreciated risks with SGML’s operations including forced/child labor concerns. We also question the positive impact the company claims to be making as they seem to be paying workers below minimum wage.

- It is our view that the Groto do Cirlo Project will require substantially higher CapEx than projected. Based on its current burn rate, we estimate the company will run out of cash if it does not begin to generate revenue within 2 years.

- All told, we agree with SGML’s insiders who have realized gains of CAD29.3 million through net sales of 924,100 shares in 2H22 and 2023. Based on expert opinions on the valuation in a buyout scenario and concerns we have highlighted above, we see ~50-75% downside in shares of SGML.

Background

Sigma Lithium Corp (SGML) is a lithium miner operating in Brazil. SGML’s stock experienced a spectacular surge amidst rising lithium prices, despite being in the pre-production stage.

The company has been in the news lately due to buyout rumors. We consider this speculation misplaced. Not only do we believe a deal is unlikely to materialize, we also have identified numerous red flags with SGML’s operations.

Despite the Hype, Nobody Wants to Buy SGML

Investors gossiped about an SGML buyout for several months before Tesla became the key piece of the story. On Friday, February 17, 2023, Bloomberg reported Tesla was weighing a takeover bid. Shares jumped 25% after hours on the news. Insiders told us a bid in the “$2bn – $3bn range” was most likely on the table.

Just weeks after the Bloomberg article, on March 1, Tesla hosted its Investor Day. Modest speculation that the news could be announced during the event ultimately disappointed. While Tesla’s CEO Elon Musk is known for his progressive leadership, he explicitly stated they are focused on the refining part of the supply chain. He did not address rumors surrounding SGML or purchasing a mine.

“There is no country that has a monopoly on lithium, or even close to it. (…) The limiting factor is the refining of the lithium into battery grade lithium hydroxide or lithium carbonate, that’s the actual limiting factor.” (Tesla Investor Day Presentation, March 1st, 2023)

“The lithium refining business is a license to print money.” (2nd Tesla earnings call, July 2022)

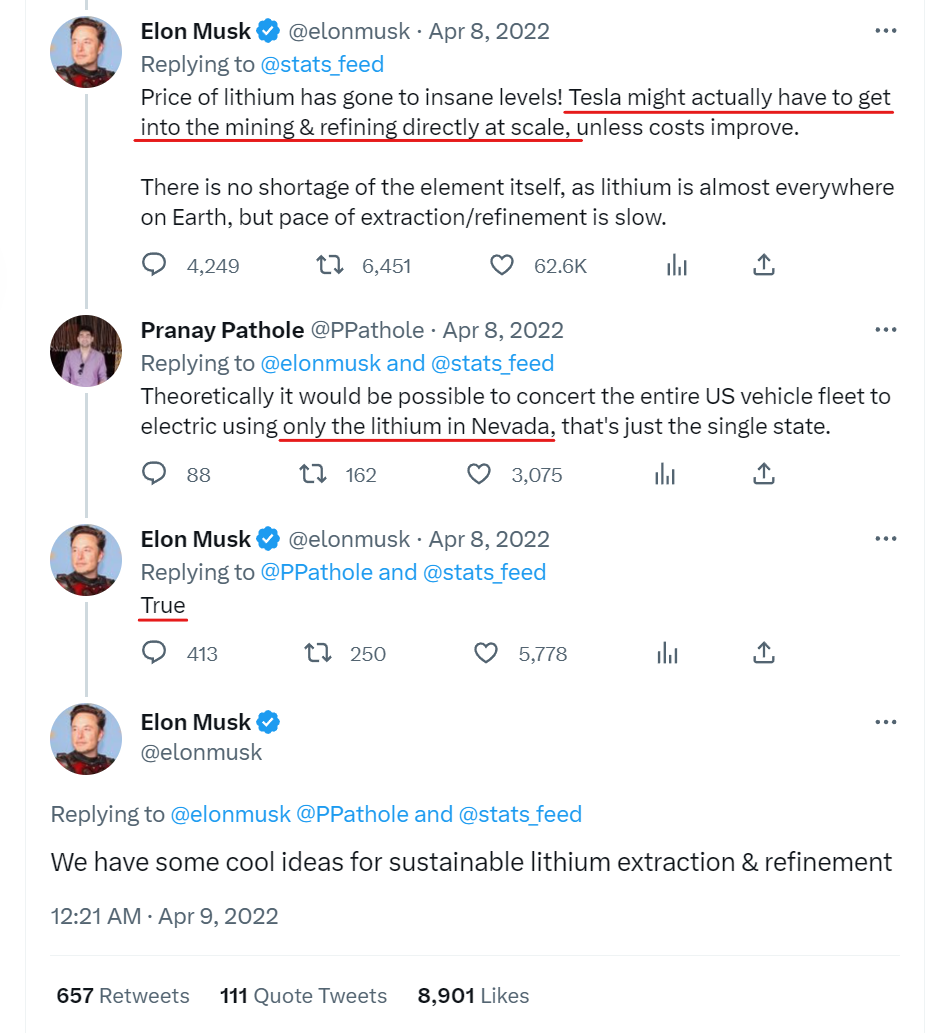

Elon has said multiple times that the issue with lithium is not its availability, but the pace of extraction and refinement. We interviewed multiple experts who unanimously agreed with his view, and SGML’s CEO mentioned this fact in a recent interview, as well.

Musk tweeted in April 2022, looking more to Nevada than Brazil:

We think there are several factors that cast doubt on the potential of Tesla buying SGML, even in the long term.

Elon is known to prefer to invest in innovative businesses. While SGML likes to bring up buzzwords like “Greentech”, there is no real innovation to show for (discussed later in the report). The company has spent virtually nothing on Research and Development in its entire history. This lack of investment would indicate that there is no differentiated technology or innovation of any kind. In a very recent March 2023 interview, SGML’s CEO even admits that the company’s approach to Greentech is “not innovative, not disruptive” at all. Meanwhile, Elon has turned his eye toward new solutions extracting lithium from clay minerals instead of mining for Spodumene.

Musk on Investor Day (“Battery Day”) presentation in September 2020:

“What is the best way to take the ore and extract the lithium and do so in an environmentally-friendly way? We have been looking at from a first principle physic standpoint instead of just the way it has always been done. We found that we can actually use table salt, sodium chloride, to basically extract the lithium from the ore. Nobody has done this before to the best of my knowledge.

(…)

Processes for extracting lithium from a clay mineral and compositions thereof are described. The extraction process includes providing a clay mineral comprising lithium, mixing a cation source with the clay mineral, performing a high-energy mill of the clay mineral, and performing a liquid leach to obtain a lithium rich leach solution.”

Location is also an important factor to Tesla, which makes SGML an even less compelling target for the company. As we will expand upon, we believe the Brazilian political environment is another relevant risk factor which should not be underestimated. Musk is known to welcome political debates, whereas the particular left- and right-wing polarization in Brazil can cause additional instability. In his role as Twitter’s new owner, Musk implied unfair dealings of Twitter in favor of Brazilian victorious presidential candidate Lula da Silva. Before that the defeated former president Bolsonaro solicited Musk directly calling his engagement at Twitter a “breath of hope” (Reuters). Brazil scores at rank 94/180 in the corruption perceiption index (2022) far behind developed nations. If Musk would invest into facilities that may raise environmental concerns or issues regarding the workers well-being, with the administration controlled by a political opponent, we see additional risk related to approvals and law suits.

We found rumors of an offtake agreement between Tesla and SGML from as early as September 2019 (Reuters), but nothing has materialized yet. Why would Tesla be interested in buying the company if they are not even interested in a supply agreement?

Don’t take it just from us. When asked about Tesla buying a mine, Goldman Sachs’ Head of Commodities predicted car manufacturers acquiring mining companies will “end in tears”. He explains: “Going in and being involved in mining projects in places like Southern Africa, it requires an expertise that is very different than producing cars.”

While we strongly doubt an acquisition of SGML by Tesla will ever happen, we also believe that a range of red flags and misrepresentations make SGML fundamentally unattractive, even for an alternative suitor.

Rumors of an SGML buyout have also stemmed from reports that mining giants like Glencore and Rio Tinto are actively looking to acquire lithium miners. And indeed, on paper, SGML seems to be an attractive target for a Rio Tinto because it has supposedly large deposits which can be extracted economically and it has forecast production will begin in April 2023. While it may check some boxes, we believe SGML is riddled with flaws which make it unattractive for potential buyers even at a fraction of the current value. We suspect sophisticated acquirers are seeing these issues while retail shareholders recklessly bid up SGML’s stock price.

The acquisition talks are only one of the indications that SGML’s executives are seeking to exit the company. In further sections, we elaborate on the reasons we believe they are desperate to sell the company including overpromising and lack of human, as well es financial resources to develop the mine.

SGML Already Lost Japanese Industry Giant Mitsui & Co. as a Client

In April 2019, SGML received US$30 million in financial backing from Japan’s Mitsui & Co to build a spodumene concentrate processing plant at its Grota do Cirilo Project. SGML confirms Mitsui already paid over $3m to SGML for this agreement.

However, on November 18, 2022, just days before the company submitted their latest feasibility study to the Brazilian regulator, the agreement was terminated, and SGML had to return the $3m to the counterparty.

SGML made it sound like this action was taken due to higher product prices, but on January 18, 2023, just 2 months after terminating the off-take agreement with SGML, Mitsui seems to have signed a new agreement with another Brazilian lithium miner, Altas Lithium Corporation. This agreement has an even higher total funding amount of $65m.

