Read below or open PDF version

- Partners Group Holding AG (“Partners Group”, “PGHN”) is a Swiss-listed alternative asset manager with approximately US$184.9 billion in assets under management. Partners Group is known for pioneering evergreen funds, which contribute almost half the company’s revenues.

- We dug through the capital structure, underlying holdings, and national filings of Partner’s Group’s biggest evergreen funds, most prominently its Master Fund. We compared our findings to industry peers and consulted with industry experts, former Partners Group employees, and finance professors who expressed grave concern about our findings. One professor commented after reviewing our analysis carefully that the situation is “worse than Wirecard”.

- We found numerous instances where the Master Fund’s valuations did not reconcile with the reality of the underlying businesses. We estimate close to 40% of the evergreen funds’ investments might be severely mismarked.

- The Master Fund’s largest Asia-Pacific holding reports 50 million fewer shares of its key investment to the SEC than it reports to the Hong Kong Companies Registry.

- Partners Group’s Master Fund marked up a Russian pharmaceutical equity investment during the same reporting window in which the Russian state seized the asset by Putin’s decree.

- Often the timing of the investment, the financial performance of the operating companies, and valuation marks seem not to square up. These include a 176.9% markup on a Swedish data-center operator whose revenue fell 18% and operating losses widened 42% over the markup period; an 857.8% common equity markup on a Portuguese biocontrol group whose revenue grew 2.9% year-over-year; and a position whose common equity jumped 383% in 26 days.

- When we were able to back out valuation multiples relatively reliably, we arrived at the conclusion that Partners Group applies multiples for its own valuation that are far in excess of what industry comparisons suggest. Through financial gymnastics, Partners Group arrives at effective valuations that are sometimes more than twice as much as our independently commissioned valuation experts suggested.

- Across the Master Fund’s direct-debt book, reported principal balances moved in ways inconsistent with standard accounting. In many instances, principal value and fair value metrices moved not only by hundreds of percent and in different directions, which is very untypical for a senior loan.

- Partners Group tells investors its private-credit software exposure is “less than half the industry average.” We estimate its actual exposure in the available sample at 32%, which is above the industry average and more than heavily-criticized peers such as Blue Owl Capital.

- Importantly, we do not see the same irregular valuation patterns we saw in Partners Group in the filings of its largest US and European peers. We see attention to Partners Group’s evergreen funds and their valuation marks as a severe risk to the company’s fund-raising ability and long-term financial health.

Content

Introduction: Partners Group a Pioneer in Evergreen Funds

Partners Group is one of Europe’s largest alternative asset managers, with approximately $185 billion in assets under management (“AUM”) as of year-end 2025. The company and its management are often praised for being innovators in the industry. They are credited with pioneering evergreen investment vehicles for private investments as well as bringing access to Private Equity and Private Credit investments to retail investors. An Evergreen fund is exactly what the name implies: It is a permanent investment vehicle as opposed to traditional private equity investment mandates that have a limited time horizon.

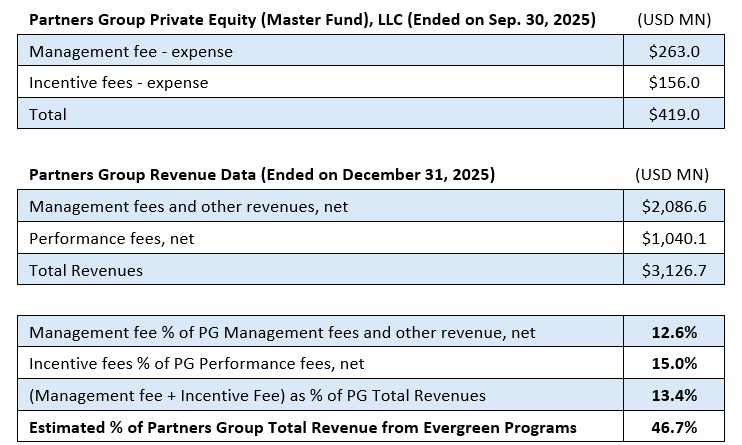

Partners Group’s most prominent evergreen fund is its Partners Group Private Equity (Master Fund), LLC (“Master Fund”), with about $15.9 billion Net Assets Value (“NAV”) of the total $56 billion in the evergreen programs. The disclosure below shows how meaningful the financial contribution from the Master Fund alone was and implies that Evergreen Programs’ contribution is almost half of Partners Group’s revenue.

Note: calculation on currency exchange is mostly relied on current rate

We also estimated the financial contribution from both the Master Fund and another one of the biggest evergreen funds in Europe, based on their 2024 financials. This calculation implies that Partners Group generated approximately 45% of its total revenue from its evergreen funds in 2024.

We also note that evergreen funds have been a meaningful contributor to overall fundraising momentum.

Source: Partners Group annual reports

The evergreen programs are important to Partners Group, but reported performance seems to be lacking. The Master Fund underperformed its benchmark in the past 5 years as of March 31, 2025, according to its own disclosure.

Source: Master Fund as of March 31, 2025

The annualized return of the benchmark MSCI World TR was 16.1% in the 5-year window, compared to the Master Fund’s 13.6% during the same period.

Financial media also reported on the lackluster performance at Partners Group’s largest European evergreen fund.

Partners Group made an extraordinary announcement at the beginning of April, underscoring stability and decent fundraising efforts. Only shortly after, the company warned in this Financial Times article that “it will impose limits on investor withdrawals if redemptions rise sharply”.

“Partners Group declined to disclose detailed investment flows for its evergreen funds but said net flows in the firm’s flagship US evergreen private equity fund were broadly similar to late 2025.

The fund entered net redemptions for the first time last year and withdrawal requests reached $750mn in the third quarter, double the same period the year before.”

In an overall precarious Private Equity/Private Credit environment, investors want to be assured about the reliability of the valuations of their investments. This is where we believe Partners Group fails by far the worst amongst all peers.

