Read below or open PDF version

- Ottobock SE & Co. KGaA (“Ottobock”) is a German-based, international market leader in orthopedic and prosthetic/orthotic technology that went public in Frankfurt in October 2025 at a total €3.8 billion equity valuation and about €808 million in IPO shares sold.

- Ottobock’s majority owner Hans Georg Näder (“Näder”) inherited the company from his family and reportedly attempted to IPO Ottobock since 2015. He has been leading the company since the 1990s and currently owns approximately 81% of Ottobock’s shares. Näder has an excessively lavish lifestyle and cash-consuming site projects, which caused him to extract more money from the company annually than it earned since at least 2011.

- Näder fully drained the remaining equity in his holding vehicle by end of 2024. After valuation gains from Ottobock’s IPO in October 2025, Näder faces full depletion again by the end of 2030, making him desperately dependent on valuation gains from Ottobock.

- Hans Georg Näder has pledged all of his Ottobock shares in a margin loan with creditors, while establishing a holding structure that guarantees him control over Ottobock. This PIK loan’s nominal is currently standing at approximately €1.5 billion and, according to our calculations, accumulating interest at roughly 15% p.a. so Naeder will have to repay roughly €2.36 billion in 2030 when the loan matures with Ottobock being the only discernible profitable asset to service the mounting obligations.

- We think majority shareholder Hans Georg Näder is drowning in debt, and minority shareholders will have to suffer for it, because it creates an enormous overhang in an illiquid, currently overpriced stock. We see a Damocles sword hanging over the heads of minority shareholders.

- Ottobock’s revenue grew from €1.0 billion in 2019 to €1.7 billion in 2025. The company uses what we view as misleadingreporting metrics, namely the “Underlying Core EBITDA,” that only seems to mask the real underlying business performance.

- Ottobock applies aggressive accounting metrics regarding the capitalization of research and development costs, as well as the consolidation of its Russia business. We believe Ottobock artificially inflates its reported earnings with these accounting shenanigans. German accounting and audit experts we consulted with called the accounting practices impermissible.

- Ottobock’s currently trades at about 42x trailing earnings, while its business is mature and oligopolistic, rather than the growth industry it is priced for. This valuation seems excessive and does not adjust for Ottobock’s aggressive accounting treatments. We estimate the fair value of Ottobock’s stock to be around €30.

- Today, Ottobock makes, we estimate, 35.1% of its total net income from sales to Russia. Export databases of customs agencies reveal that the majority of Ottobock’s exports have been end up in low-GDP countries and larger proportions might actually be routed to Russia, as well. We believe Ottobock actively supports the Russian war propaganda effort by acting lenient regarding regulatorily required checks for military use of its products. Russian media has publicly featured soldiers that received Ottobock prosthetics.

- The industry margins in Western markets are under pressure, due to technical product maturity and competition. We think Ottobock trades higher Russian margins for brand degradation and risk of facing legal, financial, and regulatory penalties for effectively servicing the Russian military.

Content

Introduction

Ottobock SE & Co. KGaA is one of the world’s leading manufacturers of prosthetics, orthotics, and mobility solutions. Founded in 1919 in Duderstadt, Germany, the company has grown into a global player.

Ottobock has been a family business. Hans Georg Näder inherited the company from his father, Max Näder, who took over the company from his father-in-law, Otto Bock. Otto Bock is widely celebrated as the founder of the company, but has been described as in a recent historical study as follows:

“Based on the surviving documents, Bock appears to have been an opportunistic entrepreneur who not only accommodated himself to the Nazi system but also knew how to exploit it for his own business purposes. In doing so, he made economic considerations the maxim of his actions and possibly subordinated moral scruples to them.” – Ronja Kieffer: Ottobock im Nationalsozialismus. Socitäts-Verlag, April 2026. (p. 86)

Hans Georg Näder joined Ottobock’s management in the 1990s. After multiple failed IPO attempts since 2015, Ottobock went public on the Frankfurt stock exchange in October 2025. The IPO left Näder with approximately 81% of the outstanding shares as the controlling shareholder.

Central to Ottobock’s structure is the tight control exercised by Näder. Through a complex SE & Co. KGaA structure and Näder’s holding companies, the Näder family retains full strategic, operational, and voting control via the personally liable general partner. This special corporate setup allows Näder and his family to dominate decision-making, with no real influence from external shareholders.

Wesee glaring conflicts of interest and a culture that panders to the needs of its dominating shareholder Hans Georg Näder while putting other shareholders and the company as a whole at risk.

It Starts With Näder’s Private Cash Consumption

Hans Georg Näder is a prominent figure in German media and often featured in boulevard press.

Several medias reported on Näder’s excessive private consumption. In August 2017, Der Spiegel already reports on Näder’s lavish lifestyle (“aufwändiger Lebensstil“). In a 2025 article, WirtschaftsWoche quotes payments to Näder of €600 million at only €340 million earnings after taxes for Ottobock from 2010 to 2022. The Spiegel article mentions “luxurious yachts”, art pieces and real estate as destination for the funds. The WirtschaftsWoche article quotes a former Näder “companion”: “[for Näder] it always must be bigger, better, greater.” In 2017, as well, Welt published a critical article claiming that Näder evades German taxes for an expensive yacht with its registration in Malta. Furthermore, union representative Oliver Mizera said openly on a stage at a local city fest Ottobock’s leadership is “partially exploiting” (“teilweise ausnehmen”) the company.

