– ZTO is one of the leading players in the intensely competitive Chinese logistics market. Despite standardization across the industry, ZTO boasts margins >2x the average of its peers.

– It is our view that ZTO’s apparently superior margins are, in fact, just the result of its potentially falsified financial statements. We believe ZTO has underreported revenue and costs to engineer these standout results. Our report highlights corroborating evidence including incessant capital raising, accounting inconsistencies, and numerous conflicts of interest which contradict ZTO’s exceptional margins.

– Characteristic of notorious “China Hustles”, ZTO’s SAIC filings (PRC) present a totally different reality than its SEC financial statement. SAIC filings reveal ZTO’s margins are actually on par with its express delivery peers. While SAIC filings show 6.3%-10.6% net margins between 2019 and 2021, the company reports 15.5%-25.7% net margins in its SEC financial statements.

– Why would a company make statements about its large employee base in China, only to hide from it in the US? We show puzzling inconsistencies in ZTO’s reported workforce which we consider evidence that the company is understating employee figures to support reported labor costs and achieve its exceptional margins. Based on conservative salary estimates, ZTO’s true employee count and associated labor expenses may be more than double the figures reported to the SEC.

– To close the loop on this accounting scheme, we believe ZTO has reported bogus CapEx in its US financials. ZTO attempts to justify PP&E and land use rights growth which outpaces its revenue growth by citing potential market share gains, but they appear to be amassing land with no strategic rationale. We are confounded that such an established company with “best-in-class” margins has raised >$3B since its 2016 IPO despite having no tangible shareholder value to show for its spending.

– We show how ZTO used acquisitions (in 2014 and 2015) to enrich insiders and/or make its accounts balance. Corporate filings show ZTO acquired franchisees (referred to as “network partners”) from related parties at exorbitant prices compared to network partner start-up costs. Even more concerning, we show Chinese records which indicate no change in ownership after the deals. As we show, we believe this may be because these entities were already operating as ZTO subsidiaries. Did ZTO invest shareholder cash for nothing in return?

– We believe ZTO has shifted operating expenses off balance sheet by utilizing a web of undisclosed related parties. Several ZTO counterparties are owned and controlled by individuals who are either employed by ZTO or are family and friends of its management team. Our site visits discovered even more potentially undisclosed related parties and shows that supposedly independent entities operate within immediate physical proximity to each other and share business logos

– Even the related party transactions ZTO has disclosed are concerning. We believe public shareholders have been unnecessarily exposed to risks in China’s real estate sector due to large loans used to fund insiders’ property investments. The burden of default risk on these personal projects falls on investors, not the related parties the loans serve to benefit.

– After adjusting for ZTO’s artificially inflated margins and applying generous trading multiples, we believe the company is trading far above its fair value. Our analysis implies at least a 50% downside.

ZTO is a logistics company that provides delivery services in China. The domestic logistics market is highly competitive in China, yet ZTO stands out to be the highest-margin operator in this sector. In this highly competitive market, with rising labor costs and overall economic slowdown, its margins were once close to those of Apple, and far exceeding the industry peers. Upon conducting thorough research on ZTO, we discovered numerous red flags that contradict and undermine the financials the company disclosed to public investors. In addition, we also discovered some related party transactions that call into question the integrity of the company’s management.

The Largest Telltale Sign – Absurdly Good-Looking Margins

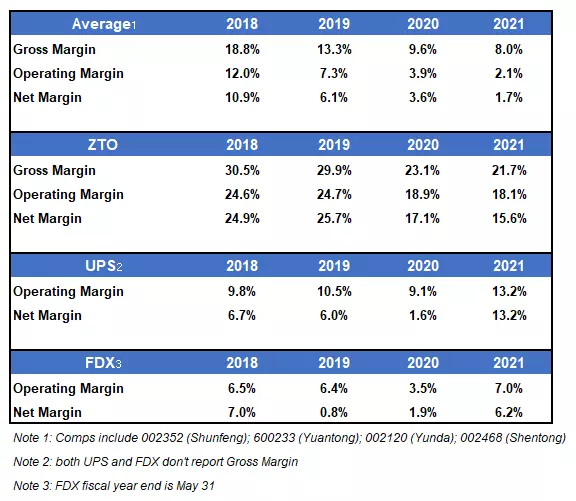

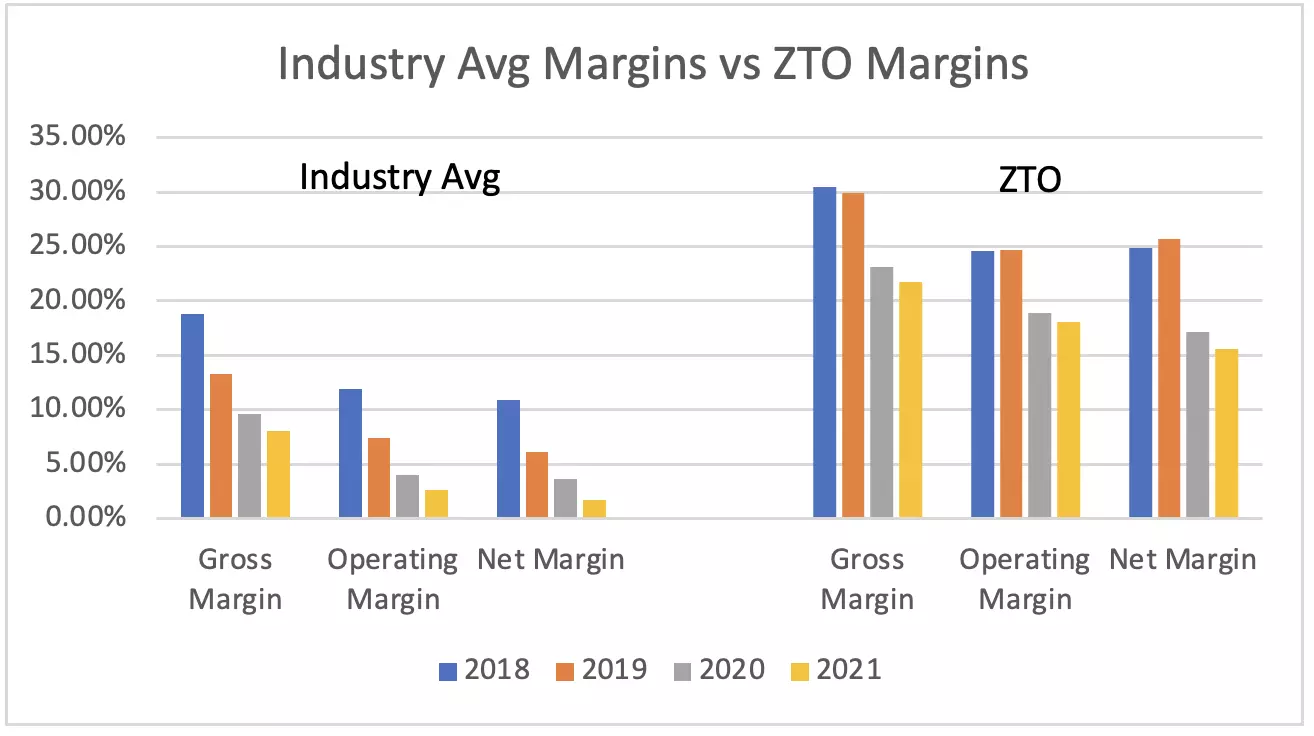

Below we have summarized the average gross margins, operating margins, and net margins for the four leading express delivery companies in China. We have also compared these metrics to best-in-class US logistics companies, UPS (UPS) and FedEx (FDX).

source: company filings, Grizzly analysis

The data suggest ZTO’s business is special. At one time, ZTO’s profitability was comparable to blue-chip companies in higher margin businesses like Apple.

Like peers, ZTO’s profitability was in a downward trend from 2018 to 2021. Yet, the decline ZTO experienced was seemingly less pronounced than its peers. The average net margin for comparable companies declined from ~11% in 2018 to 1.7% in 2021. Meanwhile, ZTO’s net margin decreased from ~25% in 2018 to 15.6% in 2021. We find it unusual that a logistics company with high labor costs and overhead has margins that are multiples of peers’ and in line with best in-class operators in more profitable industries.

Our conclusion for this outperformance is that ZTO either has an exceptional management team or the financials are too good to be true. While we would like to believe ZTO’s executives are superior, our due diligence has led us to believe investors have, in fact, been duped.

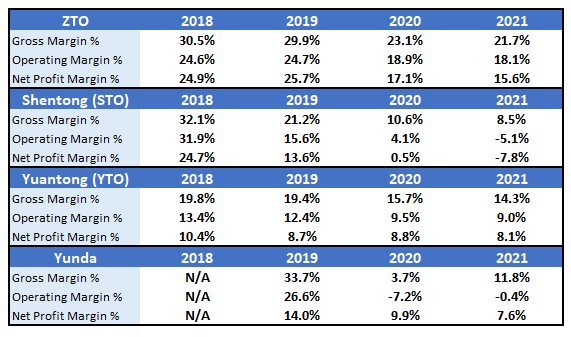

After first observing ZTO’s standout margins, we figured there must be an obvious explanation for the dramatic differences between peers. We thought our suspicions would be tempered after adjusting for last-mile delivery services which Yuantong (YTO), Shentong (STO), and Yunda include in their results and ZTO excludes. To make an apples-to-apples comparison, we excluded the last-mile delivery services from revenues and cost of goods sold across the peer group. The table below compares the relevant financial metrics following this adjustment. We can see, however, that ZTO still commands dramatically higher margins that these peers.

source: company filings, Grizzly analysis

SAIC Financials Show ZTO Exaggerated Net Margin by Understating Revenues and Overstating Net Profit

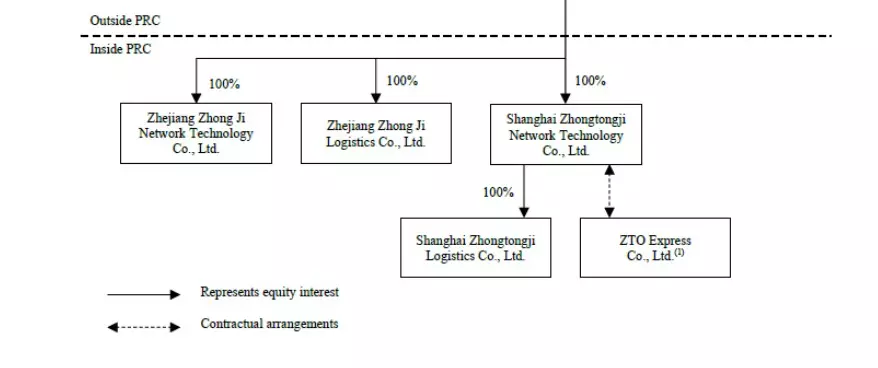

ZTO’s Annual Report identifies 5 subsidiaries operating within China.

Source: ZTO 2021 Annual Report

The 5 relevant entities are summarized in the table below.

We obtained the SAIC files for these companies and consolidated their financial data from 2019 to 2021. The State Administration of Industry and Commerce in China is a useful yardstick for investors to check the integrity of the financials reported to the SEC. Discrepancies in the reported financials between SEC and SAIC filings often indicate financial fraud. This inconsistency has been prevalent in almost all major Chinese frauds such as Sino-Forest, Focus Media, and GOTU (previous ticker: GSX).

We also noticed that ZTO happens to have the exact same auditor as GOTU, namely Deloitte Touche Tohmatsu Certified Public Accountants LLP. We consider GOTU as one of the most brazen and obvious frauds in recent history, and Deloitte Tohmatsu continued to sign off on GOTU’s financials despite overwhelming evidence that the financials were likely fabricated. It seems to us they are doing the same for ZTO.

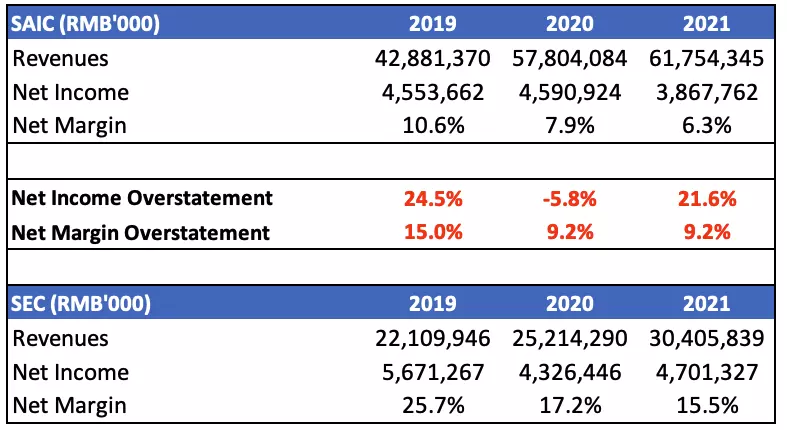

After comparing the consolidated financials from SAIC, a Chinese government source, with the financial data that ZTO reported to SEC, we find significant discrepancies between these two sets of data. We were unable to obtain the balance sheet data for one of the 5 entities, which reported zero revenues.

source: SAIC financial data; company filings

First, let’s look at the operating metrics including revenues and net income. It appears ZTO significantly understated its total revenues in its SEC filing. For example, in 2021, the consolidated SAIC revenues were 61.75B RMB as compared to 30.41B RMB reported in ZTO’s SEC filings. In the meantime, ZTO also overstated its net income in SEC documents. For example, in 2021, the consolidated SAIC net income was 3.87B RMB, however, ZTO reported 4.70B RMB net income in its SEC disclosure, which is 21.6% higher than that from SAIC data.

The net margins reported in ZTO’s SEC filings were 25.7%, 17.2%, and 15.5% for 2019, 2020, and 2021, respectively. Whereas the net margins from SAIC financials were 10.6%, 7.9%, and 6.3% for the same periods. These margin differences are significant and also support our suspicions that were laid in the previous part: ZTO’s SEC-reported margins are simply too good to be true, while adjusted SAIC numbers are in line with Chinese competitors.

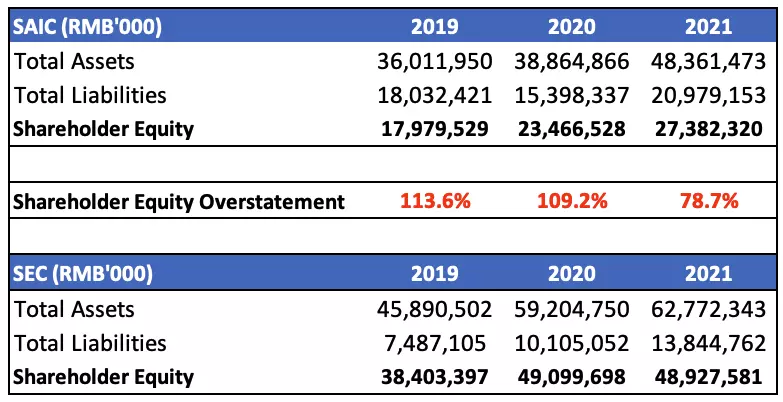

Furthermore, not only did ZTO overstate its net income and net margins, but we believe it also dramatically overstated shareholder’s equity in the past years by overstating total assets and understating total liabilities. The table below summarizes the SAIC data vs the SEC-reported data by ZTO.

source: SAIC financial data; company filings

The discrepancy between SAIC financials and SEC reported financials is astonishing when it comes to ZTO’s balance sheet data. For example, in 2021, the consolidated SAIC total assets were 48.36 B RMB, yet ZTO reported 62.77B RMB of total assets in its SEC filing. In the meantime, ZTO understated its total liabilities in its SEC filing. It reported only 13.84B RMB total liabilities, yet SAIC consolidated total liabilities were shown to be 20.98B RMB. This overstatement in total assets and understatement in total liabilities resulted in a significant overstatement in ZTO’s shareholder equity. For example, the SAIC consolidated shareholder equity was 27.38B RMB in 2021, however, ZTO reported 48.93B RMB in its SEC filing for 2021, a 78.7% overstatement! The discrepancy in shareholder equity between SEC and SAIC filings was even worse in earlier years. For example, ZTO overstated its shareholder equity by 113.6% and 109.2% in 2019 and 2020, respectively.

To us, the discrepancies between SAIC and SEC filings make perfect sense. ZTO positions itself as the operator with the highest margins. This attracts investors and allows ZTO to continue raise money from investors.