A Significant Portion of the Equity Portfolio Seems Severely Mismarked

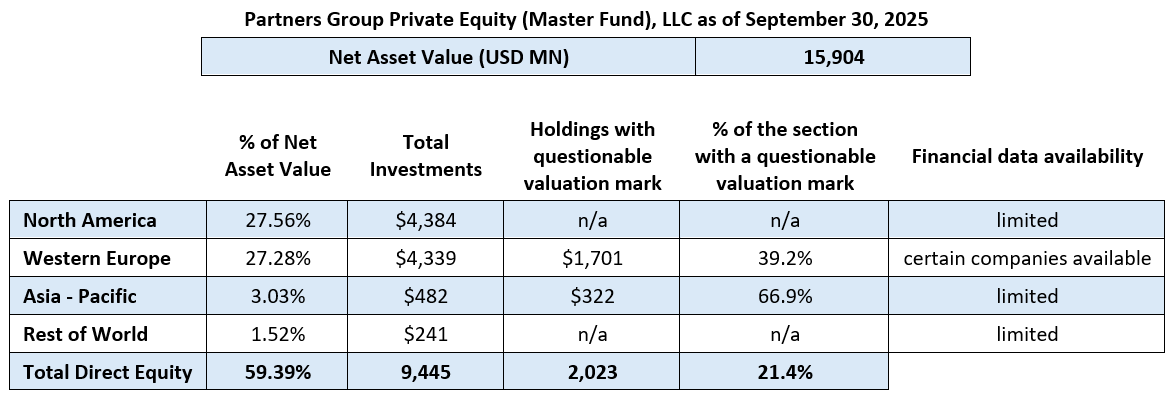

The Master Fund’s Direct Equity portfolio ($9.45 billion) represents 59.39% of the Fund’s NAV as of September 31, 2025. Within that, $4.34 billion is in Western Europe. There are also holdings that were categorized into regions such as Asia–Pacific and the Rest of World.

The reality is that there is little transparency about the detailed financial performance of privately held US-based companies and we usually cannot make a serious assessment of the valuation marks without financial data to cross-check. We do, however, call valuation marks into question in extraordinary circumstances, such as an asset seizure, even when we do not have financials available. We note that the regions where we do have data available show that close to 40% of the valuation marks seem highly questionable.

We compared our findings to the funds of the largest industry peers in Europe as well as in the USA. We did not find irregular patterns that we comparable to our findings in Partners Group. We consulted with over a dozen experts on our findings. A forensic compliance expert commented:

“[J]udging by the figures, there is going to be a scandal with this fund and its portfolio companies worse than the one with Wirecard. Wirecard had a fraud of 4 billion dollars in inflated assets. But here, there could be fraud involving tens of billions in inflated assets of the portfolio companies and the fund itself.

Even from just a surface-level look, there is accounting fraud, investment fraud, and fraud involving loans and offshores.”

A $322 Million Holding Where the Majority of Shares is Missing

Partners Group’s flagship US evergreen fund holds a Hong Kong position, Zenith Longitude Limited, at a fair value of $322.0 million as of September 30, 2025. That single position represents about 67% of the fund’s entire $481.6 million Asia-Pacific portfolio in Direct Equity.

The Master Fund’s September 30, 2025, filing reports the fund as holding 26,838,037 shares of Zenith Longitude Limited. We cross-checked the Hong Kong registry, and the reported share numbers are off by a meaningful amount.

Zenith Longitude Limited’s 2025 annual return filed with the Hong Kong Companies Registry records the Master Fund as holding 76,288,162 shares.

Zenith Longitude’s earlier Hong Kong filings tell a consistent story. Between 2021 and 2022, the Master Fund’s recorded shareholding rose from 149,884,481 to 149,888,161 shares. In 2023, following an overall share-count reduction at Zenith Longitude, the Master Fund’s recorded shareholding dropped to 76,288,162, and remained at that level through Zenith Longitude’s 2024 and 2025 annual returns.

The Master Fund’s disclosed 26,838,037 shares are not the consequence of any corporate action we can identify in Zenith Longitude’s publicly filed documents. This share count has stayed stable in both 2024 and 2025 according to Partners Group’s disclosure, which simply does not match the disclosure in the Hong Kong registry.

We checked for subsidiaries or off-shore entities that could hold the shares, and looked for other possible explanations. We consulted with Hong Kond lawyers and confirmed that any of the possible reasons for the mismatch would ordinarily appear in Partners Group’s disclosures to investors.

It is also noteworthy that we did not find any records in China or Hong Kong regarding Zenith Longitude actually making any investments in operating companies. Given the sums involved, we expected at least some media coverage in China or Hong Kong.

Equity Holdings Are Marked at Fair Values That Apparently Do Not Reconcile With Financial Performance

Partners Group’s Master Fund holds most of its investments in Western Europe through Luxembourg SPVs that file annual accounts in Luxembourg’s Registre de Commerce et des Sociétés.

After reviewing thousands of pages of documents and reports, we found that close to 40% of the Master Fund’s portfolio in Western Europe had disparities between Partners Group’s reported fair value and the underlying operating company’s financial statements that were apparently unjustifiable.

Most of the Luxembourg holdings below are capitalized as a thin layer of common equity sitting on top of a much larger preferred-equity layer (a “thin-common, thick-preferred” structure). The common-equity slice absorbs all enterprise-value appreciation above the preferred accrual level, which is why Partners Group’s headline common-equity returns sometimes exceed 50,000%.

Those headline common-equity figures are not the comparable we chose. We chose to compare the combined common plus preferred mark to the reported fair value. We show both figures where available. We frame the critique around the combined mark, not the common-equity slice alone.

We sorted the cases into several categories. The private equity and private credit industries are notorious for a lack of transparency and there might be possible explanations for some of the cases we point out, like a restructuring that was not communicated to investors or the media. After our consultation with over a dozen experts on private equity and credit valuations we concluded that possible explanations would either be farfetched or would at the very least involve major disclosure violations by Partners Group.