Näder showcasing is luxury yacht for Bunte (18 | 2018)

Näder proudly presents his lifestyle to the public by being featured in mainstream tabloid media, such as Bunte and Bild. He presented his favorite yachts in the yacht magazines Boote Exklusiv, the Pink Gin VI (2017-04) and, the Pink Shadow, in Boat International (2024-04). Furthermore, Näder owns and uses a private jet, a Bombardier Global 7500, for international and intercontinental travel.

Hans Georg Näder’s (“HGN”) Bombardier Global 7500 (costs: $81M + $4.4M annually), via WirtschaftsWoche

The man seems like a proper international playboy, but does he have the skills to back it up?

Näder with his local contacts for Bunte (18 | 2018)

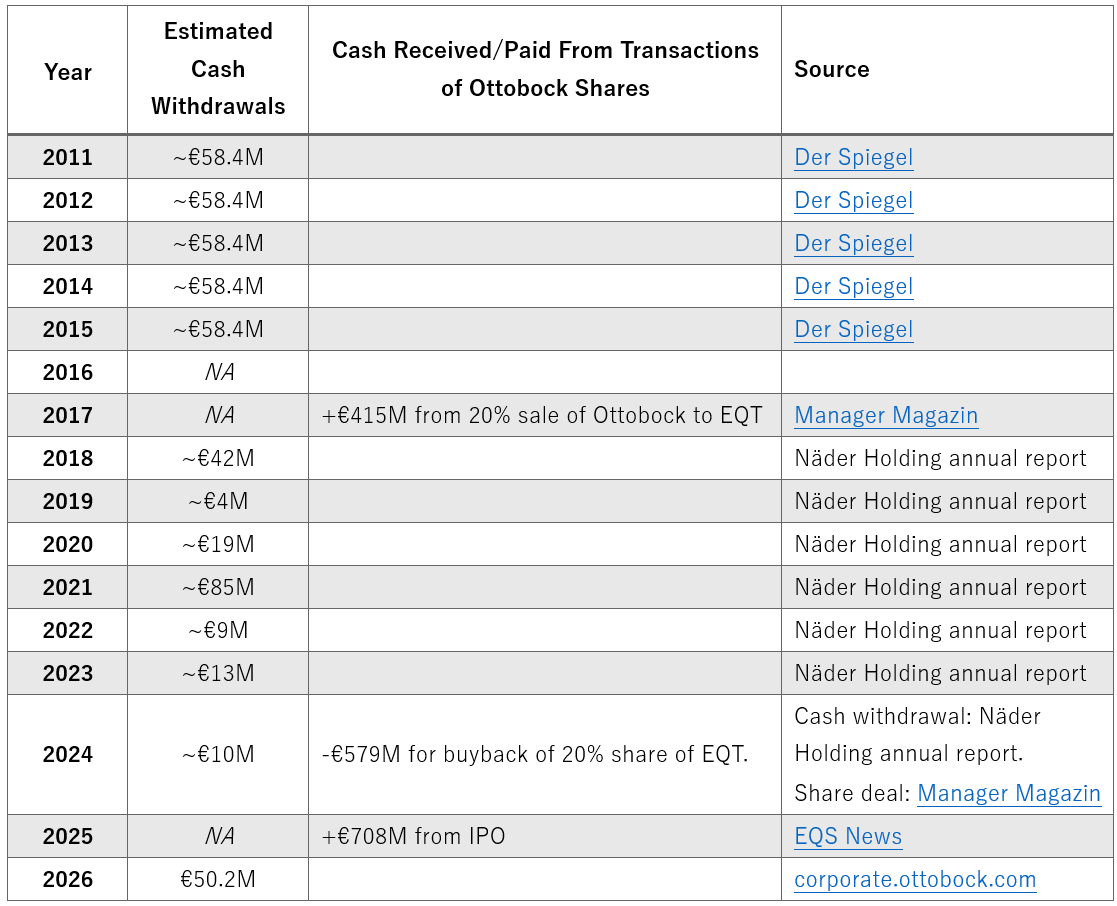

Näder Holding Fully Exhausted Its Equity by 2024

The following table shows Näder’s annual cash withdrawals from Ottobock for his private consumption and endeavors unrelated to Ottobock.

Note: estimates according to sources (Der Spiegel, Manager Magazin, Manager Magazin, EQS News, corporate.ottobock.com, investors.ottobock.com).

