Find a PDF version of this report here, and an auto-translated German version here.

- HelloFresh operates a subscription-based meal kit delivery service. Despite rapid growth during COVID lockdowns, the business is now in sharp decline, with management seemingly prioritizing self-enrichment at shareholders’ expense.

- CEO Dominik Richter’s private company borrowed massively against his HelloFresh’s shares to fund highly leveraged real estate investments by his brother Benedikt Richter, apparently triggering margin calls amid a steep share price drop. Our estimates indicate another significant margin call looms with just a 23% further decline and that Richter and his entities have run out of cash as well as shares to pledge.

- HelloFresh’s aggressive buyback program, backed by an activist with a history of value destruction, has burned ~€100m YTD 2025 yet failed to stop the share price from dropping ~50% YTD. We believe the accelerated pace is a desperate bid to avert CEO margin calls amid persistent business underperformance.

- Co-founder Thomas Griesel has repeatedly extracted value by selling call options on HelloFresh shares, which is one of the more egregious conflicts of interest for a sitting executive we have seen.

- Share transaction patterns around recent quarterly announcement suggest potential insider trading via frontrunning.

- Core demand is collapsing: since 2022 peaks, U.S. Google searches for HelloFresh are down 80%, website traffic is down over 61%, and its app has fallen from top-20 to outside the top-100 in Food & Drink downloads.

- Management obscures this via KPI manipulation, emphasizing “high-value” customers amid high churn, inflating growth with food price rises, and pivoting to saturated, low-margin segments.

- HelloFresh’s reputation is tarnished by ethical lapses and corner-cutting, including:

- U.S. child labor law probe (December 2024)

- Several clashes with employees in Germany, the U.S. and U.K. over “horrible working conditions”, union busting, and a retaliatory site closure

- U.S. regulators traced E. Coli infections in multiple states to HelloFresh (2022)

- Abrupt Japan unit closure without timely employee notice (December 2022)

- False marketing claims, including about CO2 neutral production and ethical chicken treatment

- $7.5M settlement for deceptive subscription enrollment (August 2025)

- $14M settlement for illegal telemarketing (2021), a poor 1.3/5 star review ratings, driven by overcharging, faulty cancellation tools, and app issues; subscription cancellations are deliberately obstructive

- We expect HelloFresh’s removal from the MDAX index in December 2025

Introduction

HelloFresh delivers pre-portioned ingredients and recipe cards to subscribers’ doors each week. Launched in Berlin in 2011 with the ambitious goal of “changing the way people eat forever,” the company swiftly expanded across Europe and into North America, Australia, and beyond, cemented its lead in the meal-kit category.

Revenue surged during the COVID lockdowns, cresting at €7.6 billion in 2022, yet growth has flatlined since. Management now pitches a turnaround centered on “high-value” customers, alternative brands, and adjacent categories like microwaveable ready meals via the Factor line, pet food, premium meats, and supplements. The company portrays confidence by running an aggressive share buyback program.

Our findings paint a starkly different picture. HelloFresh is in steep decline, obscured by shifting metrics and quixotic pivots. More troubling, leadership appears fully cognizant of the trajectory and is aggressively extracting personal value while leaving shareholders exposed to outsized risks. The first part of this report examines the mechanisms enabling this self-dealing and the leverage perils it has created as well as other management digressions related to self-enrichment. The second part of this report dissects the true state of the core business and why the official narrative no longer holds.

Content

For our readers’ convenience, we made this report index with clickable links to the relevant section.

A Reckless Leverage Play that Puts Shareholders at Risk

Dominik Richter, HelloFresh’s founder and CEO, once positioned himself as a visionary tech entrepreneur. Since the company’s share price peaked in 2021, however, his priorities appear to have shifted dramatically. Our research indicates that he is now focused on redirecting personal wealth into real estate while quietly extracting maximum value from HelloFresh.

How the CEO Extracts Cash

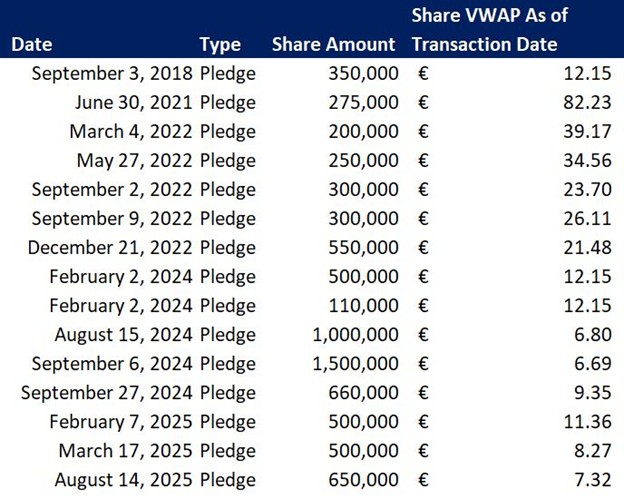

Through his private firm, DSR Ventures, Dominik Richter has extracted cash by pledging HelloFresh shares as collateral for bank loans. This approach lets him access liquidity without selling shares outright, but it carries the acute risk of margin calls if the stock price falls. In a severe scenario, if the borrower cannot post additional cash or collateral, the bank may liquidate the pledged shares, often triggering a sharp drop in the share price.

Germany’s public filing database discloses the number of shares pledged, though the exact loan amounts and the purpose of additional pledges, whether for new borrowings or margin calls, remain unclear. What is evident is that pledges increased significantly while HelloFresh’s stock price declined, strongly suggesting they were tied to margin calls.

Dominik Richter’s insider transactions (source: EQS News)

As of now, we calculated that 77% of Dominik Richter’s HelloFresh holdings are pledged via DSR Ventures. This implies that a further 23% drop in the share price would trigger another margin call. Our calculations are detailed in the Appendix.

What makes these pledges particularly toxic is that DSR Ventures used the loan proceeds to fund illiquid, highly leveraged real estate investments. Our research indicates opaque and concerning methods used to source the shares required to satisfy margin calls.

The Borrowed Money Funds Highly Levered Real Estate Investments

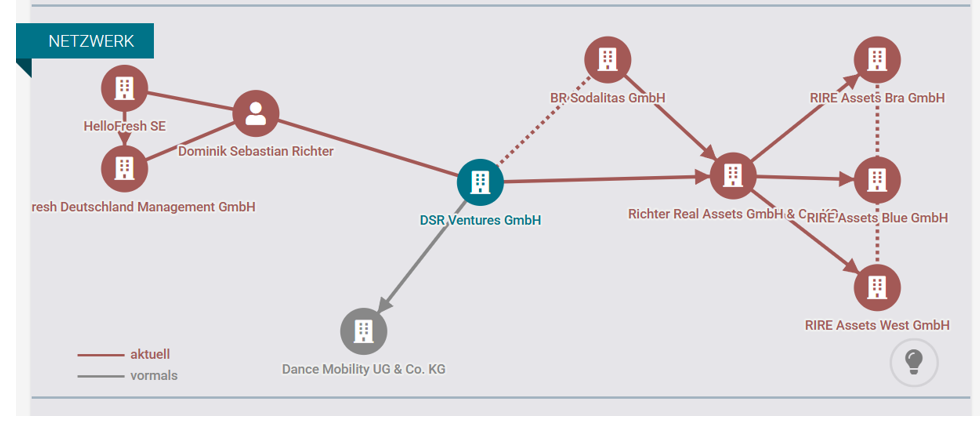

DSR Ventures presents itself as an angel investor, yet we found no public record of meaningful startup investments, no company website, and no employees listed on LinkedIn. Instead, the borrowed funds were channeled into a network of real estate companies.

Source: Northdata.com

Benedikt Richter, brother of HelloFresh CEO Dominik Richter, gained initial wealth from the 2017 HelloFresh IPO as a mid-level manager and left in 2018. After a failed WeWork-style venture, he assumed management responsibilities of the Richter family real estate empire in 2020. He owns BR Sodalitas GmbH.

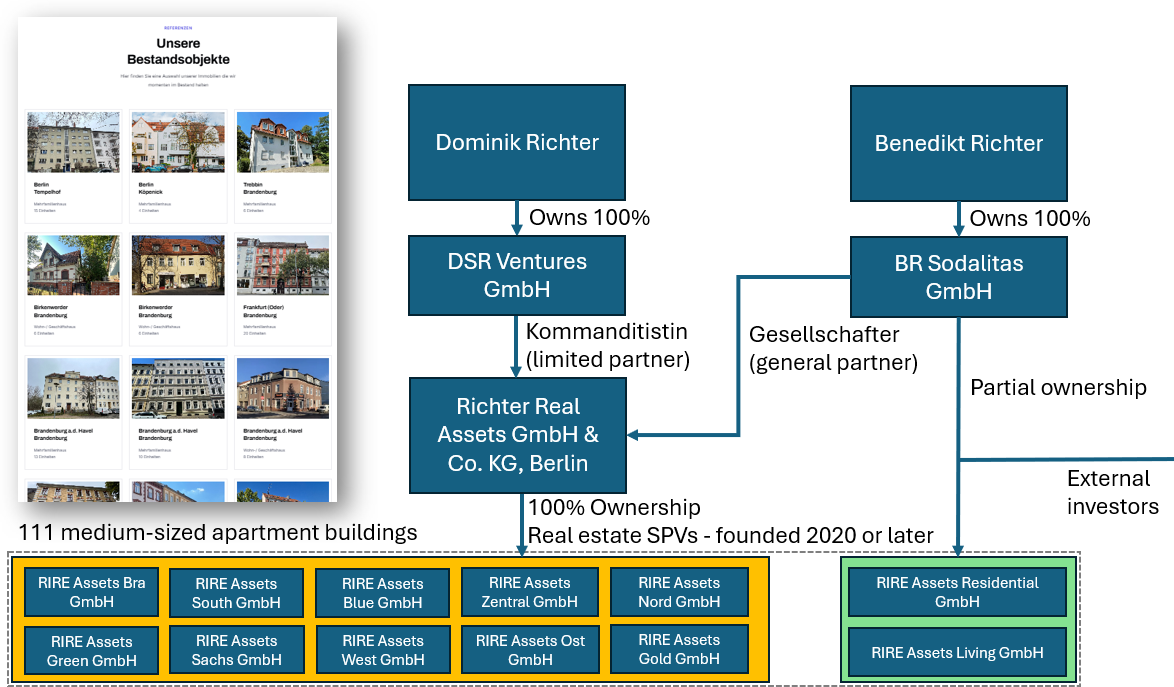

DSR Ventures serves as the primary financing partner, appearing as a limited partner in multiple entities within this real estate network. The portfolio includes 111 mid-sized apartment buildings, mostly low-income properties requiring renovation. The network’s website, launched in 2021 (per archive.org), names Benedikt Richter as owner but omits any mention of Dominik.