Valuation Mark Does Not Reconcile with Reported Financials and Public and Private Transaction Data

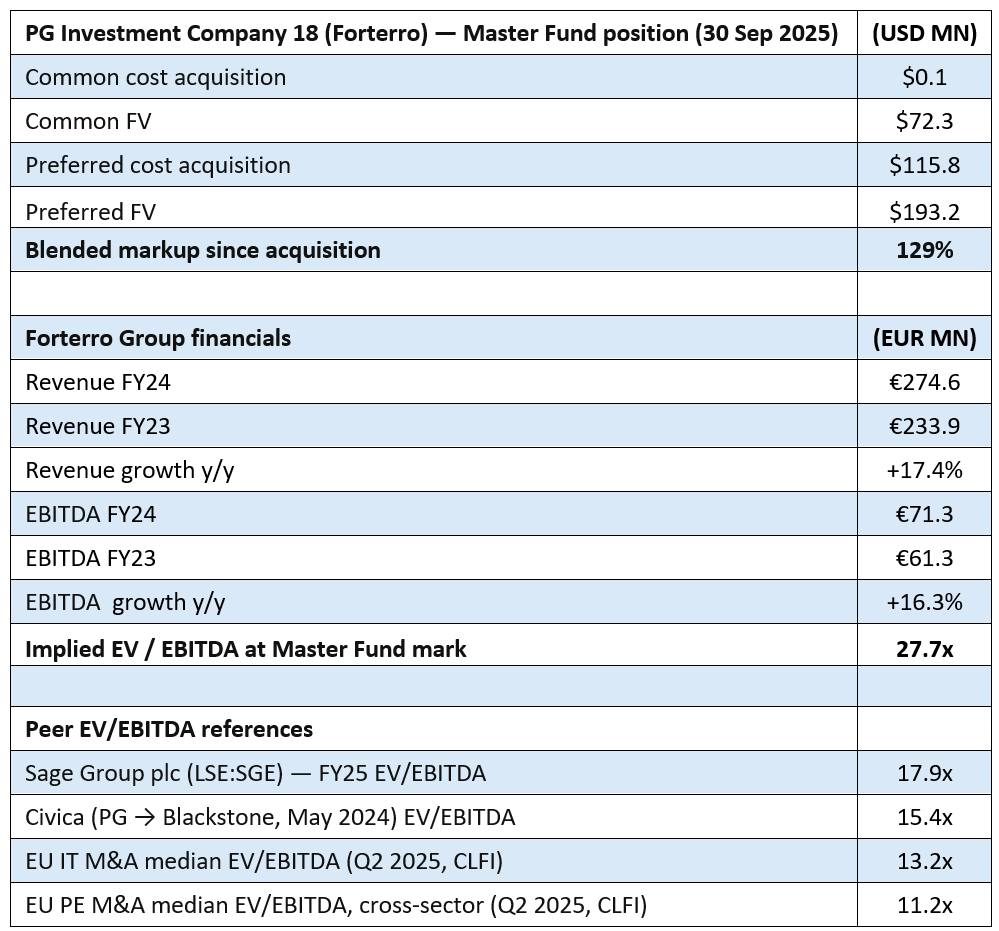

PG Investment Company 18 (Forterro, Software Company) 129% Blended Markup and Valued at 27x EV/EBITDA

As of September 30, 2025, the Master Fund held 113.85M preferred shares of PG Investment Company 18 S.à.r.l. (“PG 18” thereafter), accounting for about 15.4% of its total preferred shares. The fund also held 12.65M ordinary shares of PG 18, accounting for 13.0% of its ordinary shares. Although we don’t have the exact percentage of Master Fund’s ownership in PG 18, we used 15% as a working assumption to illustrate the process.

Based on Forterro’s 2024 annual report, it generated EUR 274.6M in revenues in 2024, as compared to EUR 233.9M in 2023. The company also reported EBITDA of EUR 71.3M in 2024, as compared to EUR 61.3M in 2023. In addition, the company recorded EUR 50.2M in Cash and cash equivalents, and a total of EUR 515.9M in Debt as of December 31, 2024.

With the Master Fund’s valuation mark of $265.5M for both preferred and common shares, the implied equity value of Forterro is about EUR 1.5 billion after considering the currency exchange. The implied EV/EBITDA based on Forterro’s 2024 financials is about 27.7.

This multiple is higher than the European comparable company, for example, Sage Group (LSE:SGE), as well as Partners Group’s previous deal and third-party M&A transaction data.

Sage Group plc trades at about 17.9 times EV/EBITDA based on the FY 2025 financials ended on September 30, 2025. Its revenue grew 7.8% y-o-y in FY25 and its EBITDA grew 11.6% y-o-y. Even though Sage Group’s revenue and EBITDA grew at a lower pace than Forterro, it was trading at a lower EV/EBITDA multiple than the implied multiple of Forterro. If Forterro were valued at EV/EBITDA of 17.9, we calculate the Master Fund’s implied preferred and common equity values in PG 18 would be 46.3% lower than its mark as of September 30, 2025.

In 2023, it was reported that Partners Group sold a software company called Civica to Blackstone for about £2 billion, and that company produced EBITDA of £130 million. That transaction was completed in the second half of 2024. This deal valued Civica at EV/EBITDA of about 15.4, according to the report. If investors were to apply 15.4 EV/EBITDA to Forterro, Master Fund’s implied preferred and common equity values in PG 18 would be 58.1% lower than its mark as of September 30, 2025.

In addition, according to the third-party report published in September 2025, private equity buyers paid a median EV/EBITDA multiple of 11.2 in Europe, as compared to 12.8x for private equity-led deals in the United States. Valuation in IT was higher and the median EV/EBITDA (2025) was 13.2x across both regions. If investors were to apply 13.2 EV/EBITDA to Forterro, the implied equity value would be 68.5% lower than what Master Fund marked its investment in PG 18.

In all of these scenarios, investors would find that the Master Fund’s valuation mark on its preferred and common equity investments in PG 18 was overstated, and the estimated market value might be 36.3% to 68.5% lower than its current mark.