Atlas Lithium Corporation (NASDAQ: ATLX) is a pre-production company as well, but they seem to have even more mining assets than SGML. However, ATLX is only valued at $81 million market cap, and they are supposedly well behind SGML in the production schedule. For some reason, Mitsui, which is a reputable $46B company, opted to terminate their SGML off-take agreement and sign one with Atlas.

So, SGML used to have two agreements with major corporations. Now they just have one left. Will LG Energy Solution (“LGES”) also soon cancel? LGES is already shopping around for other suppliers. In July 2022, LGES signed an offtake agreement with U.S. lithium provider Compass Minerals. In September 2022, LGES entered into agreements for lithium supply from SGML’s Canadian competitors Snow Lake Resources and Avalon Advanced Materials. In February 2023, LGES’ recent parent LG Chem signed offtake agreements with Piedmont Lithium for a total of 200,000 metric tons of spodumene concentrate (SC6). In a market where new supply is coming rapidly online, these other agreements sound like a vote of distrust in SGML to us.

We Believe the Management Team is Ill-Suited to Ramp Up Production

It is never good for management teams to be in disarray, especially when talks of a sale are ongoing. These problems are compounded when management is in a hurry to sell. We believe this rush to strike a deal may have prompted management to misrepresent its financial situation to investors. Our suspicions are supported by several red flags we have identified in management’s backgrounds.

Divorced Co-CEOs are not a Good Sign

SGML is really the vision of its two co-CEOs Ana Cabral-Gardner and Calvyn Gardner. According to to Brazilian corporate records, Calvyn originally formed the company in 2012. Calvyn has an impressive mining CV, while Ana brought in an investment banking background and financial expertise when she joined in 2017. With this combination, it seemed like the two could be a real power couple.

Unfortunately, their personal relationships have created a cloud over the company. We found an interview in Brazil where Ana states that they have two children together and are currently divorced. We reached out to insiders and people close to SGML, but received unclear responses on their relationship, with most refusing to comment directly.

To clarify, we do not believe the intricacies of the co-CEOs’ divorce should be made public and we wish no harm on their relationship. That said, we think the relationship poses unnecessarily negative implications on the working environment, as well merger negotiations.

We believe Ana’s sole focus is personal gain and do not buy that she has the skills to ramp production. She is the Co-Founder and Managing Partner of A10 Investimentos, SGML’s largest shareholder. A10 Investimentos also owns the SPAC (Special Purpose Acquisition Company) with the ticker XPAC. We found that a company called XP Investimentos is entitled to $2.3m of advisory fees in the event of a business combination. XP Investimentos is a Brazilian brokerage firm that has a questionable line of officers. These individuals were sued on multiple accounts for fundraising violations under SEC Rule 505:

- Failing to disclose R$100M of “system failures and order execution errors.”

- Failing to disclose they were a part of an increasing number of legal proceedings in Brazil.

- Failing to disclose they were the target of multiple regulatory investigations. – page 2

CFO Track Record Littered with Regulatory Issues

CFO Rodrigo Nazareth Menck CFO was previously an executive and board member at Oderbrecht, a large mining company. While Menck was Director, “dozens” of Oderbrecht executives were arrested, including the CEO for bribing politicians and officials in exchange for contracts with Petrobas (April 2019). Oderbrecht paid $3.5B USD to Swiss, Brazilian, and US authorities to settle. Oderbrecht was also sued for human trafficking and maintaining slave labor conditions for their Angola operations.

Rodrigo Menck recently resigned as CFO of Nexa Resources S.A in June. Nexa’s CEO was formerly a Director who was fined R$500k for failing to disclose loans while he was a Director at Vale.

Insiders Are Selling

SGML’s own management team seems to agree with our view that the current stock price is overstretched. Why else would you sell stock aggressively this close to production start in April 2023? We also note that news articles quoted people familiar with the matter who said that Rio Tinto is not interested in a deal due to a high asking price. An insider we interviewed confirmed this to us. If potential acquirers and insiders deem the company too expensive, why should public investors keep buying the stock?

Insider Transactions at SGML (Bloomberg)

We Believe SGML Is Fundamentally Overvalued – Management Misrepresents Economics

We agree with management that is selling stock and do not see fundamentals to support SGML’s current valuation. Today’s stock price is based on future expectations about the economics of the mine which we believe are totally unwarranted.

SGML’s Current Stock Market Valuation Far Exceeds the Bid Offers by Rio Tinto or Tesla

Typically, when a large competitor acquires a company, the target receives a premium above its market valuation to account for strategic gains and synergies the buyer receives. An extensive academic study for the Australian and Canadian mining industry revealed historical acquisition premiums of 71.8% (mean in Australia) and 54.2% (mean in Canada). You would expect this to hold true for a potential buyout of SGML from any large mining player.

We consulted several insiders about the valuation at which a rumored takeover would occur. One of the insiders we spoke to represented multiple potential buyers in initial conversations with SGML in 2022. He quoted a price of “2 to 3 billion USD” for all of SGML as the most optimistic realistic outcome. Assuming a 50% premium gets you to the midpoint valuation above, we would expect buyers to be interested in acquiring SGML for market cap of $1.66B. The actual current market cap is $3.9B, an overvaluation of 134%.

New Rumors About a Completely Unrealistic Buy-Out from China

On March 17, 2023 yet another take-over rumor appeared: the American business analytics company ION published the “Breaking News” that “Hong Kong- and Shenzhen-listed lithium producer Tianqi Lithium (SHE: 002466) is in talks to acquire all of private-equity-backed Toronto- and NASDAQ-listed Sigma Lithium Corp’s mines, according to three sources familiar with the matter and a source with knowledge of the matter. Jiangxi, China-headquartered Ganfeng Lithium (SHE: 002460), which is Hong Kong- and Shenzhen-listed, is separately also preparing to bid for the mines, according to the first two sources familiar. State-owned Hong Kong-listed, Xiamen-based copper-and-gold miner Zijin Mining Group is also considering a bid, said the first source familiar.” The article states “Tianqi expects to bid USD 4bn-USD 5bn”. To us this news appears completely unreliable for several reasons:

- Why is the bid price so extremely high compared to other bidders and economic analysis?

- A Canadian lithium miner is a strategic asset and a sell the China is unthinkable in political terms.

- It’s uncommon to have competing bidders from China for foreign assets.

- Why is an American outlet publishing such intimate news about Chinese companies first?

Last year saw a fundamental shift in Canada’s trade policy. As the year dawned, Canada still permitted, perhaps even welcomed, investments by Chinese companies. By the end of 2022, however, the government had adopted what amounts to a complete ban on Chinese investment in Canadian firms that operate in critical sectors of the economy, particularly critical minerals. Lithium Chile (TSXV: LITH), one of three Canadian miners hit by Ottawa’s decision to block Chinese investment in some critical minerals, said it regrets losing an “incredible shareholder with a valued expertise in lithium brine,” Canada’s Financial Post reported, noting that Chinese-owned Chengze Lithium International has sold its stake in Lithium Chile. (Global Times, February 21, 2023)

Our best explanation is that these take-over rumors from Chinese competitors are rather planted to strengthen SGML’s valuation which apparently worked out because SGML’s stock price increased by about 9.7% on the following trading day.

Continuously Improving Forecasts Seem Bogus

It is worth noting that SGML has made multiple updates to its technical feasibility studies, and each subsequent study implied dramatically better economics. Here is a short timeline of the company’s important announcements regarding its feasibility studies.

- December 7, 2020: SGML updates the feasibility study report to include a capacity increase from 220,000 tons to 440,000 tons per annum. On July 15, 2021, the technical expert report on doubling planned production is formally filed.

- April 11, 2022: SGML updates feasibility study again, implying a massive increase in assumed mineral reserves by the factor of 2.6x to 34 mega tons and a combined potential production capacity to a total of 450,000 tons per year.

- June 22, 2022, SGML substantially increases mineral resource estimate by ~50% to 86 million tons, adding 27 million tons of high-grade 1.49% Lithium. August 9, 2022: SGML files updated technical report supporting the previously announced increase in mineral resource estimate.

The following chart shows how SGML’s share price dramatically increased in the weeks following the announcements.

Upon taking a closer look at the feasibility studies, we deem them untrustworthy.

The alleged increase of mineral resources in the study results coincides with an exchange of “independent expert witnesses”. This pattern suggests SGML could be shopping for experts who are willing to authorize more aggressive estimates.

The two experts that remained engaged for all reports are Porfirio Cabaleiro Rodriguez and Marc-Antoine Laporte.

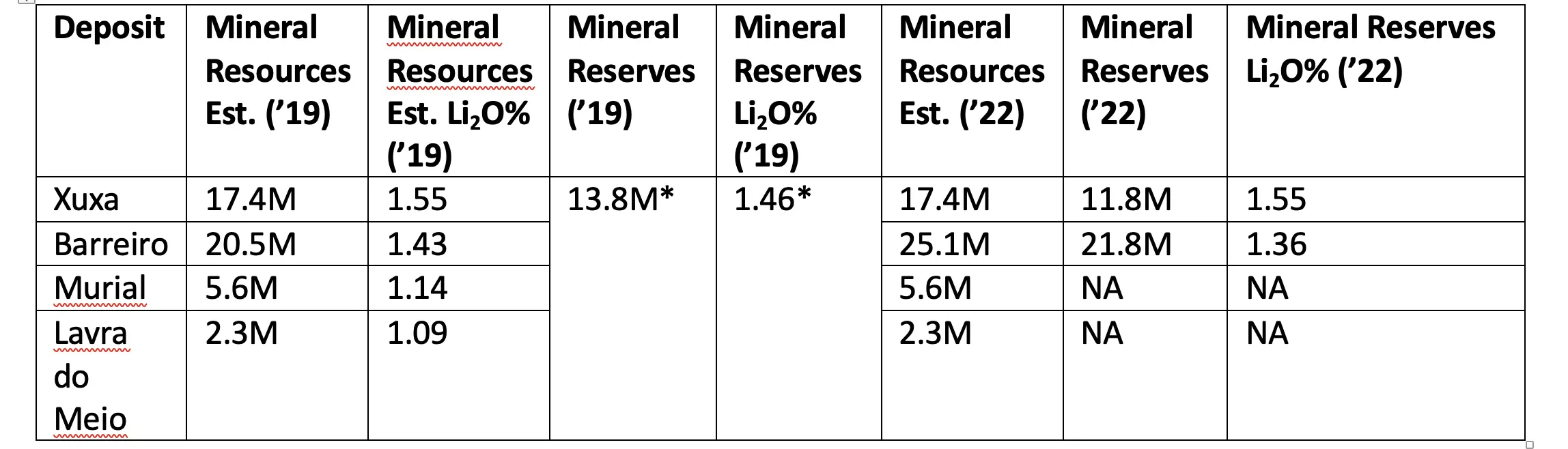

* Mineral Reserves are not separated by deposits in 2019 report.