Source: Grizzly Research, Unternehmensregister.de

These investments are heavily leveraged. Consolidated balance sheets of the property-holding entities show €7.2 million in equity against €60.8 million in liabilities, an equity ratio of just 10.6%. Cash is fully committed to illiquid, over-levered assets. DSR Ventures’ 2023 balance sheet reports €32 million in financial assets (presumed to be HelloFresh shares) and €15 million in liabilities, implying a 50% loan-to-value ratio. Cash holdings are below €1 million, indicating nearly all borrowed funds have been deployed. Across the entire real estate group, cash balances are minimal, raising doubts about meeting working capital needs, let alone margin calls.

Source: Unternehmensregister.de

The Richter real estate structure appears severely cash-constrained. Holding illiquid assets while facing liquidity demands during a margin call creates a dangerous mismatch. This raises the question of how Dominik Richter and his entities continue to source shares for additional pledges. Additional details are in the Appendix.

For the few entities that Benedikt manages without Dominik’s investment, he pools funds from eleven other investment entities, indicating that he cannot finance such deals alone.

Shareholders Will Likely Suffer for the CEO’s Excessive Private Leverage

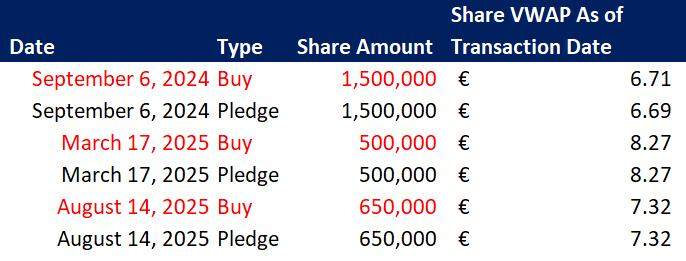

Dominik Richter appears to have exhausted his pledgeable shares at least three times. EQS filings reveal three instances where DSR Ventures purchased HelloFresh shares and immediately pledged the exact same amount.

Dominik Richter’s insider transactions (source: EQS News)

Dominik Richter appears to have exhausted his pledgeable shares at least three times. EQS filings reveal three instances where DSR Ventures purchased HelloFresh shares and immediately pledged the exact same amount. Only one purchase was on the open market via Xetra in August 2025, following dismal quarterly results and a sharp stock drop. The other two were off-market transactions. Combined, DSR Ventures spent approximately €19 million on these acquisitions. This raises serious red flags.

Where did the cash come from? We strongly suspect these were emergency responses to margin calls, each followed a significant share price decline and was paired with an immediate pledge. Margin calls are sudden and unforgiving. Yet the latest balance sheets of Richter-affiliated entities show less than €3 million in total cash across the entire network. Our calculations are in the Appendix.

Richter’s net worth is tied almost entirely to his HelloFresh shares and the DSR Ventures real estate portfolio. He has no other significant income source, no inherited wealth, and his only other notable venture, a SPAC, failed to close a deal.

We demand transparency. The filings claim cash purchases, but if DSR Ventures had €19 million readily available, why borrow against HelloFresh shares in the first place? With cash depleted and nearly all shares pledged, we fear HelloFresh is already misusing its share compensation system and buyback program to cover Richter’s margin calls. We call upon BaFin to scrutinize the situation.

Our concern is amplified by the compensation framework, which allows the Supervisory Board to adjust financial and non-financial performance targets during the fiscal year, creating dangerous latitude for abuse.

An Accelerating Buyback Program to Support the Falling Share Price and Avoid Margin Calls

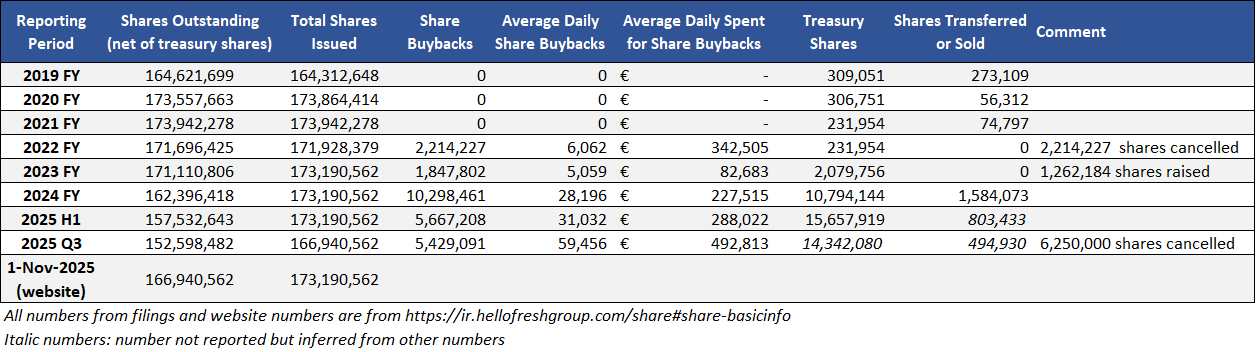

HelloFresh has run aggressive share buybacks since 2021, with programs repeatedly extended. Yet since early 2022, the stock has lost 90% of its value despite continuous repurchases.

The 2025 trend is particularly alarming. Despite buying back over 12.5 million shares for more than €100 million YTD, a sharp acceleration in pace, the share price has still fallen nearly 50%.

With CEO Dominik Richter likely having faced multiple margin calls on his pledged shares, he has a clear incentive to prevent further declines. Our analysis suggests the company is deploying its cash reserves to counter persistent selling pressure in a fundamentally deteriorating business. The fact that even this accelerated buyback program cannot halt the stock’s collapse while it drains cash reserves is deeply alarming.

The Chef Doesn’t Like His Own Menu

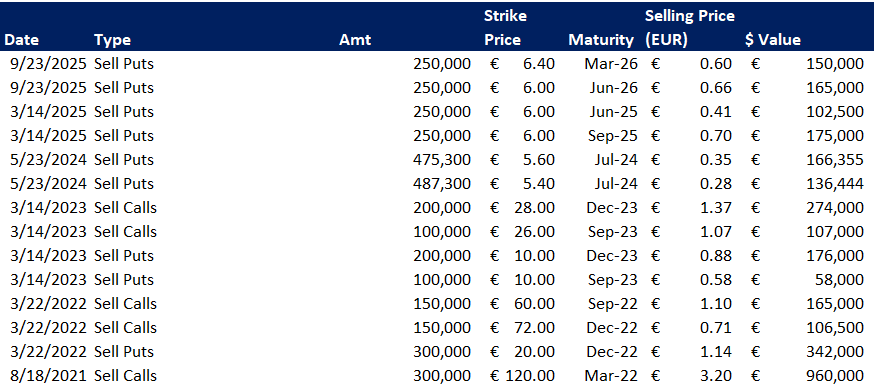

Thomas Griesel is Co-Founder of HelloFresh and CEO of CEO International. He has used his shares in HelloFresh differently to extract value. Griesel sold options on HelloFresh stock to collect the options premium. Most egregiously, Griesel has sold call options on HelloFresh on four different occasions, essentially betting that HelloFresh share price will not rise above a certain price.

This constitutes, in our opinion, an egregious conflict of interest. High level management has inside information and influence about the messaging. When a co-founder and board member actively wagers against upside in the company he leads, it demands regulatory scrutiny.

Griesel’s insider options transactions (source: EQS News)

Find his full insider transactions list in our Appendix.

HelloFresh recently announced that Griesel will not renew his Management Board mandate beyond April 30, 2026. CFO Christian Gärtner stepped down in October 2025. Against the backdrop of our findings, these exits appear to reflect a loss of confidence in the company’s future.

Misleading or Dysfunctional Website Information

HelloFresh’s investor relations site, ir.hellofreshgroup.com, projects a polished image but delivers inaccurate or broken information at critical points.

Under News > Director Dealings, the page lists insider transactions, including share pledges, but clicking any entry redirects to unrelated Ad Hoc releases. We verified this malfunction across multiple dates as of the writing of this report. The effect is to conceal details of sensitive dealings.

Link: ir.hellofreshgroup.com/financial-news#news-dd

Under Share > Basic Information, the site prominently states “Shares issued: 173,190,562” and “Shares outstanding (net of treasury shares): 166,940,562.” These figures contradict the latest official filings, which report 152,598,482 shares outstanding net of treasury—implying more than 14.3 million treasure shares and not the 6.25 million implied on the website. HelloFresh canceled 6.25 million treasury shares in July 2025, yet the website appears to misrepresent or confuse its own metrics.

While incompetence may explain some errors, the pattern consistently obscures data unfavorable to management. This raises questions about transparency.

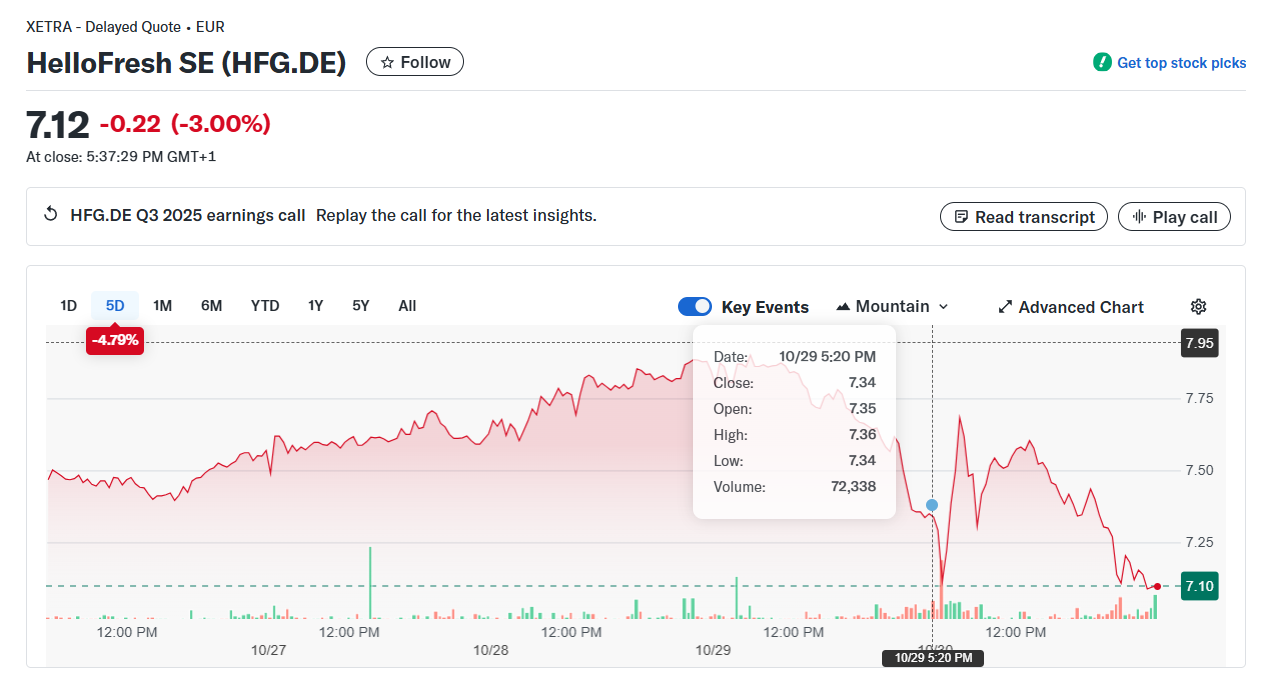

Spurious Intraday Trading Pattern Point to Illegal Insider Frontrunning

HelloFresh released its Q3 2025 earnings on October 30, 2025, before the Frankfurt market opened. The company reported a €–0.36 EPS, far below the €–0.06 consensus.