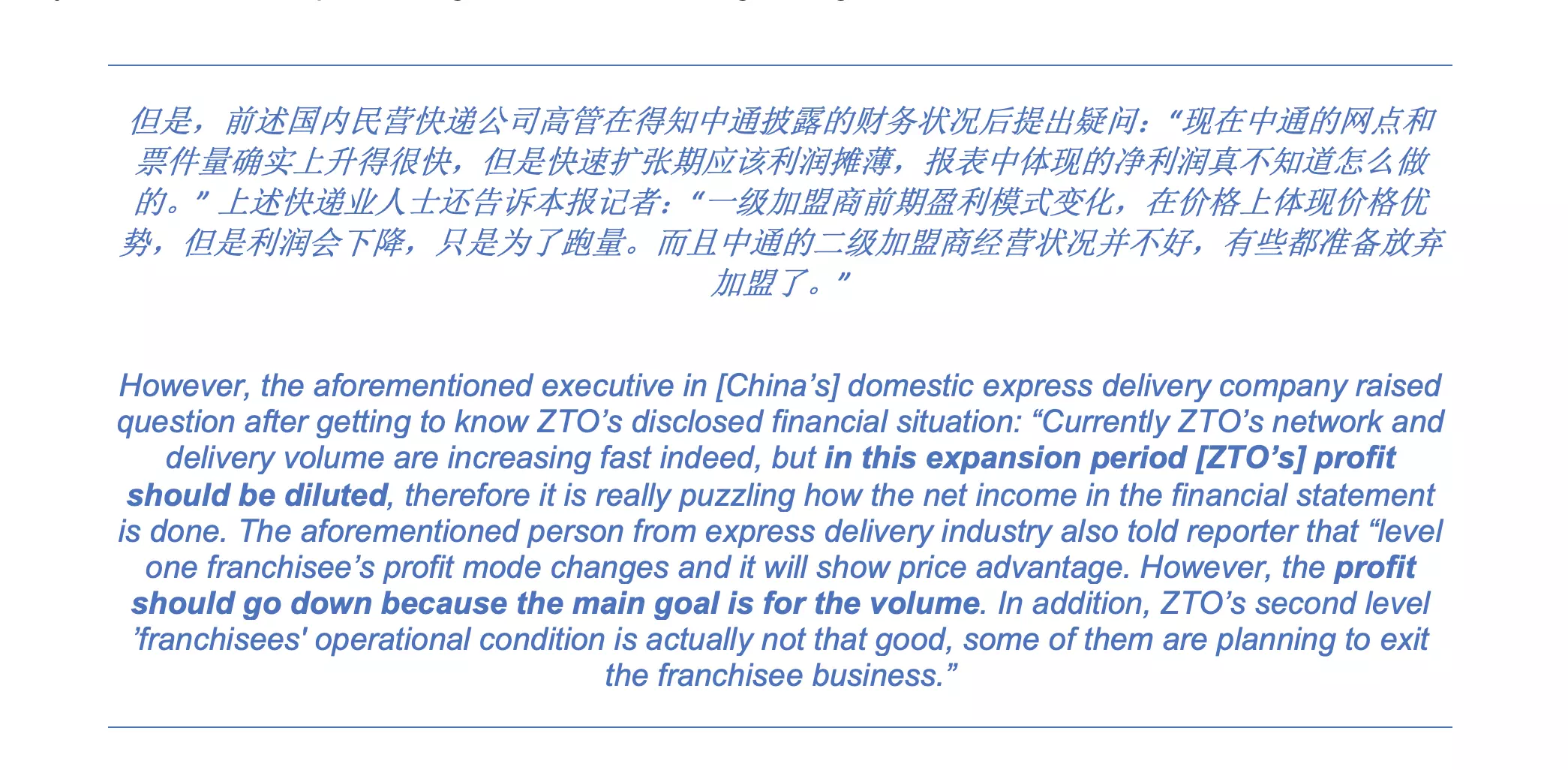

After ZTO launched its IPO process in 2016, there were numerous articles that questioned ZTO’s disclosed high margins as compared to its peers. For example, this article in October 2016 cited an executive from the express delivery sector in China, questioning ZTO’s disclosed high margins.

We believe the high margins are achieved by cherry picking more profitable subsidiary financials for its consolidated results. We believe ZTO accomplished this through a convoluted web of “network partners”, as well as via disclosed and undisclosed related party dealings.

ZTO Potentially Underreports Employees to Decrease Its Costs

ZTO’s express delivery services business takes the form of a “network partner” model described in its prospectus. This involves operating “a logistics network by focusing on the build-out and operations of the core sorting hubs and line-haul transportation assets while relying on network partners to carry out pickup and last-mile deliveries.”

By design, this business model is supposed to enable ZTO to focus on its core competencies, while last mile is outsourced. Our research, however, has revealed this business model also allows ZTO to manipulate the numbers.

Reason 1: ZTO Paying Social Insurance for Outsourced Employees As If They Were ZTO Employees

source: company filings

According to the company’s disclosure, since 2016, its direct network partners increased from approximately 3,500 in 2016 to over 5,700 as of December 31, 2021. The relationship between the company and its indirect network partners is described below according to its 2021 annual report:

Based on the company’s disclosure, the indirect network partners are more like an extension of its current network partners, because most of its indirect network partners also work exclusively with ZTO. The company ceased to disclose the number of its indirect network partners in 2019, but we can see that its direct network partners kept growing from 4,500 in 2018 to over 5,700 in 2021. A reasonable assumption would be that ZTO’s indirect network partners also increased through this period.

Unlike its other three peers, ZTO discloses its outsourced employee count, instead of the more common annual outsourced working hours. Take Yuantong Express (600233) for example, it disclosed that the total outsourced working hours is 115,793,552 hours in 2021 which costs the company RMB 2.316 B. However, ZTO disclosed that it had over 57,000 outsourced personnel as of December 31, 2021. The table below summarizes ZTO’s employee count in the full-time and outsourced categories (previously referred to as dispatched and contractor workers).

source: company filings

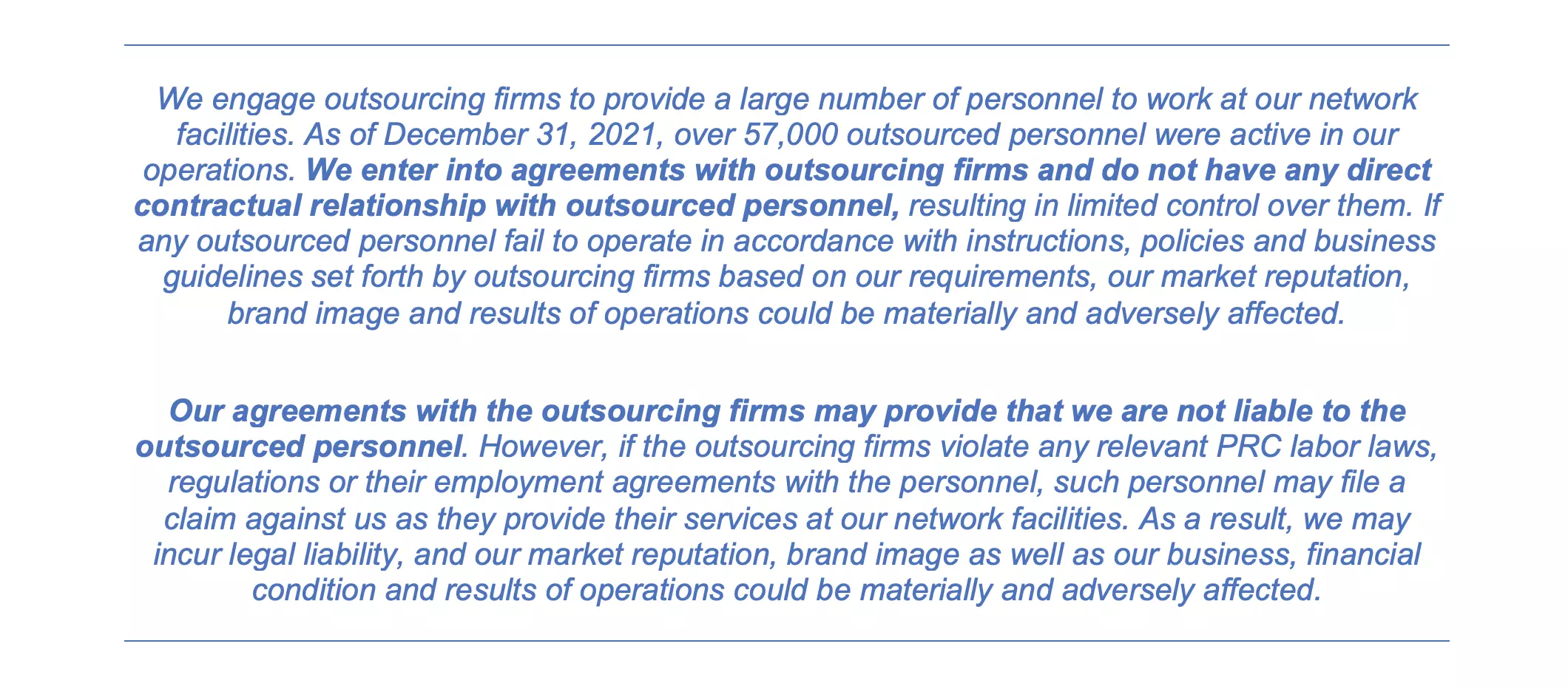

According to ZTO, it does not have a direct contractual relationship with outsourced personnel.

We engage outsourcing firms to provide a large number of personnel to work at our network facilities. As of December 31, 2021, over 57,000 outsourced personnel were active in our operations. We enter into agreements with outsourcing firms and do not have any direct contractual relationship with outsourced personnel, resulting in limited control over them. If any outsourced personnel fail to operate in accordance with instructions, policies and business guidelines set forth by outsourcing firms based on our requirements, our market reputation, brand image and results of operations could be materially and adversely affected.

Our agreements with the outsourcing firms may provide that we are not liable to the outsourced personnel. However, if the outsourcing firms violate any relevant PRC labor laws, regulations or their employment agreements with the personnel, such personnel may file a claim against us as they provide their services at our network facilities. As a result, we may incur legal liability, and our market reputation, brand image as well as our business, financial condition and results of operations could be materially and adversely affected.

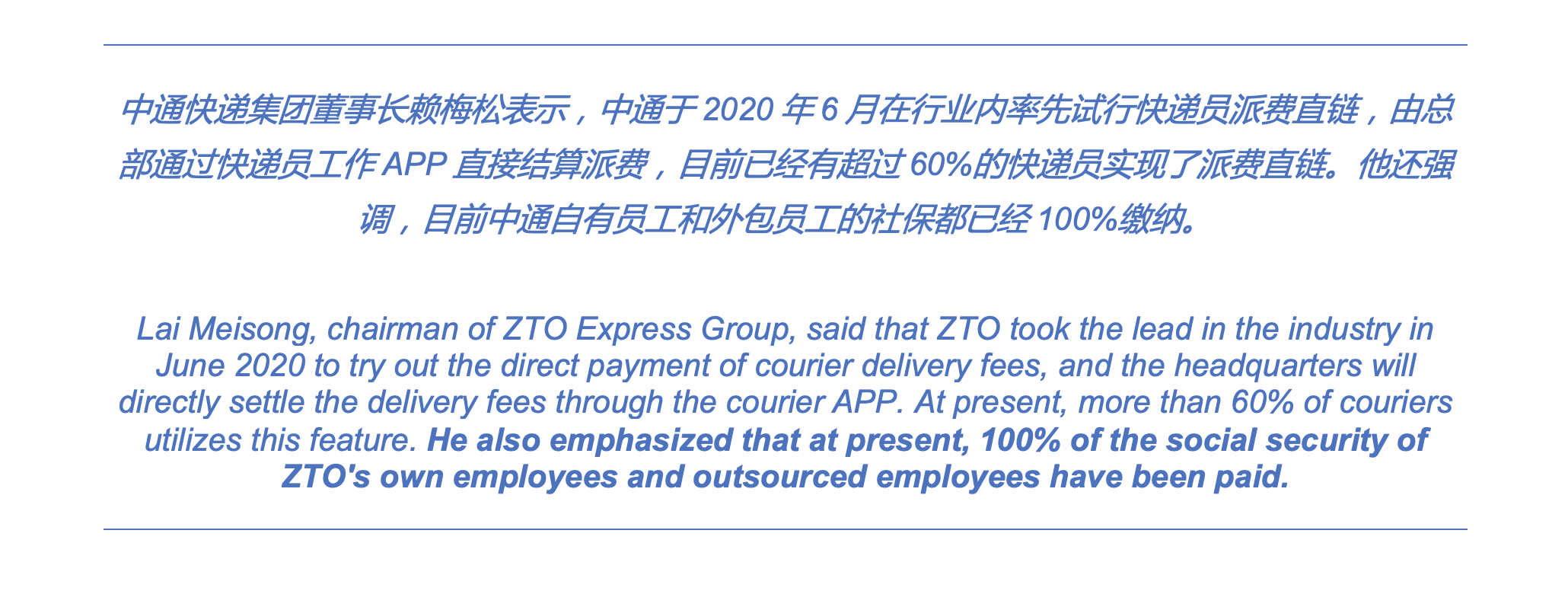

According to our research, this is a misrepresentation. An August 2021 article reveals ZTO’s Chairman Meisong Lai personally claimed the company paid 100% of the social insurance for both full time employees AND outsourced employees.

Recall, ZTO also disclaimed all liability for outsourced personnel and denied any direct contractual relationships existing with them. Are we expected to believe that ZTO is paying for their social insurance as an act of good faith?

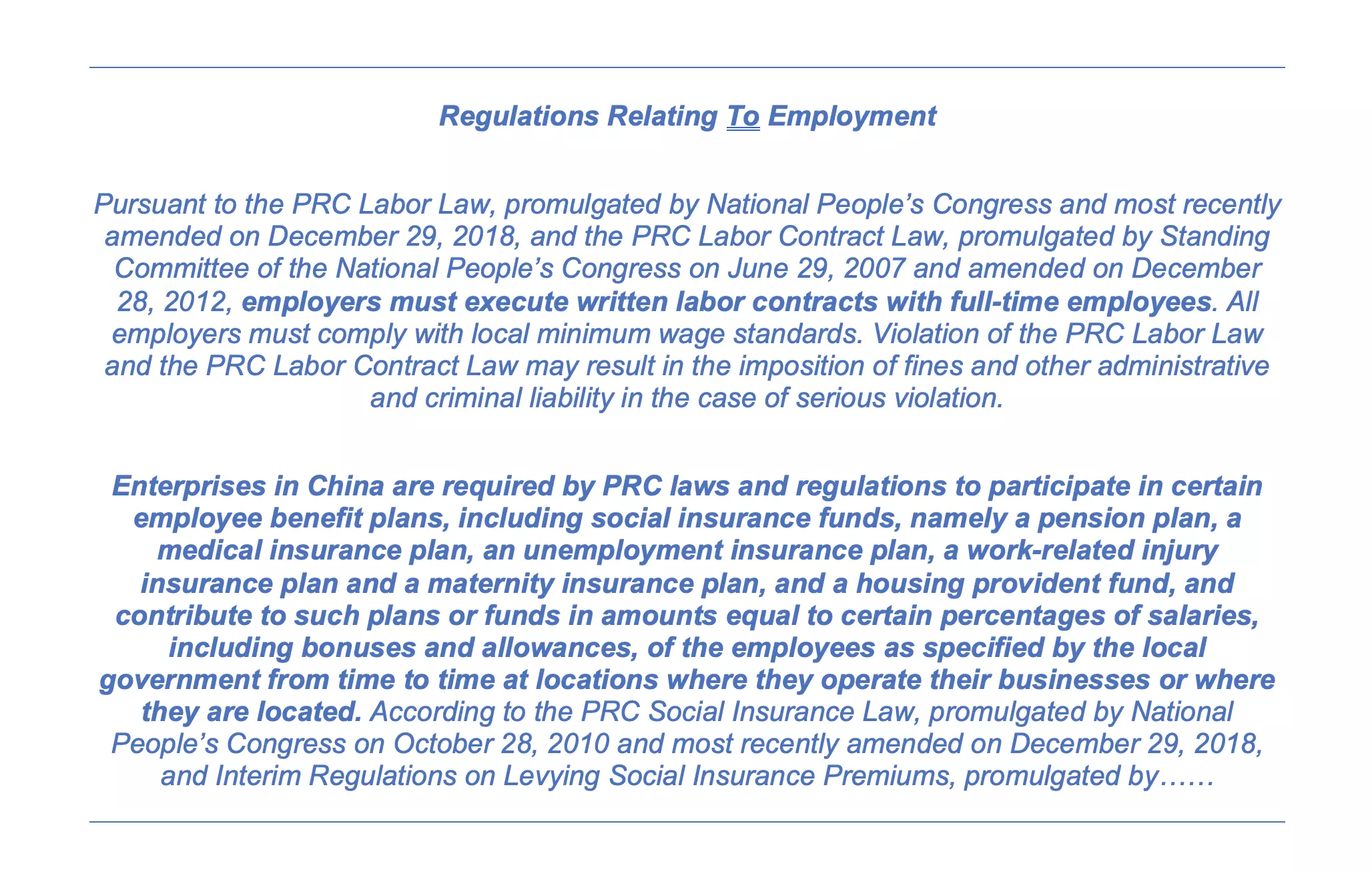

Below are regulations related to employment in China, according to ZTO’s 2021 Annual Report, where enterprises are required to provide benefits including social insurance to only their employees.