SGML’s bullish remarks about their reserves are inferred from the increased resources and reserves estimates for Barreiro and Xuxa, as well as an increase of lithium market prices. The Qualified Person (“QP”) for the 2019 and 2022 Barreiro and Xuxa deposit mineral resource estimate was Marc-Antoine Laporte. The QP for the Barreiro and Xuxa mineral reserves results is Porfírio Cabaleiro Rodriguez. (For clarification: that part of a mineral resource, which has been fully evaluated and is deemed commercially viable, is called a mineral reserve.) In other words, those QP’s who were willing to provide more bullish estimates were kept in the projects as experts.

The crucial Barreiro resource increase from 20.5Mt to 25.1Mt is simply explained by an increase of the pit size from 8,605,468 m³ to 10,100,000m³ which comes with a reported decrease of lithium reserves purity from 1.46% to 1.36% Li2O. In other words, SGML did not make any profoundly more favorable discovery and mainly framed the wording in their press releases to lure investors. In their presentation material SGML updated the reserves to mine in “Phase 1” slightly from 34kt LCE in March 2022 to 36.7kt LCE in March 2022. However, due to the lower Li2O concentration, the additional reserves will be mined under higher extraction costs.

We want to make clear that we do not see anything categorically wrong with the experts or the way that SGML chose them. Simply stated, we believe their analysis which is supposed to support the valuation SGML is seeking in a sale and trading at today is flawed, however.

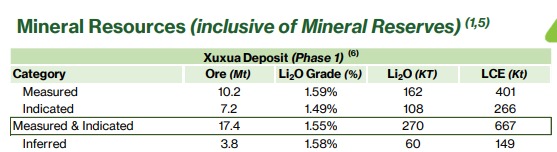

Phase 1 of production, the Xuxa mine, has been subject to particularly ridiculous increases in feasibility studies.

We found the feasibility study that SGML submitted to regulators in the Brazilian registry. PAE is the Portuguese term for the feasibility study and is also referred to as Preliminary Economic Assessment (the “PEA”).

Reserves estimated according to the PAE on July/7/2020 show drastically lower results than currently presented by SGML. We are talking about the same mine that has supposedly seen its reserve increase by over 5x.

And annual production of lithium:

And annual production of lithium:

And stating the mine has a total life of only 7-years.![]()

The company now presents an annual production of 270k tons per year for the same project and the lifespan from 7 to 8 years.

The reserves grew to over 21 million tons for the same project. This is an increase of more 5x within a suspiciously short period of time.

We want to note that SGML’s new PAE, which was initially filed in November 2022 according to Brazilian public records, is still hidden from the public. Transparency is the enemy of the fraudster.

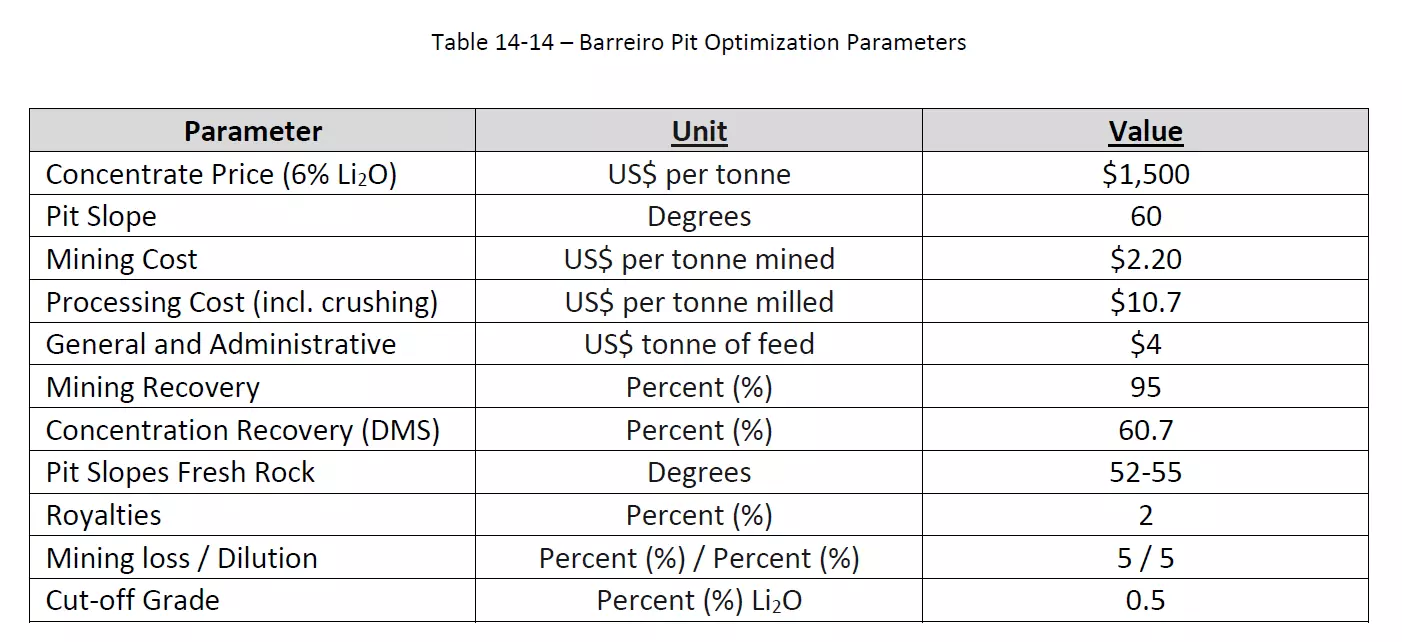

Lithium Price Assumptions Are Not Credible

In the 2022 technical report the financial forecast changed drastically compared to the 2019 forecast. This is the 2019 forecast:

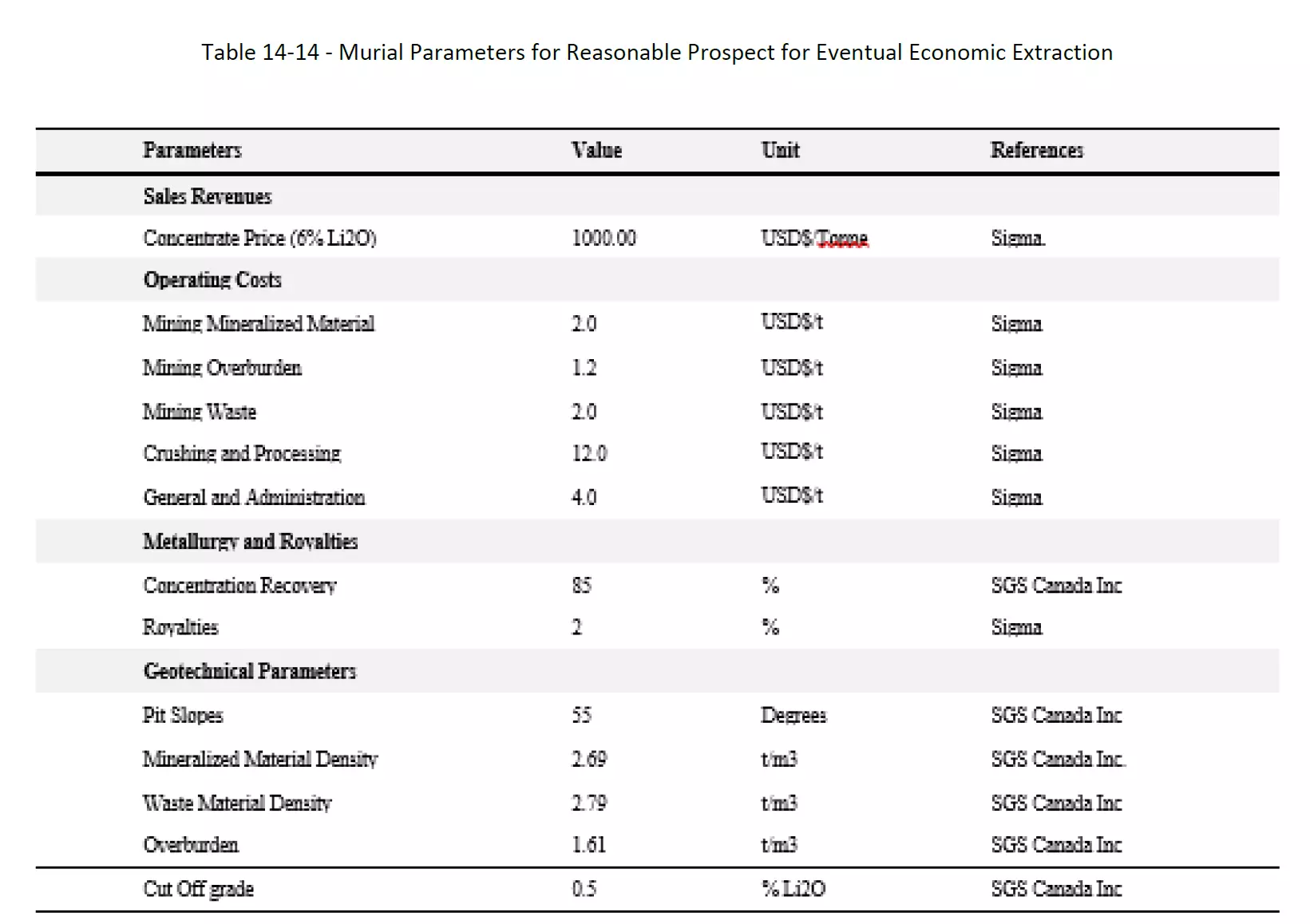

In summary, a long-term commodity price of $1,000 USD per ton is assumed at total extraction costs of $19.20 per ton.

