- ESS Tech Inc. (“ESS”, NYSE: GWH) develops and produces utility-scale batteries for long-duration storage of electricity employing a “simple yet revolutionary technology: iron, salt and water”

- The market for long-duration battery storage is highly competitive and technically challenging. We argue ESS’s claims about its technology are overstated and targeted at creating investor hype for laypeople regarding the field of battery engineering.

- On August 11, 2022, ESS announced a “breakthrough partnership” under which ESS will initially supply 70 of its Energy Warehouse systems to an Australian company, Energy Storage Industries Asia Pacific (“ESI”). This breakthrough finally comes following a complete lack of revenue after over 10 years of ESS’s operations.

- The ESI partnership is the only relevant revenue generating agreement and the only major announcement ESS had since going public and seems to be the key aspect sell-side analysts are concentrating on.

- Our research uncovers ESI is a de-facto subsidiary of ESS masquerading as third-party client. ESI changed its name in February 2022 and shared a near-identical logo with ESS until this change. We found this supposedly massive strategic partner has no discernible activities outside of its work with ESS.

- We believe ESS took significant efforts to conceal its relationship with ESI before announcing their big agreement which makes us believe that management is trying to deliberately mislead investors.

- ESI announced a $70m new flagship battery factory for their alleged collaboration with ESS with a groundbreaking ceremony in July 2022. We found evidence that the factory is not being built. ESI does not reveal an address for the company. In ESI’s presentation material they show a plot of land for the factory that is not owned by ESI and no construction takes place there. The construction company seemingly tasked for building the factory does not mention it in their project list, which includes much smaller projects.

- ESI has apparently not even an office for operations, and their headquarters is a post box in a local café.

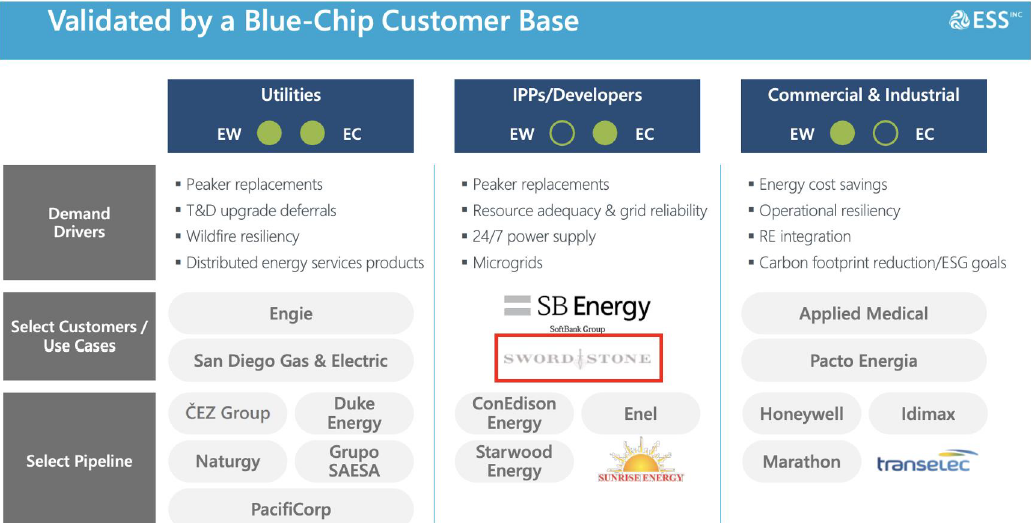

- ESS has boasted about a “blue-chip customer base”. However, all these pre-agreements were later abandoned without any re-contracting or any recognized revenue for over ten years. A history of consistent failure when working with marquee potential customers leads us to disbelieve the company’s very bold claims about its differentiated technology.

- ESS’s engineering team has a personal history of grifting from failed projects. The two founders worked many years in leading engineering roles for ClearEdge Power, Inc, a fuel cell company that declared bankruptcy in a sudden announcement. ESS’s lead engineer was formerly the responsible engineering head for the famously dysfunctional Tesla solar tiles.

- In January 2022, the most powerful insiders, founder and president Craig Evans, CEO Eric Dresselhuys, as well as CFO Moftakhar Amir started selling their shares to the market, and already netted over $1.7m in private gains.

Background

ESS Tech Inc. (“ESS”, NYSE: GWH) develops and markets iron-flow batteries to store electricity for durations of a few hours. The intended primary application is to shift the output from solar and wind electricity to the demand hours throughout a day on a grid-wide, industrial scale.

The Oregon-based company was founded in 2011 and went public at a $1.1bn valuation in October 2021 through a SPAC deal with ACON (“ACON”) S2 Acquisition Corp. Since inception, ESS’ business model of developing and selling batteries has not changed.

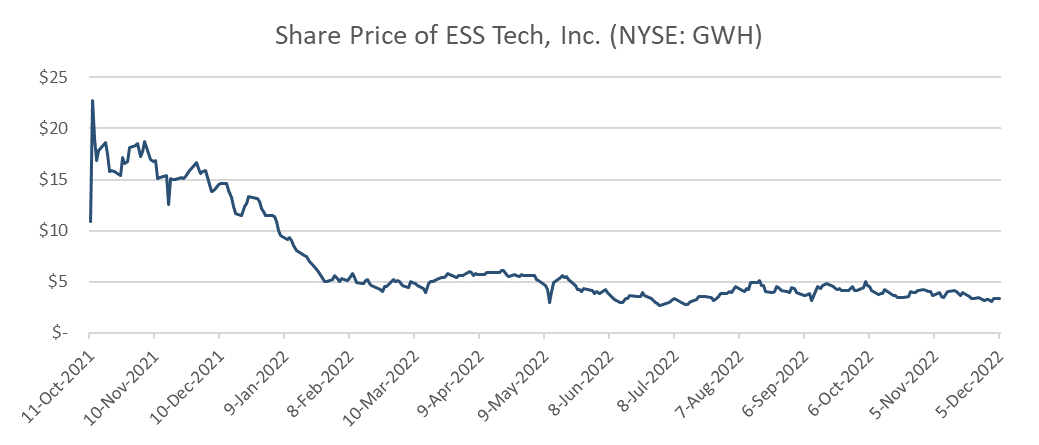

ESS’ market cap on December 6, 2022 is $439.9m with a current share price of $2.875 and average daily trading volume of about 1.3M shares.

As of December 5th, 2022

Previously, as a technology startup, ESS was already awarded a $1.73M grant in 2012 from the Department of Energy’s ARPA-E program as well as $250,000 from the Oregon Nanoscience and Microtechnologies Institute and $150,000 from Oregon BEST. ESS raised at least $46m in confirmed venture capital investment before the SPAC deal, in which ACON and the European chemical giant BASF SE invested $250m each.

ESS’ founders, Craig Evans and Dr. Julia Song, have backgrounds in engineering and chemistry. Before founding ESS, both Evans and Song worked on fuel cell projects at ClearEdge Power, Inc., a company that filed for bankruptcy in 2014.

ESS still does not report any meaningful revenue today. The company remains at a pre-production stage, despite having reported their first “commercial deployment” and “product line launch” in 2015 and 2017. ESS faced allegations of inflated revenue promises in October 2021 which continue to underpin its current valuation. ESS’ response to this scrutiny has been the announcement of a new key customer, which we claim is even more misleading and points to an even more dire situation for the company.