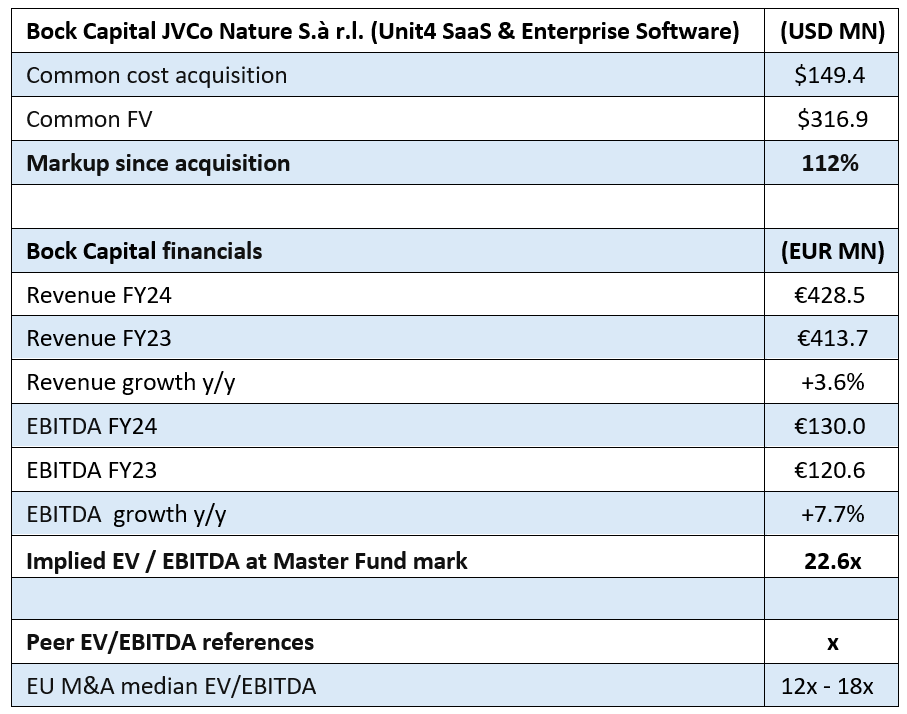

Bock Capital JVCo Nature S.à r.l. (Unit4 SaaS & Enterprise Software) — 112% Mark Up on 22x EV/EBITDA multiple on a SaaS Business with Unimpressive Growth

As of September 30, 2025, the Master Fund held 12.59 billion shares of the Luxembourg company named Bock Capital JVCo Nature S.à r.l. (“Bock Capital JVCo I” thereafter) as a common equity position, which accounts for about 12.9% of its total outstanding shares. Bock Capital JVCo I essentially holds an enterprise software company called Unit4 Group, which is based in the Netherlands. Master Fund’s investment in Bock Capital JVCo I appreciated 112.1% since July 2021, with its initial cost of $149.4 million increasing to its fair value of $316.9 million.

Based on Unit4’s consolidated annual report of 2024, the company generated EUR 428.5M revenues in 2024, an 3.6% increase from EUR 413.7M in 2023. The company also reported EUR 130.0M in EBITDA in 2024, which is a 7.7% increase from EUR 120.6M in 2023. In addition, the company recorded EUR 993.2M of Borrowings and EUR 139.2M of Cash and cash equivalents as of December 31, 2024.

With the Master Fund’s valuation mark of $316.9M from Bock Capital JVCo I, the implied equity value of Unit4 is about EUR 2.1 billion. The implied EV/EBITDA based on Unit4’s 2024 financials is about 22.6. This multiple is once again higher than the European comparable company, as well as the third-party M&A transaction data. Other data points suggest that a EV/EBITDA valuation multiple in the 12 to 18 range seems more realistic, which implies that Partners Group should mark down this account by 29 to 58%.

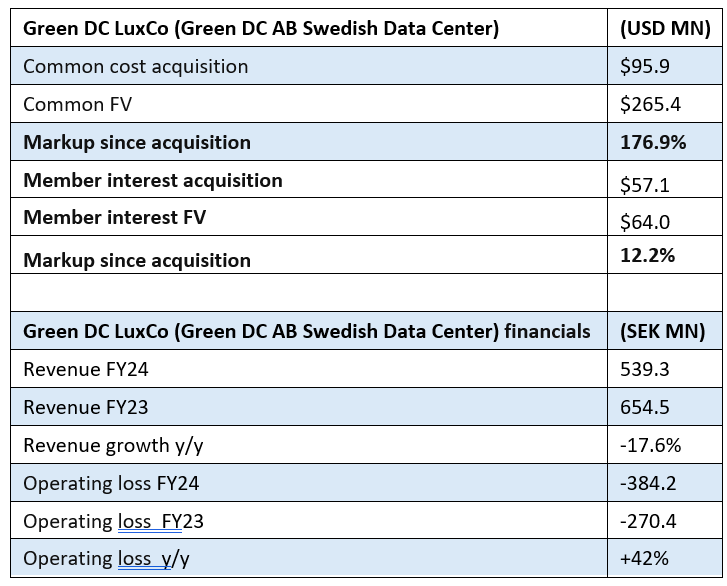

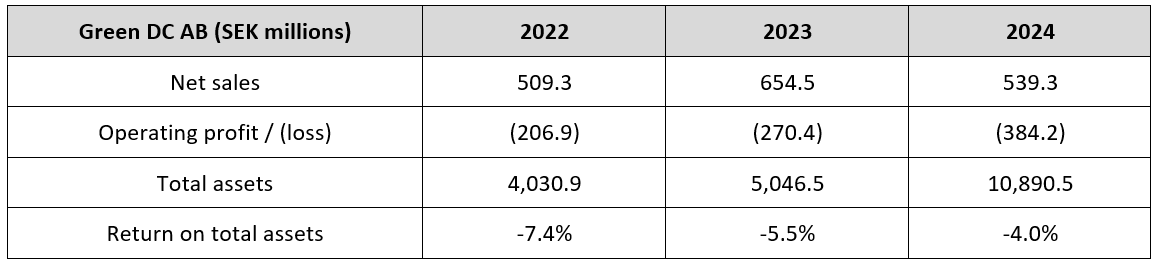

Green DC LuxCo (Green DC AB Swedish Data Center) +177% Mark While Revenue Fell 18%

The Master Fund’s Green DC LuxCo common equity position is marked up 176.9% since January 2022, with a cost of $95.9M to the fair value of $265.4M as of September 30, 2025. The combined common equity and member interest marked up 115.5% during this period.