The 2022 assumptions are much more optimistic:

The assumed commodity price is assumed to be 50% higher, $1,500 per ton, while the extraction costs are set at $16.9 per ton. SGML explains the reduced extraction costs by the more favorable currency exchange rate. However, the commodity price for 6% enriched lithium spodumene is doing the heavy lifting in the profitability forecast.

In their latest investor presentation (March 2023) SGML is deliberately vague about the prices they use for their calculations.

“Lithium Concentrate Price” is unclear because the purity and chemistry is important for the prices. In particular, the Li2O percentage of spodumene is relevant. Market prices of $3,956 or even $8,000 for 5.5% spodumene is highly unrealistic for mid-term or long-term trades. On a later slide they also call prices “LiOH Forecast (US$/t)”. This is similarly misleading.

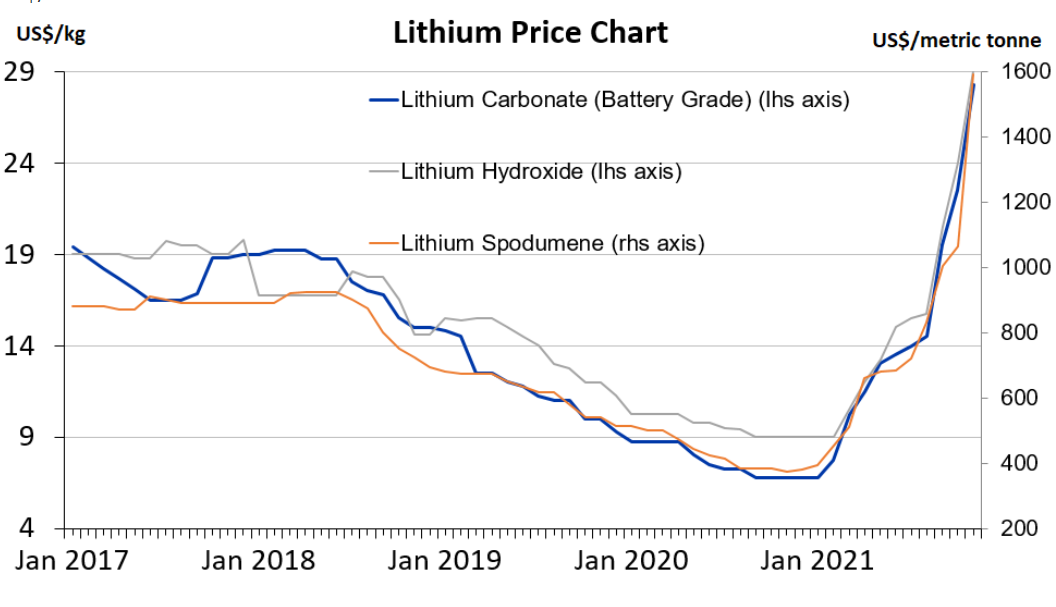

The valuation of the mine is obviously highly sensitive to lithium prices. We believe SGML is deriving their valuations on extremely inflated numbers. As we detail in the following section, SGML’s reference to spot prices is misleading because through 2022 into the beginning of 2023, lithium prices were extremely inflated due to short term speculation.

SGML Assumes a 87.5% Higher Lithium Price than other Independent Experts

Recent auctions for 6% Li2O spodumene resulted in $5,000/t (April 2022) and $7,708/t (September 2022). However, Goldman Sachs, in a market study from May 2022, estimates a price of $800/t for 2024 and 2025 the commodity due to strong increase in supply. (p. 14) Canaccord Genuity estimates prices of $1025/t for 2024, $750/t for 2025 and $1000/t for the years past 2025.

The following chart illustrates a downtrend in spodumene prices below $500/t until a strong jump in 2021 due to very recent and short-term supply constraints. The future price development is highly uncertain.

(chart by Consensus Economics)

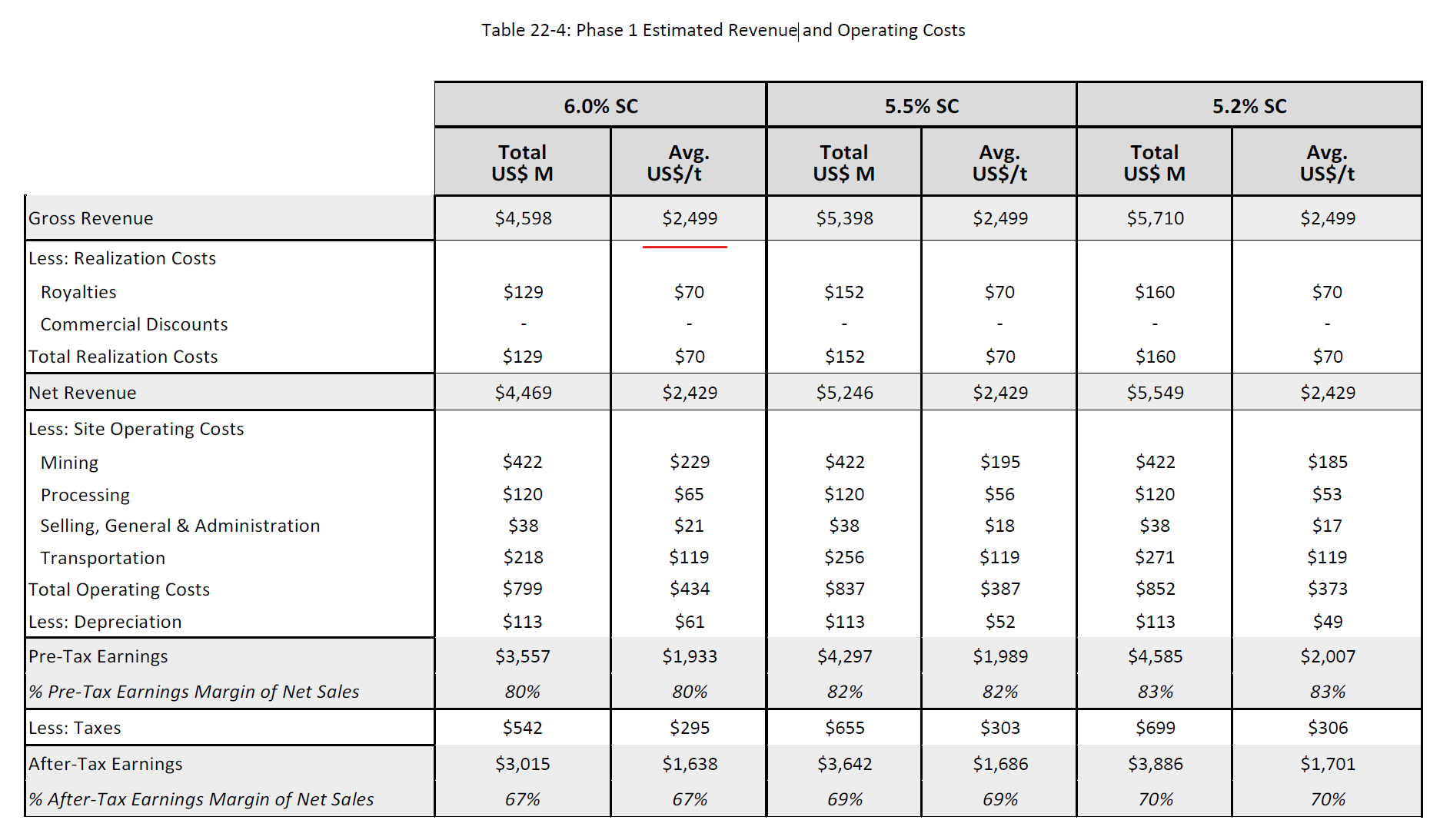

The selling price for the mine’s final product is central to SGML’s revenue and profitability estimates. For the yet to be finished phase 1 mines, SGML assumes even $2,499/t as average selling price.