On the prior trading day (October 29), the stock fell 7.9% from 10:20 AM to the 5:30 PM close, while the MDAX dropped only 0.9%. The next morning, after the weak results hit, the stock initially plunged 4.0%, only to rebound sharply, closing 4.7% above the prior day’s finish on heavy volume.

The sequence is striking:

- Heavy selling in the final hours of October 29, before the public knew the numbers.

- Dismal earnings released pre-market on October 30.

- A brief sell-off, followed by aggressive buying at depressed levels.

This pattern suggests insiders with advanced knowledge of the poor results shorted the stock late on October 29 and covered aggressively the next morning.

Source: finance.yahoo.com/quote/HFG.F/

While definitive proof of insider trading is beyond our scope, the timing demand immediate scrutiny from BaFin.

Key Activist Investor, Active Ownership Capital, Has a Dismal Track Record

Luxembourg-based Active Ownership Capital (AOC) now holds 8% of HelloFresh, making it the largest shareholder. The fund has intensified pressure on management, demanding aggressive cost cuts and a supervisory board seat. Yet AOC’s European track record is deeply underwhelming.

Source: EQS News, corporate filings, news media

In nearly every prior campaign, AOC pushed for capital raises, board overhauls, or operational restructurings, only to see target companies underperform and shareholders disappointed. This pattern casts serious doubt on whether AOC’s HelloFresh intervention will create genuine value.

AOC markets itself as a disciplined value investor, but its campaigns have consistently coincided with cash-intensive turnarounds and negative returns. Detailed analysis of past AOC campaigns is in the Appendix.

Steeply Downwards Trending Customer Interest and Interaction

At the core of HelloFresh’s troubles is a business in fundamental decline.

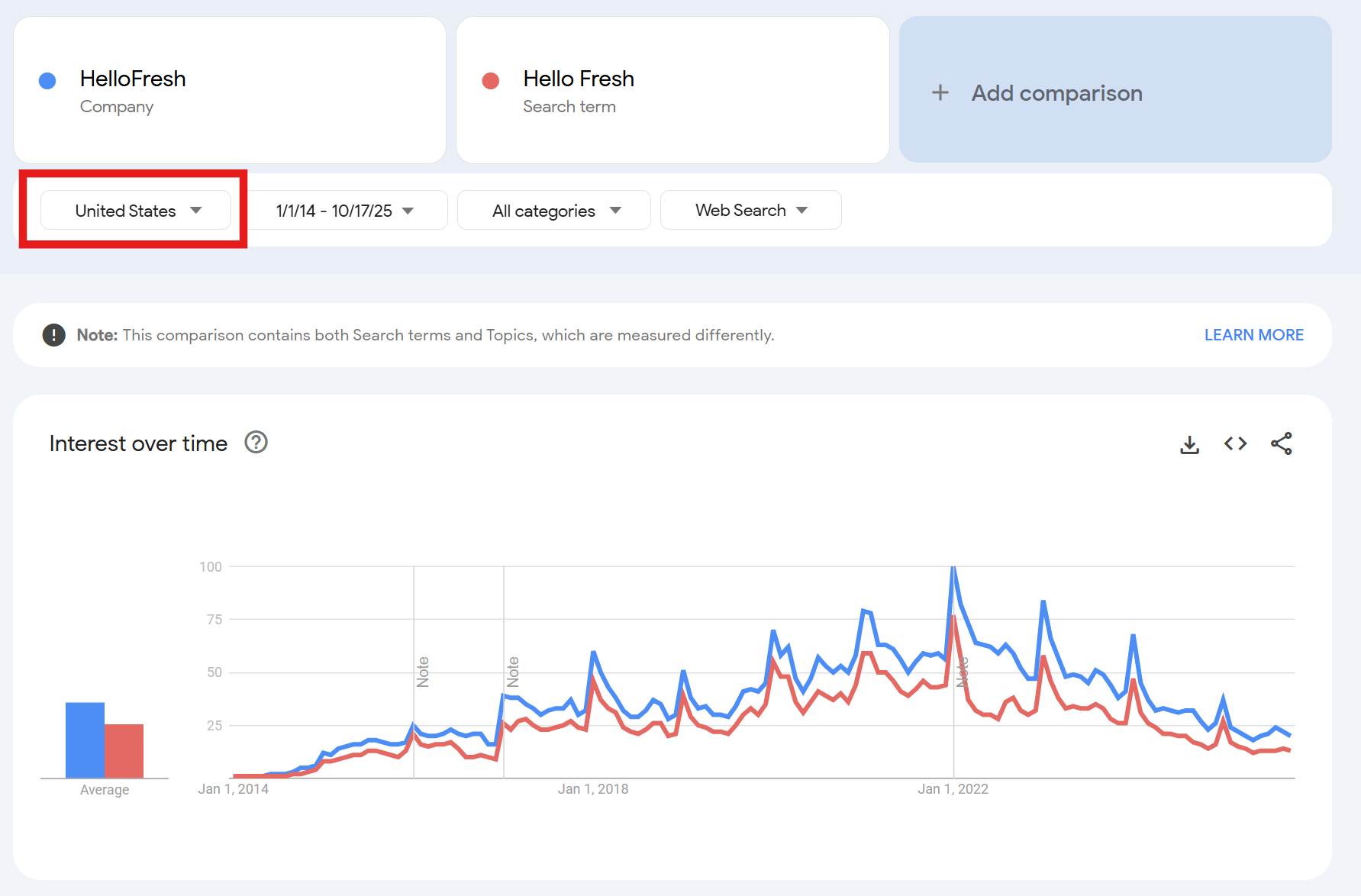

We analyzed independent, market-level data to assess the true health of the company. Roughly 50% of revenue comes from North America, where U.S. Google searches for HelloFresh have fallen to just 16% of their January 2022 peak, levels last seen in 2016.

Google Trends

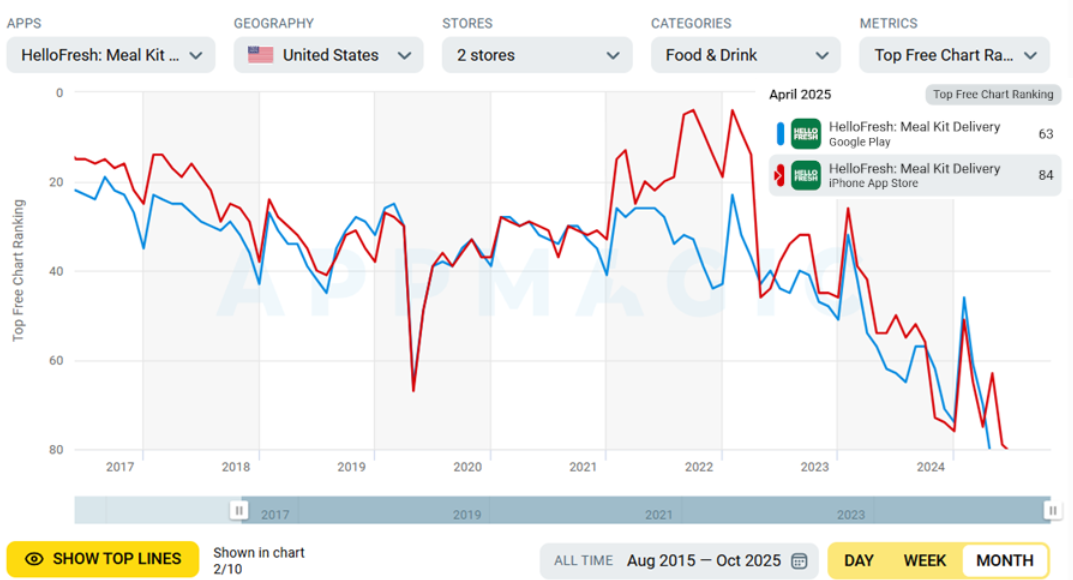

App downloads have also trended sharply lower since 2022 on both iOS and Android, with the HelloFresh app now outside the top 100 in the Food & Drink category.

AppMagic’s app download ranking

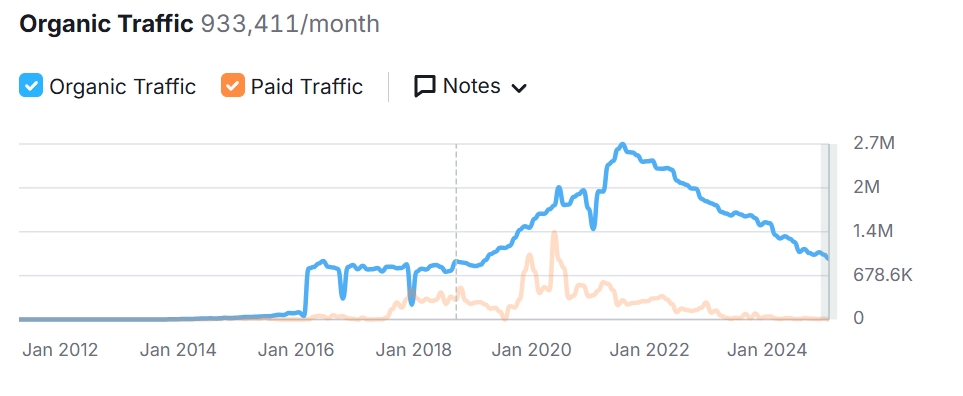

Organic U.S. website traffic to hellofresh.com has collapsed to pre-COVID levels.

SemRush.com: organic website traffic to hellofresh.com from U.S. users

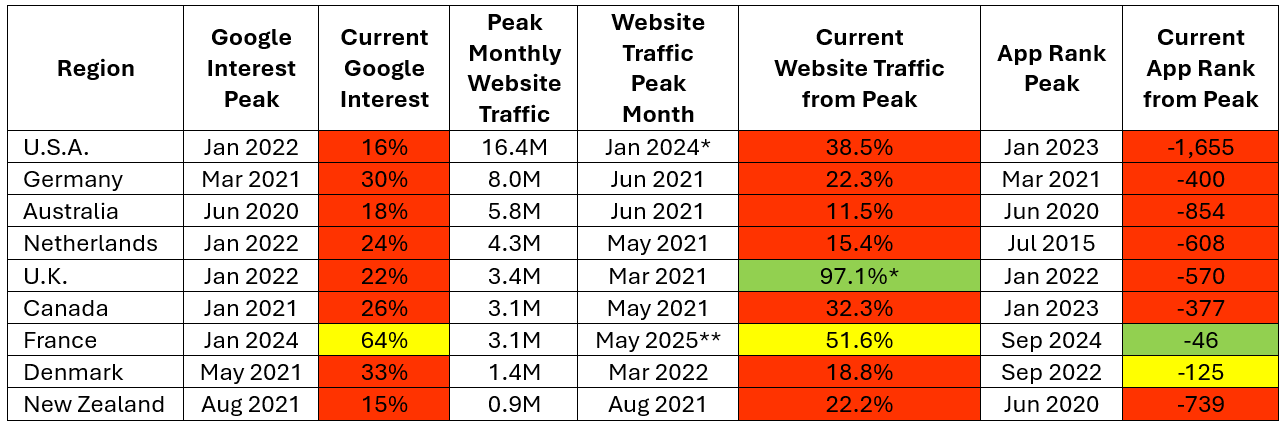

The same deterioration appears across all mature markets like Canada, Australia, Germany, the UK, and the Netherlands. Newer entries like France, Italy, and Spain saw brief spikes post-launch, but interest quickly faded. These expansions temporarily masked the core decline, nothing more.