We don’t fall for this being some sort of charitable act. Rather, we think ZTO is covering its outsourced employees’ benefits because they are likely ZTO employees. This begs the question: how many employees does ZTO actually have?

Reason 2: Wayback Machine from ZTO’s Website Shows Multiples of Currently Disclosed Employee Count

Based on an archive from ZTO’s website, the company had over 250k employees as of June 2016.

This contrasts ZTO’s 2016 Annual Report filed with the SEC in which disclosed 40.2k employees, including BOTH full-time employees and outsourced personnel, just 1/6 of the figure they disclosed on their own website!

The inconsistency has endured. Per its recent SEC report, ZTO disclosed about 80.9k employees (including full-time and outsourced). This does not sync with a recent article which quoted ZTO’s Chairman, Meisong Lai, stating ZTO had ~0.5M people in its business as of December 2021.

The pattern is clear. In SEC filings, ZTO understates its workforce and deliberately distinguishes between full-time and outsourced employees. Meanwhile, in the Chinese media, the company reveals its true employee count on multiple different occasions.

To estimate ZTO’s potential labor expense for 0.5M employees, we calculated the weighted average salary of the hundreds of positions ZTO is currently advertising on recruitment websites. The average calculated salary is RMB 91,765, resulting in an implied labor expense of RMB 45.9B. Even if we only use the 250k employees that ZTO claimed on its own website in 2016, the total annual labor cost would still be RMB 22.9 B. In comparison, ZTO’s 2021 Annual Report disclosed RMB 8.4B of labor-related costs, ~63% lower than the estimated RMB 22.9B labor cost using figures from ZTO’s own website in 2016, and ~82% lower than the estimated RMB 45.9B labor cost based on the third-party article quoting ZTO’s Chairman Meisong Lai.

Some may question our estimates for labor costs citing ZTO’s reported revenue of RMB 30.4B in 2021. Surely something must be wrong with our estimates if ZTO’s estimated labor costs would be higher than their revenue? Our explanation is we believe ZTO has also underreported revenue. We have found cases where outsourced partners are in fact ZTO controlled/related entities. We believe these entities may operate at lower margins, leading ZTO to shift them off balance sheet. If ZTO consolidated these entities, revenue would be higher, but profit margins would decline.

Regardless, it is certain that ZTO’s labor cost should be much higher than its current disclosed number, thus making its real margins much lower than what was disclosed to public investors.

ZTO’s Endless Cash Hunger Despite Its High Margin Business

One of the benefits of high margins is that it provides a source of funding for future growth. Despite its outstanding profitability, this does not seem to apply to ZTO.

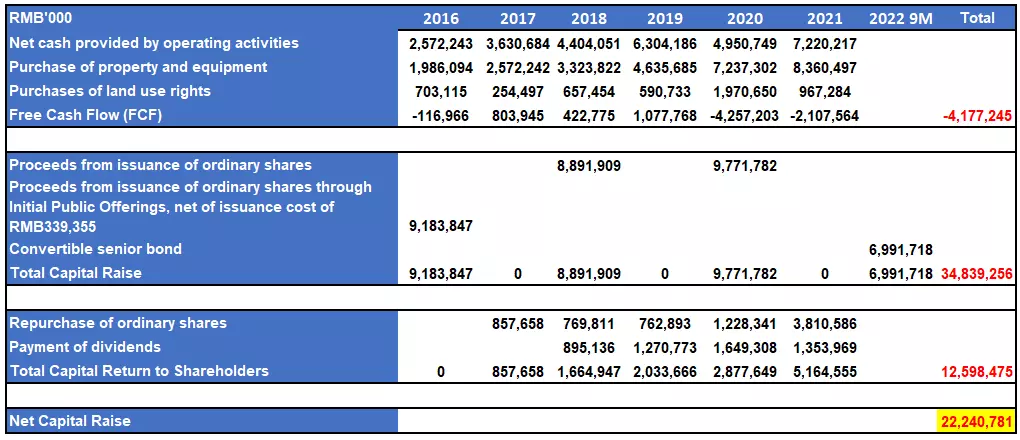

The table below summarizes ZTO’s free cash flow versus total capital raised since its IPO in 2016. Somehow, ZTO boasts blue-chip accounting margins but has reported negative RMB 4.18B free cash flow since 2016. Meanwhile, ZTO has tapped the capital markets for net financing of RMB 22.2B via share issuance and convertible bond issuance since its IPO. We believe this constant need for cash is another red flag suggesting the use of accounting shenanigans.

source: company filings, Grizzly analysis

We considered ZTO’s capital expenditures (CapEx) as this is a common way for income statement profits to be offset on the Statement of Cash Flows and a possible explanation for the cash burn. We are particularly intrigued by the spike in CapEx at ZTO in 2020 and 2021. As investors are likely well aware China’s economy has undergone a dramatic slowdown amid its COVID-19 lockdown policies. Why did ZTO’s CapEx increase from RMB 5.2B in 2019 to RMB 9.2B in 2020, and to RMB 9.3B in 2021? According to these figures, ZTO almost doubled its CapEx in both 2020 and 2021 (vs. 2019) despite facing constant economic disruption from “Zero COVID” policies in the country. We are highly suspect of these cash outflows against this economic backdrop.

source: company filings

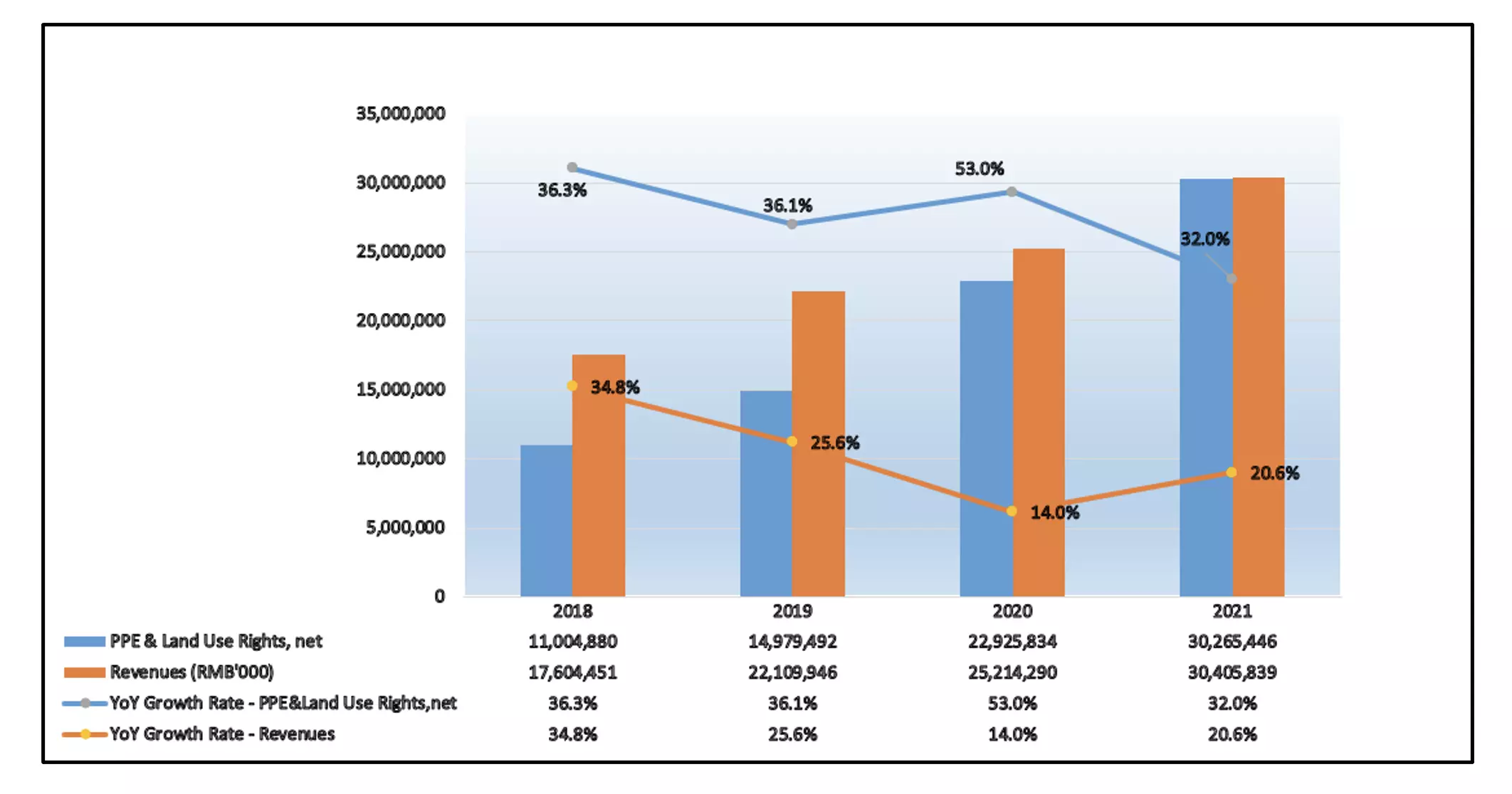

The diagram above compares the year-over-year growth rate on ZTO’s revenues and its property, plant, and equipment (PPE) plus land use rights. We can see that every year the growth rate of net PPE & land use rights exceeds ZTO’s revenue growth rate. For example, in 2021, ZTO’s revenues grew ~21% year-over-year, while net PPE & Land Use Rights grew 32%.

This pace of CapEx relative to revenue growth is unusual. Looking into the issue, we learned ZTO’s Hong Kong prospectus reveals that the company did not obtain title certificates for land use rights with respect to certain parcels of land used by the company and title certificates for certain buildings used as sorting facilities and general and administrative purposes. Without detailed information on the locations of these lands and buildings, it is difficult for investors to make an assessment of the value of these lands and properties, and to know who owns them.

We suspect ZTO has used its glaringly high margins to raise capital, while fake capital expenditures are used to explain away the profits. So far it appears ZTO’s strategy has worked well for them, as they have raised RMB 34.8B from public market investors.

We Believe ZTO Utilized Sham Network Partner Acquisitions to Enrich Insiders

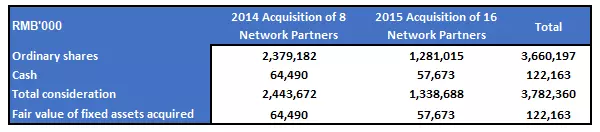

We can see that ZTO paid RMB 122.16M in cash and RMB 3.66B worth of stock to acquire 24 network partners from 2014 to 2015. However, the fair value of the fixed assets of these 24 network partners in total is only RMB 122.16M, which is exactly the amount of cash paid by ZTO.

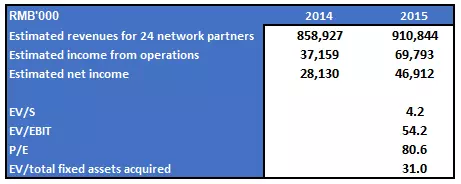

Based on the estimated financials of these 24 network partners provided by ZTO, it appears that ZTO has vastly overpaid for these acquisitions. For example, as for 2015, the total consideration to operating income is 54.2x, and the total consideration to net income is over 80x. In addition, the total consideration to fixed assets acquired is an astonishing 31.0x!

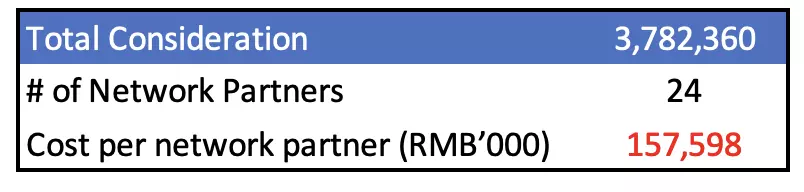

Another way to look at this transaction is to use the acquisition cost per network partner from 2014 to 2015 and compare it to current and publicly available costs to join ZTO’s network.

According to our calculations, the cost per network partner from acquisition averaged almost RMB 160M. Just to give a frame of reference: based on third-party website, the total investment amount required to open a network partner in the capital city of provinces is only RMB 322,000.

source: https://www.jiamengfei.com/xm/2289

It seems ZTO has drastically overpaid for its network partner acquisitions from 2014 to 2015.

Evidence Shows that 2014 Acquisitions Might Have Never Happened; Money was Paid but No Ownership was Transferred

According to the Chinese corporate database Qichacha, among the 8 network partners ZTO claimed to have acquired in 2014, 3 network partners show no history of ownership change to ZTO. 8 years after the “acquisitions”, these supposedly acquired companies have never listed ZTO or ZTO subsidiaries as its shareholders. This does not square with RMB ~1.295B ZTO claims to have used to acquire 4 network partners (including these 3) from one group of sellers. In reality, it seems the companies were never actually transferred! Where did the cash go? We strongly suspect these funds were siphoned off by insiders.

Company 1: Shenzhen Chengxin ZTO Industrial Co., Ltd. (“Shenzhen Chengxin”; 深圳市诚信中通实业有限公司)

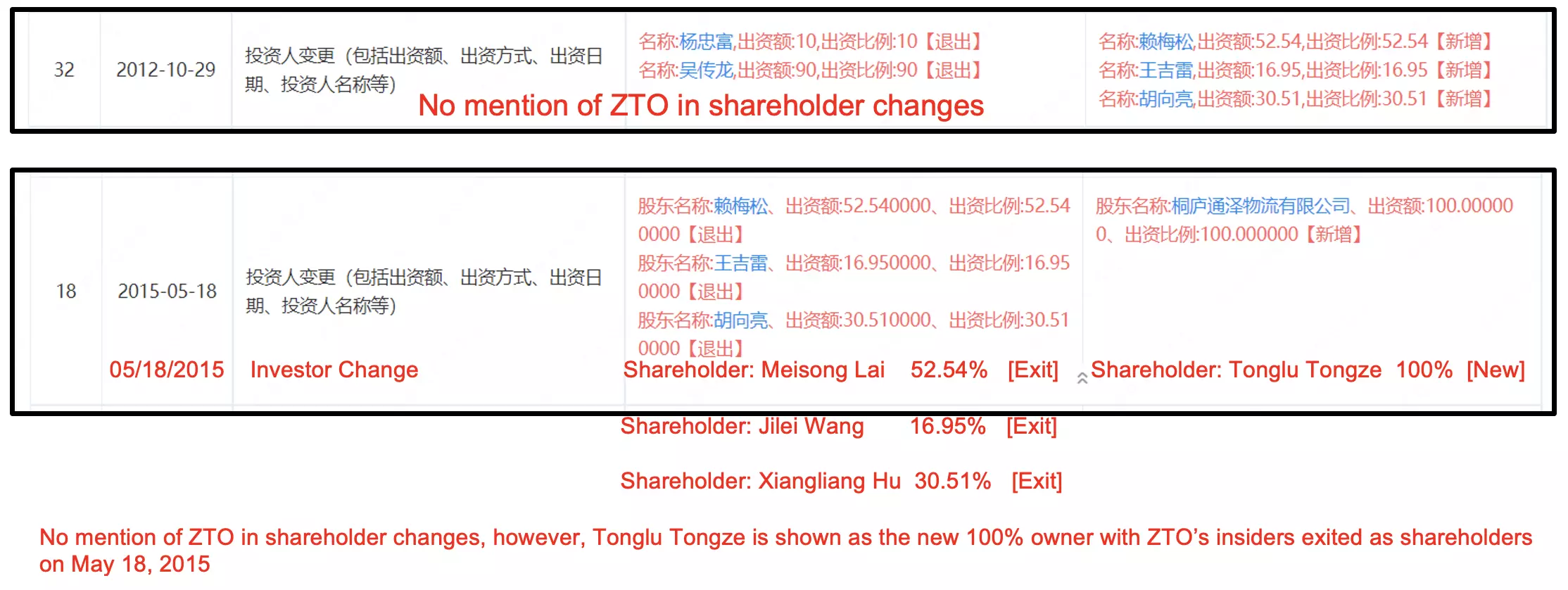

The shareholder change record from Qichacha shows no history of ZTO or a ZTO subsidiary being a shareholder. There was not shareholder/investor change in the year of 2014. However, Tonglu Tongze, a related party disclosed by ZTO itself, became Shenzhen Chengxin’s 100% shareholder in 2015. Tonglu Tongze is not owned by ZTO, but rather majority-owned by ZTO employees.