Green DC AB’s filed Swedish accounts show the underlying business going the other direction:

The company’s revenue was SEK 539.3M in 2024, a decrease of 17.6 y-o-y from SEK 654.5M in 2023. In the same period, the operating loss widened from SEK 270.4M in 2023 to SEK 384.2M in 2024, an increase of 42% y-o-y. The company attributes part of the revenue decline to the decommission of older facilities and the high Tier 3 facilities conversion.

Partners Group marked the equity up 177% and the combined common equity and member interest up 115.5% over a period in which the operating business lost more money and generated less revenue.

Root JVCo (Rovensa Group) – 72% Blended Markup on 3% Revenue Growth

Rovensa Group’s filed accounts showed that its revenue were €728.5 million for the year ended June 30, 2025, as compared to €708.3 million for the prior year, an increase of 2.9%. Its EBITDA was €140 million, which is a 28% increase year-over-year. Rovensa operates in the biocontrol, biopesticides and biostimulants subsegment, a higher-growth category than traditional crop protection.

The Master Fund’s combined common equity, preferred equity, and member-interest positions in Rovensa were marked up 71.8%, from $81.6 million to the fair value of $140.2 million. The headline 857.8% common equity figure reflects the SPV capital structure which emphasizes a thin common equity layer and a thicker preferred equity layer.

Ciddan S.à r.l. – The Fund Marks Up Its Investment in the Same Period When The Russian Government Seized the Asset

The Master Fund held both preferred equity and common equity in the company called Ciddan S.à r.l. (“Ciddan”). Ciddan, through certain entities, indirectly owns the Russian pharmaceutical manufacturer JSC Nizhpharm. On April 4, 2025, the Russian government transferred 100% of JSC Nizhpharm, a leading Russian pharmaceutical manufacturer indirectly owned by Partners Group’s flagship US evergreen fund, to state-managed Pharmirus LLC by Presidential decree.

Over the same reporting window, which is the six months from March 31, 2025, through September 30, 2025, Partners Group marked its combined position of both preferred and common equity in Ciddan up 12.0%, from $77.1 million to $86.4 million. The mark-up happened during the period when the seizure occurred, not before it or after it.

Source: Master Fund filings for March 31, 2025 and September 30, 2025.

Partners Group has not publicly disclosed how it values a Luxembourg holding company whose primary underlying operating asset has been transferred out of its control by a sovereign state. In our view, Partners Group should have written this position down substantially between March 31 and September 30, 2025. Other companies whose assets were taken by the Russian government did write-offs. Instead, Partners Group wrote it up.

Just two months before Putin transferred Nizhpharm’s assets to a little-known Russian company, the odds of recovering value from a seized Russian asset looked vanishingly small. Of the 30 companies whose assets had been partially or fully seized, only three had recovered any portion of their investment, recouping about $630 million while still absorbing roughly $2.7 billion in losses, according to the Kyiv School of Economics.

In April 2025, the same month when Nidda Lynx lost control over Nizhpharm, FT reported a Kremlin-organized campaign to take over Western-owned businesses in Russia. Since 2022, the Russian state has systematically seized Western corporate assets, with the total value reportedly approaching $50 billion by the summer of 2025, Reuters reports. For further details, see “Chain of Ownership Nizhpharm” in the Appendix.

We also checked the fair value of both the common and preferred equity in the past years, and we noticed that the fair value of the common equity in Ciddan did come down from $84.6M on September 30, 2023, to $56.1M on September 30, 2025. It is unclear to us if the Master Fund had already written off the JSC Nizhpharm investment way before this decree incident happened in April 2025. We also saw that Ciddan had other investments in operating companies about which we have no further information.

During this period, when Ciddan’s common equity fair value went down as much as 33.7% from September 2023 to September 2025, its preferred equity fair value actually increased by 11%. This kind of opposite movement in the value of common equity and preferred equity should be viewed as an additional red flag and deserves more explanation from the company.

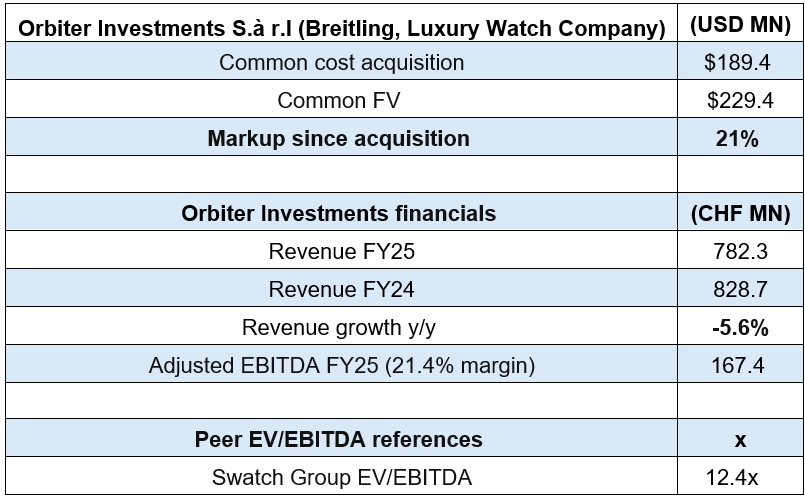

Orbiter Investments S.à r.l (Breitling, Luxury Watch Company) – Valuation Mark Not Consistent with Media Report and Rating Agency

Orbiter Investments S.à.r.l. owns the majority of Breitling, a luxury watch company that is headquartered in Switzerland. Partners Group initially invested in Breitling in 2021 and later bought a majority of the company from another private equity firm CVC, according to this Financial Times article. According to the article, the 2023 transaction between CVC and Partners Group on Breitling was based on a valuation of $4.5 billion, and “Morgan Stanley and Swiss consultancy LuxeConsult estimate that Breitling’s sales declined about 3 per cent last year, lagging both the broader Swiss watch market and the sector’s strongest private brands.” Both companies chose to mark down their investments, with CVC marking the investment down to 0.5 times invested capital based on the 2023 level and Partners Group valuing its holdings at about 0.7 times, according to the report.