Market and Technology: An Ultra-Hard Engineering Problem with Lots of Competition

There is a large, global market for solutions to grid instability caused by renewable energy generation. A McKinsey study forecasts trillions of dollars of related investments in the coming years and there is a growing list of companies and technologies competing for the opportunity. ESS uses the hype by, for example, prominently citing a “$56bn TAM by 2027 at 33% CAGR” for their flow batteries in their investor presentation. (May 2021, p. 13)

Technology solutions for long-duration electricity storage in use or development include pumped hydro storage, lithium-ion batteries, sodium-sulfur batteries, flow batteries, gravity batteries, zinc-based batteries, lead batteries, heat storage, other liquid-metal batteries, air compression, and power-to-gas. In flow batteries alone many different configurations of ingredients are competing including vanadium, organic fluids, organometallic fluids and vitamin derivates.

In other words, long-duration batteries are an ultra-hard engineering problem. That is why it has been tried to solve from very different technical angles by many different research and entrepreneurial groups. Currently, the industrial-scale market is dominated by decades-old and refined technologies like large-scale hydro-pump storage, Li-Ion batteries, and lead-based batteries. The obvious reason for this is that none of the new technical approaches to solve the issue currently performs better than those older concepts.

ESS’ Theranos-Like Wunder Battery Claims

To date, almost all newly proposed solutions to long duration storage have proven uneconomical, but ESS claims it has made a list of breakthroughs. They promise a technology which addresses many of the common challenges around costs, materials, toxicity, and durability [1] [2]. Some of ESS’ claims in its marketing materials are as follows:

- “Lowest levelized cost of storage of any long-duration technology”

- “Non-toxic, non-hazardous chemistry poses no risks to installers, customers or the environment”

- “Secure, reliable supply chain with no reliance upon critical minerals”

- “Unlimited cycling and zero capacity fade”

- “Safe for use within commercial sites or in wildfire-prone regions”

- “Recyclable at end of life”

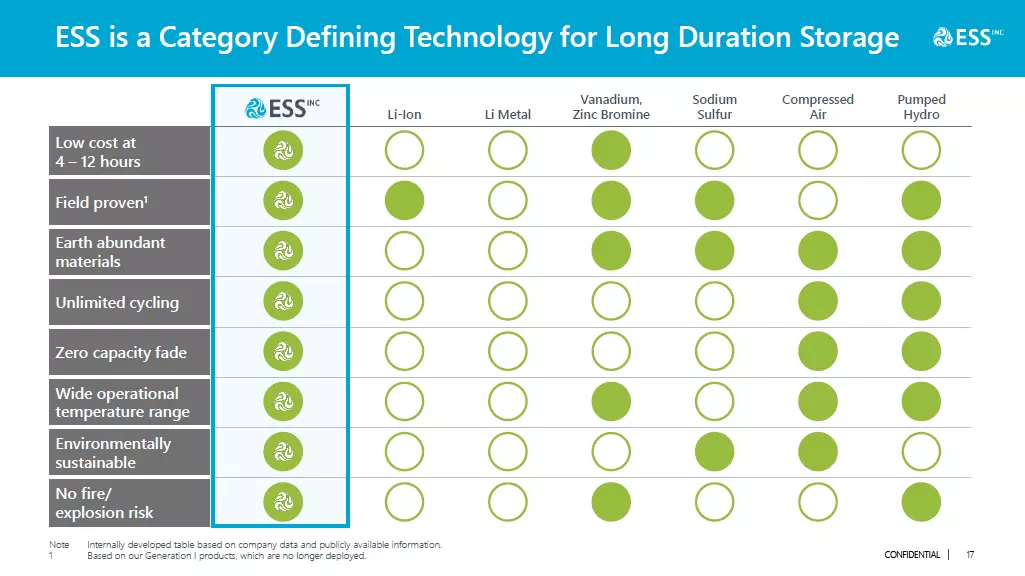

ESS present their wunder batteries as a magical jack-of-all-trades solution. The following slide summarizes well how ESS claims to have solved many ultra-hard problems of long-duration battery engineering that many competitors failed to address.

In other words, ESS makes Theranos-like claims about solving all the ultra-hard problems of long-duration battery engineering at once. With doing this, ESS sets an extremely high bar of expectations that forces ESS to back up these claims with impressive showcases of their batteries. As we show in this report, ESS does not provide any further convincing information about how they achieved their wunder battery. Most importantly, not a single third-party customer believes in their product after closer inspection behind closed doors.

The simplicity of ESS’ battery chemistry, which only uses iron, salt, and water raises doubts. Why do so many competitors see a need for more rare and expensive materials? Where is the secret sauce that make ESS succeed where so many others fail? From an engineering perspective, ESS’s presented design does not reveal anything unusual about their flow battery. In other words, the alleged secret sauce of ESS’s wunder battery is not communicated in any prominent manner to a sophisticated audience. This is a common red flag for alleged breakthroughs in engineering solutions accompanied with bold promises about the performance.

ESS refers to their registered patents. Investors must rely mostly on trust that behind these patents is the secret sauce that make the base design so much more performant than all the competitors’ development attempts. Without extensive laboratory work and practical implementations, it is impossible to reliably identify the technical problems with ESS’ design.

Flow batteries have notorious problems that are widely discussed even in laboratory setups.

- lacking efficiency,

- material corrosion,

- parasitic (on-site) load to power the pumps,

- maintenance need due to many moving parts, in particular pumps and seals

- the economies of scale for the competitors’ jack-of-all-trades lithium-ion batteries could be unbeatable, even on a long-term horizon.

As the illustration above indicates, a flow battery is a complex technical machine. We were not able to find any published comment on the batteries’ performance by EES’ commercial customers. NDA agreements about a new technologies’ performance are common and explain this lack of information. However, a direct competitor, Voltstorage GmbH, delivered their iron salt flow batteries to private customers, who described the technical issue in internet forums. Comments include that “efficiency was below 50%. (…) after two months the battery broke down completely—the stack and electrolytes had to be replaced. (…) I assume massive technical problems.” (user Bernie, Oct. 19. 2021) Another customer complaints: “Common downtimes—It seems to me they never figured out to make it work.” (user Johan, Jan. 10, 2022). “We noticed a 50% decrease in system electricity outflow in the second year.” (user ChristianB, Feb. 17, 2022). That is why, to take ESS claims about their wunder flow battery serious for sophisticated investors, ESS needs to communicate or showcase how they solved the long list of technical issues that their competitors failed to solve, or to really showcase their working battery to their commercial customers. ESS showcased their batteries to sophisticated customers and we identified a lot of signs that they failed to accomplish this.

We cannot investigate how ESS solved the problems behind closed doors. Instead, we focus on the actual product appeal to sophisticated customers that had the chance to inspect and test ESS’ battery. This serves as a very reliable proxy for the success of their technical battery design. After more than ten years of development, ESS should have established some working product or, at least, a trusting relationship to investors and clients. The market potential of a leading long-duration storage solution should make investors and early customers line up in droves if they are convinced the technology works as promised by ESS.

Caught Red-Handed: The Promising New Key Partner, “Energy Storage Industries Asia Pacific”, is Not a Real Third Party and Has No Business

ESS did not recognize any revenue from 2011 to 2021, despite multiple installations of their batteries to partners, which include blue chips and international corporations. In the chapter after this one, we elaborate on how these partners cut ties to ESS. That is why ESS currently needs to desperately signal some meaningful business success to their investors. The discontinuance of all third-party investor and client relations until 2022 are major red flags for all observing investors.

Only in 2022 Q2, ESS started to recognize $686 thousand in revenue, which they present as a “significant milestone”. ESS attributed revenue to “three Energy Warehouses™ in the second quarter” without further detail on the client. (Red flag!) In the same report, they announced the new relationship with a company called “Energy Storage Industries Asia Pacific” (“ESI”), who “has placed multiple orders for more than 70 Energy Warehouses™” and towards which “ESS began shipping in July”. “ESI plans to invest $60 million to develop a manufacturing facility to deliver an expected 400 MW of annual capacity for that region [Australia]”. In their Q3 release in November 2022, ESS announced only one other small revenue-recognized delivery of $189k.