Moreover, we can refer to the investor change information for 2015 above. The previous shareholders of Shenzhen Chengxin before it became a 100% owned entity by Tonglu Tongze in 2015 are Meisong Lai (52.54%), Jilei Wang (16.95%), and Xiangliang Hu (30.51%). In ZTO’s 2016 prospectus, it listed Meisong Lai as Founder, Chairman and CEO, Jilei Wang as Director and VP of Infrastructure Management, and Xiangliang Hu as Director and General Manager of Guangdong Province. In other words, all these three shareholders of Shenzhen Chengxin are ZTO’s insiders.

Company 2: Guangzhou Xin ZTO Express Co., Ltd. (“Guangzhou Xin”; 广州鑫中通速递有限公司)

The company was established on 01/31/2009. Shareholders were never changed before it was deregistered on 08/06/2017. It appears that ZTO’s insiders Meisong Lai (52.54%), Jilei Wang (16.95%), and Xiangliang Hu (30.51%) were also Guangzhou Xin’s shareholders before it was deregistered.

Company 3: Dongguan Kaisheng ZTO Express Co., Ltd. (“Dongguan Kaisheng”; 东莞市凯盛中通快递有限公司)

According to Qichacha, there was no shareholder change in 2014.

Up until now, the company’s 100% shareholder is an individual called Jiangen Yu, rather than ZTO or a ZTO subsidiary.

Evidence Shows that 2015 Acquisitions also Might Have Never Happened; Again, No Ownership was Transferred

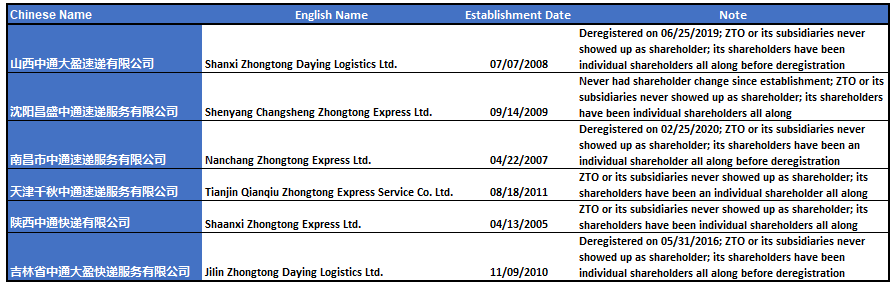

We observe a similar pattern in 2015. Although ZTO didn’t disclose the names of all 16 network partners, we identified 6 network partners where ZTO used to have equity interest and later acquired the rest of the interest in October 2015. These 6 network partners and their information are summarized in the table below.

source: company filings, Qichacha, Grizzly analysis

Of these 6 network partners listed above, ZTO has explicitly stated that it “had been our equity investee until it was acquired by us in October 2015”. ZTO spent RMB 213.14M in total consideration (RMB 22.68M in cash + 3,915,720 ordinary shares @ RMB48.64 per share). However, based on the SAIC information we found on these 6 companies; we seriously doubt the acquisition ever happened. ZTO or its subsidiaries never appeared as shareholders of these 6 companies before or after October 2015!

ZTO didn’t disclose the other 10 network partners that it acquired in October 2015 (3 network partners in Fujian province and 7 network partners owned and operated by unrelated third parties). However, based on the 6 network partners we were able to identify, we strongly suspect that these remaining 10 network partners were not really acquired either.

We see that the 2015 acquisitions share the same pattern as we show above for the 2014 acquisition. We highly suspect the acquisition considerations went into the pockets of insiders, mainly Chairman Meisong Lai and his affiliates. ZTO shareholders seem to have paid tons of money for nothing but thin air!

We Believe ZTO Enriched Insiders with Related Party Transactions

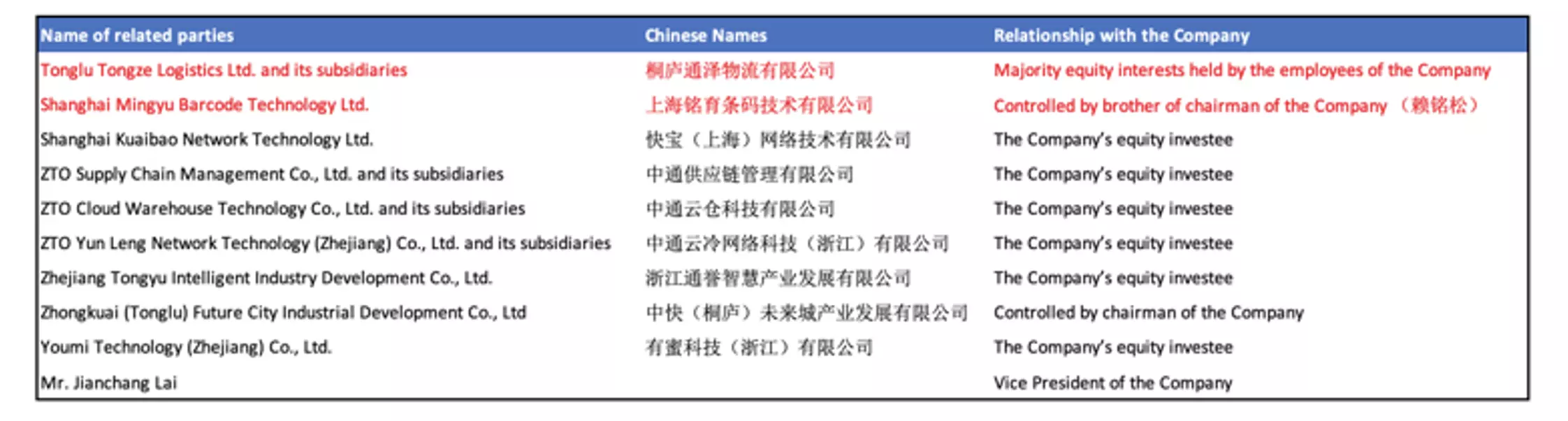

ZTO disclosed the following related parties in 2021. There are two companies that deserve scrutiny.

Tonglu Tongze: Unreasonable Payment to A More Than Related Company

According to Qichacha, Weimin Chen is the legal representative of Tonglu Tongze, and Fang Wang is the 40% owner. These two individuals are also employees of ZTO. This makes Tonglu Tongze a related party. For starters, we find it highly questionable that ZTO employees also run logistics related businesses on the side. However more concerning is that media reports in China suggests that Tonglu Tongze is much more than a related party and should rather be consolidated as a subsidiary.

According to this article, Fang Wang is (ZTO)’s Supervisor of Service Quality Center, and she represented the company in hiring for ZTO.

![]()

In another article, Weimin Chen was referred to as the VP of Gansu Zhongtong Management Center (Gansu ZTO). It seems that the company is much more closely connected to ZTO than the company suggests.

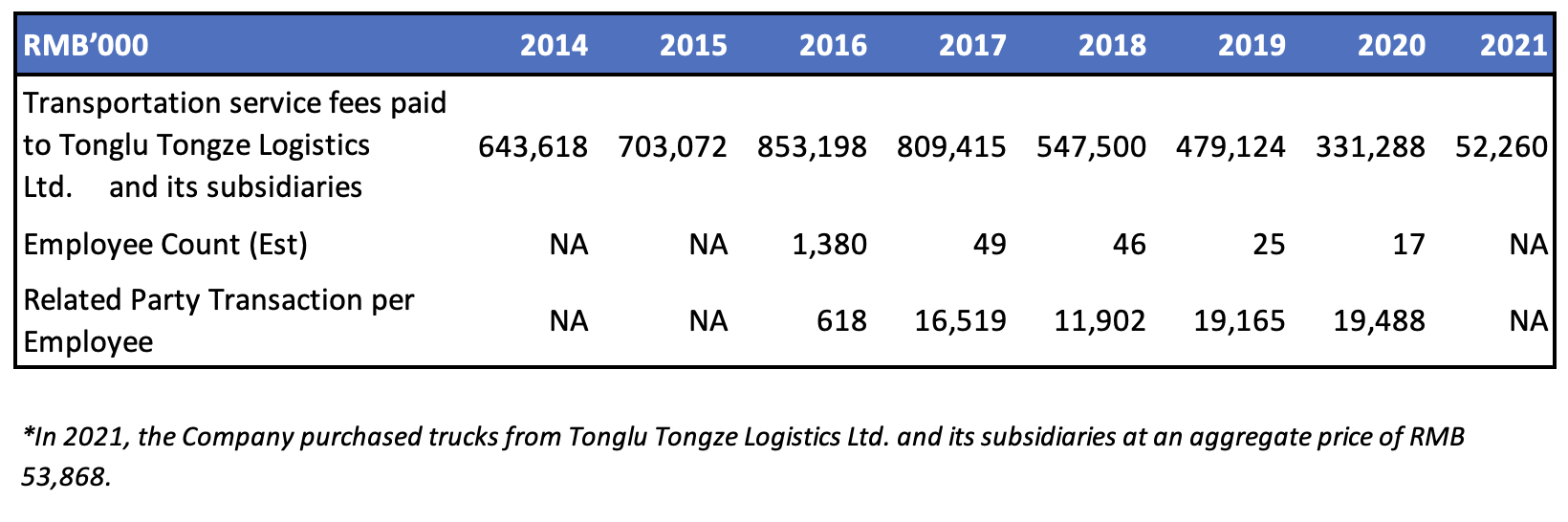

Furthermore, ZTO has ongoing business with Tonglu Tongze as disclosed in its annual reports.

We see that ZTO was paying hundreds of millions RMB to Tonglu Tongze for transportation services from 2017 to 2020. We do see a reduction in such fees from 2019 onwards, which we believe is consistent with the overall underperforming Chinese economy due to covid lockdowns.

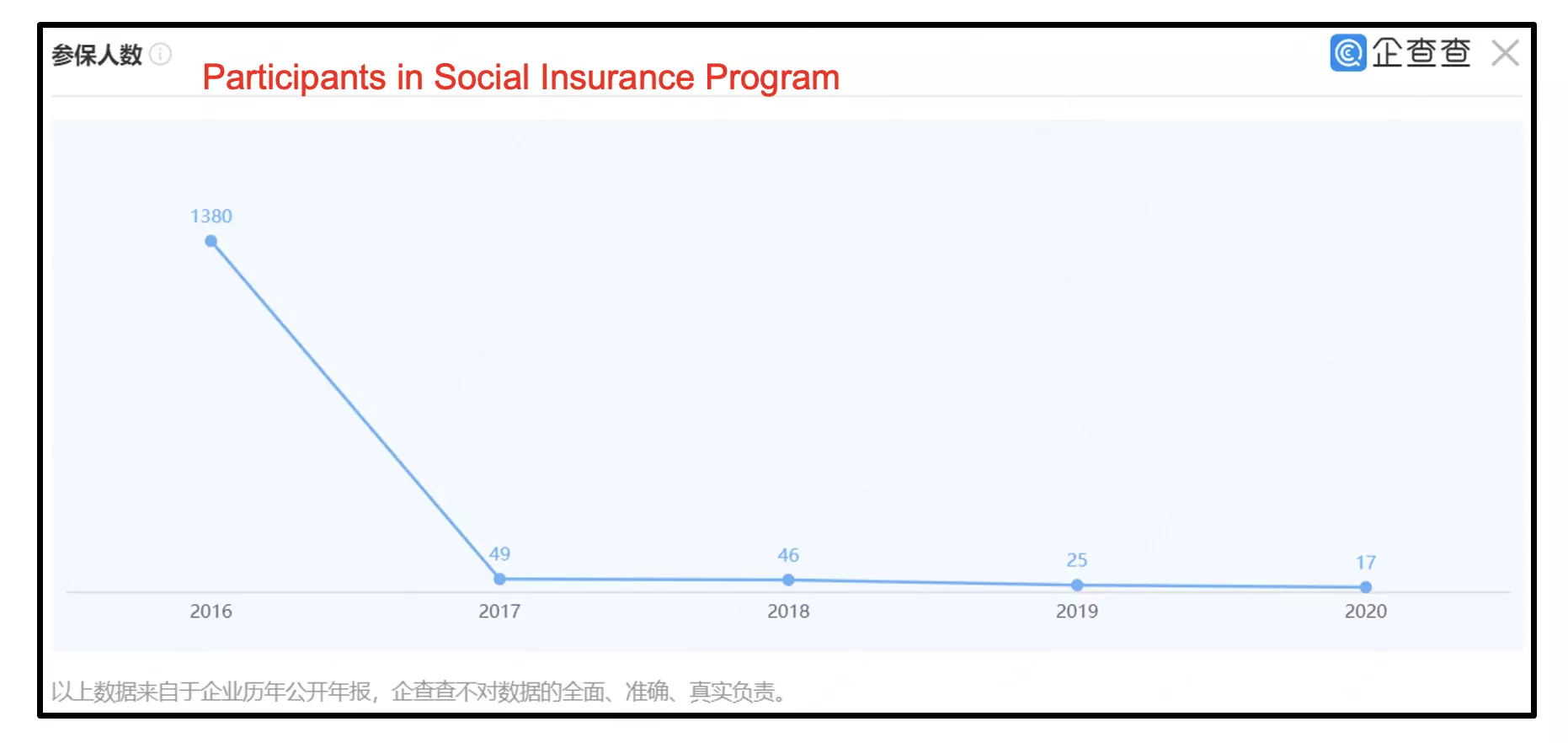

Looking at Tonglu Tongze’s employee count, however, reveals more suspect details.

According to Qichacha, the number of Tonglu Tongze’s employees that participated in the social insurance program (which usually only full-time employees are able to participate in) decreased from 1,380 in 2016 to 49 in 2017. The employee count further decreased to 46 in 2018, 25 in 2019, and 17 in 2020, respectively. Essentially, despite employee count decreasing from over 1,000 to less than 50 in 2017, ZTO was still paying almost the same amount of money to Tonglu Tongze (RMB 809.4 million in 2017 vs RMB 853.2 million 2016). Even after Tonglu Tongze’s employee count continued to decline after 2017, ZTO was still paying RMB 300-500M of transportation service fees to Tonglu Tongze. How can a company with only 17 employees in 2020 generate ~40% of what it did with 1,380 employees (RMB 331.3M in 2020 with 17 employees vs RMB 853.2M in 2016 with 1,380 employees)? The revenue per employee increased by roughly 31 times!

This is mind-blowing to us, and it certainly makes us believe that the management of ZTO has been siphoning money out of ZTO to Tonglu Tongze via this related party transaction.