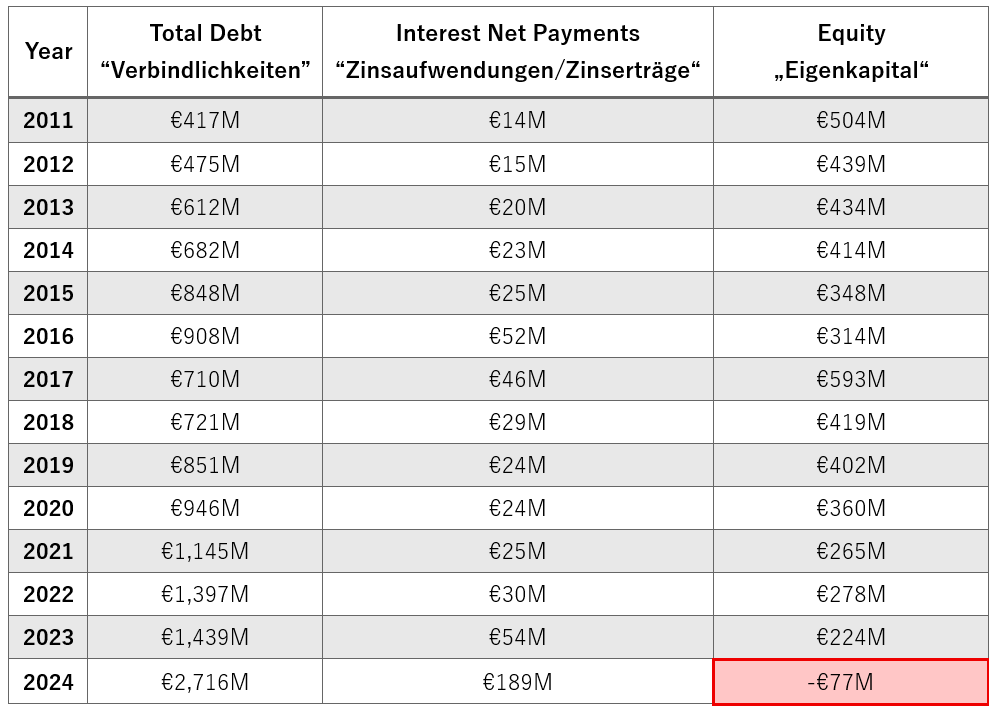

In addition to cash withdrawals, Näder’s holding company, Näder Holding GmbH & Co. KG (“Näder Holding”), is engaged in a multitude of other businesses and real estate deals with a €176.0 million total loss in 2024 and total liabilities of €2,716 million.

As of the latest available public Unternehmensregister data from year-end 2024, Näder Holding has equity of -€77 million, down from €593 million in 2017. While Näder Holding fully depleted its equity over time, interest expenses have escalated due to ever increasing debt burden and the changing interest rate regime since 2023.

The 20% Ottobock share repurchasing deal in 2024 implies a total valuation for Ottobock of around €2,895 billion. Thus, with a current valuation of €3.846 billion, Näder Holding’s asset value from their 80.88% Ottobock stake has increased by about €769 million minus about, we estimate, €260 million in interest payment until May 2025 minus further potential operational losses in other ventures that are not publicly reported yet.

These results point to a dramatic situation for Näder: with an estimated €423 million in equity left today, against interest expenses of around €200 million annually plus private consumption, Näder Holding faces negative equity again in about two years. We think the only viable option for Näder to generate the cash needed to service the debt is the sale of Ottobock shares.

Näder’s Margin Loan Puts Ottobock at Risk of a Takeover

Näder entered a Payment-in-Kind (“PIK”) loan of €1,100 million in March 2024, which he used to buyback 20% of Ottobock from Swedish private equity firm EQT before the IPO. PIK loans allow borrowers to avoid cash payments by using additional debt as a substitute, delaying cash payments to maturity. The literature describes “PIK securities are often used in high-risk financial strategies,” and “borrowers without access to bank credit lines often rely on PIK features to manage liquidity shortfalls.”

“PIK is risky for almost everyone involved. For shareholders, the most worrying aspect of PIK debt is the way it can snowball to a size that eats into the equity of the business.” – Bloomberg

According to the 2024 annual report of Näder Holding (p. 34), the loan is due in 2028 but interest payments before maturity are added to the nominal. The interest rate depends on the EURIBOR rate and is likely EURIBOR+x. The annual report mentions €1,222.8 million as current loan valuation on December 31, 2024, which implies under HGB accounting rules an interest rate of close to 15% p. a. and loan nominals, for 2025/2026/2027/2028 of €1,406.2/€1,617.2/€1,859.7/€2,138.7 million.

On page 17 of 2024 annual report of Näder Holding we find the following sentence that indicates all of Näders’ Ottobock shares pledged for lonas: “Als Sicherheit für die sonstigen verzinslichen Darlehen gegenüber Dritten wurden die Anteile an der Ottobock SE & Co. KGaA verpfändet.“

However, Ottobock’s IPO prospectus that was filed in September 2025, about nine months after Näder Holding’s annual report’s accounts’ date, describes the loan differently. The loan principal is reduced to €1.02 billion, and the maturity is extended to March 31, 2030, while all shares are still pledged. (cf. p. 34) It seems, Näder restructured the loan for a later maturity.Assuming the interest rate remained at a similar level, we expect a due payment of about €2.36 billion at the end of maturity.

The loan is facilitated by the following financiers:

- Carlyle Global Credit

- Kohlberg Kravis Roberts

- Hayfin Capital Management

- Macquarie Capital Principal Finance

The loan is collateralized with Ottobock shares, meaning that the default of repayment obligations gives the lenders the right to seize Näder’s Ottobock shares.

The loans maturity is in 2030 and becomes immediately due if Näder’s share in Ottobock falls below 60% or Näder loses control over Ottobock according to the IPO prospectus (p. 34).

While the precise terms of the agreement are not public, a typical range of collateral loans given against pledged shares are 30% to 40% of the stock value at the time of the agreement.

Näder has burned about €45 million annually on average from 2011 to 2024 between his other operations, private consumption and interest payments. (We inferred this amount from the decline in Näder Holding’s equity value.) Näder will only be able to service his loan in two ways:

A) Näder extracts substantial cash from Ottobock, hurting it’s share price

B) Näder defaults on the loan, and hands over the shares to the consortium

We see indicators that the consortium is capable to execute case B.