According to the obtained consolidated 2025 annual report as of March 31, 2025, Breitling recorded CHF 782.3M in revenue, which is a decrease of 5.6% from CHF 828.7M in 2024. The operating income decreased from CHF 104.0M in 2024 to CHF 90.9M in 2025, a 12.6 decrease y-o-y. In July 2025, S&P Global downgraded Breitling to “B-“ from “B”, with its overview stressing the continuous underperformance to its base case, as “group’s reported sales contracted 5.6% in fiscal 2025 (ended March 31, 2025), while S&P Global Ratings-adjusted EBITDA margin fell to 21.4% versus our previous expectation of 23.0%-23.5% over the same period.” S&P Global estimates the adjusted EBITDA was about CHF 167.4M for fiscal 2025.

We chose the public company Swatch Group (UHR.SW) as a comparable to Breitling. The company is considered one of the world’s largest watch manufacturers by volume, and is also headquartered in Switzerland. We used financials for Swatch Group’s FY2024 ended on December 31, 2024, which is only 3 months away from Breitling’s fiscal 2025 (ended March 31, 2025), to conduct the valuation comparison. Swatch Group was traded at roughly 12.4 EV/EBITDA in September 2025 according to this site. If we apply this multiple to Breitling based on its fiscal 2025 financials, it would suggest the equity value of the company should be written down by the 60% range, which is even lower than CVC’s 0.5 markdown. Even if Partners Group had some initial investment in the company at a lower valuation in 2021, we think the overall position should still be marked down substantially.

Common Equity Investment Value and Preferred Equity Value Are Moving in Opposite Directions

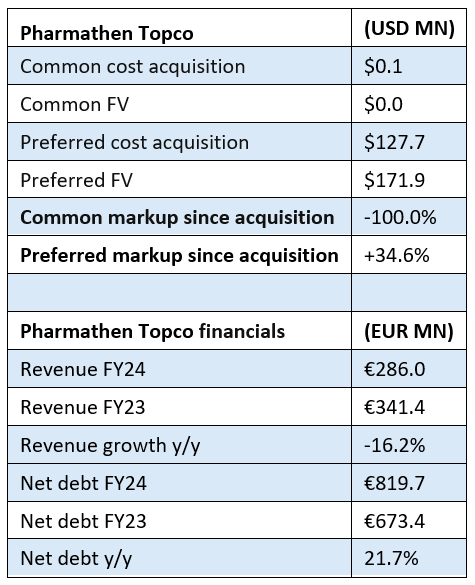

Pharmathen Topco – Common Written to $1; Preferred Marked Up

Pharmathen Bidco’s 2024 accounts disclosed a 16.2% year-over-year decline in revenue, two consecutive years of net losses, and net debt growth from €673.4 million to €819.7 million.

The Master Fund has written its Pharmathen common equity position down to $1 after 3 years, almost a total write-off. Over the same period, the Master Fund’s biggest preferred equity tranche in the same company are marked up 37.9%, whereas the other two preferred equity tranches were marked up 5.9% and 25.6%, respectively, after little over half a year.

An increase in the preferred mark in a stack where the common has been written to near-zero requires assumptions about recovery value on the preferred tranche that Partners Group has not disclosed. Once again, it seems to us that the numbers were bent to arrive at the desired valuation.

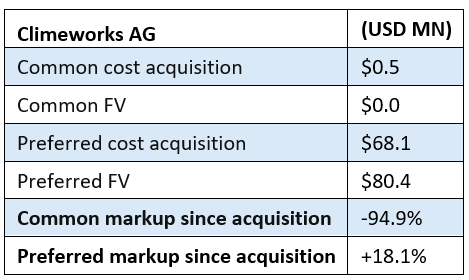

Climeworks AG – Common Written Down 95%; Preferred Still Marked Up 18%

The Master Fund has written down its Climeworks AG common equity investment by 94.9%, from a cost of $465,142 to the fair value of $23,847. That write-down seems to be consistent with public reporting that Climeworks has been cutting approximately 22% of its workforce as weaker US policy support and funding uncertainty hit its carbon-removal projects, particularly a planned Louisiana facility.

Over the same period, however, the Master Fund’s preferred equity investment in the same company is still marked up 18.1% as compared to its cost.

Common Equity Investment Value Jumped Hundreds of Percent in a Short Period of Time

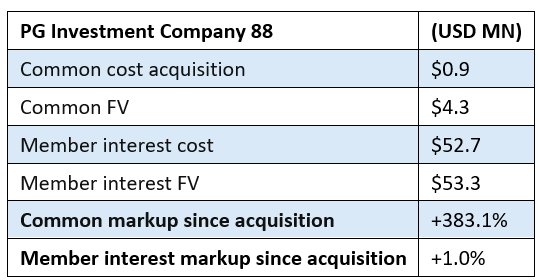

PG Investment Company 88 – 383% Common Markup in 26 Days

The Master Fund acquired its position in PG Investment Company 88 S.à r.l. on September 4, 2025, at a combined cost of $53.6 million ($895,945 in common equity; $52,715,562 in member interest).

At the September 30, 2025, reporting date, 26 days later, the combined position was marked at $57.6 million, a 7.4% return, driven by a 383.1% markup on the small common-equity slice.

We were unable to obtain the filed accounts of PG Investment Company 88 S.à r.l. Partners Group has not publicly disclosed the inputs or transaction data supporting a same-month markup of this magnitude on a newly-acquired position.

A 383% common-equity markup within 26 days of acquisition is not a conventional Level 3 fair-value update. It requires either an immediate third-party reference transaction or a material change in the underlying business, in either case, one that warrants disclosure.

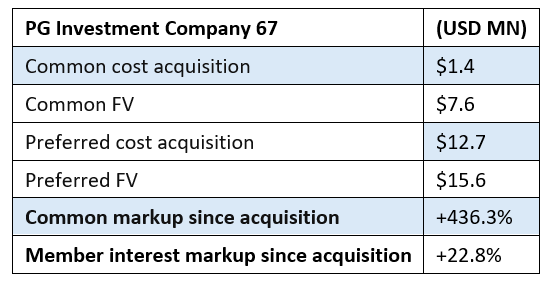

PG Investment Company 67 (Afileon) – 436% Mark Up within 14 months deserves Explanation

PG Investment Company 67 S.à r.l. owns 99.6% of Afileon Lux WP S.à r.l. (related to the professional services firm Afileon that is focused on tax consulting, auditing, legal advice) and 100% of SCUR-Alpha 1716 GmbH.