This, at first sight, indeed looks like the milestone achievement the company has been waiting for. The new agreement was praised without question by sell-side analysts and retail investors alike. The problem with the transaction is that ESI is not actually a third party but an entity completely reliant on ESS without a real office, staff, or current business.

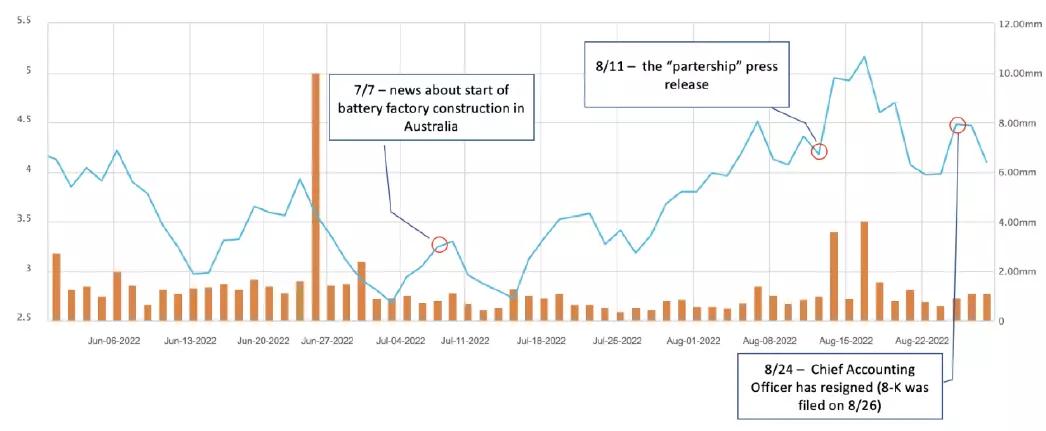

On August 11, 2022, ESS released its Q2/H1 earnings. ESS reported losses of $24m. ESS announced verbatim a “strategic partnership” to deploy long-duration energy storage in Australia and deliver an “expected 12 GWh” of iron flow batteries. In the dedicated press release, that same day, ESS further detailed a deal to initially supply ESI with 70 complete 75kW / 500kWh Energy Warehouse systems in 2022 and 2023. Concurrently, ESI will construct a manufacturing facility in Queensland, Australia equipped to conduct final assembly of ESS systems from 2024 onward. In the earnings call, CEO Eric Dresselhuys referred to the agreement as a “landmark partnership” and added:

“ESI conducted an exhaustive evaluation of technologies to address the need for long duration energy storage in Australia, and we are thrilled to be working with them as partners. This agreement provides further validation of ESS’s technology and the global market opportunity in front of us.”

ESI mirrors the wording in their LinkedIn feed by also announcing the agreement as a “strategic partnership” with ESS, who the present as the “ideal technology partner”.

In the days following the announcement, the share price jumped 25% on the “partnership” news (and ESS was up 62% since July 7, when the first news about the project in Australia has appeared – “Iron flow battery factory under construction in Queensland, Australia”).

On August 24, 2022, ESS’s Chief Accounting Officer announced his resignation from his position. The timing of his departure makes us question whether it was motivated by fear of being held responsible for the recent false and misleading announcements.

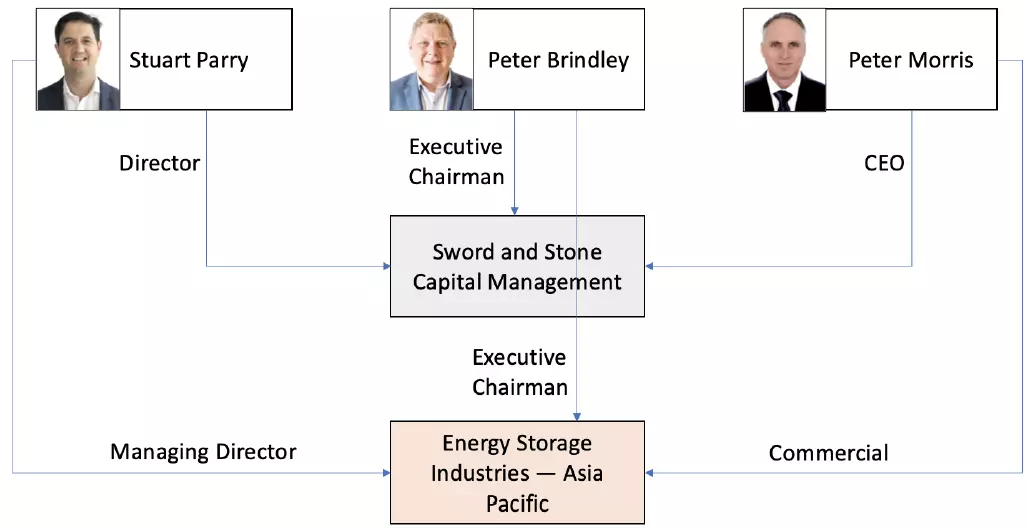

Here is the problem with this business relation: Energy Storage Industries Asia Pacific is not an unrelated third party but instead, basically, fully controlled by ESS themselves. That is why ESS’s and Dresselhuys’ announcements on the “partnership” are deliberately misleading.

ESI is embedded in a complex net of corporate structures, which includes the names “ESI ASIA PACIFIC HOLDINGS PTY LTD”, “ESS ASIA PACIFIC PROPERTIES PTY LTD”, “ESS NTH AUSTRALIAN AND PACIFIC EXPORTS PTY LTD”, and a list of Investment firms and private investors. In the following we show a clear trace how ESI is closely tied to ESS for years.

An older, undated presentation by the company Sword+Stone (S+S) Pty Ltd, on an Australian government server, describes the company ESS Asia Pacific as a joint venture between ESS, Inc. and S+S.

The company logos indicate a close relationship between ESS, Inc., and ESS Asia Pacific.

![]()

(ESS Asia Pacific’s logo used in the old presentation, and ESS, Inc.’s logo from their current website)

Australia filings [1], [2] corroborate that ESI Asia Pacific is indeed ESS Asia Pacific after a simple renaming of the business entity.

The renaming to “ESI Asia Pacific” was filed on February 2022.

To further conceal the close relation between ESS and ESI not only the name, but also the logo was changed.

![]()

(ESI’s current logo from their company website esiap.com.au)

The company domain was only registered on January 27, 2022 (WhoIs database, Wayback Machine), further indicating that ESI is not the experienced company that ESS’ management claim it to be.

Giving ESS the benefit of the doubt and assuming their joint venture partner acts independently, how meaningful is the vote of trust by S+S for ESS’ products?