- The Carlyle Groupowns a large diversified private equity portfolio. They often hold controlling equity in private companies before selling them at exit events (SPAC, sale, IPO). There is concrete recent precedence of a comparable takeover case: in 2024, Keter, a Dutch-based manufacturer of outdoor furniture and storage products, failed to repay a €1.2 billion loan to a group of lenders that included Carlyle Global Credit. Carlyle assumed control by swapping debt for equity and took ownership from former private equity sponsors BC Partners and PSP Investments.

- KKR & Co. Inc. holds sizeable equity positions in a wide range of companies in tech, healthcare, consumer, and industrial sectors around the globe

Hayfin Capital Management and Macquarie Capital Principal Finance mostly provide loans.

As of the latest available Bafin filings (March 31, 2026), Näder owns 80.88% of Ottobock’s shares that currently are valued at €3.053 billion. This means the current loand-to-value (“LTV”) ratio stands at 36.1%. A realistic margin call trigger for a collateralized position in a mid cap value stock like Ottobock is an LTV of about 55%.

Thus, if Ottobock’s share price falls below a price somewhere close to €38.58, we expect Näder to experience a margin call.

One might argue that Ottobock is better off without Näder in the picture, but in the medium term a situation like this would create a lot of turmoil and uncertainty.

How Näder’s Financial Pressure May Tie Into Ottobock’s Corporate Culture Directly

In our experience, fraudulent actors do not usually set out to commit fraud. They find themselves in situations where they feel forced to commit what they might see as little white lies, but sooner than they know they find themselves amidst a full-sized corporate fraud.

We think the financial pressure that Hans Georg Näder put on himself personally has forced Ottobock to an IPO, while Näder intends to stay fully in charge at his company. At the same time, we see Näder’s debt spiraling out of control.

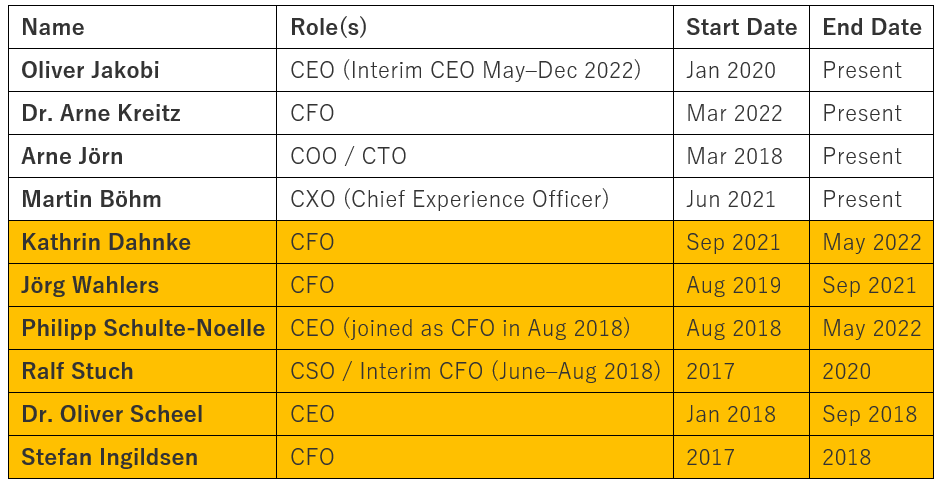

One potential indicator of unreliable leadership in a public company is the turnover in executive positions. The following table summarizes the turnover in key executive positions at Ottobock since 2017. The company saw six different acting CFOs and three different CEOs since 2017. Especially the high turnover in the CFO position makes us suspect that Näder wanted to push financial decisions through that the acting executives were not willing to sign off on. In particular the CFO position has been discussed before in the context of Näder’s potential demeands in relation to the IPO.

Note: orange highligthed names left the company by now

Ottobock’s Russia Business

According to 2023 data, which is the last available with sufficient granularity, Ottobock’s Russian operations provided earnings of over €12 million at only €48 million (i.e. 25% of total) earnings from the prosthetics business overall that year. Ottobock’s main competitor Össur said prominently it suspended its Russia business in 2022. Ottobock tries to frame its Russian operation as less operationally relevant but discontinued its regional sales reporting for 2025 annual reporting by subsuming Russian business into the “EMEA” (Europe, Middle East and Africa) reporting unit.

“To mitigate the risks of declining profitability associated with business activities in Russia, the extent and necessity of good deliveries are continuously evaluated. Ottobock does not have any material long-term assets in Russia, and there are no critical supplier relationships with companies based there.” – Annual Report 2025, p. 57.

According to the IPO prospectus, Ottobock generated 8.8% of its global revenue from Russia in the first half of 2025, the last available transparent number, up from 6.8% in 2024, and 5.0% in 2023. despite having announced to reduce “its presence in Russia from seven locations to four since the war began”. While earnings from Ottobocks Russia business for 2025 are not specified by the company, and only subsumed into “EMEA” region numbers, an extrapolation from the above figures indicate that these are material.

In total, while Ottobock’s revenue grew by 12.4% from 2023 to 2025, revenue from Russia grew by %76.0 (conservatively applying the 2025 H1 share of revenue for FY). Revenue growth from Russia is around €56.8 million of €184.0 million (i.e. 31% from total growth). If we assume a similar profitability for Ottobock’s regional business lines in 2025 as recorded for 2023, the profit share of Ottobock’s Russia business is €21.1 million of €60.0 million, or 35.1%.