We analyze the biggest markets by Google interest, panel website traffic, and total App rank.

*The data indicates aggressive click ad campaigns by HelloFresh in January 2024 in the U.S from June to September 2025 in the U.K. Controlled for this, U.S. traffic peaked in April 2021 at 15.1M, and U.K.’s May 2025 traffic is 47.1% from its peak. Find more details in the Appendix.

** HelloFresh focused on growth in the French market much later, from 2022 on. That is why French metrics still look healthy compared to more mature markets, where HelloFresh is already defeated and shrinking dramatically. Find more details in the Appendix.

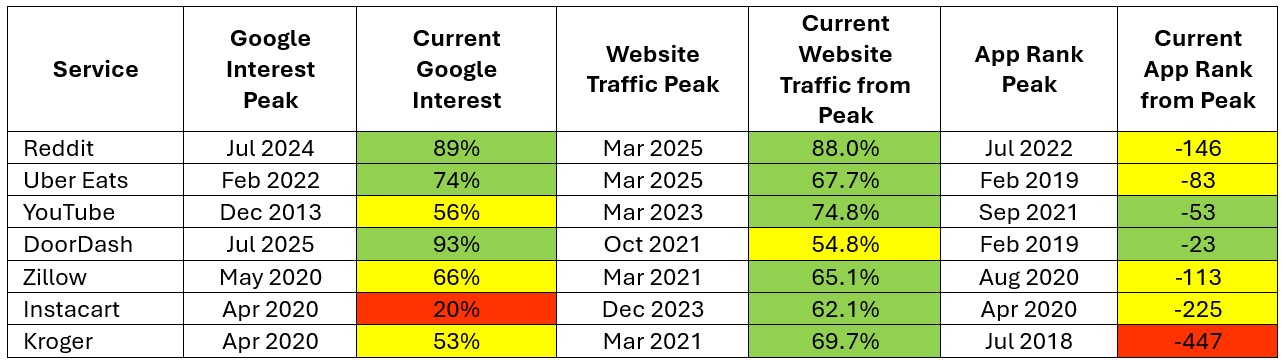

For comparison, here are the same data points for some other web-based services that are well-known or are in similar industry segments as HelloFresh. Note that many of these services received heightened interest during COVID lockdowns, as well.

(Data for U.S. market)

Across nearly every metric and market, HelloFresh is in rapid, structural decline. The brand is losing relevance at an accelerating pace. Each quarter is poised to be worse than the last.

More country-level data details are presented in the Appendix.

Our Third-Party KPIs for Customer Interest

We rely on independent, third-party KPIs to estimate customer engagement and forecast revenue trends for the coming quarters and years.

For HelloFresh, these leading indicators reveal steep, unaddressed declines that neither management nor investors have acknowledged.

To validate their predictive power, we measured the correlation between annual changes in these metrics and HelloFresh’s global revenue growth.

* Changes in annual averages of all KPIs are tested against HelloFresh’s annual revenue change

These indicators, particularly iPhone app rank and organic traffic, collectively explain nearly all of HelloFresh’s revenue trajectory during the COVID-to-2023 period. Their current collapse signals a structural, irreversible decline.

Why People are Leaving the Service – a Fundamentally Unfixable Business

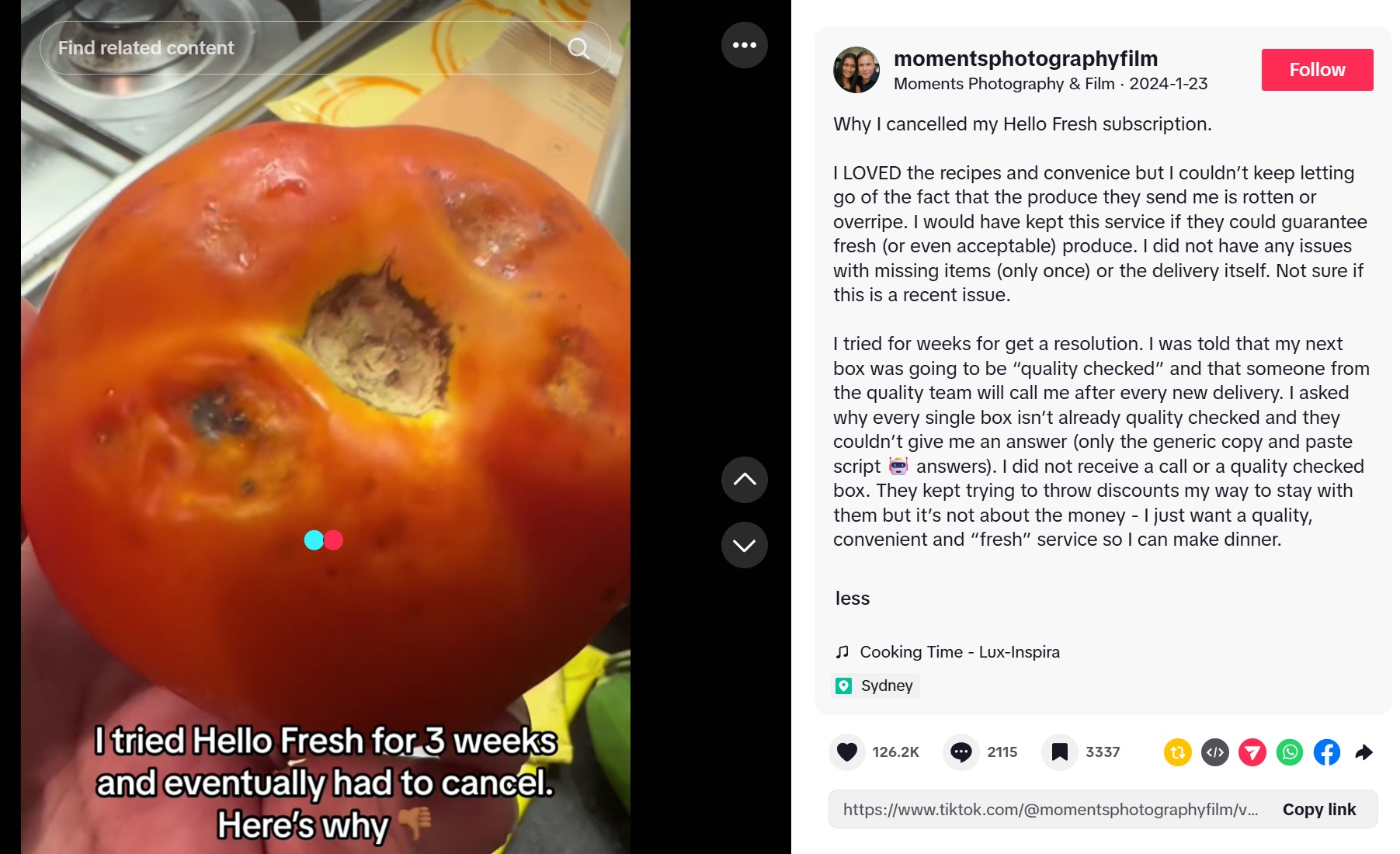

Delivery failures, spoiled ingredients, leaking packs, are common complaints. While logistics is complex, operational improvements could mitigate these issues.

A viral TikTok post with over 126 thousand likes describing that HelloFresh sends out spoiled food

However, more fundamentally concerning is the trend exemplified by comments by users under a YouTube video:

These are the customers HelloFresh wants to reach, and they are satisfied with the service but they simply don’t need continue after a short trial phase where many customers enjoy initial discounts. For many, the only value added by HelloFresh are the recipes of which every customer only needs a finite collection, and can be easily shared without subscriptions.

Pre-portioned boxes cost ~50% more than delivered supermarket groceries and even more versus in-store shopping. This premium is inherent to the added logistics layer and widely known (e.g., The Guardian, Reddit threads, viral YouTube clips). No amount of efficiency can close this gap.

Yet another issue for HelloFresh is the wasteful packaging from small ingredient unit sizes and cooler packs that stands in stark opposition to ecological trends of waste reduction. This is yet another problem that hurts the brand and seems fundamentally hard to solve in the business model.

Trash from one HelloFresh box. By @PlasticEveryday on X/Twitter

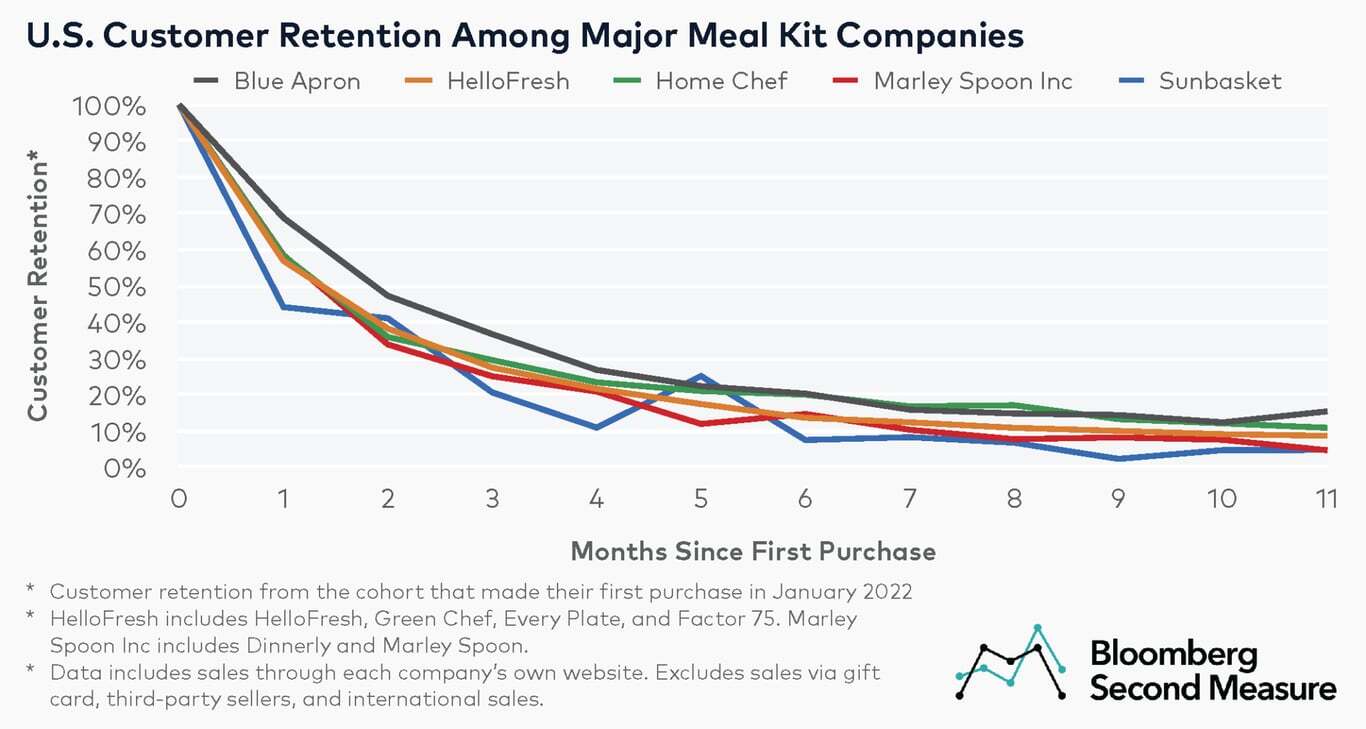

The result of these issues is an abysmal customer retention rate that renders the business model infeasible. A 2022 analysis revealed that customer retention for HelloFresh is only 9% over twelve months.