Source: SGML’s technical report, August 2022, p. 449

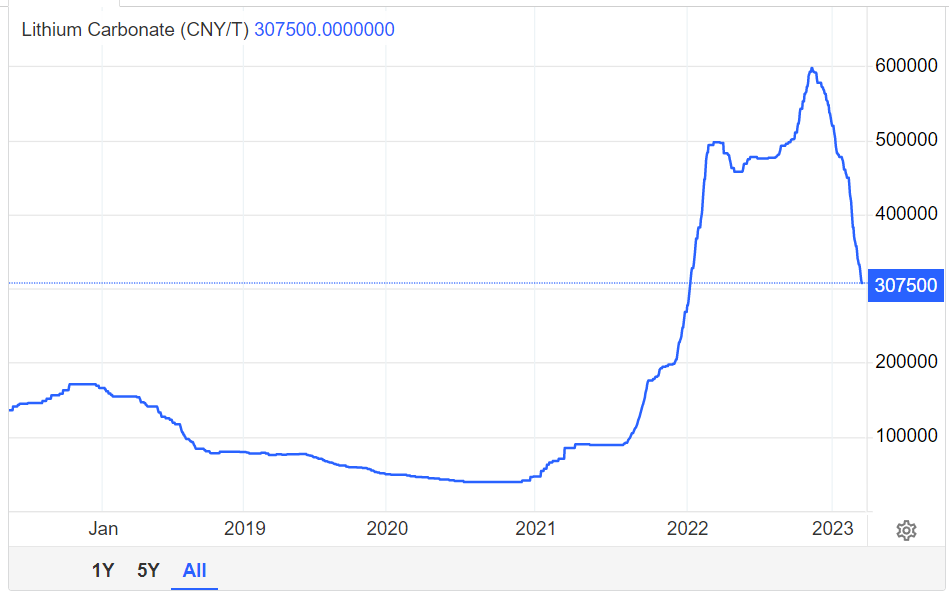

SGML hasn’t started the large-scale operation, but lithium prices have been on a sharp downtrend since November 2022:

(chart by TradingEconomics.com)

We believe SGML’s improving forecasts and valuation are underpinned by these assumptions about lithium prices. These model inputs appear exaggerated when compared to the estimates of independent experts. The industry experts we spoke to confirm the spot prices are currently heavily inflated because lithium is a very new industry, the volume isn’t large enough, and most contracts are negotiated privately between buyer/seller directly. The current price does not reflect long-term expectations.

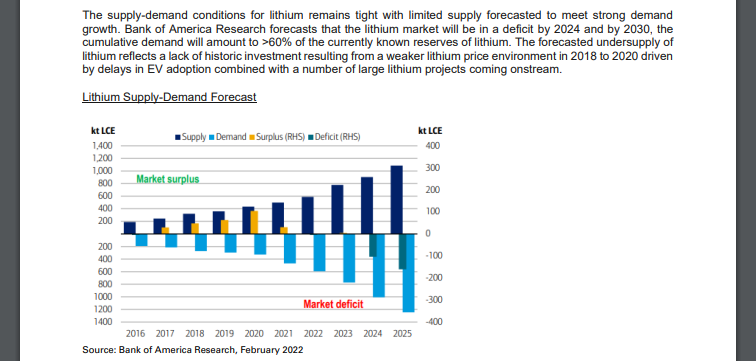

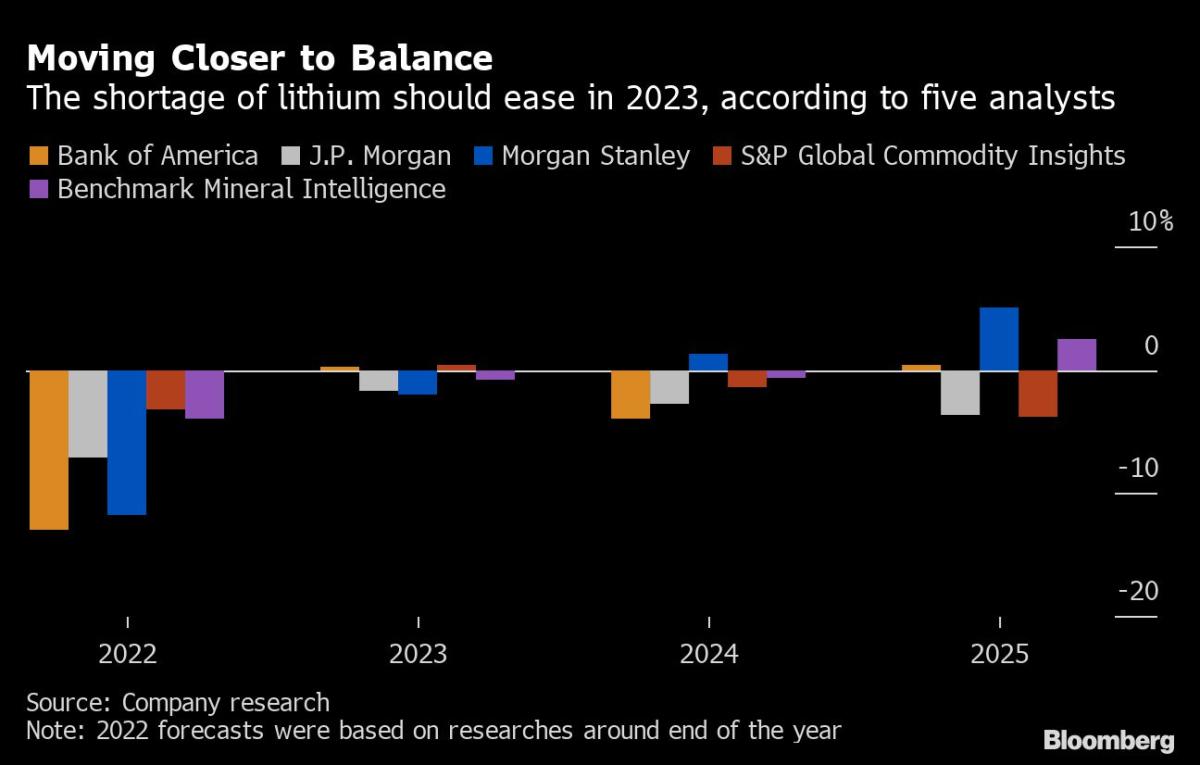

For their long-term forecasts, SGML cherry-picks the most favorable forecasts that do not mirror the industry consensus. In their 2022 annual report (p. 63-64) SGML refers to a supply-demand forecast by Bank of America, which implies a deficit regime of supply in the coming years. This is how SGML frames the supply/demand forecast:

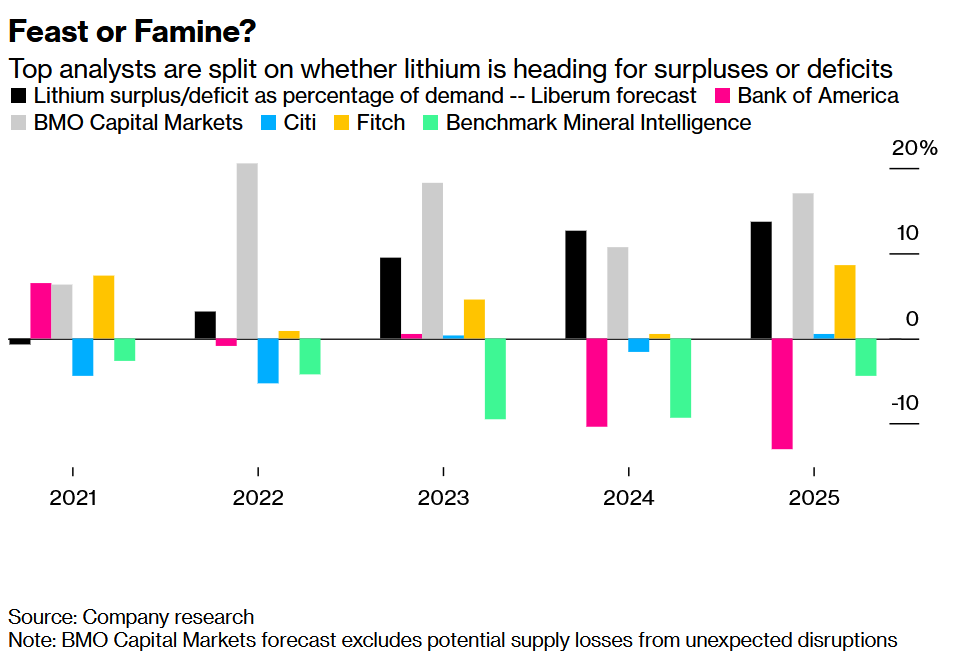

Benchmark analyses by Bloomberg reveal that Bank of America, provided the most bullish 2024/2025 demand/supply estimates for miners in February 2022, and revised its numbers by the end of 2022. We show the original presentations to underline how the information is conveyed:

Left: Bloomberg’s February 2022 analysis. Right: Bloomberg’s end of 2022 analysis.

As another example, Goldman Sachs forecasts an increasing market surplus of lithium from 2023 and onwards, which results in a long-term price of $800/t for 6% spodumene.

We spoke with dozens of industry experts, mining specialists, and people close to the company. Our conversations mirror the findings in independent expert reports. These experts agree lithium prices will be substantially lower than SGML anticipates in its analysis.