Ottobock’s close relations and ongoing business with Russia has been reported on before. In December 2017, Ottobock’s now CEO Oliver Jakobi met with Russian president Putin at a lobby event. In early 2025, Manager Magazin (now only available on web.archive.org) reported that Ottobock has delivered a substantial volume of products (“in erheblichen Umfang”) to Russia, according to 2023 shipment data, which was only possible after buying out private equity investor EQT, who opposed business with Russia. In April 2025, Business Insider published a detailed investigative report about Ottobock’s prosthetics appearing in Russian media and propaganda channels for veteran care and redeploy ability to the battlefield. Ottobock emphasized that it only services Russian civilians and openly fosters its access to the Russian market with local collaborations and conferences. However, the broader issue here is that Russia gains great propaganda value from visible access to Western leading mobility aids for their military, even if the products are only used sporadically for actual redeployments of troops. In September 2025, Wirtschaftswoche published an article that describes how Ottobock exported sanctioned goods into Russia and has ongoing business relationships with at least one Russian military hospital while the company claims it received all necessary special permits from German authorities and only aims to serve civilian purposes.

Furthermore, in May 2022, about three months after Russia’s invasion into Ukraine, Näder fired Ottobocks CEO and CFO, and replaced them with company insiders, making Jakobi the new CEO. Handelsblatt commented this rotation as „unexpected.“ While Ottobock’s public rationale for this seems nebulous, the timing raises the question as to whether the move might have been caused by fundamentally differing strategic priorities between Näder and the CEO.

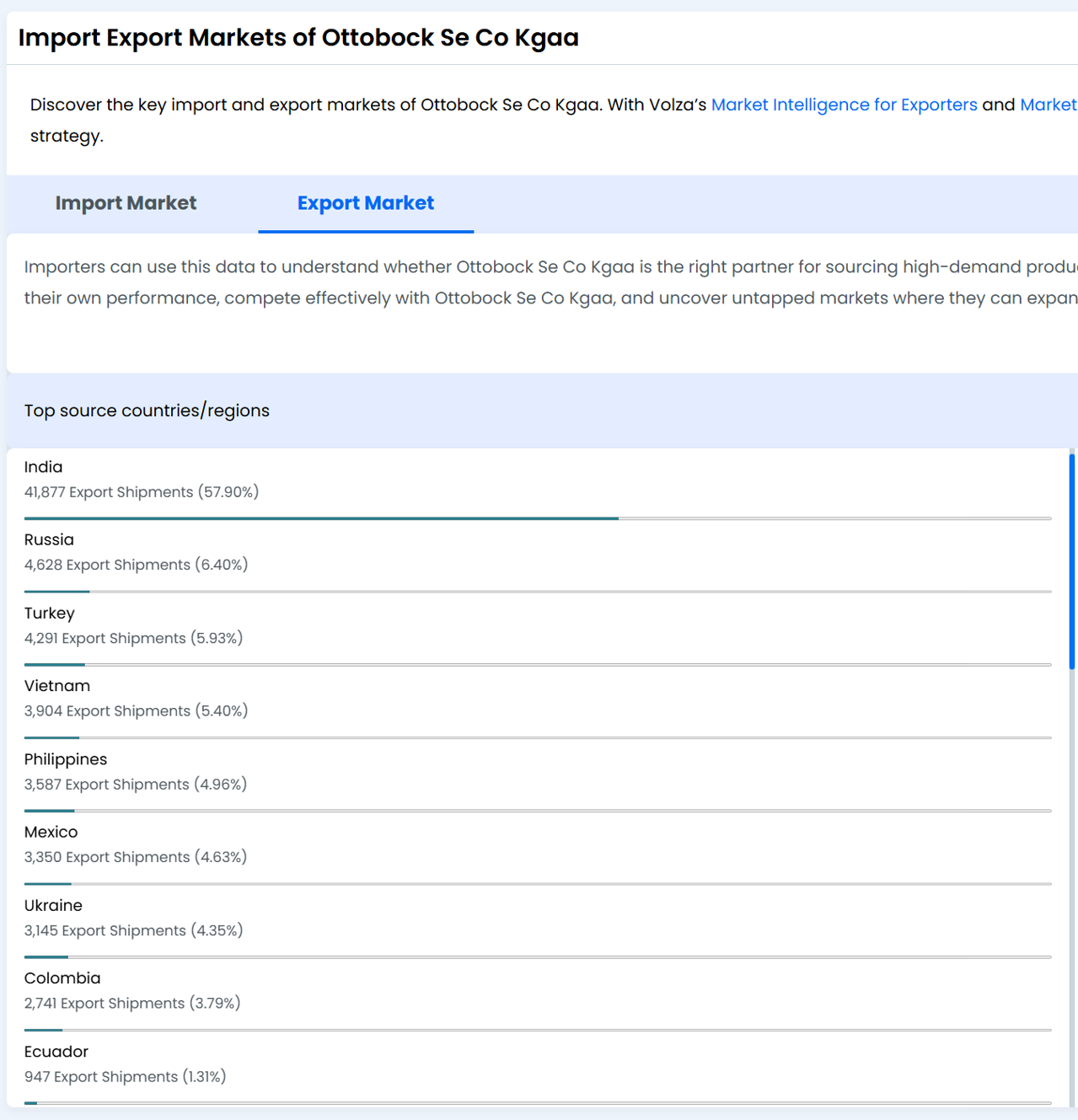

We see from public export data that Russia is Ottobock’s second biggest export market. Ottobock apparently has production facilities in India which explains the high exports of intermediary parts to the country.

