Since the publication of our critical report about ZTO Express Inc (ZTO), the company and banks have come out to defend the stock and keep up an appearance of credibility. Unfortunately, the Chairman of ZTO admitted in its latest conference indirectly to several of our accusations. This might be widely unknown to US investors since the CFO did not translate fully the Chairman’s important comments.

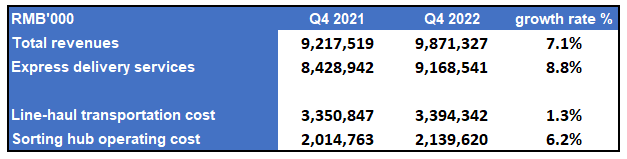

It appears to us ZTO’s Chairman admitted on its Q4 2022 earnings conference call that ZTO and its related companies are sharing transportation costs, sorting hub operating costs, and labor costs. In other words, we feel confirmed that ZTO has been offloading costs to its related companies to report higher margins. The table below shows that transportation costs and sorting hub operating costs are two of the main costs associated with ZTO’s express delivery business. In Q4 2022 ZTO’s revenues from the express delivery services grew 8.8%, but its transportation costs and sorting hub operating costs only grew 1.3% and 6.2%, respectively. This is one of the main reasons ZTO reported much higher net income growth than revenue growth.

As we illustrated in our previous report, we believe ZTO’s reported financials lack integrity because of the many disclosed and undisclosed related parties that are used to shift costs at will. ZTO’s Chairman’s statement at its earnings conference shed more light on the margin issue. The quote below is from the Q4 2022 earnings call recording starting at 51:16. ZTO’s Chairman was answering a question related to its logistics park. The Chairman stated in detail (in Mandarin) how ZTO Express, ZTO Freight, and ZTO Cloud Warehouse were intertwined with each other. Be reminded ZTO Freight and ZTO Cloud Warehouse are both disclosed related parties to ZTO.

中通过去几年确实我们也获取了一些土地的资源,我们建了很多分部中心。以前呢我们建分部中心主要是给快递用的,那我们现在呢,更像物流园区,里面有快递,有快运,有冷链,有仓,就把资源效率最大化。我们认为拓展生态呢,主要是做好两件事情,第一个就是协同,第二个把资源用好。我们以前,我举个例子,就是我们以前建的这个分部场地是两层楼,一层下面分拣,二层安装智能化设备。现在有很多的中心是六层,三四五六就是给云仓用。这有什么好处呢,零距离发货,成本更低,这个三家企业更好,就是它,晚上七点八点十点下班,也能够发出去,这个用户体验更好,能够提前一个频次,或者有些提前一天到。第三个呢,成本更低,我们的园区都是在工业园区里面的,中国其实我们一线的员工,指所有的啊,打工的人,都希望能够赚到更多的钱,有些呢可以做三份工。就是我们大部分这个仓里面都是制件工制,或者是小时工制,干一个小时30块钱25块钱,其他的工人而且是长期的每年就是每天都有的干,可以增加员工的收入。那我们如果这个仓在外面呢,就会固定会养很多工人,比如说【语音不清晰】就会养个一两百个工人,其实就干了两三小时的活,它要付一天的工资。比如说我们这个园区里面,有快运,有快递,因为是同向的,如果是半车货,它就可以拼车。也会节省一些成本。包括这个办公场所啊,设施啊,比如说食堂可以共用一个。我们认为,未来就在资源利用上面,中通拓展生态方面呢,我们把资源用好。这个就是竞争力。谢谢。

Translation [Paraphrase]