SGML’s Current Stock Market Valuation Far Exceeds a Fundamental Analysis Valuation

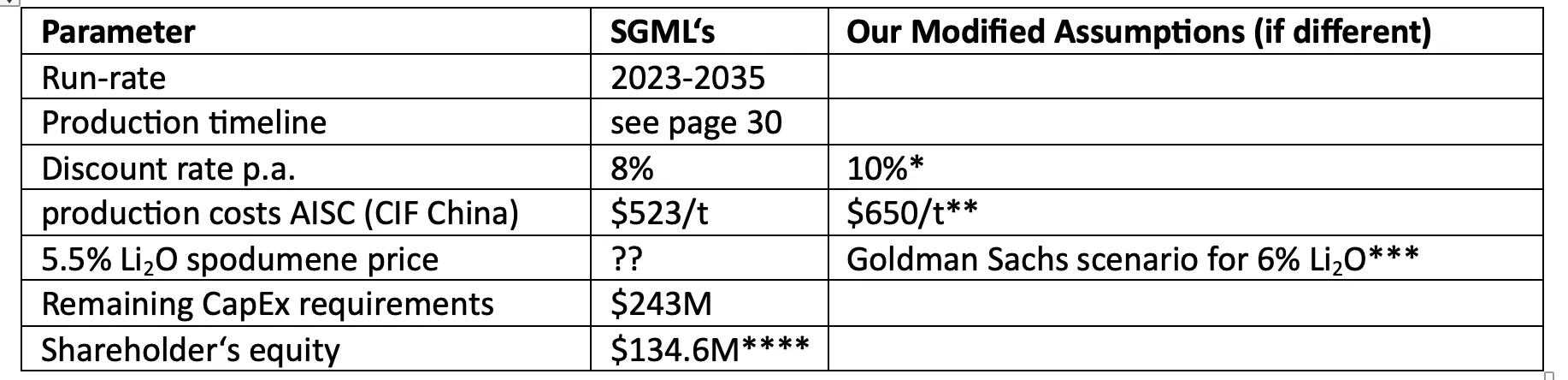

We conducted a standard cash-flow valuation analysis for SGML. We take SGML’s own assumptions from their March 2023 investor presentation with three modifications:

* “An expert advised us to slightly up-mark the discount rate to account for extra “country risk”. 10% is a discount rate we also found applied at a bullish analysis for SGML by PI Financial Corp in March 2023.

** Insiders we talked to suggests the production cost “is more than $600+ but still puts them [SGLM] quite low compared to others.” Another expert, mentioning the high inflation regime suggests “$630 to $680 per ton”.

*** 6% Li2O spodumene has higher value than 5.5% Li2O spodumene due to higher concentration.

**** According to the latest available company filings (September 2022), SGML has a shareholder’s equity of $134.6M (CA$185.8M).

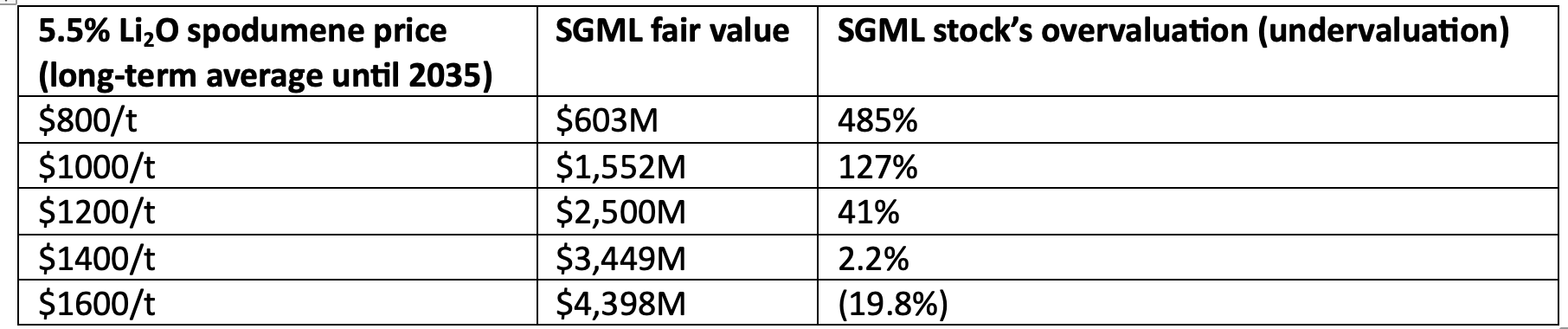

The resulting discounted profit from operations amounts to a total of $794.6M. Adding the shareholders equity and subtracting remaining CapEx requirements we derive a fair value of $686.1M. This implies the stock is overvalued by 414%. Calculation details can be found in the appendix.

Below we highlight the extreme sensitivity to lithium prices with the analysis under otherwise identical assumptions.

We Expect Continuous Delay of Production Start and Expansion

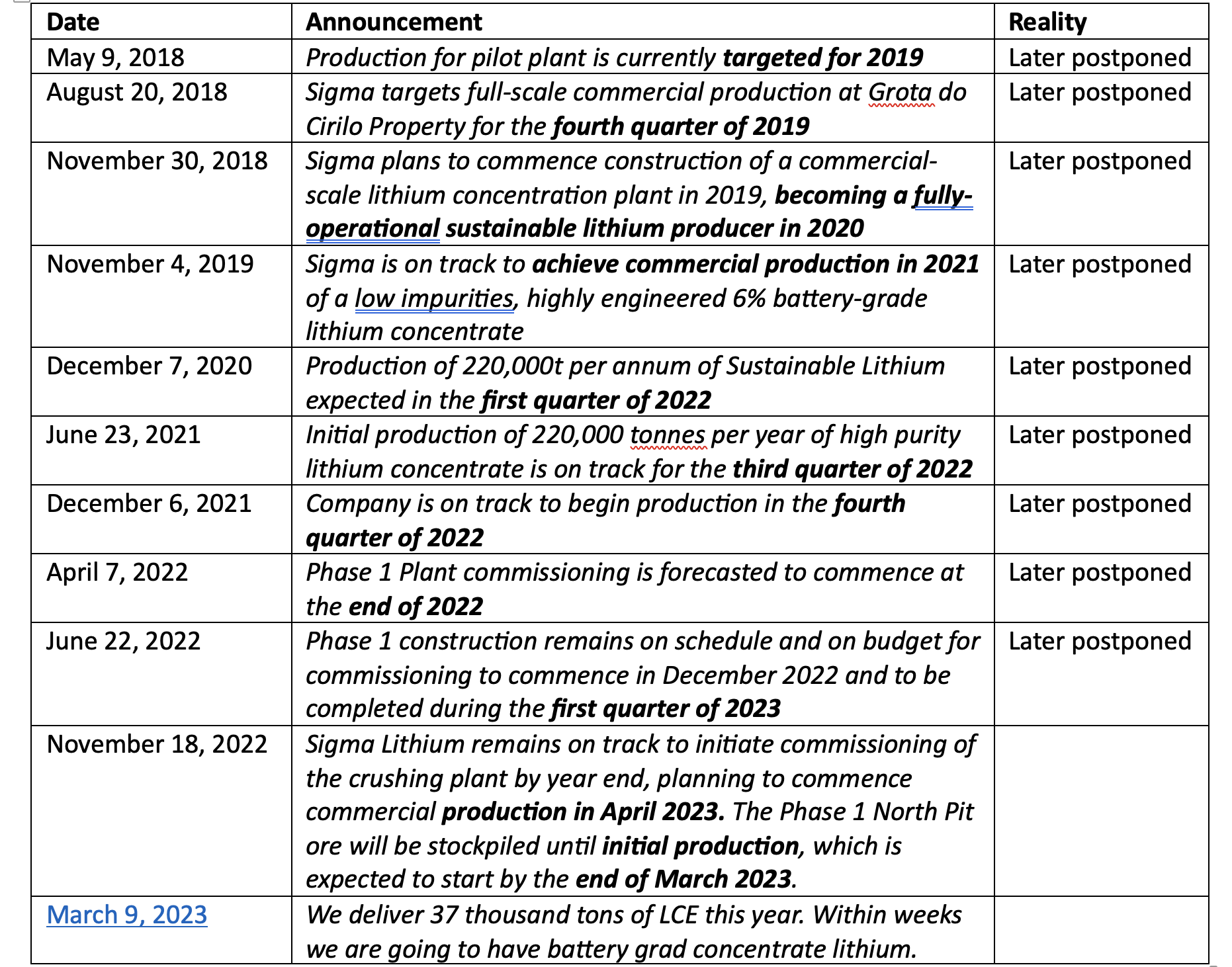

Currently the company is planning to start production at its Brazilian mine in April 2023. This is an important milestone; however, we believe production start will be delayed. This should come as no surprise as SGML has a history of repeatedly delaying this catalyst.

SGML has a History of Production Delays

We looked into SGML’s SEDAR filings to create a timeline of promises to investors about the production start. The overly aggressive timeline had to be stretched again and again. Why would anyone believe the current forecasts that are so crucially important to the businesse’s financial success?

We find it astonishing how quickly investors seem to have forgotten SGML’s track record of missed deadlines and history of overpromising.

Local Mining Expert Warns: Xuxa Mine is still Missing Key Licenses to Start Producing

As part of our diligence, we consulted with local mining experts in Brazil. We received a detailed analysis from an expert which has lead us to conclude that licensing issues will cause production start delays for the company.

The relevant license is the mining license for the Xuxa project, which is supposed to go into production in April 2023 and scale up rapidly. Our expert reported that a key environmental license is missing. This environmental license must be obtained from the State regulator, called SEMAD, for production to begin.

There are three steps to get the final environmental license: (1) Licença Prévia – Preliminary License; (2) Licença de Instalação – Installation License; and (3) Licensa de Operação – Operational license.

While we were able to confirm SGML has obtained the first two parts, the third part is currently missing.

We double checked with another state regulator and were still unable to locate the license.

Our sources advised us that obtaining this environmental license can take several months and might take up to an indefinite period. We found out that the company seems to have requested that last part of the license on January 25th 2023, but has not received it yet. We also noted that there were small protests by local environmental activist against SGML’s use of the local water resources.

Our local mining expert also advised us that SGML is still missing approval for its Feasibility Study or PAE from the regulators. That study is still hidden from public access, but we can see that it was submitted in November 2022. It is unclear at this stage whether SGML has received approval or not. This is another key approval that is necessary before one can start mining.