Source: volza.com. Retrieved in February 2026. Data shows shipments until July 2025

Ottobock’s claim that they believe their products remain in non-military use only seems unconvincing. For example, Ottobock’s client Orto Dynamics LLC openly advertises their veteran services on social media ([1],[2]) and their webpage. Propaganda programs, like the Russian TV show “Doctor” feature Ottobock prosthetics for injured fighters.

The 19th EU Sanctions Package (October 2025) and Russian countersanctions (latest renewal in September 2025) have significantly restricted the ability of foreign companies to repatriate cash from Russia. If Ottobock cannot “repatriate” those profits, the €12 million to €21 million annual (see our Russian business share estimates above) profit from Russia is essentially “trapped cash,” which some analysts argue should be discounted in a conservative valuation.

We think it is reasonable to assume that the Russia business, which has been growing to 8.8% of revenue, produces significantly higher profit margins. With Össur having exited Russia entirely, Ottobock is left with significantly reduced competition. Additionally, grey area markets usually provide a certain risk premium that is expressed in higher profit margins.

Champion of Adjusted Numbers and Accounting Trickery

Ottobock’s predominant reporting number is “Underlying Core Ebitda” (c.f. Ottobock IPO prospectus, p. 117) The metric is defined as follows (emphasis added):

“Underlying Core EBITDA is defined as the Underlying EBITDA generated by our core business (i.e., the Products & Components (B2B) and Patient Care (B2C) product categories). Underlying EBITDA is defined as our EBITDA adjusted for extraordinary items which distort sustainable profitability.”

EBITDA is an often-discussed ([1],[2]) misleading metric for, in aprticular, physically producing industries with production facilities and/or high capitel expenditures. This is how Warren Buffet and Charlie Munger summarize it:

“References to EBITDA make us shudder—does management think the tooth fairy pays for capital expenditures? We’re very suspicious of accounting methodology that is vague or unclear, since too often that means management wishes to hide something.” – 2000 Berkshire Hathaway Letter, p. 17

What does not fall under core businesses for Ottobock?

“For management reasons, the revenue of subsidiaries or business units which were either already divested, discontinued, or for which a resolution for a divestment or discontinuation within the next 18 months was made, are reported in the non-core product category.” – Ottobock Annual Report 2025, p. 34 (emphasis added)

Thus, Ottobock can exclude all poorly performing business segments by categorizing them as non-core. Ottobock’s leadership just has to formally decide to offer the unit for sale, even if no buyer is available. Thus, the “core” accounting category is a genuine application of cherry-picking.

In their latest annual filings, Ottobock presents “Underlying Core EBITDA margins” of 26.0% to its investors according to their own EBITDA metric, while actual GAAP IFRS net margins are only 5.3%.

Balance Sheet “Optimization”

For the IPO, we believe Ottobock used all accountinglevers to increase its reported assets and earnings, a practice that is commonly called window-dressing. To highlight Ottobocks maximal aggressive interpretation of the accounting rules for their own account, we compare the relevant accounting metrics to those of Össur hf., formally now Embla Medical hf. (“Össur”) since 2024, from Denmark/Iceland, Ottobock’s most similar industry peer.

Russian Branches Consolidation Without Business Share Disclosed

Currently, Ottobock fully consolidates its Russian branches in their group level accounts. However, the sanctions package and Russian counter sanctions have made it very uncertain if cash can be moved out of Russia for Western companies. This is in accordance with IFRS accounting standards, but investors must be properly informed about the share of revenue, assets and profits in Russia. Why did Ottobock disclose this in the prospectus but discontinued the regional reporting in their 2025 annual report? We estimate, Russian operations account for about 35.1% of total group profits, which would demand a dedicated disclosure of basic Russian branch financials.

R&D Cost Capitalization

Under IFRS (IAS 38), research costs must be expensed as incurred, while development costs are capitalized as intangible assets only when the company can demonstrate: (i) the technical feasibility of completing the asset, (ii) the intention and ability to complete and use or sell it, (iii) probable future economic benefits such as expected commercial viability or reimbursement, (iv) the availability of adequate technical, financial, and other resources to complete the project, and (v) the ability to reliably measure the directly attributable development costs.

This is what we found in the 2025 annual accounts. Competitor Össur reports $21.8 million in carrying amount for “Patents & Development Costs” (p. 118), which represents 1.25% of Össur’s total assets. Ottobock records €246.6 million “Development Costs” in carrying amount (p. 220), which represents 12.0% of Ottobock’s total assets. Össur’s annual R&D expenses were €45.9 million (equivalent to 2.6% of asset value), and Ottobocks annual R&D expenses were €72.7 million (equivalent to 3.5% of asset value). Over the last years neither Össur, nor Ottobock changed their R&D funding dramatically. If both companies follow the exact same internal accounting rules, we expect Ottobock’s capitalized development costs relative to total assets not to surpass Össur’s by more than twice. However, Ottobock’s accounts show a 9.6 times higher valuation of their capitalized development costs on the balance sheet compared to Össur. We believe this multiple is too big to be explained by product portfolio and development efficiency alone. We suspect that Ottobock has over-aggressively capitalizing development costs to artificially inflate profit margins.