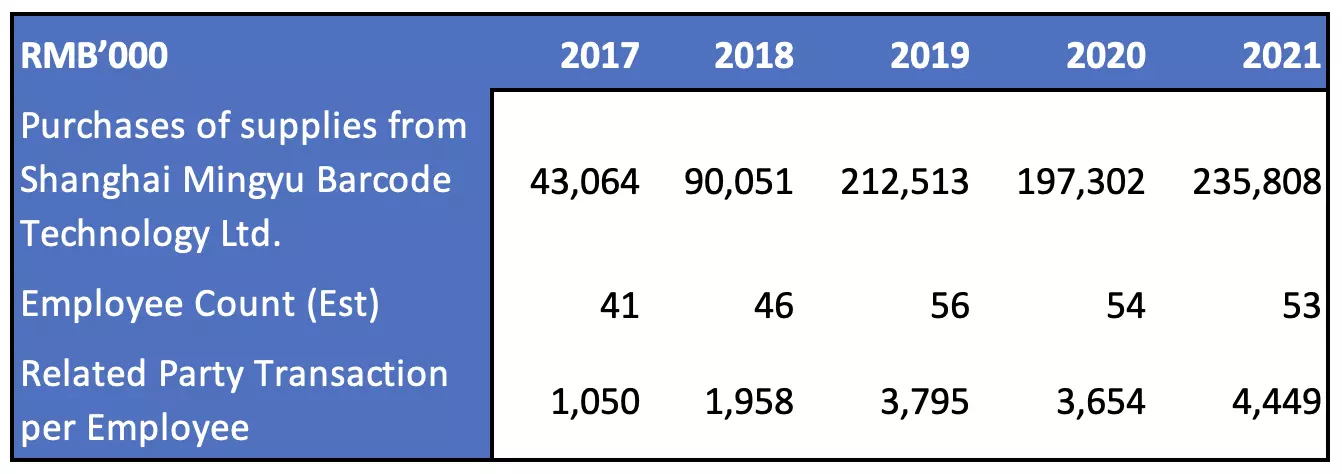

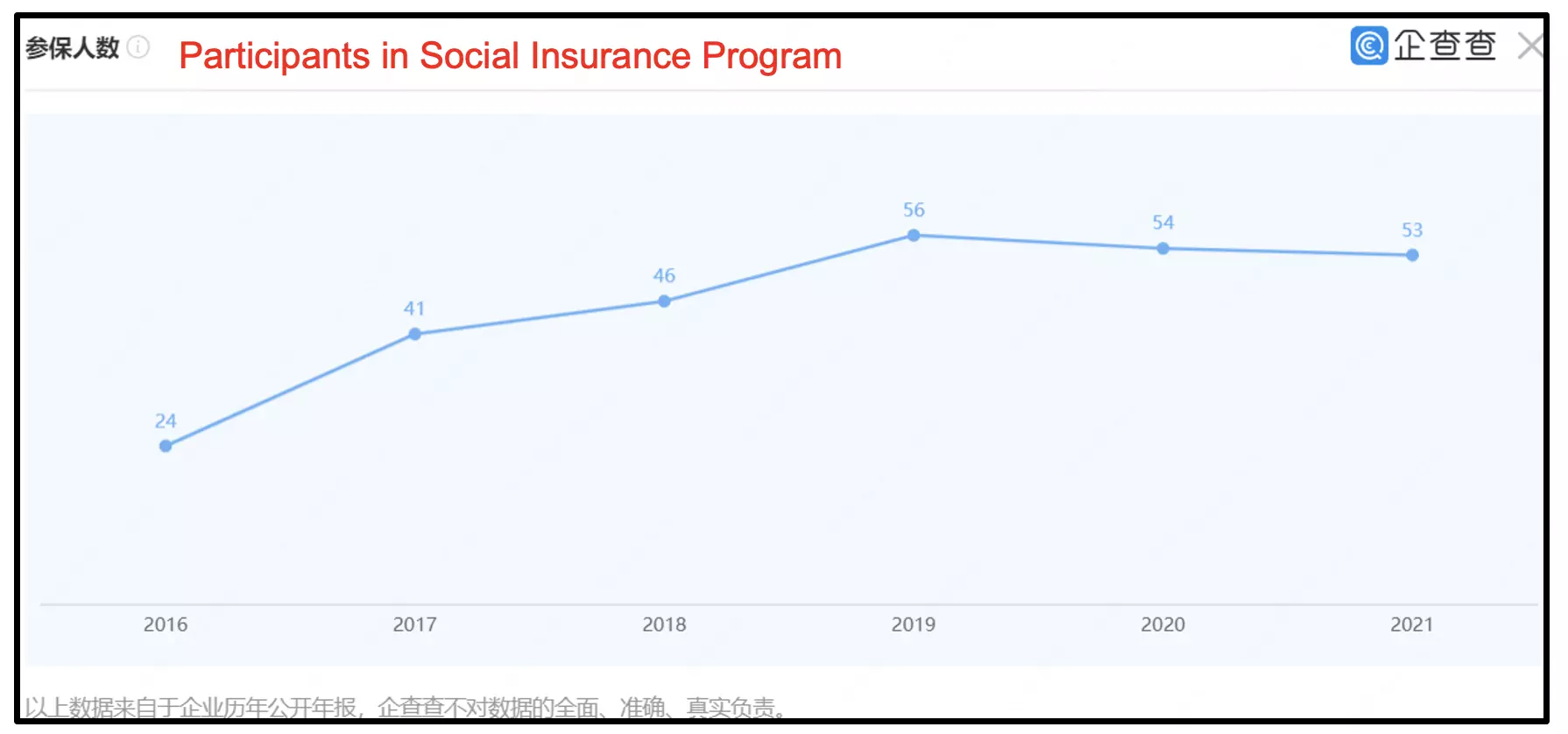

Shanghai Mingyu: Disproportional Growth Indicates Questionable Related Party Payments

According to ZTO, Shanghai Mingyu is controlled by the brother of the Chairman of the Company. We found out that the name of the brother of ZTO Chairman’s is Mingsong Lai. Based on ZTO’s disclosure, the related party transactions with this business have increased from RMB 43.1 million in 2017 to RMB 235.8 million.

However, based on Qichacha, its employee count only increased from 41 in 2017 to 53 in 2021.

We think it’s reasonable to question what business ZTO is conducting with Shanghai Mingyu to drive such dramatic increase in the transaction volume, despite just a modest uptick in headcount.

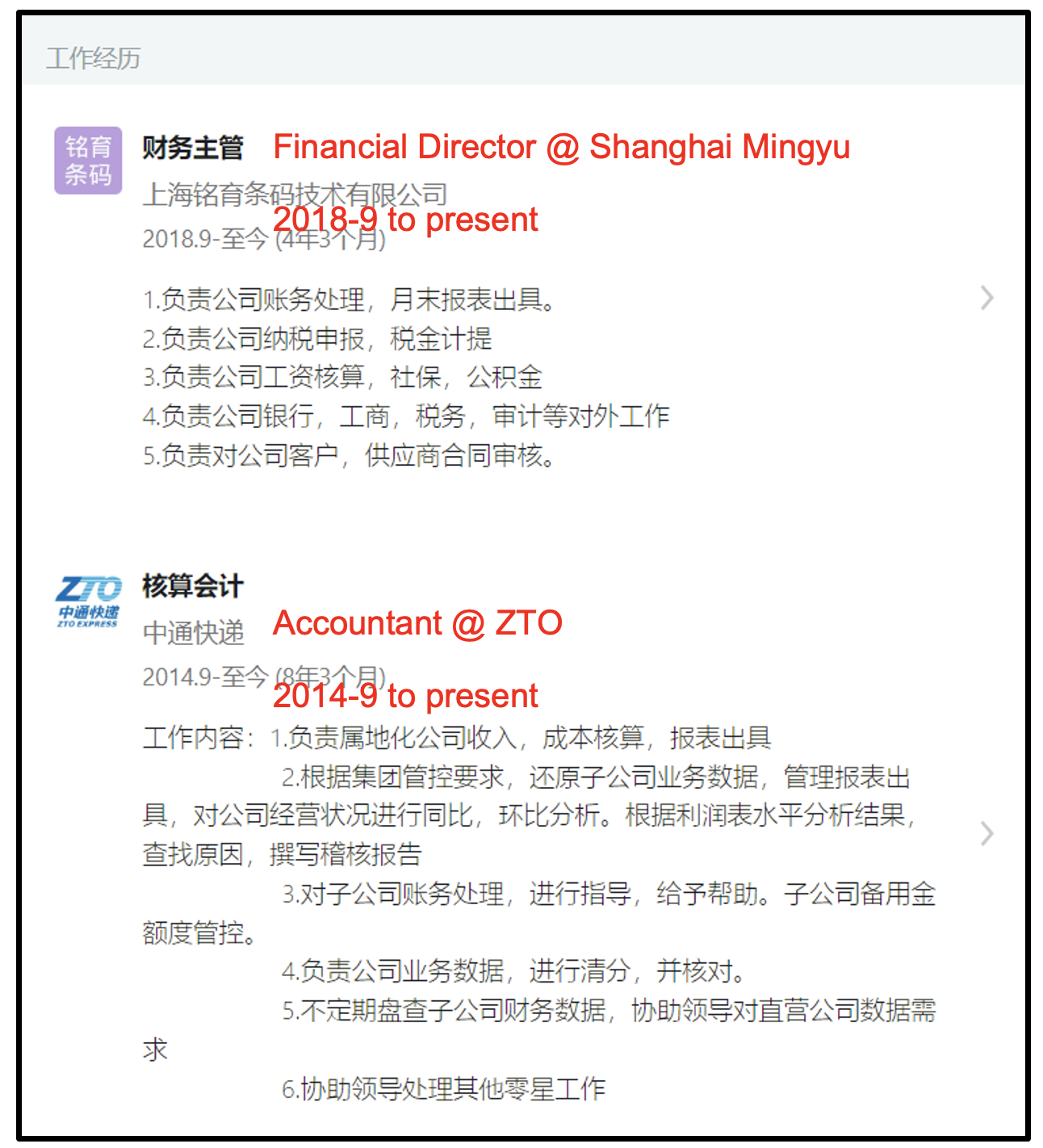

We also found that the Shanghai Mingyu’s Director of Finance is also a ZTO Accountant. The resume for this individual, Fengli Ma, per maimai.cn (a social network site in China that is similar to LinkedIn in the U.S.) shows that she has been working for ZTO as an Accountant since September 2014. Fengli Ma has simultaneously been working for Shanghai Mingyu as a Director of Finance since September 2018. If the accounting for both companies is done by the same group of people, how can investors of ZTO be assured that the transactions between ZTO and Shanghai Mingyu are at arms-length and fair? We believe the company controlled by the brother of ZTO’s chairman is also used to funnel cash from ZTO to insiders.

source: www.maimai.cn

ZTO Is Introducing More Risks By Lending Money to Real Estate Related Parties

We discovered evidence that ZTO’s controller Lai and his affiliates are using ZTO to bankroll personal real estate projects. Investing in the Chinese real estate sector currently carries tons of risks on its own. If these loans go into default, it is likely that ZTO shareholders will have to bear the risks.

ZTO has been lending money to its related parties, namely Zhongkuai (Tonglu) Future City Industrial Development Co., Ltd (“Zhongkuai Tonglu”; controlled by ZTO’s Chairman) and Zhejiang Tongyu Intelligent Industry Development Co., Ltd. (“Zhejiang Tongyu”; ZTO’s equity investee).

As of December 31, 2021, Zhongkuai Tonglu and Zhejiang Tongyu together owe RMB 611.1 million to ZTO. Note both entities’ main business is related to real estate development. Investors who have kept following China’s economy would know that currently there is a large risk in the real estate sector. And we believe it is a large red flag that ZTO is lending money out to related parties that are within the real estate business sector.

For example, Zhongkuai Tonglu is reported to be developing both commercial and residential properties in the city of Hangzhou, Zhejiang Province in China.

According to a Tonglu County’s press release, Zhongkuai Tonglu is the construction company for second category residential properties (mid to high-level residential buildings, with a total of 1,184 apartments and a construction area of 225,410 square meters).

Source: http://www.tonglu.gov.cn/art/2021/3/5/art_1572937_58962648.html

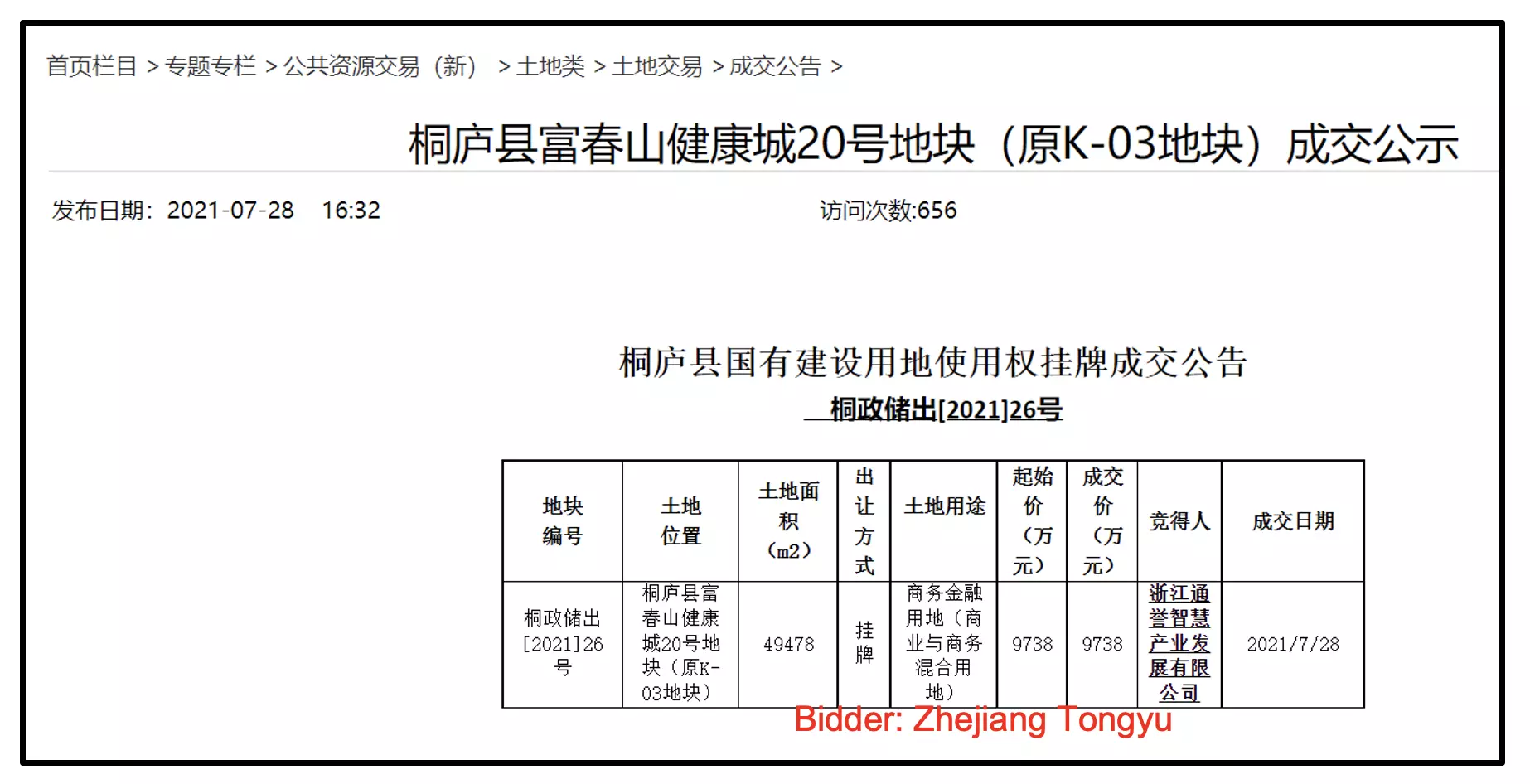

Hongqun Hu(胡红群), Zhejiang Tongyu’s main shareholder, is the COO of ZTO. While Zhejiang Tongyu’s Legal Representative, Jianchang Lai (赖建昌), is also a ZTO related party.

The Tonglu County local government disclosure shows that Zhejiang Tongyu purchased land on July 28, 2021 for a consideration of RMB 97.38M, and the land usage is for commercial and financial purposes. The total area of the land is 49,478 square meters.

Source: http://www.tonglu.gov.cn/art/2021/7/28/art_1229514952_58988070.html

Source: https://zrzyt.zj.gov.cn/art/2021/8/2/art_1229457153_126130.html

We think that it is a huge red flag that ZTO is lending money to businesses controlled by insiders which are completely unrelated and carry tremendous risks in the current environment.

Moreover, besides lending money to these two entities, ZTO also lent out over RMB 300M to its employees in through various channels. Added together, ZTO lent out almost RMB 900M to its related parties and employees.

Do you really want to be a shareholder in a company that is clearly abused by insiders as their private piggy bank?

Multiple Undisclosed Related Parties Raise Further Serious Concerns

Thus far, our report has highlighted several entities which are operating at less than arms-length. These relationships seem detrimental to shareholders. Unsurprisingly, we have found multiple other undisclosed related parties that further call into question the integrity of ZTO’s financial statements.