In an article from April 2021, S+S founder Peter Brindley admits that S+S “is working on its first project, a large-scale battery farm in Queensland.” In other words, S+S has no business other than their joint venture with ESS. That is why the ESI executives are the same people than the S+S executives:

(sources: https://www.swordandstone.com.au, https://esiap.com.au)

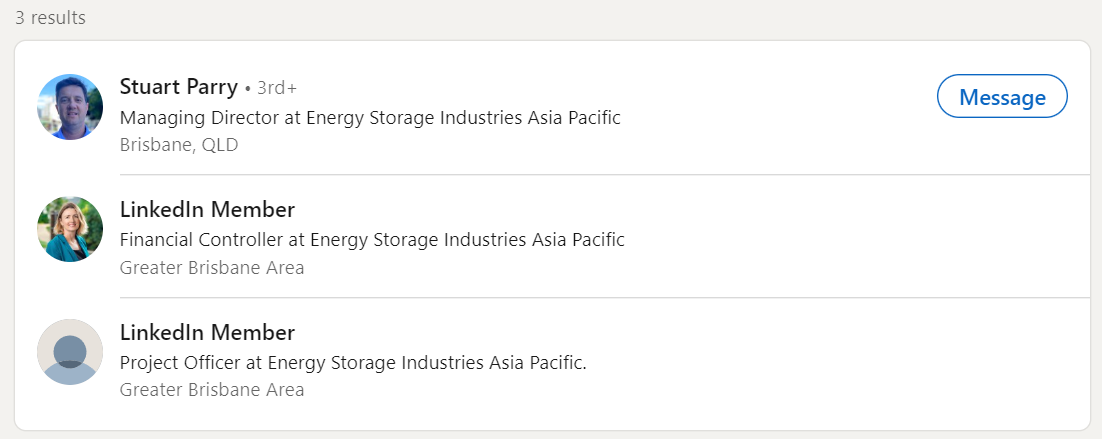

LinkedIn lists a staff of only two members for ESI, both with anonymous LinkedIn profiles, indicating that operational activity at ESI must be very low.

ESI’s employee list on LinkedIn

S+S is also already mentioned in ESS’ May 2021 presentation.

This information makes us believe that S+S was, and ESI still is just a strawman entity for ESS. ESI’s current website corroborates this impression. Under “Products & Services” in their main navigation we find a description of ESS’s batteries without mentioning ESS. The description is a direct paraphrase from ESS’s wording in their company material about the product. Most importantly, no other business offers than the manufacturing, distribution, supply, installation, and on-going maintenance of the iron-flow batteries are mentioned. ESI is the de facto Australian branch of ESS.

Why does ESS target the Australian market? PV Magazine reports the ESI project is “among plans for 13 large-scale battery systems outlined by the Queensland government in the most recent state budget” for a particular plan. “Queensland is becoming a renewable energy superpower.” In other words, the regional politics are particularly gullibly to stories about new technology in the long-duration battery sphere, and are likely willing to cut short on proper due diligence.

Does the ESI Factory Project Even Exist?

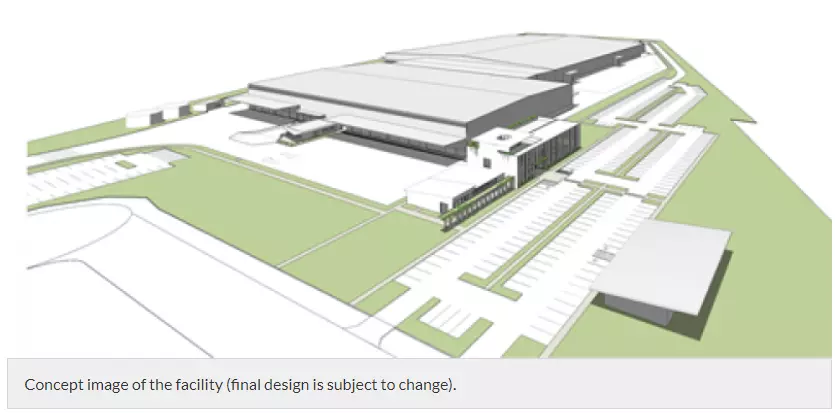

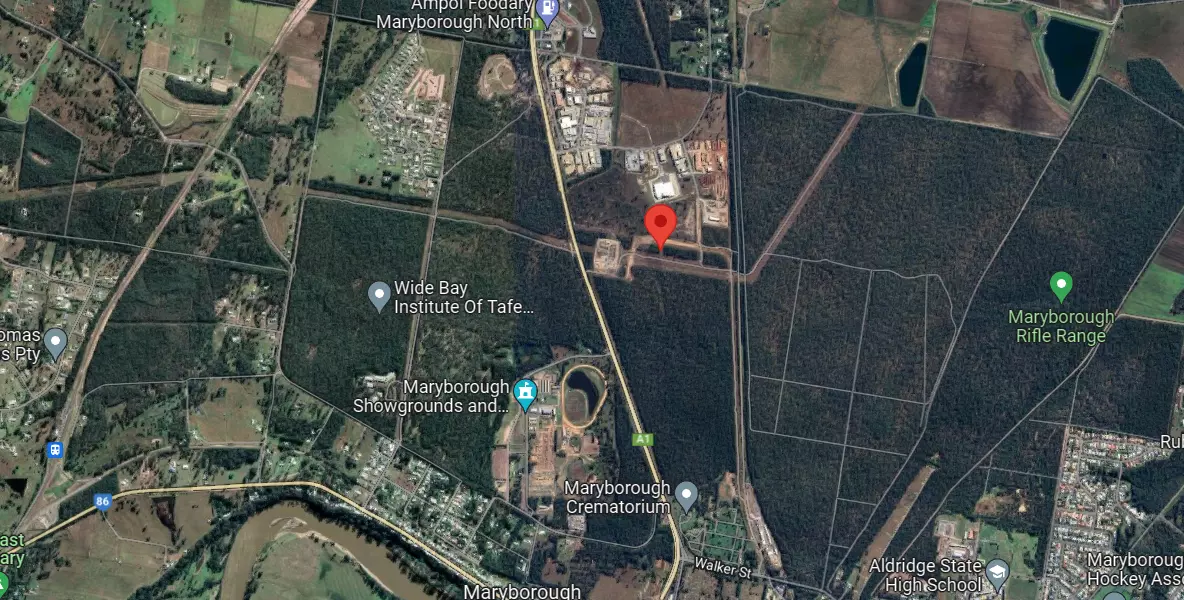

In ESI’s official July 2022 announcement of the new production facility, ESI claims the “work on our $70 million Maryborough facility officially started on Wednesday, 6 July 2022.” Neither the company announcements, nor any other company material provides an address for the facility or any other clear indication on the exact location. We were not able to find any marked location on Google maps or the regional White Pages under any version of ESI’s company name.

However, we were able to geolocate ESI’s alleged new factory in Maryborough at 25°29’53″S 152°40’13″E based on a presentation on YouTube by ESI Asia Pacific’s own YouTube channel. The Maryborough transformer station in the picture make us unambiguously conclude that this is in fact the location. The pictures by ESI below show a clear indications of construction activity in an early stage at that site. The area is seemingly being levelled. Note the construction vehicles in both shots from the video below. Google Earth provides a satellite picture for July 9, 2022, which corroborates ESI’s claim of conducting basic levelling work during this time.