The Master Fund’s position was acquired on July 16, 2024, at a combined cost of $14.16 million ($1.41 million common, $12.74 million preferred). Approximately 14 months later, on September 30, 2025, the Master Fund reports the common equity part marked up 436.3% (to $7.59 million), and the preferred equity part marked up 22.8% (to $15.65 million).

We were only able to obtain the balance sheets for the underlying operating entities. In the absence of other accounts, Partners Group’s reported 436.3% common equity return in approximately 14 months cannot be independently verified against underlying financial performance. The absence of verifiable disclosure is itself the finding: Partners Group is marking a position that outside investors cannot check.

The Master Fund’s Direct-Debt Book Contains Reported Movements That Cannot be Reconciled with Standard Accounting

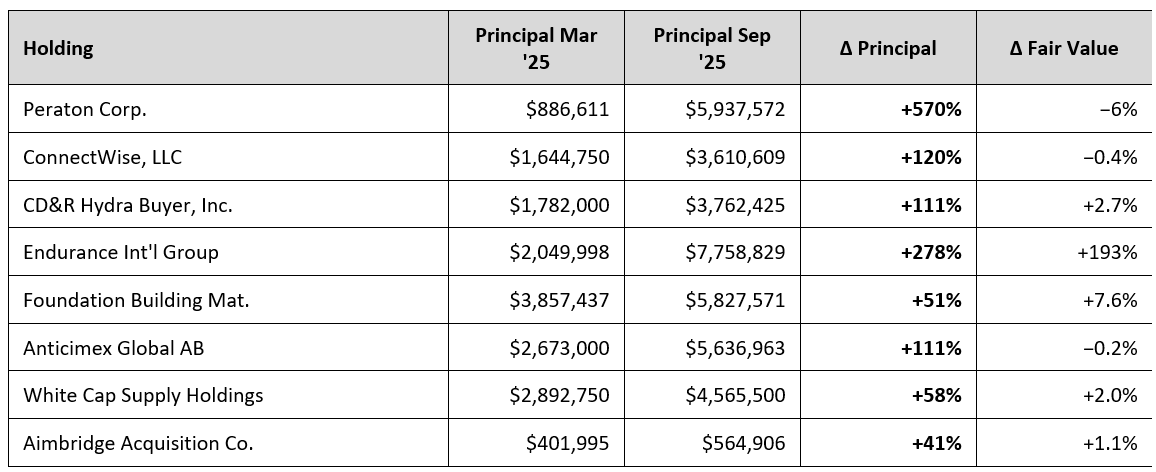

Across Partners Group’s flagship US evergreen fund, the Master Fund’s direct-debt portfolio spans hundreds of positions in senior loans, second-lien debt, and mezzanine instruments, valued in aggregate at approximately $840 million as of September 30, 2025. Between March 31 and September 30, 2025, the principal balances reported for numerous positions moved in ways that, following a valuation methodology a former Partners Group valuation professional described, should not occur absent a follow-on investment or a paydown. On seven positions, principal rose by between 40% and 570% while fair value barely moved. On two positions, principal was reported as zero while fair value remained in the millions. Partners Group has not publicly explained the mechanics producing these marks.

A former Partners Group valuation professional confirmed the standard mechanics: principal is the actual amount owed back by the issuer of the debt. Principal on a debt instrument doesn’t change. The only reason the principal on Partners Group statements would change would be if they made a greater investment. When they do, the cost needs to increase accordingly. There shouldn’t be any principal change without a corresponding cost change.

Between the Master Fund’s March 31, 2025 schedule of investments and its September 30, 2025 semi-annual report, we identified ten direct-debt holdings where the reported principal balance moved in ways that would require, under that standard logic, a corresponding move in cost and fair value. The corresponding move did not occur.

Pattern A: Principal Up Substantially, Fair Value Barely Moved

Source: Master Fund schedules of investments as of March 31, 2025 (N-CSR) and September 30, 2025 (N-CSRS). Dollar figures are as reported by Partners Group in the respective SEC filings.

Pattern B: Principal Reported as Zero, Fair Value Still in the Millions

On two holdings, the Master Fund’s September 30, 2025, schedule reports principal of zero, while carrying material fair value:

A senior debt instrument with zero remaining principal should not carry a positive fair value on a solvent issuer. Partners Group has not disclosed the accounting methodology that produces these marks.

What Standard Accounting Should Look Like

For a private-credit position valued under ASC 820 (Fair Value Measurement) and held by a registered investment company:

- If the borrower makes a scheduled principal payment, the reported principal balance decreases by the payment amount, the cost basis is reduced in parallel (as the adviser’s economic exposure shrinks), and the fair value is remeasured on the remaining principal.

- If the borrower defaults, the fair value is marked down to expected recovery value. The reported principal does not go to zero unless the loan has been fully written off or the debt forgiven. A zero-principal / positive-fair-value combination is not a standard presentation.

- If the adviser makes a follow-on investment (increasing the debt outstanding), the reported principal increases and the cost basis increases by the amount invested. Fair value then moves based on the new total exposure.

The expert we interviewed emphasized that the last case is the only mechanism by which the reported principal on a debt instrument should change, absent a payment or writeoff. ‘There shouldn’t be any principal change without a corresponding cost change,’ the expert told us.

In the Master Fund’s September 30, 2025, direct-debt schedule, we observe principal changes that do not correspond to either payment flows or documented follow-on investments. In the Dentive Capital and Sigma Holdco lines, the reported principal goes to zero while the fair value remains materially positive, a combination that is neither the scheduled-payment case (where FV would also decline) nor the default-and-recovery case (where principal would not be reported as zero).

Partners Group’s Private-Credit Software Exposure is Likely Understated

In February 2026, Partners Group issued a press release stating that the firm “has reduced its software exposure to less than half the industry average.” Partners Group did not disclose either the industry average it was benchmarking against or its own exposure figure.

Third-party estimates of private-credit software exposure cluster in a range:

- S&P Global: For Q3 2025, the software and affiliated sector accounts for 28.7% of fair value of loans held by BDCs and interval funds.