Today, HelloFresh avoids disclosing sufficient information to estimate customer retention.

The Last Industry Player to Fall

The collapse of the meal-kit sector is no secret. Once-hyped competitors have already imploded. HelloFresh is the final domino, a zombie company whose business model has already failed but clings to survival.

Prominent competitor Blue Apron Holdings Inc. went public on the NYSE under ticker “APRN” in 2017 but was in September 2023 acquired by Wonder Group for $103 million.

Marley Spoon Group SE went public in Frankfurt in January 2022 at €10 per share, and trades today at €0.29 (-99.7%).

Sunbasket and HomeChef (acquired by Kroger Co. in 2018 for $200m plus contingent premiums) are privately owned companies. The market is further saturated with struggling smaller companies, including BistroMD, Purple Carrot, Hungryroot or Thistle.

How HelloFresh’s Management Tries to Gloss Over the Issues

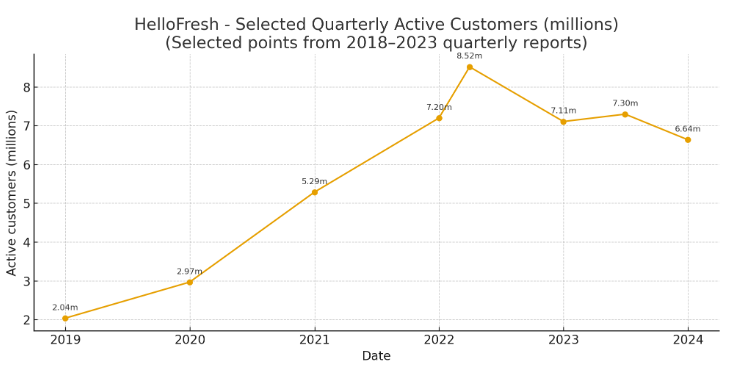

A failing company dreads transparency. HelloFresh has rolled out new metrics to obscure the core business collapse. In 2024, it quietly retired the long-standing Active Customers KPI, once the clearest gauge of demand, and pivoted to “high-value” customers and margin focus (see Q4 2024 earnings transcript). We view this as a direct response to catastrophic churn.

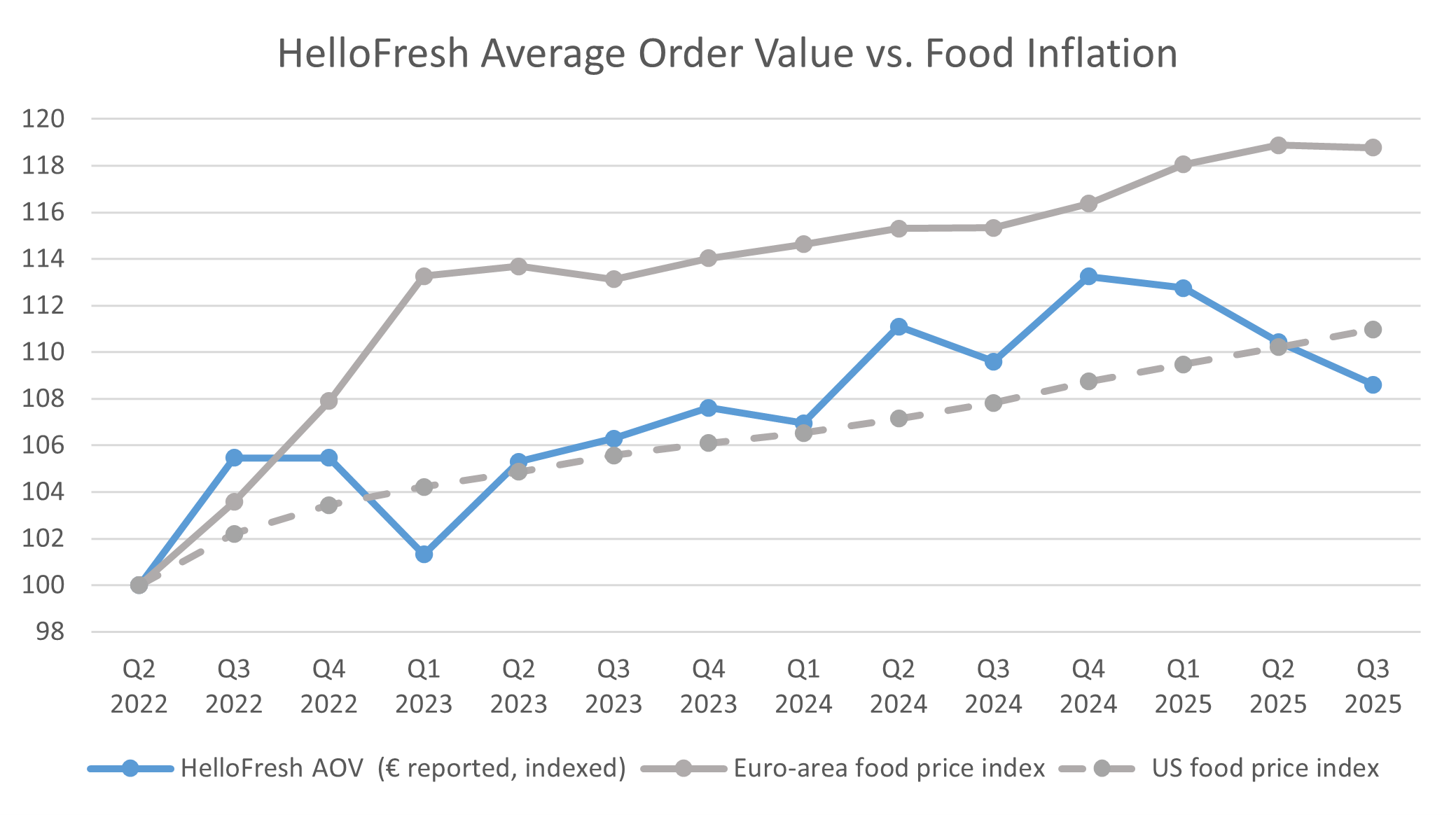

Since then, Average Order Value (AOV) has become the centerpiece of customer reporting. Yet, despite claims of shedding price-sensitive users, AOV growth has merely tracked food price inflation. We see no evidence of a successful “premium” shift.

Sources: HelloFresh filings, Eurostat, FRED

In Q4 2023 results they reiterated that the slight decline in orders/new customers was “more than offset by the continued expansion of AOV throughout the year.” This is an obvious mis-framing of overall increased food costs.

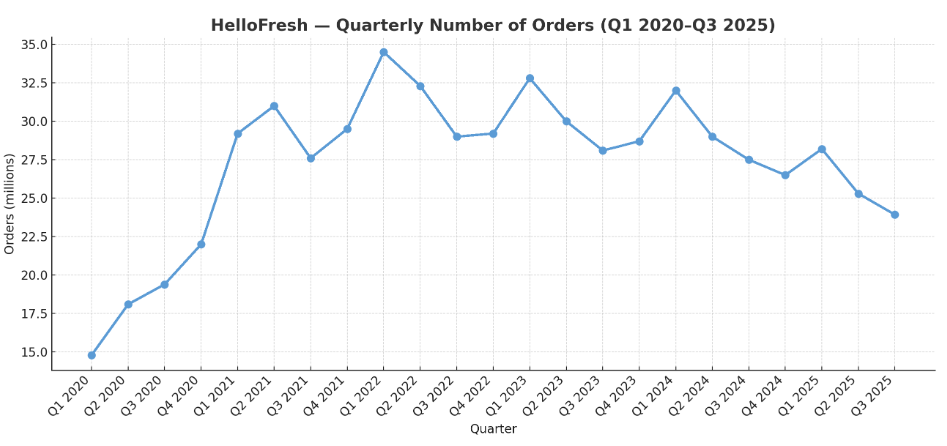

The total number of orders is, of course, also collapsing.

A Thousand Nasty Tricks Destroy the Brand

HelloFresh’s weak value proposition demands a robust brand and tight cost control to sustain the model. Yet aggressive marketing and cost cutting have backfired, with repeated legal violations and ethical lapses eroding trust. These incidents not only tarnish the reputation but expose desperate measures are needed to achieve subpar results.

The Child Labor Scandal

In December 2024, U.S. regulators launched a high-profile probe into alleged child labor violations at a HelloFresh facility in Aurora, Illinois, operated by its Factor75 subsidiary.

Migrant children were reportedly working in cooking and packaging as recently as summer 2024, prompting a securities fraud investigation. HelloFresh blamed staffing agency Midway Staffing and terminated the relationship, claiming zero tolerance for child labor.

But as the principal employer, the company bears responsibility for supply-chain compliance.

U.S. Regulators Trace E. Coli Infections in Multiple States to HelloFresh

In October 2022, the USDA’s Food Safety and Inspection Service (FSIS) investigated a multistate E. coli O157:H7 outbreak linked to ground beef in HelloFresh meal kits shipped July 2–21. Seven illnesses across six states led to six hospitalizations; no deaths were reported. E. coli risks stem from poor handling or contamination prevention, underscoring supply-chain vulnerabilities.

Union Clash and Site Closure in U.K.

In October 2024, HelloFresh announced the closure of its distribution center in Nuneaton, U.K., putting 900 jobs at risk. The decision followed protests just days earlier over the dismissal of 79 workers, which union bosses alleged were in retaliation for complaints about working conditions. A union spokesperson claimed HelloFresh had a “draconian approach to its workforce”, prevented workers from taking toilet breaks, and had dismissed workers “without following any sort of fair procedure.”