ZTO acquired some land resources in the past few years, and we built many branch centers. Previously we mainly built these centers for express delivery, but now it’s more like logistics parks, within which there are express delivery, freight, cold-chain logistics, and warehouse. That is to maximize resource efficiency. We believe in order to expand the ecosystem, there are two things to be done: first, it’s cooperation, and second good use of resources. We previously, I am giving an example, built this kind of branch facility with 2 floors. The first floor is used for sorting, and the second floor is to install smart equipment. Now many centers have 6 floors, within which the 3rd, 4th, 5th, and 6th floors are given to Yuncang (note: Yuncang here means ZTO Cloud Warehouse Technology Co., Ltd. and its subsidiaries, an equity investee company disclosed in ZTO’s annual report). What’s the benefit of doing this? Zero distance to send out delivery, and the cost is lower. These three companies are better. That is, [workers] can get off work at 7pm, 8pm, or 10pm, [the delivery] can still be sent out. This customer experience is better because it can speed up and some delivery can arrive one day earlier. The third point, the cost is lower. Our parks are all in the industrial parks, and our workers all hope to make more money. Some of them can work for 3 jobs. Most of our warehouses are hourly pay, it’s about 25 or 30 RMB per hour. Workers can work every day, and this can increase workers’ income. But if our warehouse is outside, then we will have to hire more workers. For example, [not clear in the audio] will need to hire 100-200 workers. They may only work 2 to 3 hours a day, but we will still need to pay them for a whole day’s worth of salary. For example, in our parks, there is freight express (note: freight express here means ZTO Supply Chain Management Co., Ltd. and its subsidiaries, an equity investee company disclosed in ZTO’s annual report), express delivery, because they are in the same direction, so if the delivery goods are only half of the truck, then we can truck-pool. This will also save some cost. Also for the administrative offices, and facilities, for example, all workers can use the same company-restaurant. We believe ZTO needs to use the resources well in terms of expanding the eco-system. This is the competitive advantage. Thank you.

There are several implications to the Chairman’s comments.

1. Potentially Under-reported Transportation Costs

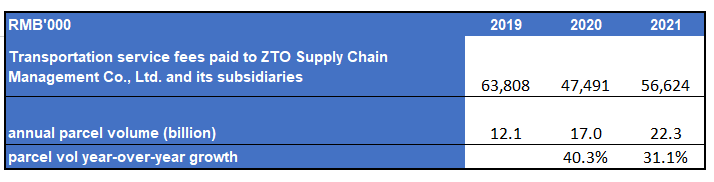

In its Annual Report’s related party transaction section, ZTO disclosed the transportation service fees that ZTO paid to ZTO Freight, it was RMB 63.8 million, RMB 47.5 million, and 56.6 million in 2019, 2020, and 2021, respectively. We will know more information on how much was transacted in 2022 once ZTO releases its full 2022 Annual Report.

As ZTO’s Chairman stated, when a delivery truck is not full, ZTO and ZTO Freight share one truck to conduct delivery services. However, after viewing the annual parcel volume that ZTO reported and the transportation service fees ZTO paid to ZTO Freight, we find it highly likely ZTO is under-reporting the transportation cost. For example, in 2020 and 2021, ZTO’s reported annual parcel volume grew 40.3% and 31.1%, respectively, whereas the transportation service fees ZTO paid to ZTO Freight in 2021 (RMB56.6 million) is even less than the transportation service fees in 2019 (RMB 63.8 million). The real question investors should ask is, is it only truck-pooling between ZTO and ZTO Freight, or is it possible that ZTO is using ZTO Freight, at least partially, to conduct express delivery services so that ZTO does not have to include the associated costs in its financials? We believe it is highly possible the latter is also the case.

Be reminded, ZTO introduced ZTO Supply Chain Management Co., Ltd. (“ZTO LTL”) in its Annual Report as follows:

ZTO LTL

On August 22, 2016, the Company entered into an investment agreement with ZTO LTL and Mr. Jianfa Lai to invest cash of RMB54,000 in exchange of 18% ordinary shares in ZTO LTL. ZTO LTL is engaged in provision of less-than-truckload transportation services in China. The principal shareholders of ZTO LTL are also the principal shareholders of the Company. Owing to the shareholders’ structure of ZTO LTL, the Company has significant influence over ZTO LTL’s operating activities. Therefore, the investment is accounted for using the equity method. In August 2017, the Company increased investment in ZTO LTL by RMB36,000 to maintain its equity interest in ZTO LTL at 18%. In 2018, ZTO LTL went through a restructuring and as a result, became a wholly owned subsidiary of ZTO Freight (Cayman) Inc. (“ZTO Freight”), a newly established Cayman company by shareholders of ZTO LTL. The Company held 18% equity in ZTO Freight after the restructuring.