We wonder how SGML’s management keeps confidently touting a production start in April 2022, when key licenses seem to be still missing.

Missing In-House Knowledge and a Tough Race Against the Clock

We consulted with other industry experts and SGML project insiders told us in interviews that SGML “requires a proper organizational structure, proper manpower, which Sigma is lacking”. An insider told us SGML is “lacking PhDs” and need to buy expertise from outside consultants. People you meet at the Toronto head office are rather “investment promoters”. Despite the solid base economics of the project, an expert warns: “There’s a problem with the junior mining companies [like SGML]. They try to save money everywhere, but then they don’t find that, that timeline is extending and that will be costing more money.”

Experts told us further that currently many lithium mines compete globally against the clock. Global undersupply faced today will quickly be filled by whoever manages to ramp up production the soonest. SGML as a small contender without a sufficient in-house knowledge base is particularly poorly situated to win this race.

**In an earlier version of our report, we mentioned that “Sigma Lithium” only shows three employees on LinkedIn. We removed this part because the list of employees we pulled from LinkedIn refers to another company with the legal name “Sigma Lithium Ltd.” And the LinkedIn name “Sigma Lithium”. SGML currently has another LinkedIn profile “Sigma Lithium Corp. (Nasdaq:SGML)” that currently lists 79 employers. However, the current LinkedIn profile for “Sigma Lithium Corp. (Nasdaq:SGML)” was seemingly renamed several times. Former or alternative names of this account, including during our time of research, include “Sigma Lithium”, “Sigma Lithium Resources”, and “Sigma Lithium Resources Corporation”. We apologize for showing statistics of the wrong “Sigma Lithium” in the earlier version of this report.

The Company Can’t Get Its Own CapEx Projections Straight

In many ways, it seems that SGML is caught between a rock and hard place. This is due to the fact that we estimate the company will run out of cash if it does not start generating revenue within 2 years at its current burn rate. On the other hand, ramping up production to produce meaningful revenue will be a lot more expensive and less economical than currently portrayed by management. This in turn would reveal SGML’s forecasts as exaggerated and would probably scare away any remaining potential buyers. We can understand why the company would try to do everything possible to consummate a deal at currently elevated prices.

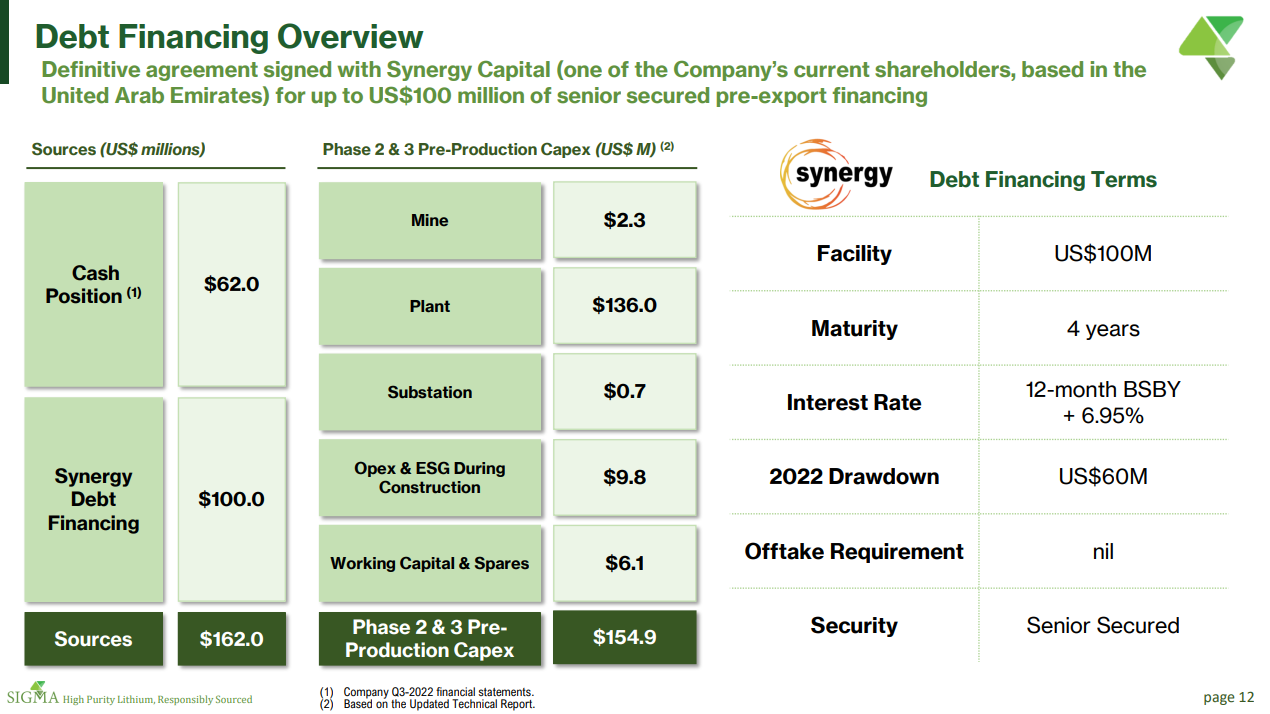

SGML bought itself some breathing room with a recently announced debt financing of up to $100m by its shareholder Synergy Capital. We fear that this will be hardly enough because management lacks the experience to actually ramp up production with the capital. We also see that the company seems to be unable to get its own CAPEX projections straight.

We strongly believe that Sigma will need additional capital very soon to pursue its planned operations, but the company is somehow trying to divert investors’ attention from that fact. Indeed, both screenshots presented below, which are from the latest presentation (March 2023), show a contradictory narrative. On the first screenshot, we can see that Sigma is showing how its new debt financing of US$100 million along their cash position of $62 million will be enough to cover the $154.9 million CAPEX spending for the Phase 2 & 3 Pre-Production.

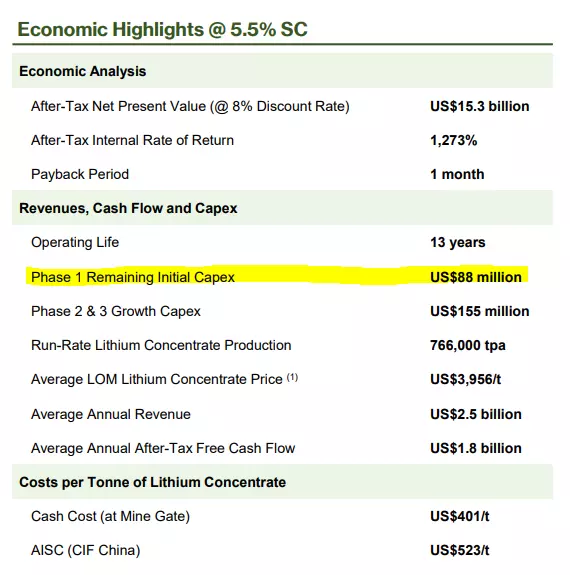

But it appears that Sigma omitted to show that it has a remaining planned CAPEX spending of $88 million for the beginning of production of its Phase 1. Moreover, this exact CAPEX estimate was also presented during the M&A discussion for the three and nine months ended September 30, 2022.

These estimate on CAPEX seem to us more like wild guesses, rather than trustworthy numbers.

We Believe Management is Dressing up a Hairy Business

Greentech Claims are Nothing but Hype

We noticed that Sigma has also been drowning investors with press releases around ESG, mostly pointed at their “green and sustainable” business. By looking deeper into it, we found that many claims that are very positive on the first look are in fact hiding some basic business practices. Moreover, some of the claims appear to be only fluff, as for the moment, none of them have been applied or confirmed by their operations.

For many years now, the company has been boasting about its future processing which should be done in a “green” environmentally friendly and sustainable manner”. More details about it reveal that this “green processing” is in reality only explained by the fact that Sigma will not use flotation or hazardous chemical reagents, such as sulphuric acid, in the concentration process. While this is an honorable thing to do, the company has been going off limits and pushed statements way too far. Indeed, while the way they will process the mine production did not change, they now call it “Greentech Transformation”. Note that the company has spent virtually nothing in R&D during its whole existence.

Most importantly SGML sells 5.5% to 6% spodumene and does not participate in the post processing to create battery grade high concentrate lithium. But this is the part that is actually highly demanding from the ecological perspective.

We believe that Sigma is probably just overhyping this part of the business. Below is an example of how the company, according to our opinion, is losing its credibility:

Sigma, a pre-production company, is calling itself “Global Leader in Sustainable Production”. This is a bold statement given that currently the company only has a “pilot program”.

Moreover, Sigma announced through a press release in May 2021 that: “The Company plans to achieve net zero carbon emission targets by 2023, partly as a result of its ESG program and strategic decision to pursue generation of internal carbon credits through “in-setting” (within its regional ecosystem).”

Only five months later, in September 2021, through another press release, the company proudly announced: “the constitution of an ESG Committee of the Board of Directors of the Company (“ESG Committee”) resulting from the program intended to achieve Net Zero emissions by 2024.”

We found one of the reasons why the company’s communication revolves so much around its sustainability aspect. Indeed, it is mentioned in the same press release that:

“NET ZERO Environmental Milestone: If the Company’s Board of Directors and shareholders approve the co-CEOs plan to reach Net Zero emissions and they successfully execute it, there will be an ESG bonus as part of the co-CEOs Performance Award tranche of 500,000 RSUs each.”