(source: ESI’s own presentation on Youtube)

(source: Google Earth/Google Maps)

(source: Google Maps)

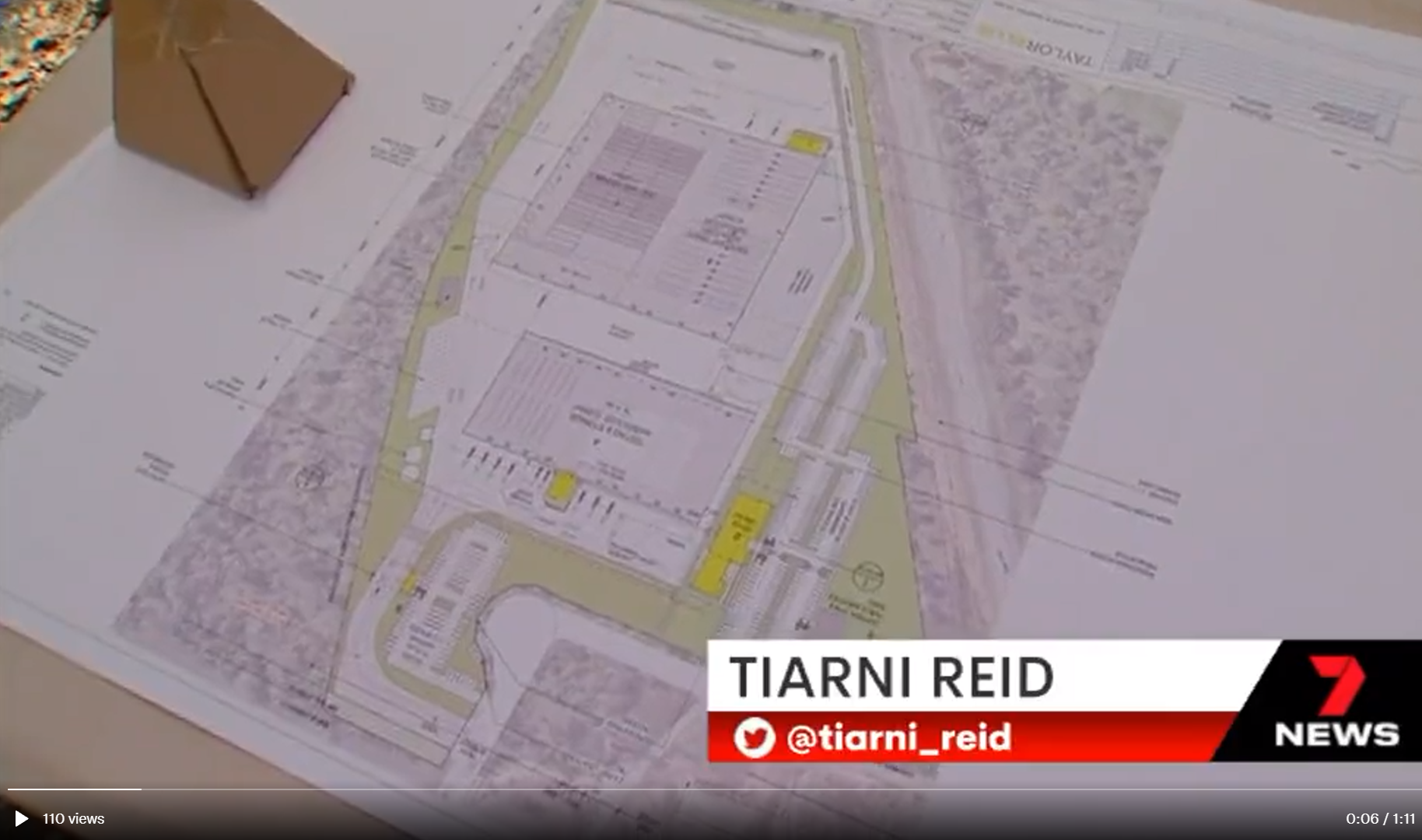

A screenshot from a News report on the project reveals a blurry construction plan.

We fitted the construction plan into the actual land to unambiguously locate the exact spot of the factory.

The following animation shows public satellite images from mid-June to December 5 in 5-day succession from surveillance satellites. The images reveal that barely any work was conducted on the site until now.

The latest available high-resolution image is dated from November 1st, and also corroborates a lack of construction activity on the site.

Site on November 1st, via Airbus SPOT satellite imagery

Source: https://search.titlesqld.com.au/product-search

Another screenshot from a News Channel’s report on the project shows a construction sign by the regional construction company SGQ.

SGQ proudly lists their construction projects on their website. The list includes much smaller projects than a $70 million cutting-edge battery factory, which is currently not shown in the list. The absence of such a large project makes us conclude that the sign is not one from the ESI construction site but a mock-up for the news report.

Another very important question for the facility’s realization is the source of the funding. Investing $70 million usually requires some sophisticated investors. ESI does not publish any information in these investors or any government participation in concrete terms. We were not able to identify the main source of funding for ESI’s expensive high-risk venture.

ESI Doesn’t Even Have a Proper Office Address

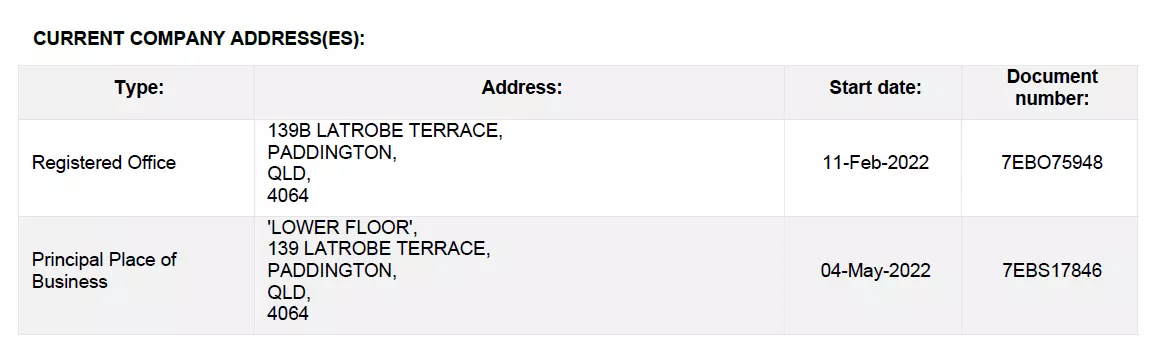

A company that currently builds a $70 million facility for “up to 500 highly skilled employees” to build “20 per cent of Australia’s renewable energy storage needs” would certainly have a somewhat useable office headquarter, right? According to regulatory filings the address is “139 Latrobe Terrace, Paddington, QLD, 4064.

Source: ESI company filings summary via kyckr.com

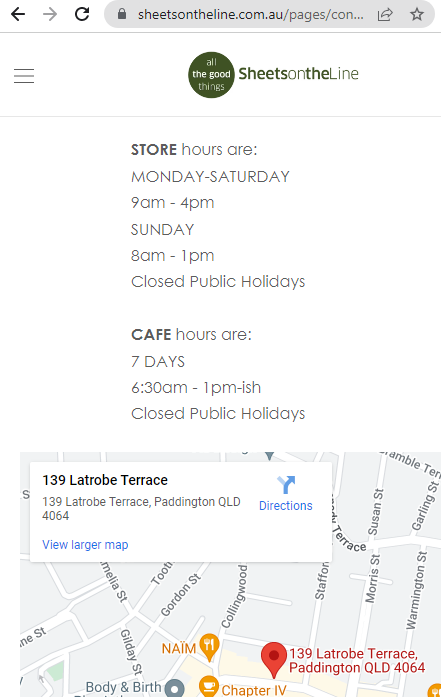

In reality, the address is just a small café with a homewares and linen store.