“Horrible Working Conditions” in California and Colorado

In 2021, workers at HelloFresh facilities in Richmond, California, and Aurora, Colorado, alleged unsafe conditions and an aggressive anti-union campaign. Injuries included crushed feet from 300-pound pallets and broken limbs; workers were forced to continue despite harm. Bathroom breaks were timed, with managers harassing employees. Low wages ($16/hour) left many needing second jobs.

Union drives failed amid these tactics.

Union Busting With False Information in Germany – Employees Sue

DW reported in 2022, that German HelloFresh employees in favor of starting a work council will take their case to Berlin’s labor court. Workers involved in the case say the meal-kit delivery service has spread misinformation and engaged in other union-busting tactics.

The Japan Failure and Delayed Information to Employees

In December 2022, HelloFresh announced to cease operations in Japan and filed for bankruptcy of its Japan subsidiary in the Tokyo District Court with a total debt of 3 billion yen (€16.9M). The company cited failure to drive reasonable return on investment as the reason for withdrawal.

Disgruntled employees complained that the Japanese team was only notified on the 20th December that they would lose their jobs on 31 December, without respecting the legal 30-day notice period. In a letter to employees, HelloFresh’s CEO admitted that there was no intention of notifying the press in advance. The company kept the failure of the Japanese business quiet for as long as possible.

Forced Monkey Labor Only Discontinued After 100k Complaints

PETA claims that from 2021 to 2023 HelloFresh sourced coconut milk from farms that practiced forced monkey labor. HelloFresh had previously denied its use of coconut milk tied to forced monkey labor, citing flimsy assurances from Thai coconut milk producers. PETA Asia has shown that the Thai government and coconut milk producers in Thailand can’t be trusted not to lie about abusing monkeys in coconut milk production. After nearly 100,000 e-mails from PETA supporters, HelloFresh has confirmed that it will remove Thai coconut milk products from its supply chain.

Empty Promises to Exploit Better Chicken Commitment Label

HelloFresh signed the Better Chicken Commitment in 2019 but faced 2022 protests outside its New York HQ for slow implementation of higher-welfare standards. Activists decried insufficient controls on faster-growing breeds and stocking densities.

Misleading “Climate Neutral” Labelling

In 2020, HelloFresh announced to become the “first global carbon-neutral meal kit company” by “offsetting 100% of its direct carbon emissions, making it the eco-friendly meal kit brand of choice.”

In 2023, the Berlin Regional Court ruled against HelloFresh following complaints about misleading marketing of “climate-neutral” meal kits. Berlin Regional Courts found offsets from forest projects unsubstantiated and disclosures inadequate.

Toxic Subscription Auto-Renewal and Cancellation Trickery

HelloFresh employs several strategies to prevent customers from successfully cancelling their subscription.

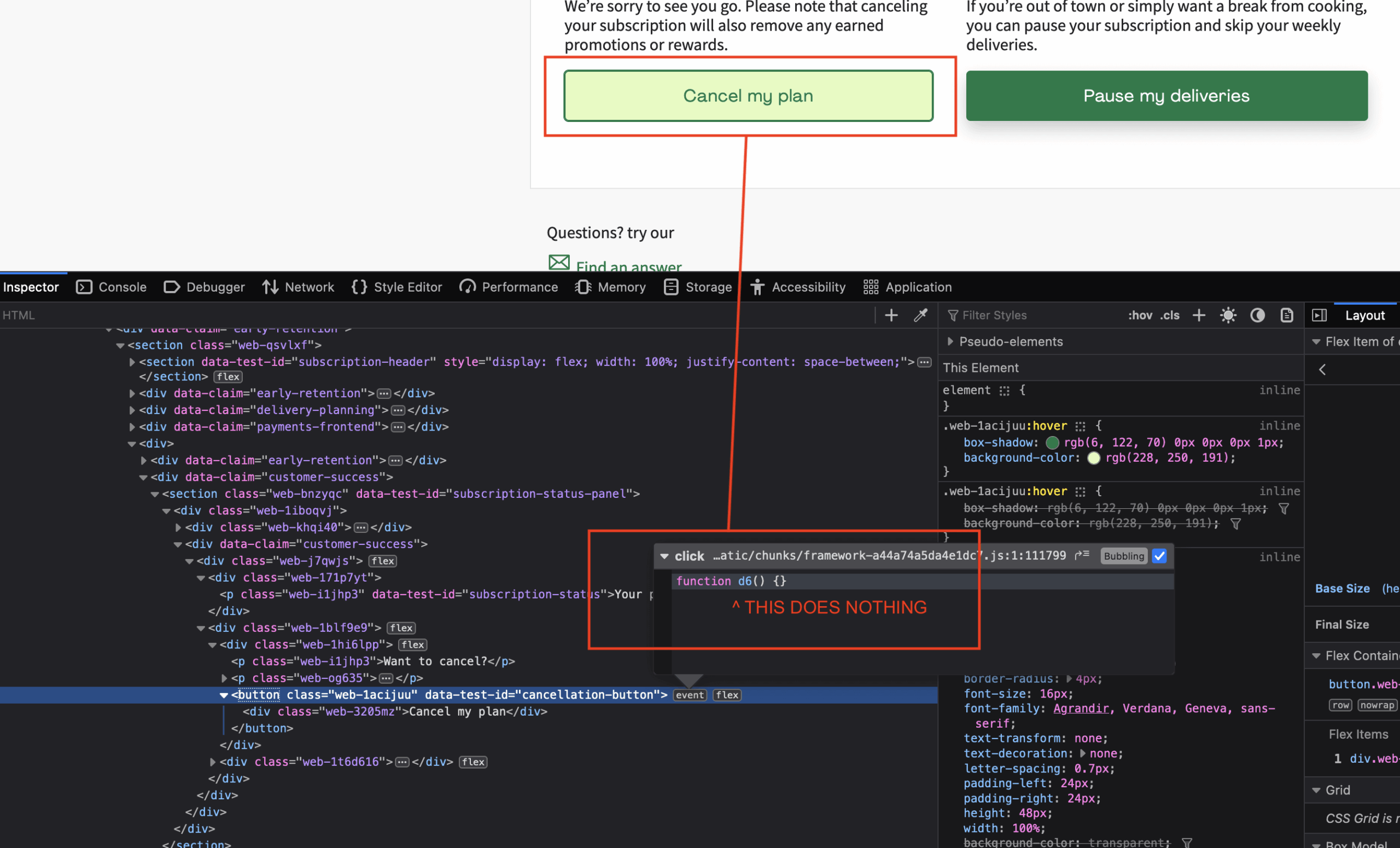

Dark Patterns, an expert journal on “dark patterns and unethical design examples on the internet” revealed in May 2024 that HelloFresh uses the so-called Roach Hotel method to make it hard for users to cancel their subscription by making it necessary to follow a complex multi-step process.

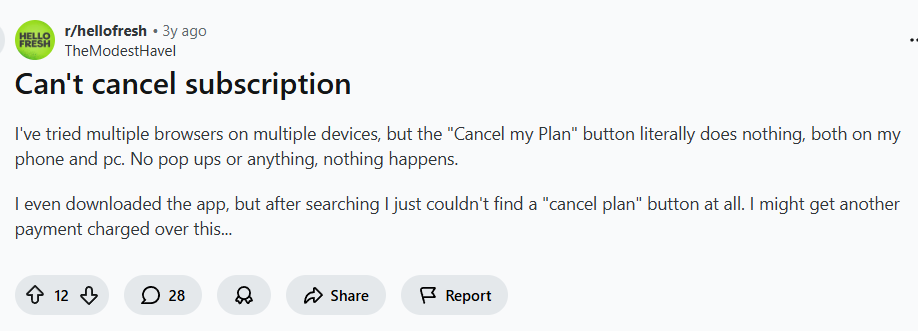

More concerning, at times, the cancellation button on the website refers to an empty function, a Reddit user claims.

Other users also complain that the cancel button does not work.

Not only anecdotal evidence supports our claim of toxic cancellation evasion tactics but also rulings by authorities.

In August 2025 HelloFresh paid US$7.5 million in a settlement due to a complaint by the Los Angeles County District Attorney’s Consumer Protection Division about misleading “dark pattern” marketing, failure to obtain affirmative consent for auto-renewals, and inadequate cancellation processes.

In January 2023, New Zealands consumer protection agency “Consumer NZ has issued a warning to customers of HelloFresh to check their bills as many continue to get charged for meal-kits they have opted to skip. Consumer NZ head of content Caitlin Cherry said the issue has been ongoing for more than three years.”

Many users complain about the impossibility of cancelling subscription or unwanted sudden autorenewals. (e.g. [1],[2],[3],[4],[5],[6],[7])

Illegal Ad Spam via E-Mail, SMS and Phone

In January 2024, HelloFresh has been fined £140,000 in the U.K. for sending 79 millions of spam emails and texts to customers over a seven-month campaign. 14 customer complaints were made directly to the Information Commissioner’s Office, and another 8,729 were made to the 7726 spam message reporting service.

In 2021, the U.S. District Court for Massachusetts approved a $14 million settlement in a national class action lawsuit against HelloFresh for illegal automated telemarketing that affected 4,831,285 individuals who were called on their cell phones or to numbers that were registered on the national or HelloFresh’s do-not-call list.

Skimming on Portions

One dirty trick HelloFresh uses to cut costs is to deliver small portions for meals. The issue has become worse recently. Here is a good example from Twitter/X (also, see this Reddit thread with 297 comments) that exemplifies the mounting customer complaints.