Wayzim Technology Co., Ltd (Wayzim Technology; 688211.SS)

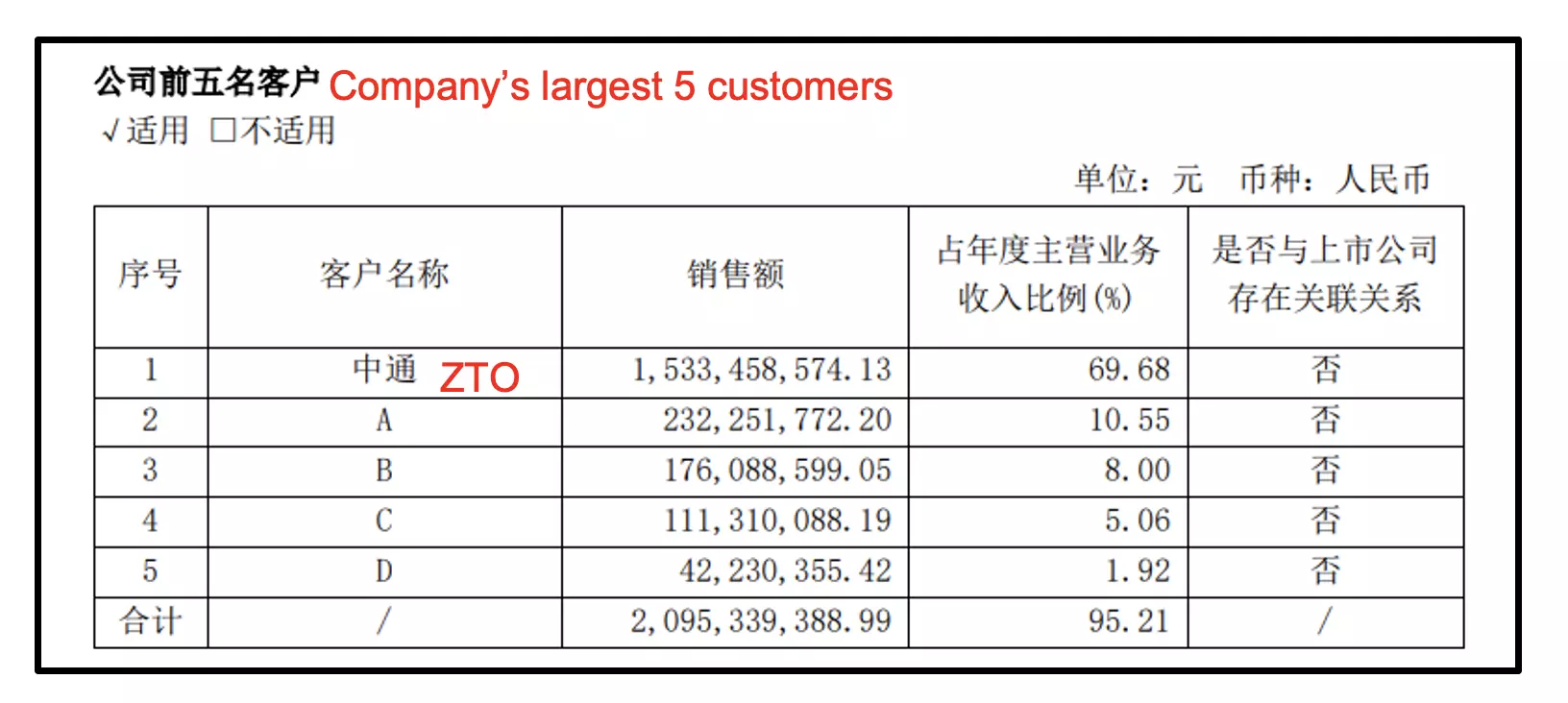

Wayzim Technology Co., Ltd. (“Wayzim Technology”; 688211.SS) is a public company in China’s A share market, and it engages in research and development, design, manufacture, and sale of intelligent logistics sorting systems for the logistics express industry in China and internationally. Based on its own disclosure, ZTO has been its largest customer since 2018. For example, Wayzim Technology’s revenues from ZTO in 2021 were RMB 1.53B, accounting for 69.7% of its total revenues.

Source: Wayzim Technology 2021 Annual Report

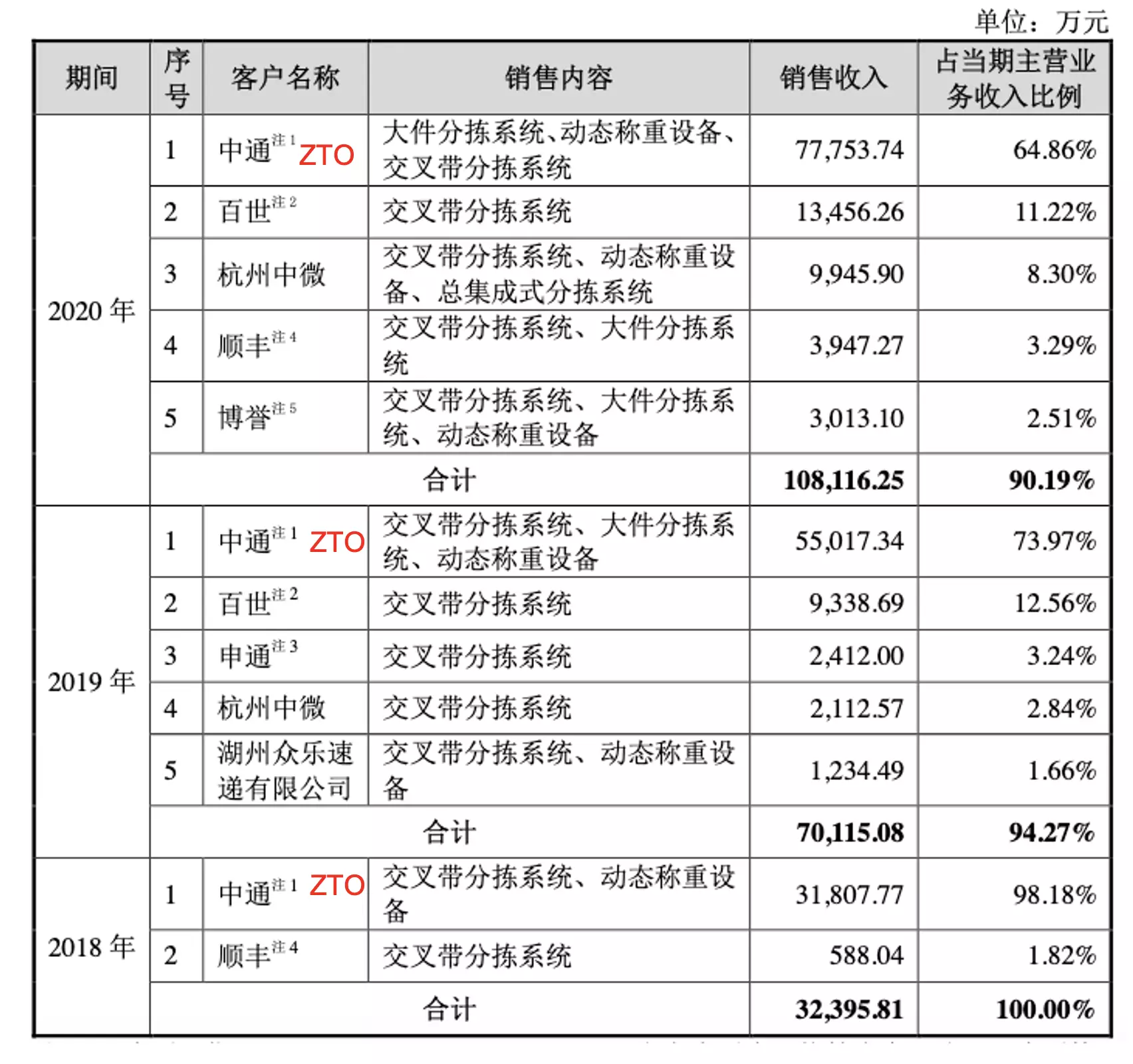

We can see that Wayzim in the diagram above did not disclose the exact names of the other 4 largest customers. However, in Wayzim Technology’s prospectus from 2019, its disclosure was more detailed.

Source: Wayzim Technology Prospectus

According to the prospectus, ZTO has been Wayzim Technology’s largest customer from 2018 to 2020. Although Wayzim’s total revenue attributed to ZTO has decreased from 98.2% in 2018 to 64.9% in 2020, they continue to be heavily dependent upon ZTO as a customer today.

An article in China shared our concern about the abnormally high revenue contribution from ZTO and outlined a series of problems regarding ZTO’s “favorable treatment” to Wayzim Technology.

The key points are as follows:

- Wayzim Technology’s gross margin (42.6%, 42.3%, and 38.3% in 2018, 2019, and 2020) and net margin (13.2%, 17.9%, and 17.7% in 2018, 2019, and 2020) are noticeably higher than its other two competitors in that sector. Wayzim’s explanation for these unusually high margins is far-reaching

- The relationship between Wayzim Technology and its largest customer ZTO, is ambiguous.

- For 2019 and the first 9-months of 2020, Wayzim’s gross margin from ZTO’s business was 47.2% and 45.6%, respectively. This compares to 41.0% and 37.7% gross margins the company generates from another logistics customer, Best Inc.

- ZTO demonstrates high purchase volume with Wayzim Technology which may be an act of undermining ZTO’s minority shareholders.

- In addition, after signing a contract, ZTO would pay a 60-70% upfront fee. Meanwhile, Best Inc. makes an upfront payment of just 30% of the contract value.

- From 2017 to 2019, Wayzim borrowed RMB 20M and 40M from ZTO’s subsidiary; There was no interest on the RMB 40 million loans. What is the business logic behind this non-interest loan between these two parties?

Based on the facts we have provided, we believe Wayzim should be considered a related party.

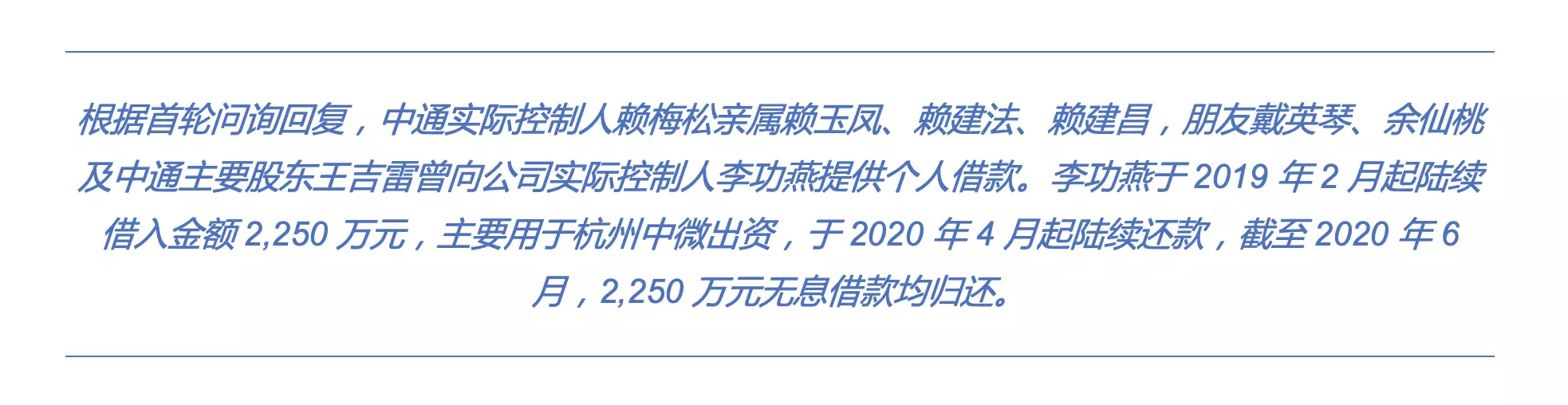

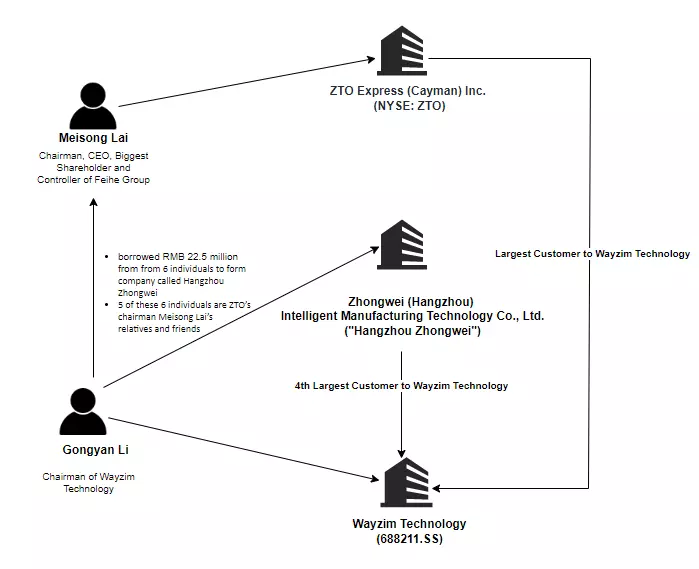

According to the second reply to the stock market regulator in China (CSRC), Wayzim Technology’s founder, Gongyan Li, borrowed RMB 22.5M from 6 individuals. 5 of these lenders are evidently relatives and friends of ZTO’s Chairman, Meisong Lai. The loans were entirely interest free! The other lender is one of ZTO’s main shareholders, Jilei Wang. The proceeds from these loans were used by Gongyan Li to jointly establish a subsidiary with Wayzim Technology, named Hangzhou Zhongwei. Note, Hangzhou Zhongwei is the 4th largest customer of Wayzim Technology.

Given the relationship between Wayzim Technology’s founder, Gongyan Li, and ZTO’s Chairman, Meisong Lai, we believe ZTO should have disclosed Wayzim as a related party. This undisclosed relationship also potentially explains the favorable terms Wayzim has received from ZTO versus those offered to other clients.

In our view, it is highly likely ZTO’s management has been engaging in undisclosed related party transactions to benefit Wayzim Technology and its founder, Gongyan Li. The relationships between ZTO and Wayzim Technology, as well as Gongyan Li and Meisong Lai, are illustrated in the graphic below.

Source: company filings, grizzly analysis

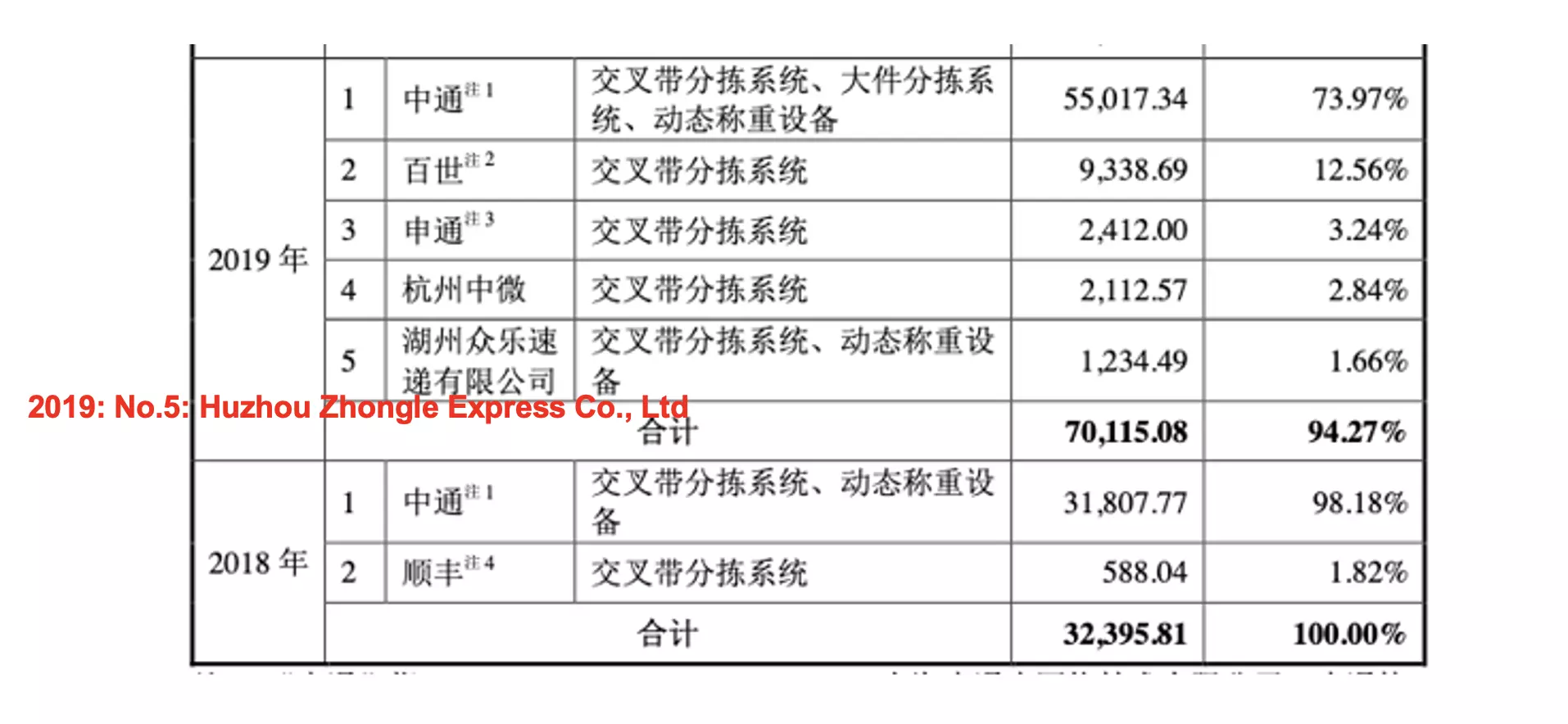

Upon diving deeper into Wayzim Technology’s customers, we discovered that it is highly likely that ZTO might be using unconsolidated entities to offload costs. For example, in 2019, the 5th largest disclosed customer of Wayzim Technology was Huzhou Zhongle Express Co., Ltd. (“Huzhou Zhongle”). It is worth noting Huzhou Zhongle has been displayed similar purchasing behavior to ZTO. Some of these similarities include purchases of sorting systems and dynamic weighing equipment.