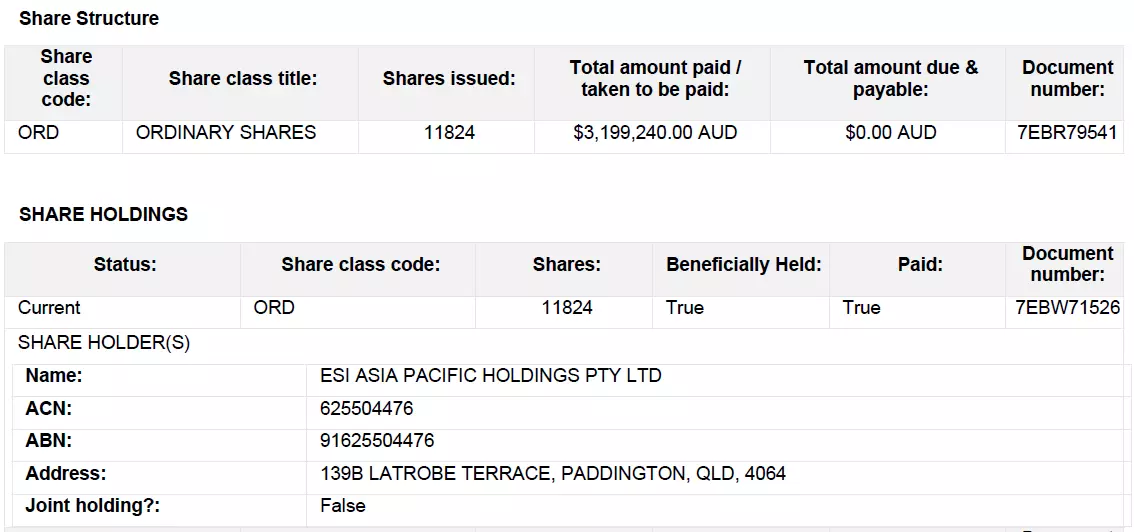

Legally, ESI ASIA PACIFIC PTY LTD is owned by ESI ASIA PACIFIC HOLDINGS PTY LTD, which—of course—is also headquartered in the café shop.

Source: ESI company filings summary via kyckr.com

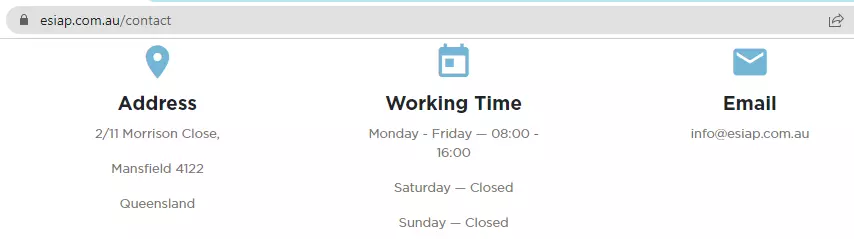

However, on their website, ESI reveals yet another company address. This one is in an actual industrial area.

The latest online photographs from May 2022 indicate other companies using office space in the property, and no prominent signs of ESI can be found. As the pictures indicate, the U.S. doors and gates company, The Chamberlain Group LLC, with their Australian subsidy Grifco, seem to be the building’s main user.

(retrieved: November 11, 2022)

Fully consistent with the lack of construction activity and missing employees count on LinkedIn, our investigation into the alleged office spaces of the company clearly corroborates that there is actually not much operational work conducted at ESI.

ESI Investors Leave

ESI is a private company but is held by a group of shareholders. However, a regulatory filing from July 21, 2022 reveals that the following investors sold all of their ESI shares back to the company, formally “ESI ASIA PACIFIC HOLDINGS PTY LTD”. The following investors left ESI:

- GRANDKI INVESTMENTS PTY LTD sold all its ESI shares (833)

- PROJECT LOUNGE AUSTRALIA PTY LTD sold all its ESI shares (541)

- BATTERY INVESTMENT GROUP PTY LTD sold all its ESI shares (208)

- A.C.N. 643 264 386 PTY LTD sold all its ESI shares (192)

- A.C.N. 625 185 033 PTY. LTD. sold all its ESI shares (178)

- BRINDLEY INVESTMENTS PTY LTD sold all its ESI shares (48)

- TE & P JONES PTY LTD sold all its ESI shares (25)

- MR JOSEPH ANTHONY CATALNO & MRS IRENE MURADA sold all their ESI shares (25)

- MR KEVIN JAMES sold all his ESI shares (8)

We interpret this leaving of investors as a severe vote of mistrust into ESI.

We believe the misleading reframing of the initial joint venture between ESS and S+S into a deal with an allegedly unrelated third-party is clearly misleading to lull investors into vain hopes.

In summary, the ESI deal is not the crucial savior project that ESS presented. Our revelations rather make us believe that ESI’s big industrial endeavor is ill-planned and will likely never come to fruition. In this case, ESS is left without any industrial partner or client, as we show in the next chapter.

Big Former Customers Who All Walked Away for Some Reason

Of the six different ESS battery installations deployed from 2015 to 2020 to customers, five were later abandoned. An earlier short report by Bonitas Research already pointed this out in October 2021. We refer to this publication for further details on the list below.

ESS’ May 2021 presentation, p. 45

- Stone Edge Farms is a winery, famous for using its own microgrid for electricity. According to ESS, the ESS battery was installed and working in May 2016. However, ESS’ battery is neither mentioned in a November 2017 extensive journalist reportage about the grid, nor on Stone Edge Farms own presentation website. Competitor’s batteries from Tesla, Sony, Simpliphi and Redflow are mentioned.

- The U.S. Army Corps of Engineers deployed an ESS battery in 2016, according to ESS. The US government contractor database reveals that the contract amount was $0. ESS gave the battery as a present without any follow-up payment or order.

- The University of California San Diego (“UCSD”) deployed an ESS battery in 2017. However, UCSD mentions current energy storage systems in their reporting. An ESS battery is not mentioned in recent reporting or by a full website search.

- The Camp Pendleton U.S. Military Base received a delivery from ESS through the subcontractor CleanSpark, Inc. for $53,000, as the US government contractor database and filings reveal. Neither CleanSpark, nor the military had any additional business with ESS after these reports in 2018.

- The San Diego Gas & Electric Company opted for a vanadium battery by ESS’ competitor Sumitomo Electric Industries, Ltd.

- The multinational chemical giant BASF is an ESS investor since 2017. Despite being an investor, BASF has yet to pay ESS any revenues for its product and decided to forego both Series-C rounds.

- InoBat and Naturgy had partner relations to ESS but ultimately decided to opt for competitors’ batteries, namely lithium-ion batteries, and flow batteries from E22.

We interpret this clear rejection of any continuing business or association with ESS as a clear sign of distrust in ESS’ technology and business.

We believe that severe technical issues, or performance problems became apparent to clients who tested the battery. Why else would they all shy away?

ESS’ Executives Learned How to Raise Money on Inflated Technical Promises in Previous Large and Failed Projects

ESS’ executives seemed to have learned in their previous roles how to successfully raise capital for ultimately failing technical developments and delay disseminating bad information to shareholders. We believe they applied their lessons learned for massive personal gain with ESS.

ESS’ founders, Craig Evans and Dr. Julia Song, worked on fuel cell projects at ClearEdge Power, Inc. (“ClearEdge”) for several years before starting ESS in 2011. Song worked for over seven years, leaving as a Vice President of R&D. Evans worked at ClearEdge for almost five years, leaving as a Director of Design & Product Development.

ClearEdge’s playbook is very similar to that of ESS. ClearEdge’s stated goal was to build a fuel cell for residential and small commercial applications that provides heat and electric power. The Oregon-based company raised more than $161 million in venture capital and grants. ClearEdge was founded in 2006 and acquired another fuel cell developer, United Technology Corporation, in 2012 to switch from their own failed product to a competitor’s development. However, in 2014, ClearEdge rapidly filed for bankruptcy, which “caught many employees by surprise”, laying off 268 of them. The company explained this measure by a “cash shortfall” and a “significant customer” hadn’t made the final buying decision.

ESS’ responsible head of engineering since January 2022, senior vice president Dr. Benjamin Heng also has a prominent background of a major product fraud. From 2014 to 2015 Heng was a senior vice president for SolarCity and was head of Solar Product Engineering and Pilot Operations for Tesla, Inc. from 2016 to 2017. During this time, in October 2016, Tesla CEO Elon Musk made a big announcement when presenting Tesla’s allegedly innovative solar roof glass tiles. This project is famously lacking massively behind Musk’s promises and deeply ill-designed with an ongoing filed class action lawsuit by customers. In other words, Heng has proven that he can oversee a dysfunctional product without complaining, resigning or alerting the press or customers.