Extended Depreciation Periods

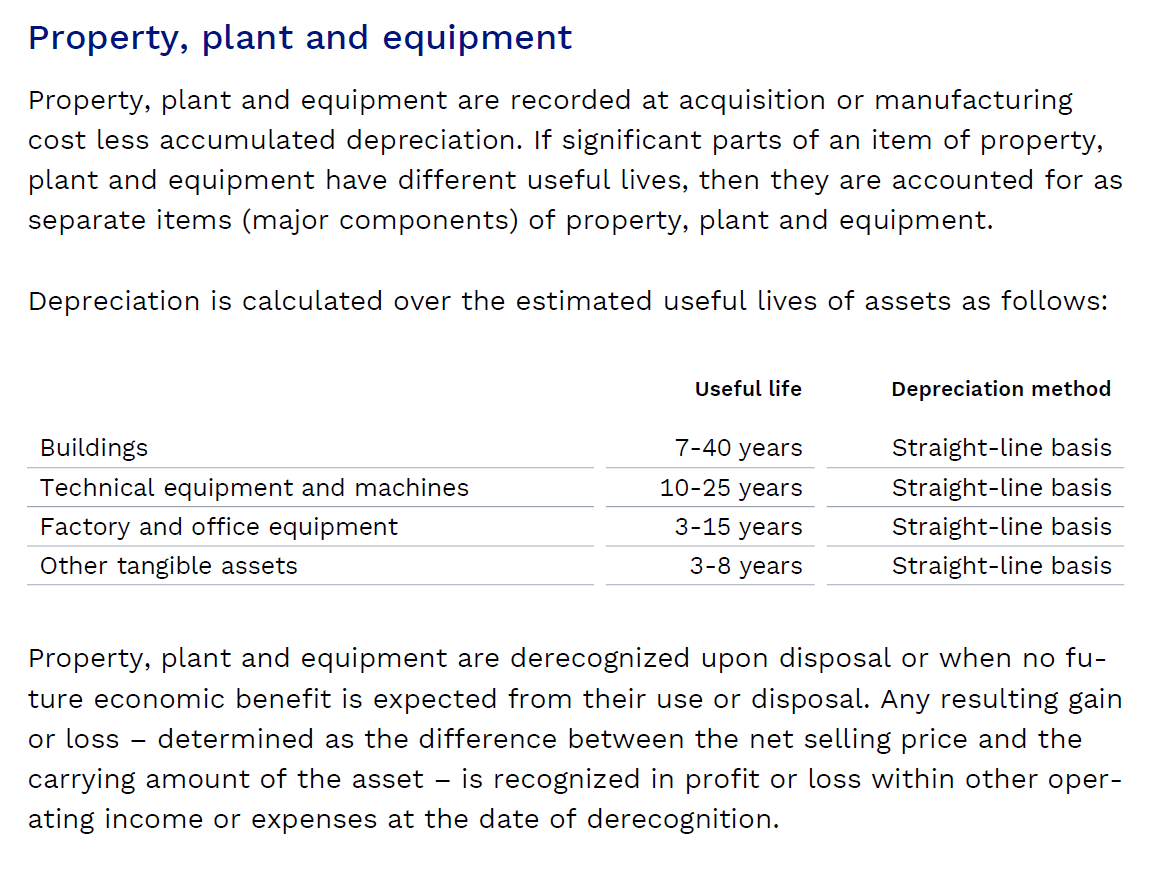

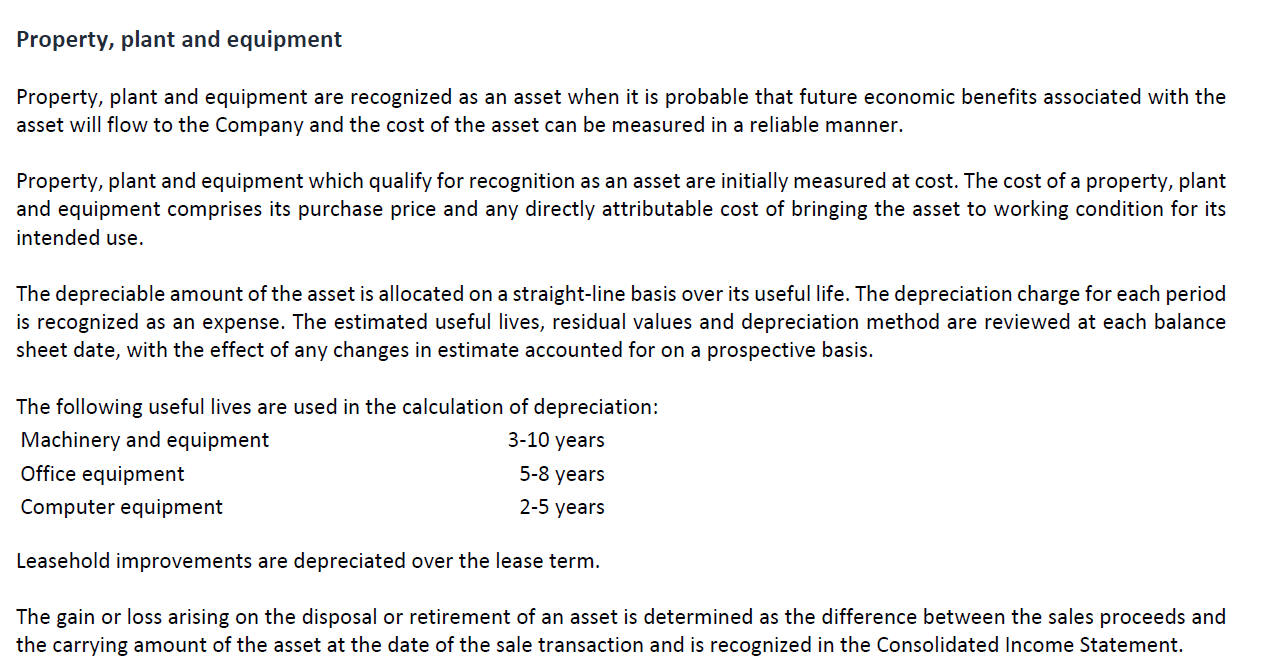

Ottobock uses much longer depreciation periods for their accounting than Össur. While Ottobock estimates the useful lives of “(Technical) equipment and machines” at 10-25 years, Össur only applies 3-15 years. In particular the maximum of 25 instead of 15 years allows Ottobock to keep large equipment units much longer on the balance sheet.