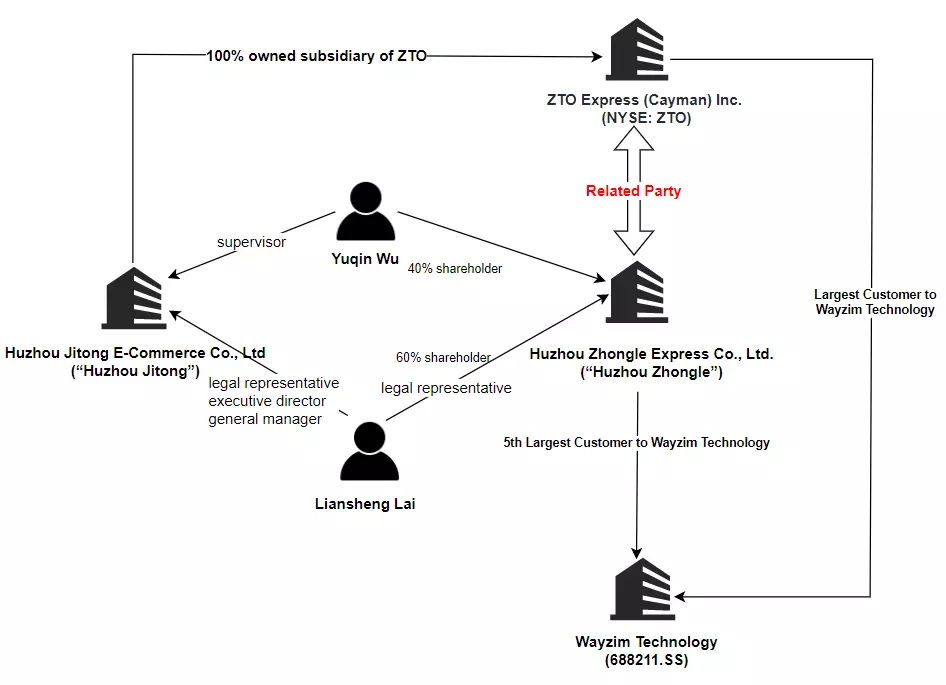

According to Qichacha, Liansheng Lai and Yuqin Wu are the beneficial owners of 60% and 40% of Huzhou Zhongle, respectively. On the surface, these two individuals appear unrelated to ZTO. Liansheng Lai is the executive director, general manager, and the legal representative of Huzhou Zhongle.

However, this same Liansheng Lai is also the legal representative of another company called Huzhou Jitong E-Commerce Co., Ltd (“Huzhou Jitong”). Through the shareholder change history, we found find that Liansheng Lai and Yuqin Wu owned 60% and 40% of the company, respectively. This was the case until April 2016 when their stake in Huzhou Jitong was transferred to Shanghai Zhongtongji Network Technology Co., Ltd. (“Shanghai Zhongtongji”). Shanghai Zhongtongji is a wholly-owned subsidiary of ZTO. However, Liansheng Lai remained the executive director, general manager and legal representative of this company which is now owned by ZTO. In addition, Yuqin Wu is also the supervisor at Huzhou Jitong currently.Per this chain of events, we suspect Huzhou Zhongle is currently working with ZTO today.

The diagram below shows the relationship between Huzhou Zhongle and ZTO.

Source: company filings, grizzly analysis

source: https://m.kuaidi100.com/network/net_3305_02200_3_1.htm

We also discovered that Liansheng Lai was listed as the main contact at a ZTO location in Huzhou, as shown in the screenshot above.

In other words, Liansheng Lai, who is currently the executive director, general manager and legal representative of Huzhou Jitong, a wholly owned subsidiary of ZTO, also owns 60% of Huzhou Zhongle and acts as Huzhou Zhongle’s executive director, general manager, and legal representative. Therefore, Huzhou Zhongle is definitely an undisclosed related party to ZTO and very likely under the control of ZTO too. In 2019, Huzhou Zhongle purchased RMB 12.3 million in sorting and weighting-related equipment, according to Wayzim Technology’s disclosure. We believe these purchases were likely off-loaded by ZTO to Huzhou Zhongle.

Site Visits Reveal Even More Undisclosed Related Parties

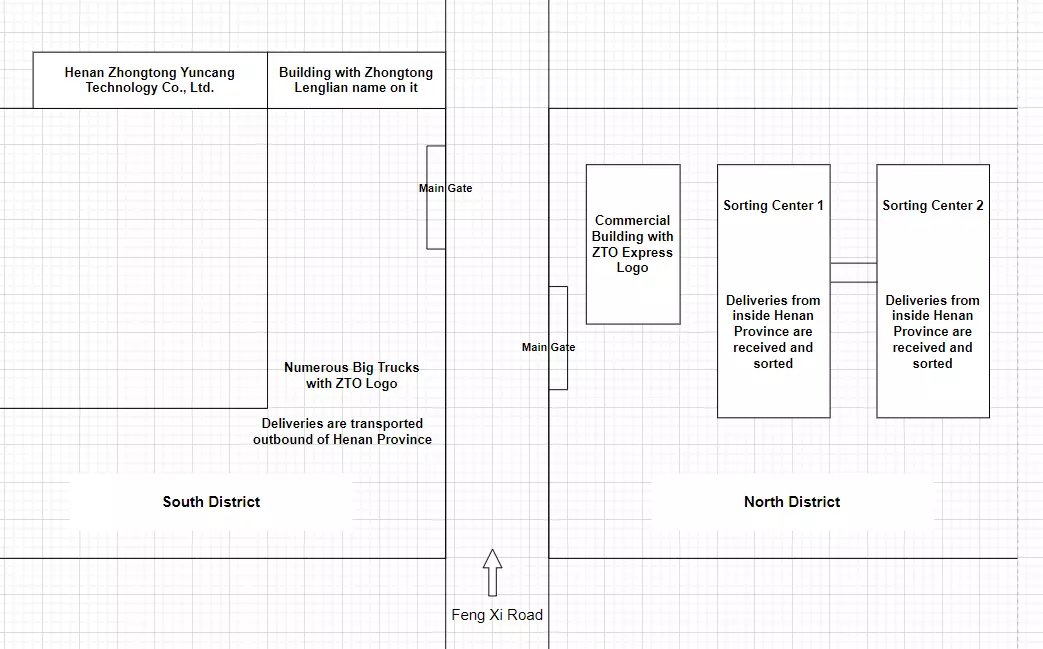

We conducted site visits to understand how ZTO’s network of companies interacts in practice. As part of our investigation, we visited what we found to be ZTO’s headquarters in Henan Province. We also identified another concrete company that we believe might be used by ZTO to off-load costs. Information on this entity, Henan Zhongtong Express Service Co., Ltd. (Chinese name: 河南中通快递服务有限公司, “Henan Zhongtong Express”), is provided in the below excerpt from Qichacha.

Henan Zhongtong Express Service Co., Ltd.

Address: Zhengzhou Economic Technology Development District Zhengzhou International Logistics Park Eastern Road North Part Road’s West

There are two other companies which are both 100% owned by ZTO and have the same registered address as Henan Zhongtong Express. These entities are (1) Henan Jirui Logistics Co., Ltd. (Chinese name: 河南省吉瑞物流有限公司,”Henan Jirui”); and (2) Henan Jirui Warehousing Service Co., Ltd.(Chinese name: 河南省吉瑞仓储服务有限公司, “Jirui Warehousing”). Our on-the-ground team used the address on Qichacha to try to find Henan Zhongtong Express. Upon exploring this turf, however, we were led into an area with numerous companies related to ZTO.

source: on-the-ground due diligence, Grizzly analysis

Images 1 and 2 below show the commercial building with ZTO’s logo and the name of Zhongtong Kuaidi (in Chinese). Based on our conversation with people near this area, we confirmed Henan Zhongtong Express is located in the area too. Image 3 below shows a building where numerous big trucks with ZTO’s logo are parked. We learned that this is the south district and these trucks would transport deliveries out of the Henan Province.

Image 1: Commercial building with ZTO’s logo

Image 2: Distance vision of Image 1

Image 3: Site for province outbound deliveries

We also saw logos for ZTO’s investment company, Henan Zhongtong Yuncang Technology Co., Ltd. (Chinese name: 河南中通云仓科技有限公司, “Henan Yuncang”). Henan Yuncang is 100% owned by Zhongtong Yuncang Technology Co., Ltd (Chinese name: 中通云仓科技有限公司,”Zhongtong Yuncang”), which ZTO owns 16.36% of. Even more interesting, Zhongtong Yuncang’s largest shareholder (24.5%) is a company called Zhejiang Zhongjun Investment Management Co., Ltd (Chinese name: 浙江仲君投资管理有限公司, ”Zhejiang Zhongjun”) whose majority shareholder (57.5%) is ZTO’s Chairman Meisong Lai. The logo of Henan Yuncang is shown in the image below.

We also found that Zhongtong Lenglian, ZTO’s cold chain logistics business (Chinese name: 中通云冷网络科技(浙江)有限公司, “Zhongtong Yunleng Zhejiang”), is located in this area. ZTO directly owns 16% of Zhongtong Yunleng Zhejiang, while its largest shareholder (22% ownership) is Tonglu Zhongyue Enterprise Management Partnership (Limited Partnership) (Chinese name: 桐庐仲岳企业管理合伙企业(有限合伙, “Zhongyue LP”). Zhongyue LP’s controller is ZTO’s Chairman Meisong Lai, and it is 99% owned by Mingsong Lai, who we identified as the chairman’s brother.

Image 4: Henan Yuncang’s company name and gate

Image 5: Building with Zhongtong Lenglian’s name

We also found two sorting centers (image 6 below) and learned that ZTO would receive deliveries from inside of Henan Province and then sort these deliveries here. We were puzzled to see one of these sorting centers had Zhongtong Yuncang Technology’s name on the top of the building (Image 7 below). This is interesting considering ZTO discloses that it owns all the sorting centers directly.

Image 6: Front view of two sorting centers

Image 7: Rear view on one of the sorting centers

In summary, our due diligence of Henan Zhongtong Express led us to properties related to the businesses of Henan Yuncang and Zhongtong Lenglian. These companies’ largest shareholders are either majority-owned by ZTO’s Chairman Meisong Lai or Meisong Lai’s brother, Mingsong Lai. Recall, Mingsong Lai also controls Shanghai Mingyu, and we presented evidence to question the fairness of the transaction between ZTO and Shanghai Mingyu in one of the previous sections. While we were not able to pinpoint the exact place of Henan Zhongtong Express, we were informed by people in the area that this is the area in which they operate. Based on our research, we believe Henan Zhongtong Express is part of ZTO and likely used to off-load costs which should be reported at the consolidated level.

Henan Zhongtong Express’s previous shareholder, Jingwei Song, seems to be a ZTO employee based on the shareholder change record. On December 19, 2021, Henan Zhongtong Express’ shareholder, Jingwei Song, exited as a shareholder and Erhui Ma became the 95% shareholder. Jingwei Song previously owned 30% of the company.

This individual Jingwei Song is listed as the “Person in Charge” of two branch companies of Jirui Warehousing which is 100% owned by ZTO.

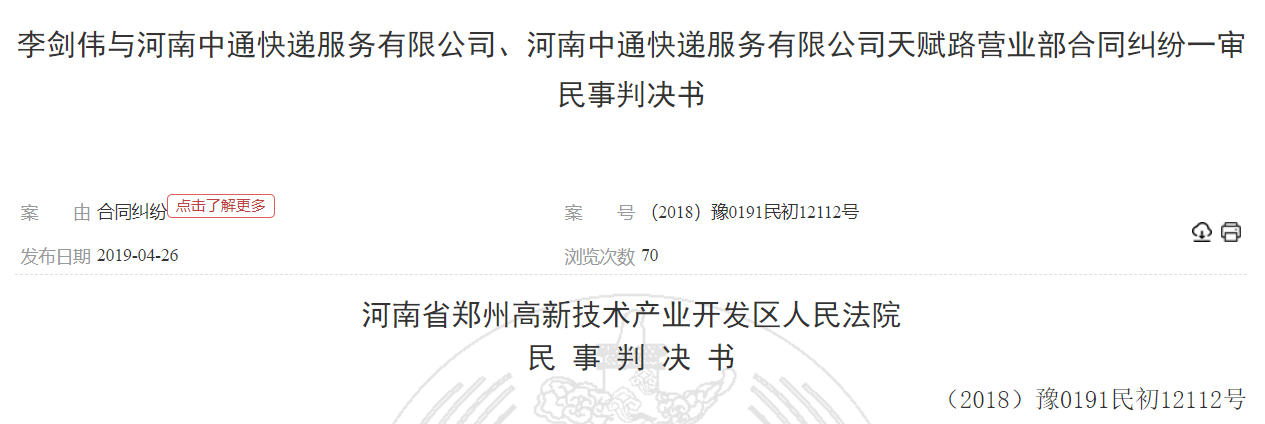

In addition, in a civil lawsuit that we found shows that Henan Zhongtong Express signed on behalf of a ZTO subsidiary.

![]()

source: wenshu.court.gov.cn

Translation on the red-underlined text:

![]()

Note, Henan Jirui Warehousing Service Co., Ltd is a 100% owned subsidiary of ZTO. The fact that Henan Zhongtong Express was able to use its name to sign a contract with other people for the delivery business shows that Henan Zhongtong Express might have been part of ZTO all along and is acting directly on ZTO’s behalf.

This also explains why Henan Zhongtong Express shares the same registration address with Jirui Warehousing and Henan Jirui, both of which are 100% owned by ZTO.

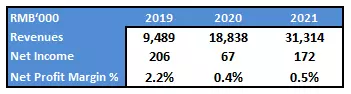

We obtained the SAIC financials of Henan Zhongtong Express from 2019 to 2021. We can see that this company’s revenues increased from RMB 9.5M to RMB 31.3M between 2019 and 2021. However, net income decreased slightly from RMB 206k in 2019 to RMB 172k in 2021. Its net profit margin is less than 1%, which is much lower than ZTO’s reported net profit margin.

On the surface, Henan Zhongtong Express is owned by two shareholders who have no affiliation to ZTO. However, the evidence we have brought forward indicates it is operating as part of ZTO. As we show in the table above, Henan Zhongtong Express has a much lower profit margin than ZTO’s reports in its consolidated financials. By avoiding direct ownership in the entity, ZTO does not need to include this lower margin business. We believe this is just one example of a company that is actually controlled by ZTO, but kept off the balance sheet to inflate the overall margins the company reports.

At Least 4 More Undisclosed Related Parties Are Potentially Used to Offload Costs

We were able to identify at least 4 more cases of undisclosed related parties.

Chengdu West ZTO Express Co., Ltd (“Chengdu West”)

According to Qichacha, Chengdu West is 100% owned by Feng Meng. Feng Meng is a 1% owner of ZTO’s VIE entity in China, ZTO Express Co., Ltd. Feng Meng is also reportedly an assistant to ZTO’s CEO and the CEO of ZTO’s cold chain division.