This award is one of the many awards that the co-CEOs can receive from their company. The main milestones, which have now been reached, were linked to the market capitalization. The co-CEOs were both to receive a total of 2,500,000 shares if the market capitalization was to reach CAD$ 2.0 billion. While this is common practice and we do not believe it to be exaggerated, the environmental milestone, on the other hand, seems totally ridiculous when taking into consideration that the company spent nothing in R&D to develop its “Greentech production”. As of March 11th 2023, these 500,000 additional shares each would be worth around $23.5 million for each of co-CEOs, for a total of $47 million. We believe this money would have been better invested in actual environmental initiatives.

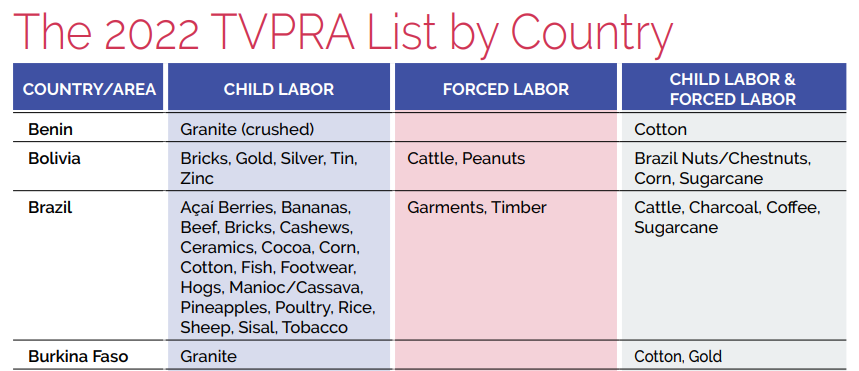

Forced and Child Labor Concerns

Major demand markets for Lithium in North America and Europe are sensitive to regulation that prohibits the imports of goods or commodities that were sourced using slave labor. In September 2022, the U.S. Department of Labor published its annual List of goods produced by Child Labor or Forced Labor. The report lists lithium/ion batteries has products of concern and raises particular awareness of issues with widespread forced labor in Brazil (p. 24):

In the competitive near future landscape of battery-grade lithium we see a significant disadvantage for SGML. From 2014-2016, SGML’s current CFO Rodrigo Menck was a board member for Odebrecht Group, the Brazilian company that was convicted by a Brazilian court for forced labor of Brazilian workers in Angola.

We are also concerned because SGML’s Brazil mine is located north of Minas Gerais state, which is the most economically disadvantaged region of the state and has been cited repeatedly in relation to child labor issues.

Is the Company Even Paying Minimum Wage?

We did a quick back-of-the-envelope calculation that implies that SGML is probably not paying its workers minimum wage.

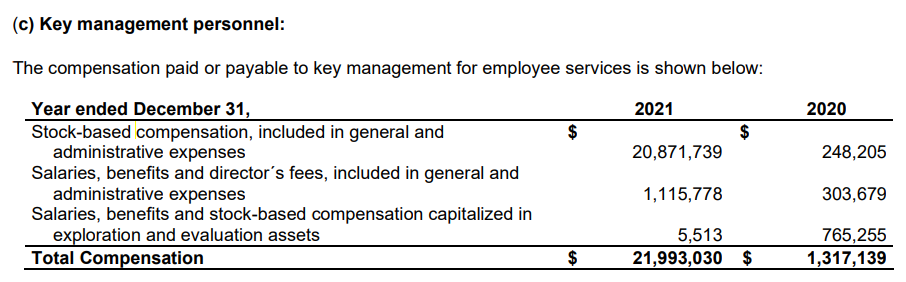

Unfortunately, there is no recent disclosure on the management compensation, which is only disclosed in annual filings. The CEOs are being compensated only in shares, so the numbers below refer to the rest of the management team. We would also guess that after the market capitalization jump, the progress towards construction and the listing in the US, those compensations are now way higher, just as the increase from 2020 to 2021 suggests.

Source: Sigma 2021 SEDAR Annual FilingsWithout any additional details given, the rough estimate for a quarter of management compensation would be CAD$1,115,778 / 4 = CAD$278,750.

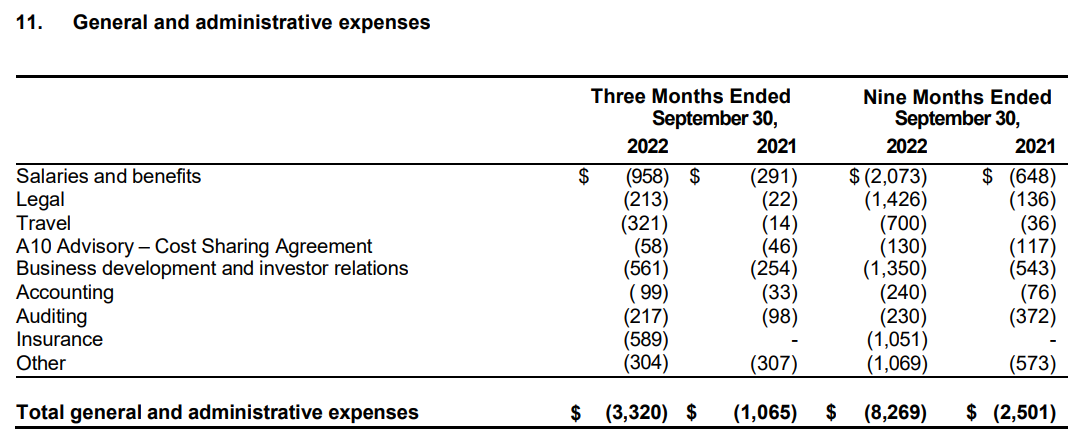

Source: Sigma Q3 2022 SEDAR FilingsThe screenshot above shows the latest data available on G&A expenses in CAD$ thousands. We notice that the salaries and benefits amount CAD$958,000 for the Three Months Ended September 30, 2022. We deduct the estimate of the management compensation to see what was paid to other workers:CAD$958,000 –

CAD$278,750 = CAD$679,250

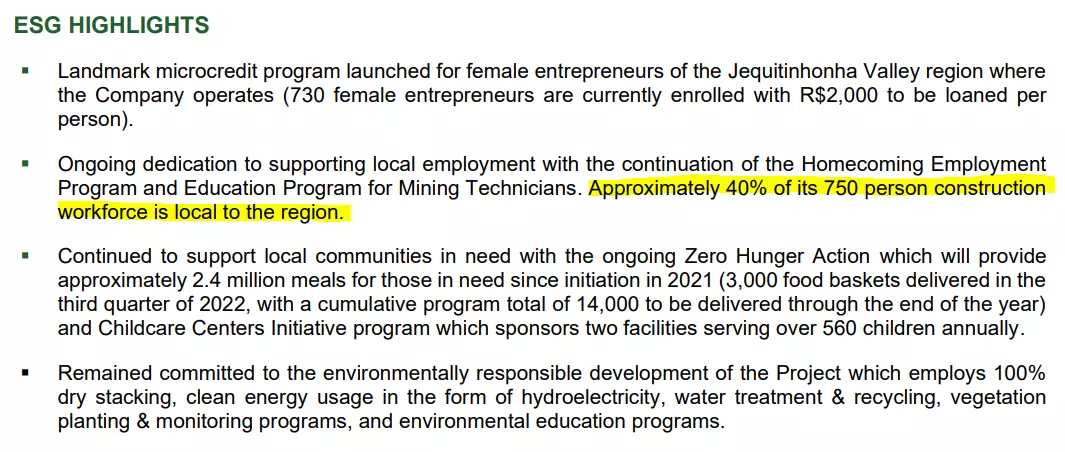

It was stated in the latest M&AD (Q3 2022) that there was a construction workforce on site of 750 people, where approximately 40% were from the mine’s region. While the number of other employees excluding the workforce was not detailed, we believe the following estimate is very optimistic.

CAD $679,250 / 3 (months) = CAD $226,416 / 750 workers = CAD $301,9 per month = BRL 1151,73

The minimum wage in Brazil for 2022 was BRL1,212 per month and has been raised to BRL1,302 per month in 2023.

We could argue that the increase in the workforce happened gradually over the three-month period. Nevertheless, this estimate does not include any extra workers that are not on site. We believe there are other employees in the US or in Canada, where the minimum wage is far higher, that are included in the CAD$958,000.

Therefore, it seems that Sigma is paying its workforce in Brazil the minimum wage or even below that. This stands in total contradiction with their countless press releases and conferences about ESG and local support.

Conclusion

We have conducted several interviews with industry experts and insiders. While the rumors about a potential acquisition of SGML have sparked investors’ interest, we believe such hopes are misplaced. Our analysis explains SGML is not only an unlikely buyout candidate at current prices, but an overall less attractive investment than portrayed to investors.

Most the stock’s success can be attributed to ever-improving feasibility studies that we call out as bogus. The increases in reserves are unrealistic and the lithium price assumptions the company uses for its models greatly exceed industry consensus figures.

We credit SGML’s management team for driving hype around their stock. They have been clever in using unrealistic studies and buzzwords like “Greentech” and pitched the story that they are the most sustainable lithium miner in the world. That said, we do not believe they have the operating expertise to develop the Grota do Cirilo Project.

SGML’s track record is rife with production delays and our diligence alongside local mining experts suggests further delays are in store. The production ramp will likely be more costly than projected and SGML’s lacks technical resources and leadership to improve the situation.

With potential acquirers passing on SGML and insiders aggressively dumping stock, we caution retail investors not to not blindly buy into acquisition rumors.

APPENDIX

Discounted Cashflow Valuation

Goldman Sachs’ Forecast Model for Lithium Concentrate Prices

These are Goldman Sachs’ (“GS”) results from their May 2022 analysis. GS forecasts an increasing lithium surplus.

Based on these estimates, GS forecasts a long-term stabilization for 6% Spodumene prices at 800 $/t.