- P. Morgan: Private credit has approximately 21% exposure to software. Exposure rises to approximately 40% when broader tech and business services are included.

- Octus: BDC software exposure is approximately 30% of investment cost and fair value.

For Partners Group’s “less than half the industry average” claim to hold, the firm’s software exposure must be below approximately 10.5% to 14% at its own book.

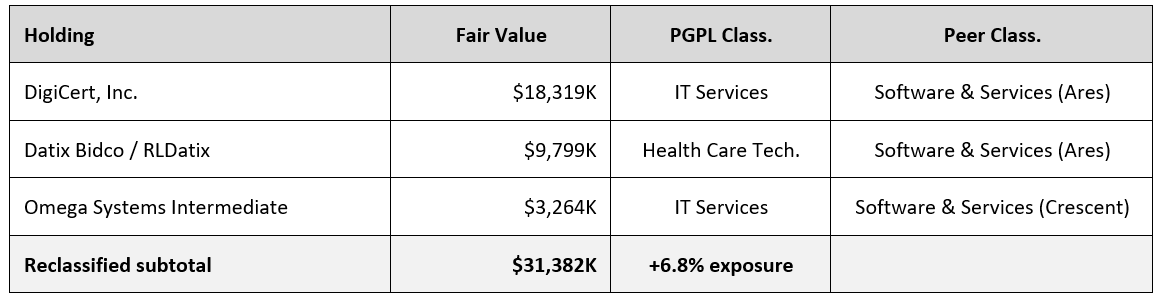

Partners Group’s SEC-registered BDC, Partners Group Private Lending, LLC (PGPL), reports 25.2% software exposure as of December 31, 2025 which already above Partners Group’s implied ceiling.

That 25.2% apparently understates actual exposure. Three PGPL holdings that Partners Group classifies outside Software & Services are classified within Software & Services by other BDCs:

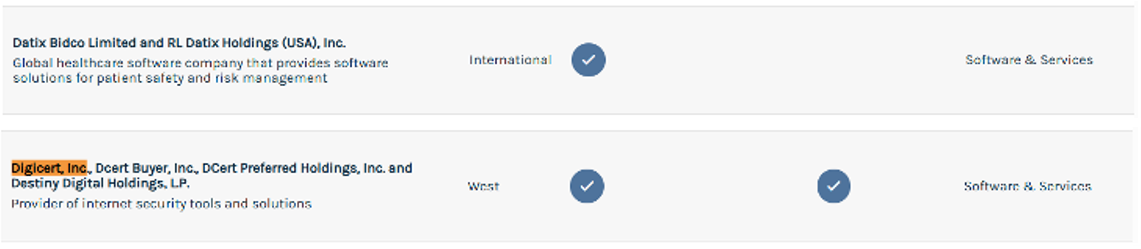

For example, Ares Management categorizes Digicert, Inc, Datix Bidco Limited, and RLDatix Holdings (USA), Inc. in the Software & Services, whereas Partners Group categorizes DigiCert, Inc. as IT Services, and categorizes Datix Bidco Limited and RLDatix Holdings (USA), Inc. in Health Care Technology.

Source: https://www.arescapitalcorp.com/portfolio

Omega Systems Intermediate Holdings, Inc. was categorized by Partners Group in IT Services; however, it is categorized by Crescent Capital BDC, Inc. under Software & Services.

On a peer-consistent basis, PGPL’s software exposure is 32.0% which makes it higher than Blue Owl Credit Income Corp’s WSJ-adjusted 21%, higher than JPMorgan’s ~21% private-credit estimate, and higher than S&P Global’s 28.7% BDC average. It is obviously not “less than half the industry average.”

Partners Group’s Chairman Steffen Meister told the Financial Times that he sees “a good chance” that private credit default rates will double in coming years, against a decade-average annualized default rate of 2.6%.

There are other signs that troubles might be on the horizon for Partners Group’s debt investments. We saw that from FY 2024 to 2025 the Partners Group Lending Fund (BDC)’s PIK loan count went from 12 to 21, but the aggregate fair value was roughly flat. There were also no new PIK issuances, meaning that existing, likely struggling loans were converted into PIK loans.

Redemptions

Based on the Master Fund’s disclosure, it appears that investors have started to be more cautious about their investments in the fund. For example, as of September 30, 2025, the redemption of common units for the Master Fund reached over $1.3 billion for the 6 months ended September 30, 2025. In the same period in 2024, there were only over $600M in redemptions from the investors.

Partners Group gave an extraordinary update in April 2026. While the company announced net subscriptions to the evergreen programs of $0.8 billion for Q1 2026, the announcement left out important details, especially about the Q4 performance. Partners Group only reports results semi-annually. We believe that fund raising momentum is already stalling.

We see redemptions ramping up once investors start looking closer into the valuation marks of Partners Group. The current environment makes this situation even more precarious for Parnters Group. A lot of assets have been bought at peak valuations, AI disruption is changing the dynamics in many industries, and experts we consulted with explicitly stressed that they doubt Partners Group will be able to refinance the associated debt of many of their deals.

Conclusion

We think Partners Group has accumulated a portfolio of assets in the evergreen funds that seem severely mismarked. Opacity about the investments combined with the ability to charge fees based on internal models in perpetuity is in our opinion a toxic mix. We challenge Partners Group to give a detailed response to the cases we outlined in this report. Investors should not accept a general dismissal or cherry picked response but demand actual transparency.

We think investors and regulators will increasingly wake up to the fact that control mechanisms in the private equity and private credit industry are often insufficient and ripe for abuse. The auditors, by design, cannot give investors an adequate view of private equity performance. Professor Luc Paugam, who teaches financial accounting at HEC Paris, told us that auditors typically view private-asset valuations as a key audit risk for material private investments. In assessing those valuations, auditors often rely on sampling: they do not review every valuation individually, but instead test a sample. He added that private-asset valuations are particularly challenging to audit because they depend heavily on judgment, involve significant subjectivity, and models are highly sensitive to small changes in key assumptions.

We think Partners Group has abused the leeway that the private equity and private credit sector grants.

The criticism that the private equity and private credit industry have recently received regarding their valuation marks might be best exemplified by Partners Group.

Appendix

Find our Appendix here.