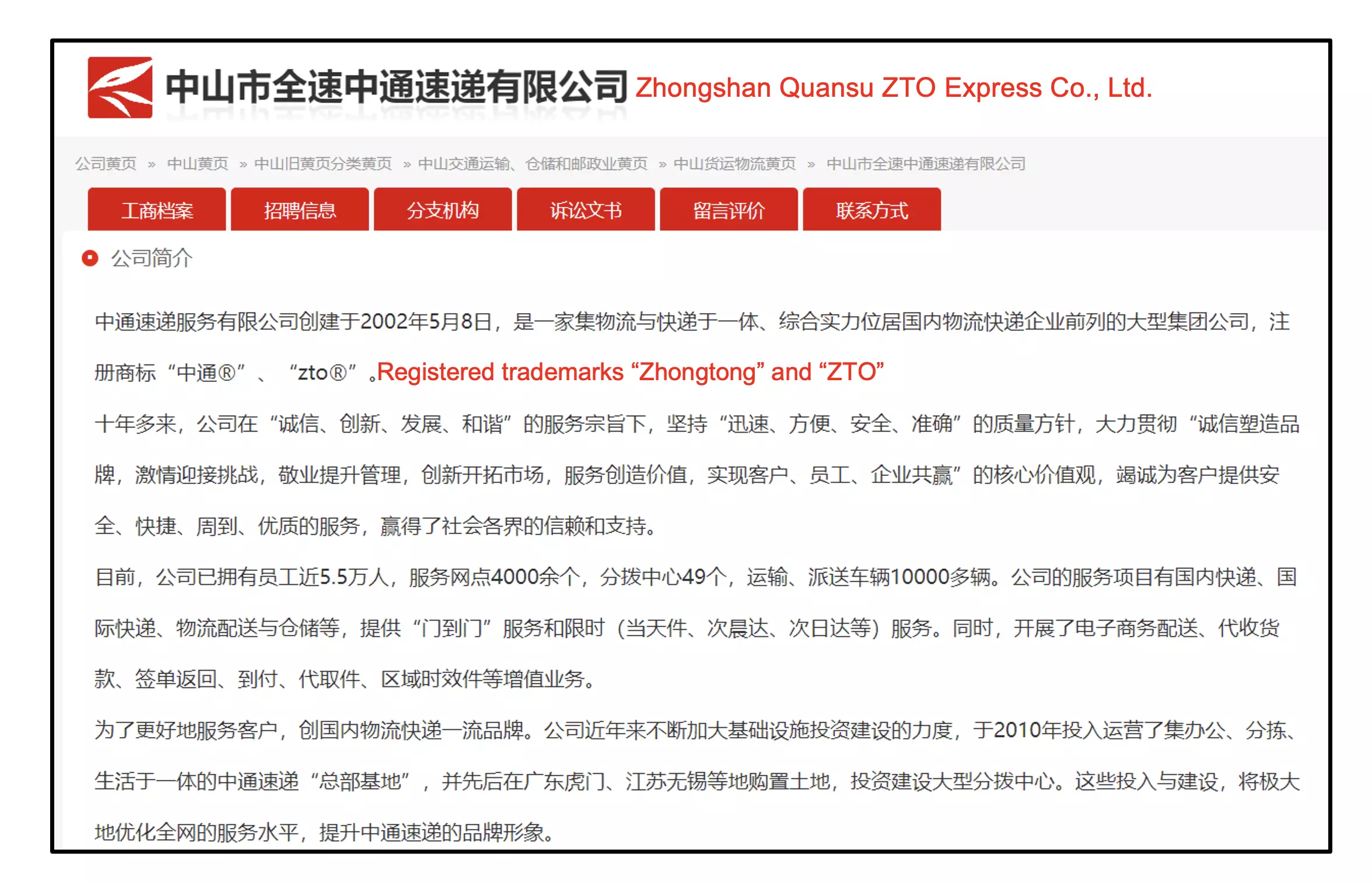

Zhongshan Quansu ZTO Express Co., Ltd. (“Zhongshan Quansu”)

According to Qichacha, two individuals, Lisheng Yang and Jie Xu, own 60% and 40% of Zhongshan Quansu, respectively. According to this website, Zhongshan Quansu lists ZTO as its trademark, indicating that it is operating as a ZTO entity. Furthermore, we can find that Lisheng Yang has been the contact agent for a couple ZTO locations. This relationship is shown below.

The below image shows Zhongshan Quansu’s company introduction. Within this description, the entity directly speaks to ZTO’s history. This makes us believe that Zhongshan Quansu is part of ZTO, rather than an independent entity.

Source: https://www.11467.com/zhongshan/co/145346.htm#gongshang

In addition, we can also find, through a third party website, that Lisheng Yang is the contact person on one network place called Zhongshan Dayong, which shows ZTO Delivery.

source: https://www.kuaidi100.com/network/net_4420__3_2.htm

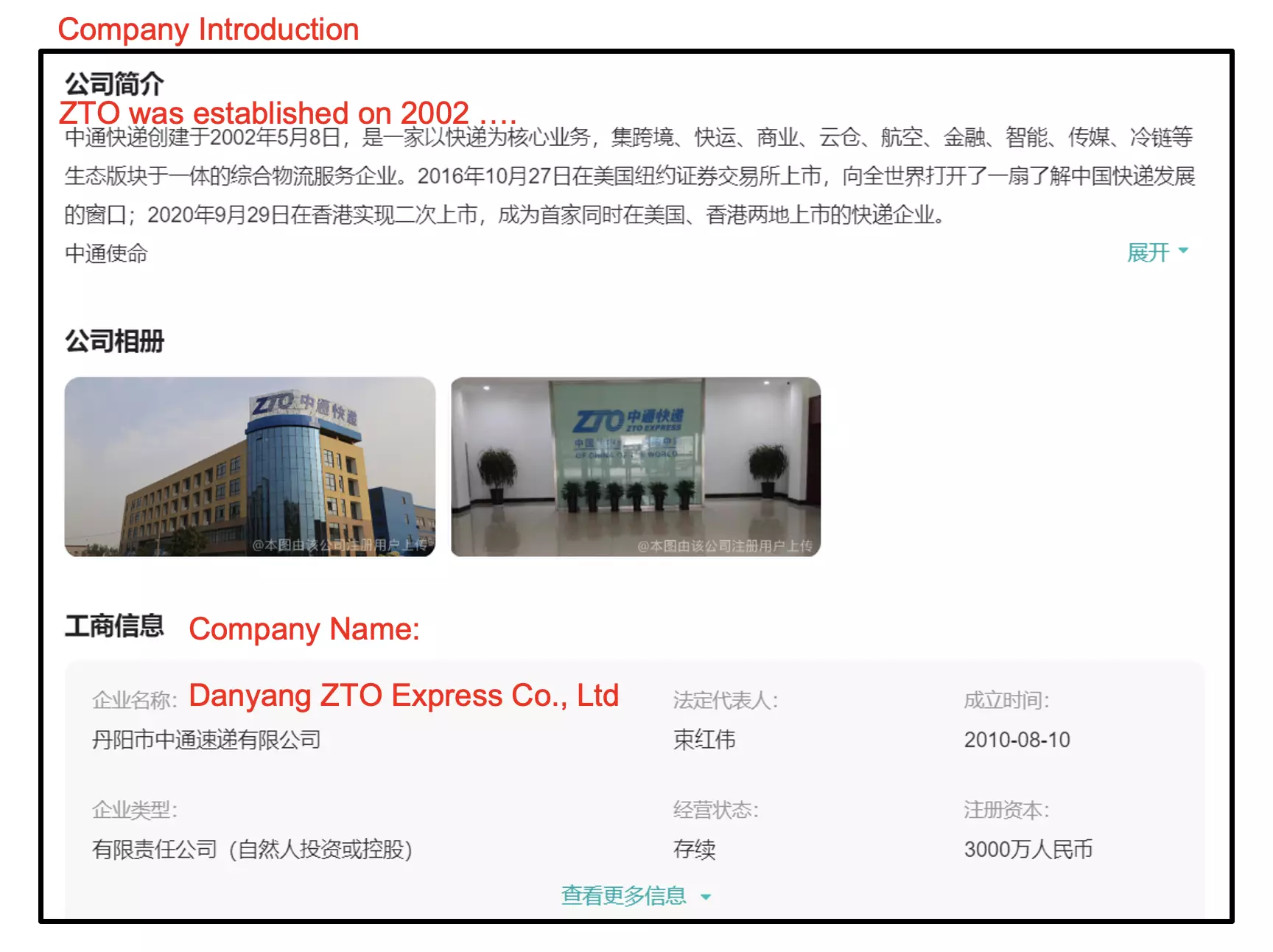

Danyang ZTO Express Co., Ltd (丹阳市中通速递有限公司)

The below image shows Zhongshan Quansu’s company introduction. This page directly introduces ZTO in way that a subsidiary would add disclosure about its parent company. This makes us believe that Zhongshan Quansu is part of ZTO, rather than an independent entity.

source: https://www.zhipin.com/gongsi/f68e4779f31c03e11nd-3ty_EFM~.html

Similarly, despite Danyang having no direct share ownership connection with ZTO, its description also shows that it is part of the ZTO group.

Yongkang ZTO Express Co., Ltd (永康市中通速递有限公司)

source: https://www.zhipin.com/gongsi/29c517f72553a8fa0n14096_EQ~~.html?ka=job-detail-company_custompage

Yongkang is another example which discloses no direct share ownership from ZTO. Meanwhile, its description on another job recruiting website zhipin describes it as part of ZTO.

We were able to find hundreds of such companies by using simply searching for the name ZTO. We suspect that many of these entities are used to offload expenses and are actually ZTO companies disguised as independent network partners.

For example, a simple search for the key word ZTO renders 3,768 reports as of the date of this report. We suspect a significant portion of them to be not only affiliated with ZTO, but also controlled by ZTO rendering them undisclosed related parties.

Valuation

There are several express delivery businesses in China which compete with ZTO. Among these businesses, S.F. Holding Co., Ltd. (002352.SZ), YTO Express Group Co., Ltd. (600233.SS), YUNDA Holding Co., Ltd. (002120.SZ), and STO Express Co., Ltd. (002468.SZ) all have meaningful market share. We believe this is a relevant set of comparable companies for investors to benchmark ZTO’s valuation against.

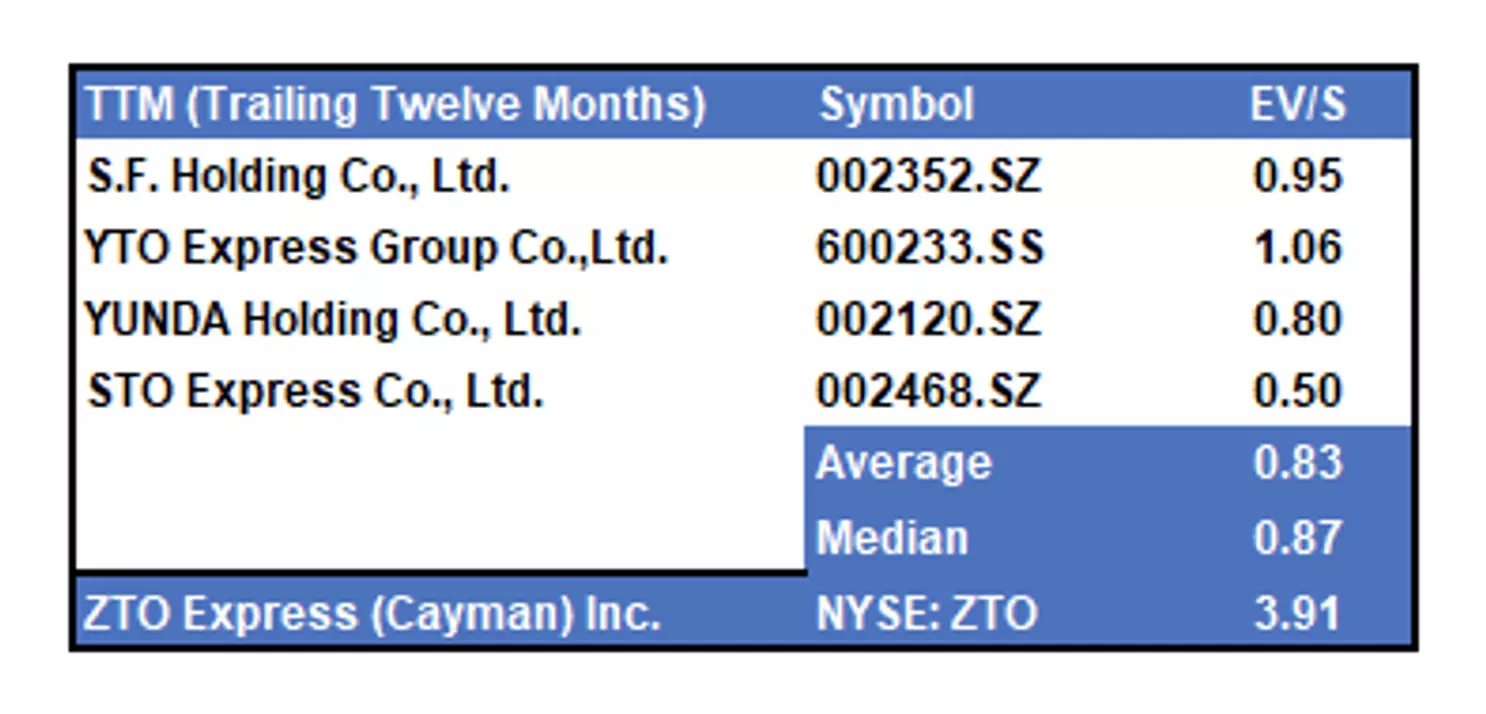

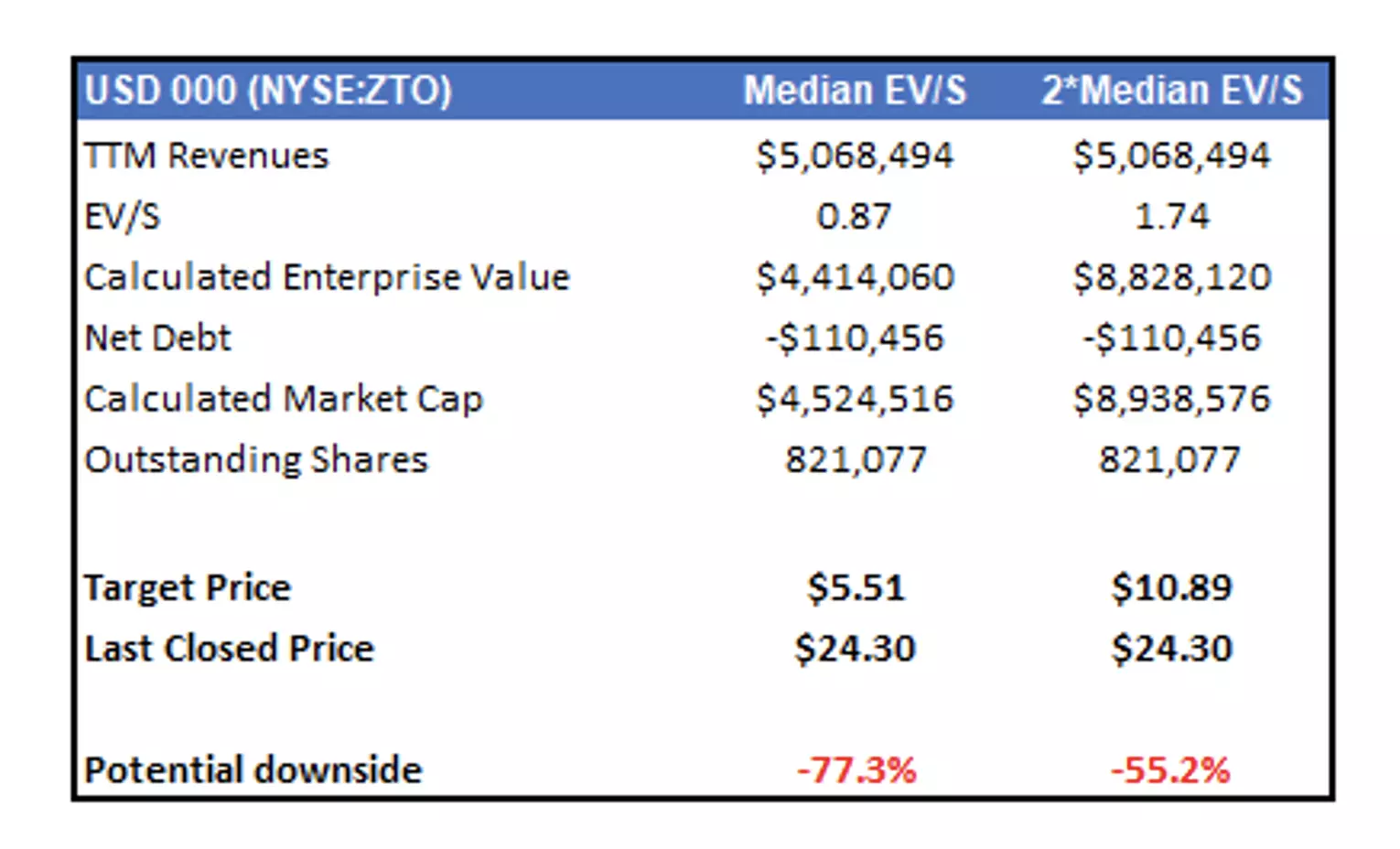

Due to our concerns over ZTO’s reported margins, we believe an enterprise value to sales (EV/S) multiple is a more appropriate metric to compare. In the summary table below, we can see that the median EV/S is 0.87x. The market seems to assign a relatively low multiple for these express delivery companies, however, ZTO stands out with a 3.9x sales multiple. We believe ZTO’s abnormally high EV/S multiple is likely grounded in its impressive margins. Considering we have significant doubts over this reported profitability, we think this multiple is unjustified.

Source: company filings, Grizzly analysis

Assuming a generous multiple of 2x EV/S across the peer group, ZTO has a target price of ~$6-$11. This calculated target price implies downside of ~55-77% from its current trading price.

Source: company filings, Grizzly analysis

Conclusion

We have laid out our case for why we believe ZTO is a dishonest company. While we believe there is some fundamental value to ZTO and can appreciate the position they have built within the express delivery market, we have significant concerns over their SEC reporting. The abundance of disclosed and undisclosed related party transactions we have presented should be concerning to investors, especially because they are not directly related to ZTO’s core business. Further, we believe we have shown an alarming number of conflicts of interest ripe for insiders to enrich themselves at shareholders’ expense.

We believe that ZTO’s SEC reported financials simply are not reliable and see at least 50% downside potential for the stock in the short to medium term.