We believe that Evans and Song, in their lead engineering roles, certainly knew about the lacking economically viability or serious technical problems of ClearEdge’s fuel cells. But they also learned how investment money can be raised in the sphere of energy engineering. Like ESS, ClearEdge was held afloat for years based on engineers’ promises of a technical devices’ inflated performance or omitted disclosure of serious flaws. The new head of engineering, Heng, supports the suspicion because he has proven himself already with letting the bosses run with flawed products on the biggest stage possible.

New Projects: Prototype-Like Tests or Unclear Funding Sources

In recent weeks, ESS added some further agreements and projects to the list following the similar pattern of the failed former projects: either the agreements are about tiny test deployments of ESS batteries or investments by ESS themselves without the source of funding explained.

On August 25, 2022, ESS announced to install one Energy Warehouse™ System at Pennsylvania Microgrid without much further details on the deal. This project is, again, a tiny prototype-like test.

On September 20, 2022, ESS and the Sacramento Municipal Utility District announce an agreement to deploy up to 200 MW / 2 GWh of long-duration energy storage solutions. As part of this multi-year agreement, ESS intends to set up facilities for battery system assembly, operations and maintenance support and project delivery in Sacramento, creating local, high-paying jobs. This means, ESS does all the investment with unexplained funding source and ESS carries all the project risk.

On November 4, 2022, ESS announced to deliver a 75 kW / 500kWh Energy Warehouse™ system to Burbank Water and Power. This project is also a tiny prototype-like test.

On November 10, 2022, ESS announced deployment of a “battery system for a solar and storage microgrid” with undisclosed capacity. In other words, this is very likely another single-unit trial run.