2. Employees Working for Three Companies (ZTO, ZTO Freight, ZTO Cloud Warehouse) at the Same Time

ZTO’s Chairman stated on the call that some workers will have 3 jobs for these 3 companies, namely ZTO, ZTO Freight, and ZTO Cloud Warehouse. The worker’s hourly salary is RMB 25-30. He also stated that if these companies are further away from each other, then they would need to hire more workers. Our question is when ZTO counts its full-time employees and outsourced employees, do they count the employees working not only for ZTO but also for ZTO Freight and ZTO Cloud Warehouse, or does ZTO exclude these employees in their annual report? Who is paying how much of the salary for such employees?

Considering that ZTO has significant influence over its related companies, we wouldn’t be surprised if ZTO offloaded labor costs to ZTO Freight and ZTO Cloud Warehouse.

3. Potentially Under-reported Sorting Hub Operating Cost

There are two points regarding this issue.

First of all, the Chairman gave an example on the earnings call that originally the branch centers ZTO built only had 2 floors and ZTO used both of the floors for its sorting business. However, many branch centers that ZTO built now have 6 floors, the first 2 floors are still being used for sorting and installing smart equipment, but the building’s 3rd, 4th, 5th, and 6th floors are given to ZTO Cloud Warehouse.

It is not clear what the Chairman exactly meant when he stated that these floors are “given” to ZTO Cloud Warehouse. However, we want to remind investors that the largest shareholder (24.5%) of ZTO Cloud Warehouse is a company called Zhejiang Zhongjun Investment Management Co., Ltd (Chinese name: 浙江仲君投资管理有限公司, ”Zhejiang Zhongjun”) whose majority shareholder (57.5%) is ZTO’s Chairman Meisong Lai himself. ZTO only owns 16.36% of ZTO Cloud Warehouse.

How many buildings that ZTO claimed to have built were partially given to ZTO Cloud Warehouse? When ZTO uses ZTO Cloud Warehouse for its delivery business, does ZTO Cloud Warehouse charge any fees? We saw ZTO disclosed that ZTO Freight would charge transportation service fees from ZTO, although we believe that fees are unreasonably low. However, we did not see any fees or costs that ZTO Cloud Warehouse charged from ZTO. Investors deserve more clarity on how this relationship exactly works.

Secondly, ZTO stated in its Q4 2022 earnings release that:

Number of sorting hubs was 98 as of December 31, 2022, among which 87 are operated by the Company and 11 by the Company’s network partners.

If ZTO wants to be transparent, it should disclose the names of these network partners that are operating ZTO’s 11 sorting hubs. As we illustrated in the original report, we found that at least certain network partners are owned or controlled by ZTO’s employees/shareholders.

The Independent Committee and Sell-Side Response are a Charade

On March 9th, 2023, ZTO announced that its audit committee decided to conduct an independent investigation into our report’s allegations. We want to note that we do not have a lot of trust in the independent committee. This is to us likely nothing more than a PR show.

Sell-side analysts came out in defense of ZTO after our report was published. While they failed to address most key allegations, even those allegations that were addressed had at best flimsy remarks.

Analysts applaud ZTO for increasing its market share, but this comes admittedly with a reduction in price per unit. How then did ZTO still manage to improve margins and consistently have better margins than peers? That just does not make sense. In addition, the unit cost argument from these sell-side analysts fails to address the real issue: we allege the company’s margins are too high because the company offloads its costs to off-balance sheet entities. Their counterargument about unit costs fails to address the key issue.

We also specifically pointed out that from 2020 to 2021 ZTO almost doubled investment in CAPEX while the zero-covid policy was in place in China. General points about CAPEX requirements to expand a network fail to address this glaring anomaly.

In Conclusion, we still stand by our research and believe the company has failed to address any of the real issues we pointed out in our original report.