Ottobock Annual Report 2025, p. 193

Össur Annual Report 2025, p. 133

Ottobock’s Nazi Past

A recently published study by Ronja Kiefer (“Ottobock im Nationalsozialismus,” 2026, Societäts-Verlag) describes Ottobock’s relationship to Germany’s Nazi regime from 1933 to 1945. The company used forced laborers, specifically women from Eastern Europe known as “Ostmädchen“, at their Königsee plant to maintain wartime production. According to the study, this labor supported their deep integration into the Nazi war economy, where they specialized in the mass production of prosthetic components for the Wehrmacht. Furthermore, the study examines founder Otto Bock’s personal involvement as a Nazi party member.

A Fair Valuation for Ottobock’s Shares

Only 14% of Ottobock’s shares trade as float. Over all exchanges and dark pools combined, Ottobock’s shares trade about, estimated, €2.55 million on average daily. As a rule of thumb, 2% average weekly turnover is considered sufficient for efficient price discovery for a stock. Ottobock’s average weekly shares turnover is only 0.3%, indicating that the stock might be inefficiently priced.

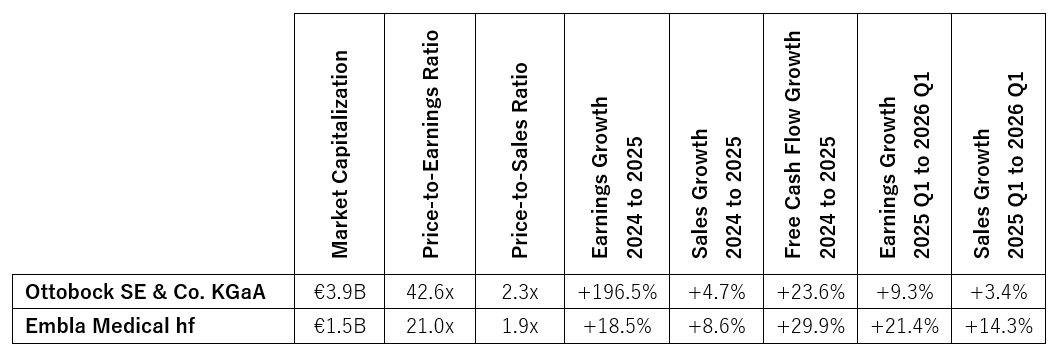

We compare Ottobock’s valuation to that of Embla Medical, who is Ottobock’s closest and long-time competitor, with its key brand, Össur. Like Ottobock, Össur focuses on non-invasive orthopedics, specifically prosthetics/artificial limbs and bracing/supports.

Source: Company filings. Ratios by 2025 annual results, trailing.

Ottobock explains its strong earnings growth of 196.5% from 2024 to 2025 being the result of its operational excellence by establishing a shared service center in Bulgaria, centralizing administrative tasks, and shifting production volumes to lower-cost platforms to realize productivity gains. Interestingly, this growth is not reflected in the free cash flow but rather distributed more complicatedly over other accounting items. The strongest regional annual revenue gains by 11.7% were tracked in the “EMEA” region, which could also be a euphemism for growth of Russia business. We think Ottobock applied aggressive window-dressing techniques to make the financials look as attractive as possible for the IPO.

Overall, this strong one-time earnings growth did not continue until 2026. Newest quarterly numbers for 2026, Q1, reveal that Ottobock’s earnings grew only moderately with 9.3% year-over-year, while Embla Medical showed much stronger growth.

While Ottobock has larger overall operations, Össur does not generate (meaningful) sales in Russia. The overall industry is mature and has limited growth prospects. We would only be willing to pay about 21 times current earnings for Ottobock’ shares, which suggests a share of €30, which is 50% below Ottobock’s current share price. This analysis gives Ottobock the benefit of doubt by taking the reported earnings at face value, while we believe Ottobock’s aggressive accounting could in reality warrant a strong discount.

Ottobock announced in March 2026 a first dividend payment for May 2026 of €0.97 per share, which is over 67% of 2025 GAAP EPS. A dividend payout ratio of 67% implies, by historical standards, a very high dividend payout suitable for a mature value stock, instead of an investment-heavy growth stock which Ottobockis priced for. It seems to us Näder did aggressively push for a big but unsustainable cash withdrawal of €50.2 million via dividend payments to Näder’s holding vehicle.

Conclusion

We think that Ottobock has a future, but not at this current valuation and probably not in the hands of Hans Georg Näder. We believe the issues we outline in this report show a severe conflict of interest between Näder the minority public shareholders of Ottobock and the company itself.

We think Näder has signed a deal with the devil by taking an aggressive PIK loan that, we believe, will ultimately cost him the company. With the PIK loan coming due in 2030, which will have accumulated to over €2.1 billion at this point, according to our estimates, Näder seems under enormous pressure to generate cash. At the same time, Ottobock’s shares, which are Näder’s main asset, seem severely overvalued and rather illiquid, creating what we see as a horrible risk-reward situation for minority shareholders.