Source: X/Twitter

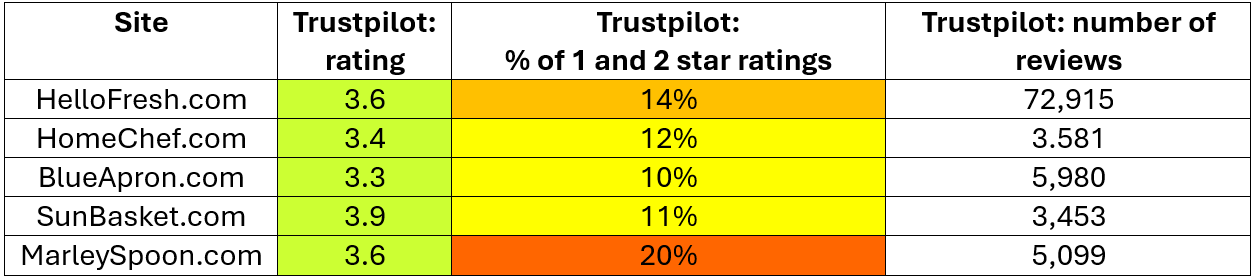

Customers Are Unsatisfied (Bad Review Statistics)

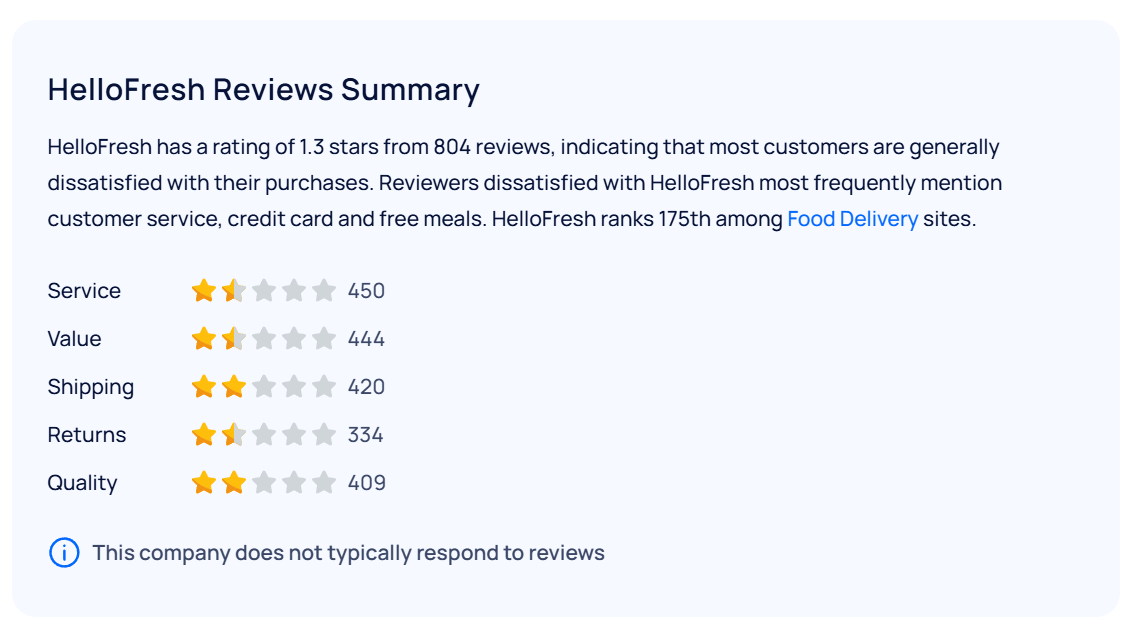

Customer review sites are only reliable if they have statistically significant amounts of reviews. We analyzed HelloFresh reviews on the two sites that have at least hundreds of reviews for HelloFresh.com, which are SiteJabber and Trustpilot.

On SiteJabber, we find that HelloFresh is one of the worse brands in its segment in terms of customer perception. HelloFresh ranks only 175th among food delivery sites due to terrible overall review scores of 1.3 of 5 on average.

Source: sitejabber.com/reviews/hellofresh.com

Data retrieved on October 28, 2025

Most meal kit brands have a similar average review score on Trustpilot. However, we found a high proportion of highly negative reviews for only two brands, Marley Spoon and HelloFresh.

Data retrieved on October 28, 2025

Systematic Order Replacement

Several Reddit users claim that HelloFresh routinely changes their orders on the backend without the users’ consent and HelloFresh claims this is a “known technical issue”.

Pivot Into Overcrowded, Low-Margin Markets

The recognition that HelloFresh’s core business model and brand face significant challenges prompted management to explore alternative strategies. However, our analysis indicates that the company’s diversification efforts and ventures into new business areas have yielded unfavorable to highly unfavorable outcomes.

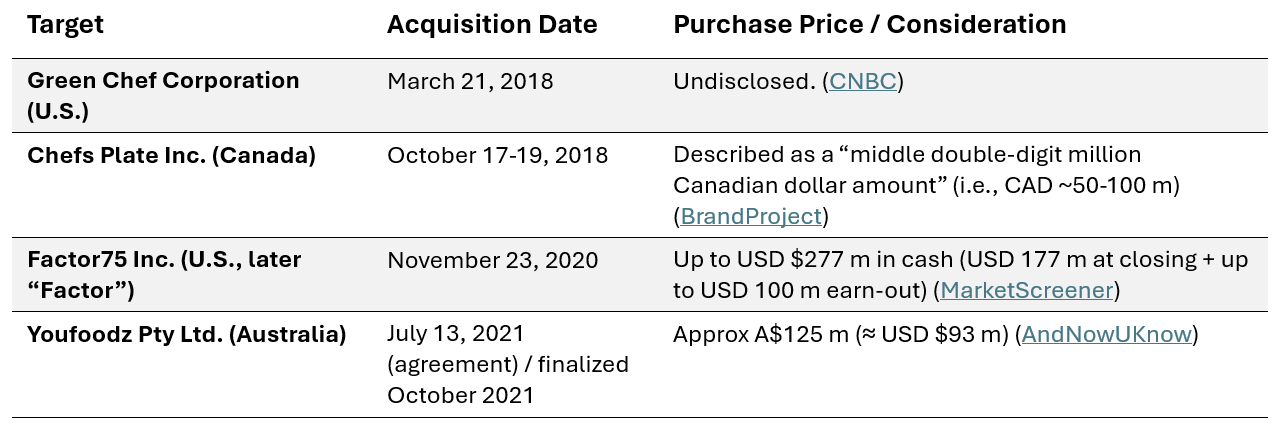

In December 2020, HelloFresh acquired Factor75 (and renamed it to “Factor” but kept the domain). In contrast to HelloFresh’s meal-kits for home cooking, Factor sells Ready-to-Eat (RTE), i.e. microwaveable, food online. Due to the more direct competition with supermarket food, RTE’s have razor slim margins. According to HelloFresh’s own “Adjusted EBITDA“, RTE margins were only 1.6% in 2024.

HelloFresh paid roughly €187 million for Factor of which €160 million (a whopping 85.6% of the total price) had to be booked as goodwill. HelloFresh’s U.S. CEO Uwe Voss promised: “Direct-to-consumer ready-to-eat meals are a nascent food vertical that we believe has the potential to grow into a multi-billion-dollar category over time.”

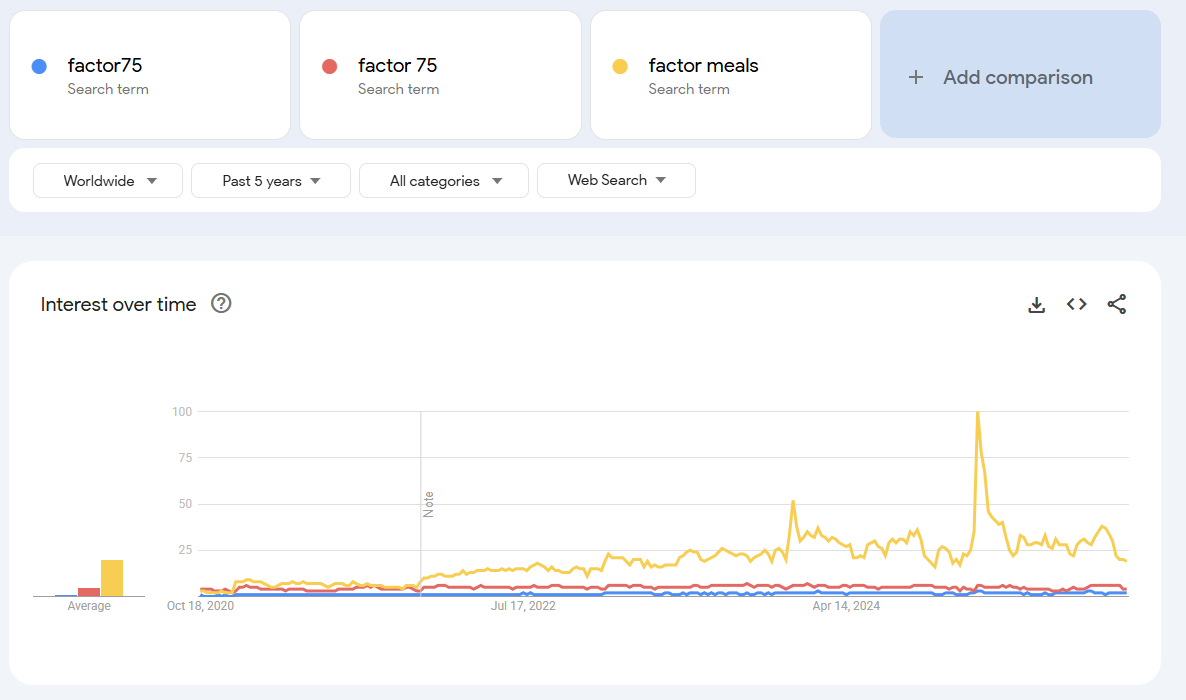

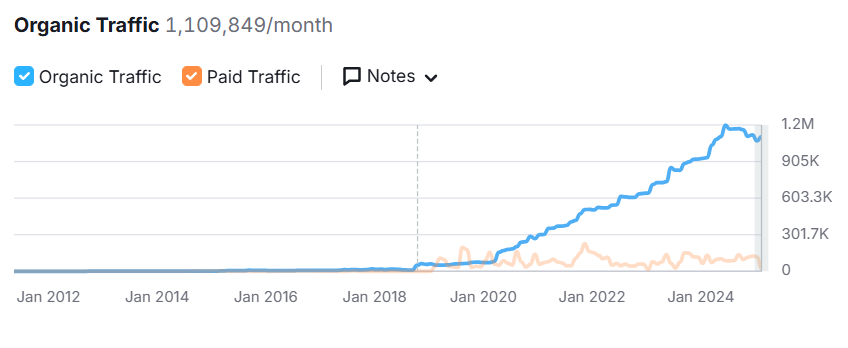

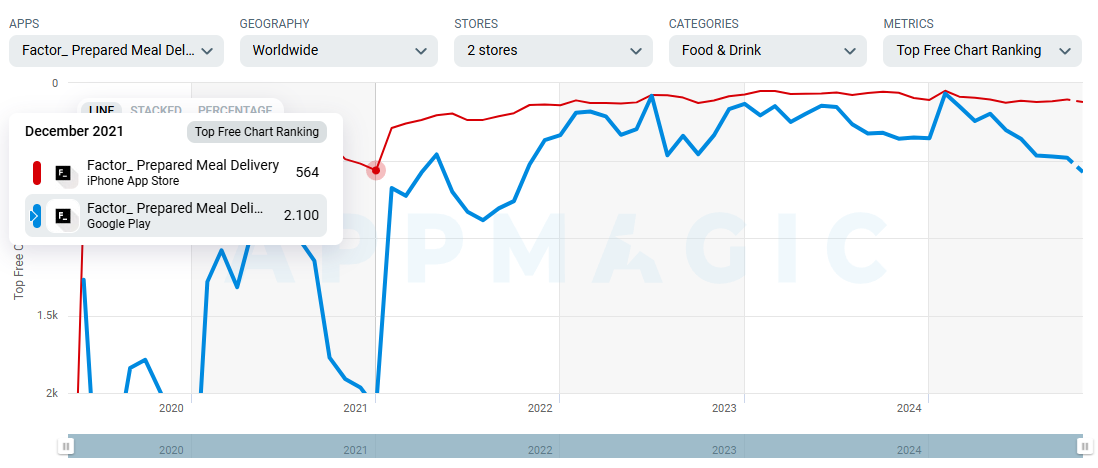

HelloFresh managed to grow the Factor business until February 2025 through aggressive advertising (especially through YouTuber sponsorships). The business is not growing anymore despite the hypercompetitive pricing.