The Financials: Big Promises and a SPAC Merger to Raise Retail Money

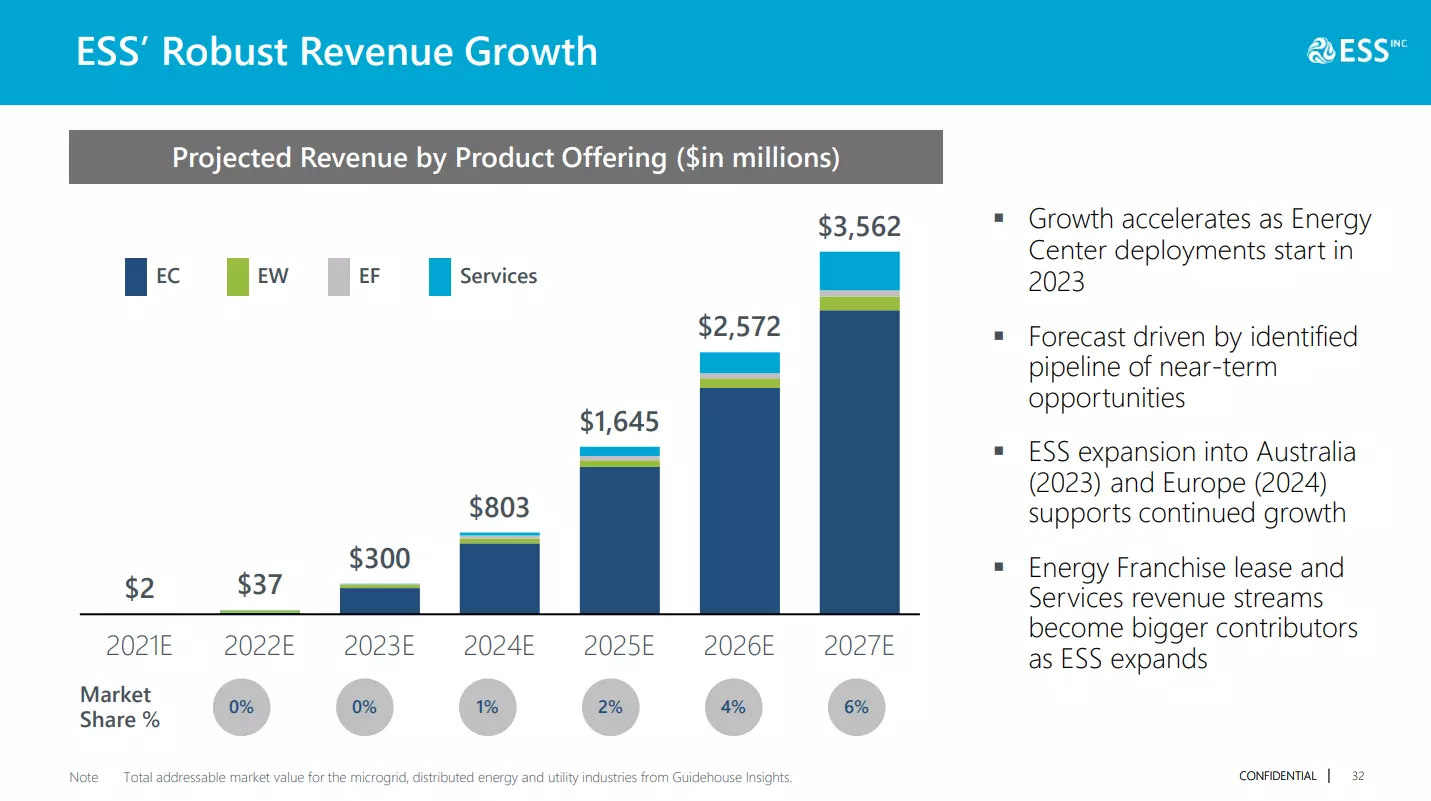

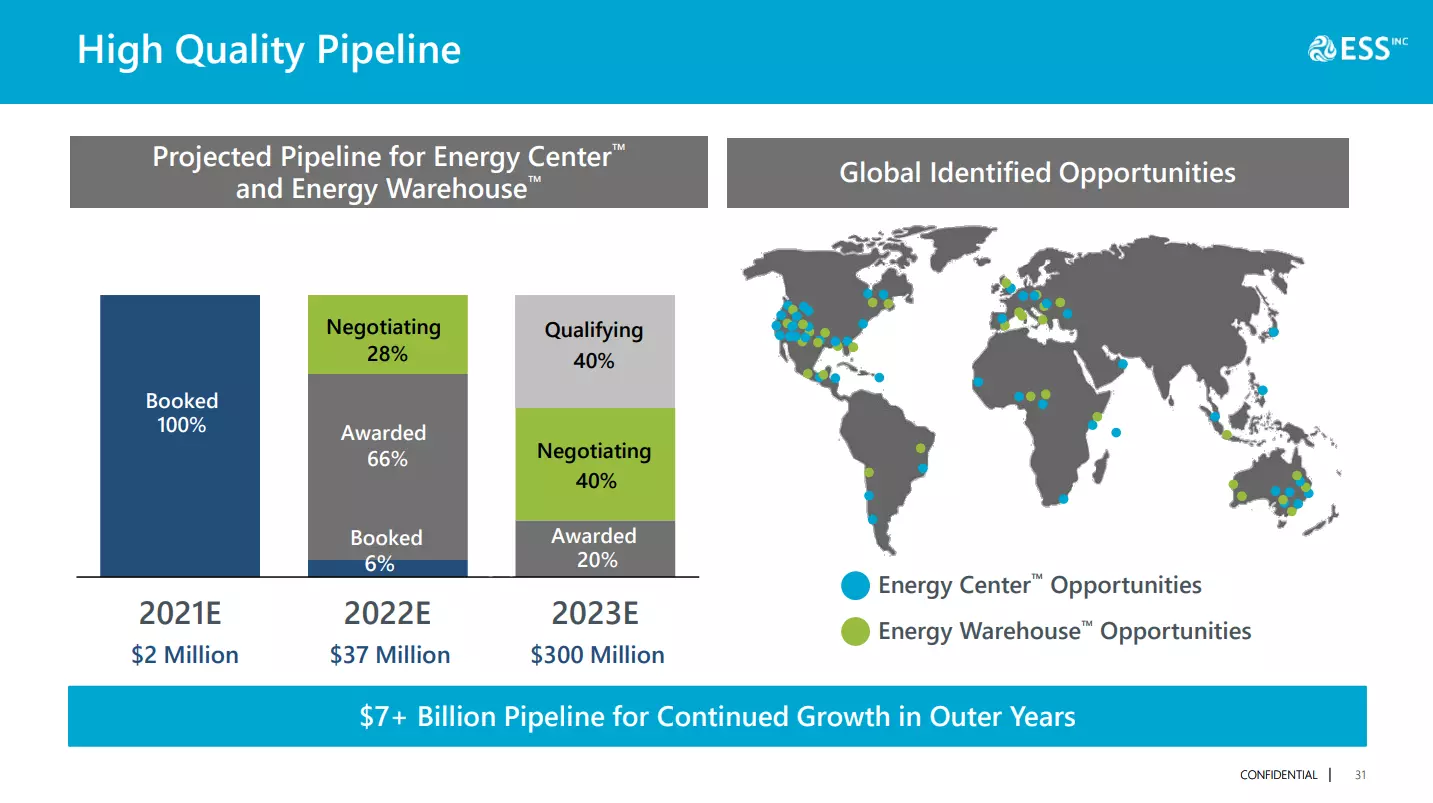

ESS’ aggressively promised growth based on non-existing customer demand. We see these baseless projections as an abuse of the SPAC merger process which allows companies to make projections they would not be allowed to make if they went through a traditional IPO process. These are some slides from the May 2021 presentation:

ESS’ past economic performance is summarized as follows.

| 2018 | 2019 | 2020 | 2021 | 2022 Q1-Q3 | |

| Revenue | $0 | $0 | $0 | $0 | $878k |

| Net income/loss | NA | -$11.5M | -$30.4M | -$477.1M | -$52.9M |

| Operating Expenses | NA | $9.9M | $17.4M | $60.6M | $75.0M |

| Common Stock Equity | NA | $15.6M | -$27.9M | $205.Mm | $158.2M |

| R&D expenses | NA | $6.7M | $12.9M | $30.3M | $49.2M |

From a valuation perspective, ESS’ business is only worth more than nothing if their battery design is economically viable. However, despite 11 years of trying to convince customers, we have not seen any reliable signal that make us believe ESS’ wunder battery performs as promised.

In 2022 ESS’ Executives Started to Sell Their Shares

Until January 2022, no insider of ESS sold any shares to the open market. However, since then president and founder Craig Evans, CEO Eric Dresselhuys, and CFO Amir Moftakhar sold shares in several tranches amounting to $1.7M in private gains.

| INSIDER | RELATION | LAST DATE | TRANS. | OWNER TYPE | SHARES TRADED | PRICE | SHARES HELD |

| EVANS CRAIG E | President and Founder | 11/21/2022 | Sell | Indirect | 6,350 | $3.82 | 2,397,089 |

| EVANS CRAIG E | President and Founder | 11/21/2022 | Sell | Direct | 58,217 | $3.52 | 5,583,400 |

| DRESSELHUYS ERIC P. | CEO | 11/21/2022 | Sell | Direct | 14,339 | $3.82 | 1,367,520 |

| EVANS CRAIG E | President and Founder | 11/18/2022 | Sell | Indirect | 50,000 | $3.93 | 2,403,439 |

| MOFTAKHAR AMIR | CFO | 10/19/2022 | Sell | Direct | 8,386 | $3.48 | 558,850 |

| MOFTAKHAR AMIR | CFO | 10/17/2022 | Sell | Direct | 63,205 | $4.03 | 583,956 |

| MOFTAKHAR AMIR | CFO | 10/17/2022 | Sell | Direct | 16,720 | $3.72 | 567,236 |

| DRESSELHUYS ERIC P. | CEO | 10/17/2022 | Sell | Direct | 110,082 | $3.72 | 1,381,859 |

| EVANS CRAIG E | President and Founder | 10/17/2022 | Sell | Indirect | 12,628 | $3.72 | 2,453,439 |

| EVANS CRAIG E | President and Founder | 10/17/2022 | Sell | Direct | 16,340 | $3.72 | 5,625,277 |

| DRESSELHUYS ERIC P. | CEO | 01/24/2022 | Sell | Direct | 59,642 | $6.05 | 869,170 |

| EVANS CRAIG E | President and Founder | 01/24/2022 | Sell | Direct | 1,342 | $6.05 | 5,373,083 |

All ESS insider sales. Data by Nasdaq.com.

Conclusion

We believe we have caught ESS in an outright lie. ESS’s largest partner and key growth driver for the next few years is a related party without any relevant own business activity. The deal which remains to play out, is therefore, of questionable economic essence.

Our view is ESS management has consciously misled investors and sell-side analysts with their “breakthrough partnership” announcement to keep the growth story alive. We believe the company will continue to fail to generate meaningful revenue because its technology is not as cutting edge as claimed in an industry of increasing technological sophistication and competition. We caution investors against trusting the outrageous forecasts tied to dishonest partnership announcements. We conclude that ESS is dishonest, un-investible, and we believe the stock is a terminal zero.

APPENDIX

ESS’ Stock and Shareholders

ESS currently has 152.9M shares outstanding. The following table summarizes the shareholders with holdings of more than 1 million shares.

| Institution | Shares held

(% of total) |

Description* |

| SoftBank Group Corporation | 36.0M (23.5%) | Aggressively optimistic tech investment fund |

| Breakthrough Energy, LLC. | 18.6M (12.2%) | Green tech investment fund |

| Pangaea Venture Funds III LP | 12.6M (8.2%) | Material engineering investment fund |

| FMR LLC (Fidelity) | 11.4M (7.5%) | Diversified funds, brokerage accounts |

| Cycle Capital Management III Inc | 9.7M (6.3%) | Venture capital investment fund |

| BASF Venture Capital GmbH | 9.2M (6.0%) | Venture fund of chemicals giant BASF SE |

| Craig Evans | 8.1M (5.3%) | Founder |

| ACON S2 Sponsor LLC | 6.1M (4.0%) | SPAC vehicle |

| BlackRock Inc | 4.6M (3.0%) | Diversified funds (incl. passively managed) |

| The Vanguard Group Inc | 3.3M (2.2%) | Diversified funds (incl. passively managed) |

| Invesco Ltd | 3.3M (2.2%) | Diversified funds (incl. passively managed) |

| Julia Song | 2.3M (1.5%) | Founder |

| Legal & General Group PLC | 2.1M (1.4%) | Diversified funds (incl. passively managed) |

| KIM LLC | 1.7M (1.1%) | Diversified funds |

| Eric Dresselhuys | 1.4M (0.9%) | CEO |

| State Street Corporation | 1.3M (0.9%) | Diversified funds (incl. passively managed) |

| Geode Capital Management LLC | 1.2M (0.8%) | Diversified funds (incl. passively managed) |

| First Trust Advisors LLC | 1.0M (0.6%) | Diversified funds |

| Smaller investment funds, other insiders and retail | 18.0M (11.8%) |

(source: regulatory filings)

*Grizzly’s ad-hoc industry assessment based on company’s service description and past trading activities in ESS’ stock.