Google Trends

SemRush.com: website traffic to factor75.com (peak in February 2025)

AppMagic

Besides Factor, HelloFresh acquired three other brands.

Additionally, HelloFresh bolstered its offering with EverPlate, which is a value-brand for meal kits launched by HelloFresh in 2018.

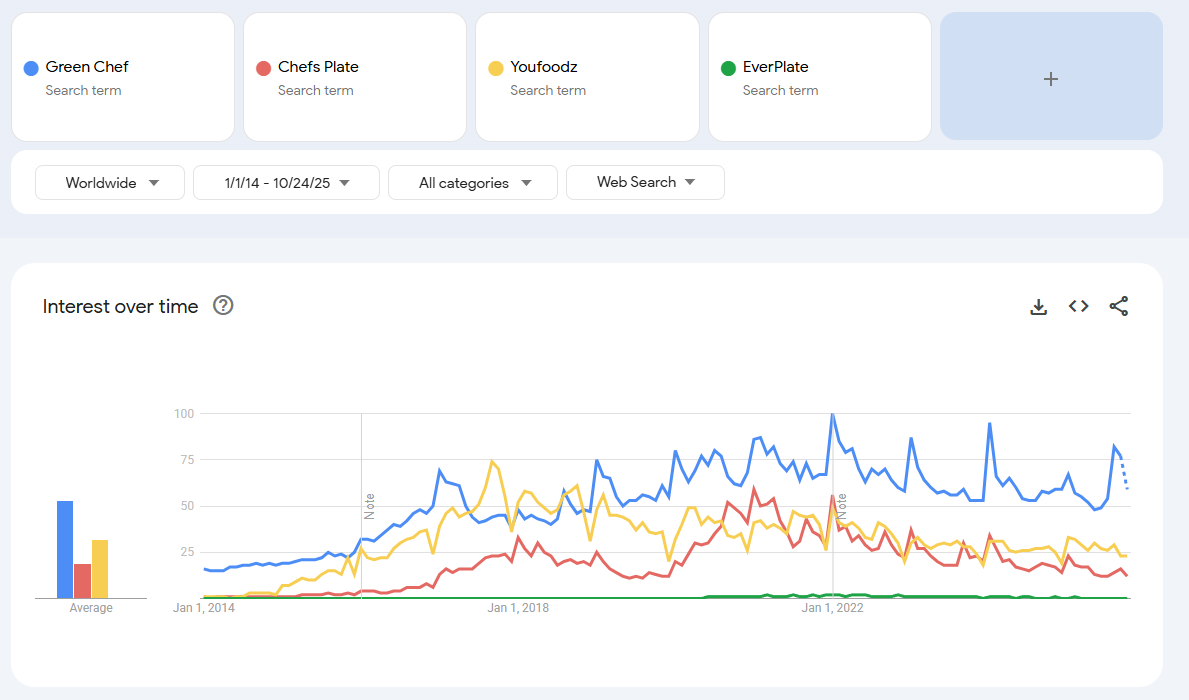

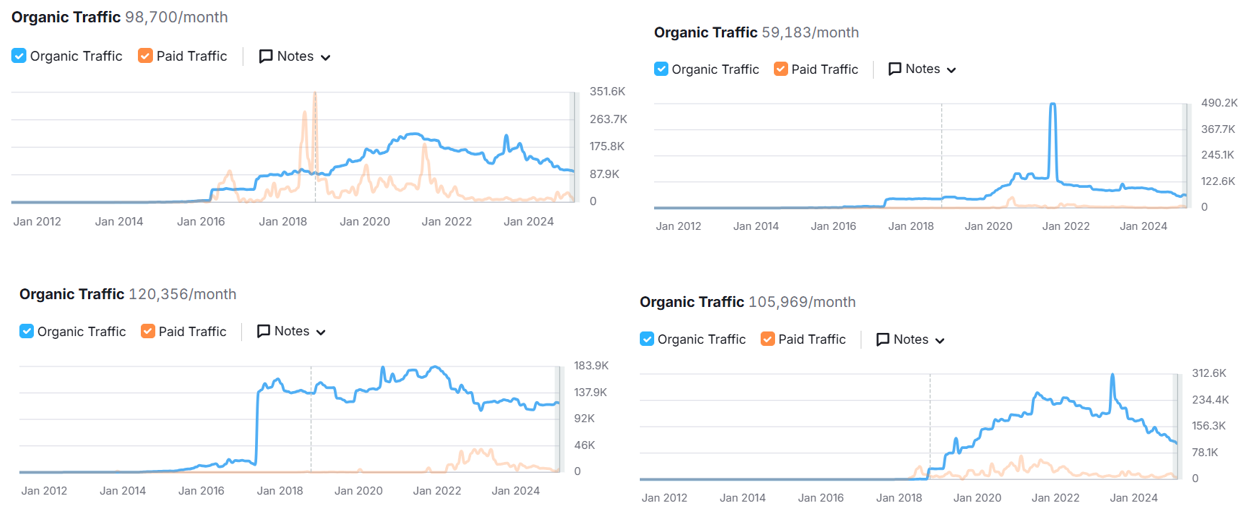

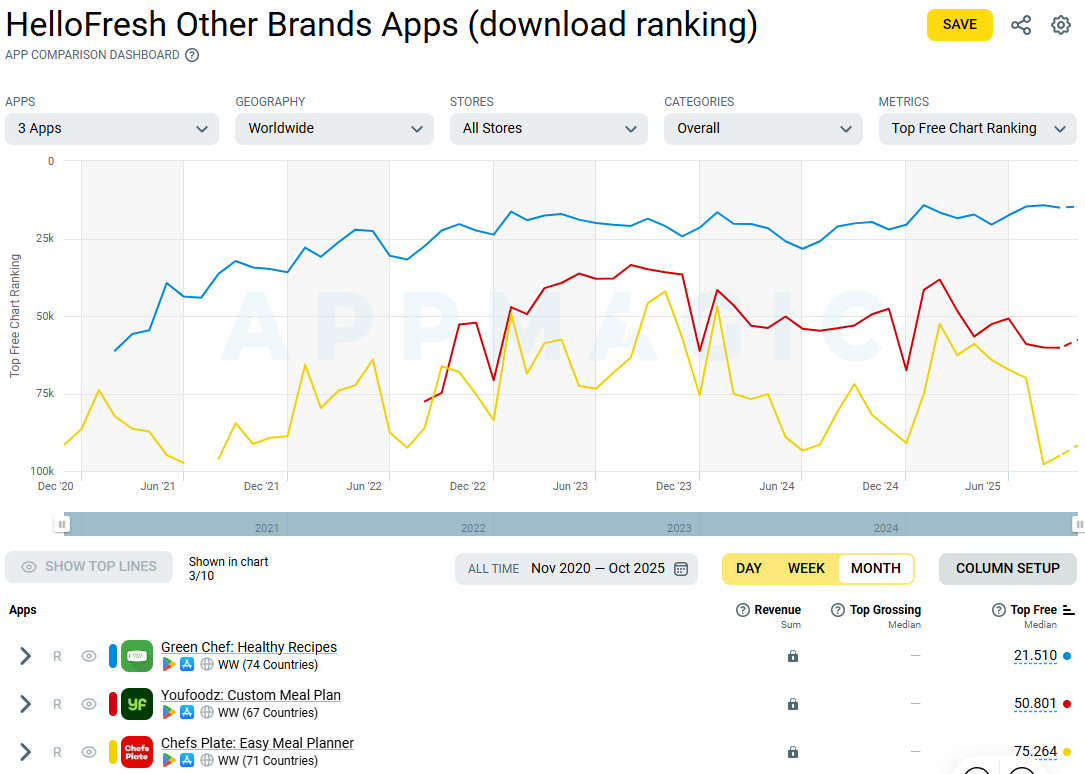

All these brands that HelloFresh owns are shrinking since 2022.

SemRush.com: website traffic to top-left: Greenchef.com, top-right: Chefsplate.com, bottom-left: YouFoodz.com, bottom-right: Everplate.com

AppMagic.com

Given the lack of meaningful profitability or growth throughout this brand portfolio, the remaining goodwill of €257.5M on HelloFresh’s balance sheet appears excessive.

Undeterred, management teased further pivots in the Q4 2024 earnings call: expansions into pet food, premium butchery, and health supplements. These are saturated, low-margin spaces dominated by incumbents, offering scant hope for a turnaround.

MDAX Exclusion

HelloFresh is currently a constituent of the German MDAX index. The stock enjoys benefits accordingly.

The main variable for the German index in/exclusion for HelloFresh is the market capitalization.

HelloFresh currently trades at around €1B, which makes it one of the very smallest of the 50 MDAX constituents by market cap. The smaller index the SDAX, includes about 30 companies of which more than 15 have currently a larger market cap than HelloFresh. Thus, we expect that one of the SDAX companies will officially replace HelloFresh in the MDAX in the next index review announcement on December 3, 2025 with effective date on December 22nd.

Conclusion

HelloFresh is a company in terminal decline. Its core meal-kit business structurally broken, its brand irreparably damaged, and its leadership fully complicit in a pattern of self-enrichment at shareholders’ expense.

The evidence is overwhelming: demand collapsing across every mature market, third-party KPIs flashing red, customer retention in single digits, and a portfolio of failed pivots into overcrowded, low-margin segments. Management’s response, KPI manipulation and accelerated buybacks, only accelerate the collapse.

CEO Dominik Richter’s private leverage game now threatens a forced liquidation that could crater the stock with just a 23% further drop. We are highly concerned about how Dominik Richter previously acquired shares that he immediately pledged, given that his private business empire seems severely cash constrained.

Co-founder Thomas Griesel’s call-option sales, alongside CFO turnover and seeming insider frontrunning patterns, complete a picture of a management team that has lost faith in its own story. A notable article about HelloFresh describes a deeply toxic corporate culture during the start-up days. We think it has not gotten better since.

A litany of ethical failures, child labor probes, union busting, E. coli outbreaks, dark-pattern subscriptions, and misleading climate claims, has left HelloFresh with a 1.3/5 customer rating and a reputation beyond repair. The meal-kit sector is dead. Blue Apron, Marley Spoon, and others have already been obliterated. HelloFresh is the last domino. We expect MDAX removal in December 2025, a likely goodwill impairment in 2026, barring radical intervention, a path toward insolvency or forced sale.

Shareholders are not invested in a turnaround. They are funding the executives’ exit.

Appendix

Find the appendix to this report under grizzlyreports.com/hfgappendix/