READ OUR DISCLAIMER HERE

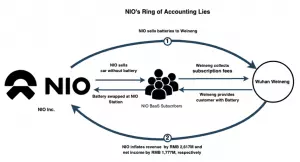

- Today, we reveal what we consider an audacious scheme by NYSE-listed NIO. Reminiscent of the Philidor-Valeant relationship, NIO is likely using an unconsolidated related party to exaggerate revenue and profitability.

- Presumably, with these stellar operating results in mind, retail investors have bid NIO’s shares up >450% since 2020, making it one of China’s most valuable EV companies.

- Allow us to introduce you to Wuhan Weineng (“Weineng”), the convenient difference-maker helping NIO exceed lofty growth and profitability estimates on The Street. Despite being formed by NIO and a consortium of investors in late 2020, this unconsolidated related party has already generated billions in revenue for NIO.

- While this rapid growth is impressive on the surface, our investigation has found Weineng might be to NIO what Philidor was to Valeant. Just as Philidor aided Valeant in habitually making numbers, NIO has curiously exceeded estimates since establishing Weineng.

- We believe sales to Weineng have inflated NIO’s revenue and net income by ~10% and 95%, respectively. Specifically, we find that at least 60% of its FY2021 earnings beat seems attributable to Weineng.

- By transferring the burden of collecting monthly subscriptions to Weineng, NIO has accelerated its revenue growth. Instead of recognizing revenue over the life of the subscription (~7 years), Weineng allows NIO to recognize revenue from the batteries they sell immediately. Through this arrangement, we think NIO has juiced its numbers by pulling forward 7 years of revenue.

- Considering Weineng’s recent disclosure of 19,000 battery subscriptions, we questioned why Weineng held 40,053 batteries as inventory on September 30, 2021. After careful investigation, we believe NIO flooded Weineng with up to extra 21,053 batteries (worth ~1,147M RMB) to boost its numbers. For Q4 2021, this number only gets worse and we estimate NIO oversupplied up to another 15,200 batteries. The effect of this action on NIO’s bottom line is enormous.

- Of course, it would take a willing potential accomplice to pull off such a scheme… While NIO represents limited control over Weineng, we identified notable conflicts of interest between the two parties: Weineng’s top two executives currently double as NIO’s Vice President and Battery Operating Executive Manager.

- NIO’s Chairman and CEO, Bin Li, is closely tied to Joy Capital and Erhai Liu, parties central to the Luckin Coffee Fraud. While he has been hailed as the “Elon Musk of China”, Li’s past ventures have seen their stocks collapse and been taken private at a fraction of their peak valuations.

- In January 2019, Bin Li transferred 50M shares to the “NIO Users Trust”, an opaque BVI entity purportedly established to provide NIO Users with more influence over the Company’s governance. In an apparent violation of these “Users” trust, Li pledged these shares to UBS to secure a personal loan. With NIO’s stock declining 50+% since the pledge, we believe shareholders are unknowingly exposed to the risk of a margin call against the Users Trust shares.

- Chinese government entities have redeemed US$2B from NIO and may collect another US$6.7B. With NIO’s cash balance of just US$8.2B. We believe shareholders risk being materially diluted in future periods.

Introduction

NIO went public in September 2018 and has been touted as one of the most disruptive EV companies in China.

Two of NIO’s key differentiators have been its investments in its Battery Swap System and Battery as a Service (BaaS) segments. These investments have garnered tremendous hype among investors and EV enthusiasts as NIO is the only major Chinese EV company funding such initiatives, setting it apart from competitors. As of June 2022, NIO had completed over 7.6 million battery swaps and deployed over 981 battery swap stations, with this number slated to grow to 1,300 stations by the end of 2022.

We have discovered that NIO has used Wuhan Weineng, an unconsolidated related party entity, to inflate its revenues and boost margins. By selling batteries far in excess of Weineng’s requirements, we estimate NIO’s net loss should be 95% higher for the 9 months ended September 2021.

Our research also revealed hidden and opaque share agreements which benefit the Chinese government at the expense of public shareholders, as well as previous affiliations and failed ventures of NIO’s CEO, Bin Li.

This scheme reminds us of a certain high-flying pharmaceutical company that took Wall Street by storm before eventually being exposed for using related parties to manipulate its financials.

NIO’s Philidor Moment: NIO is Pulling Forward Revenue and Manipulating Costs to Boost Margins

NIO has been using an unconsolidated, related party subsidiary to engineer its financials and consistently beat Wall Street targets in a scheme reminiscent of that which was used between Valeant and Philidor. For the nine months ended September 2021, NIO has inflated its revenue and net income by ~10% and 95%, respectively.

Source: Grizzly Research

In August 2020, Wuhan Weineng Battery Asset Co. Ltd (“Weineng Battery” thereafter, Chinese name: 武汉蔚能电池资产有限公司) was formed by NIO and a consortium of government entities and private investors like CATL. NIO holds a 19.8% stake in Weineng and accounts for the company using the equity method of accounting:

“In August 2020, the Group and three other third-party investors jointly established the Battery Asset Company. The Group invested RMB200,000 in the Battery Asset Company and held 25% of the Battery Asset Company’s equity interests. In December 2020, the Battery Asset Company entered into an agreement with the other third-party investors for a total additional investment of RMB640,000 by those investors. In 2021, the Group further invested RMB270,000 in the Battery Asset Company and upon the consummation of the investment, the Group owns approximately 19.8% equity interests of the Battery Asset Company. The Group, as a major shareholder of the Battery Asset Company, is entitled to appoint one out of nine directors in the Battery Asset Company’s board of directors and can exercise significant influence over the Battery Asset Company. Therefore, the investment in the Battery Asset Company is accounted for using the equity method of accounting.”

Since Q4 2020, NIO has surprised net income expectations by an average of 33% while beating top-line estimates by an average of 5%. For FY2021 the Street expected NIO to lose 5,947 million. Instead, NIO posted a net loss of 3,007 million RMB, an amount that was 50% higher than expectations(a difference of 2,940 million RMB). Due to a lack of regularity in Weineng’s financial reporting, we can only infer the true effect of the financial engineering between the two companies for the 9 months ended September 2021. From these figures, however, we can see Weineng was crucial to this upside surprise in earnings.

Battery Swapping

NIO owns and operates battery swapping stations across China where its vehicle owners can exchange their batteries for new and fully-charged battery packs in just a few minutes. This initiative has historically had mixed results because of its flawed economics.

In 2008, a start-up called Better Place launched the initiative in Israel. After spending $850M on capital expenditures, Better Place filed for bankruptcy in 2013. Tesla presented a similar idea in 2013 but completely abandoned the plan due to marketing, technical and financial reasons.

Despite this history, NIO has mysteriously taken a misfit business and transformed it into a promising one and a key factor in investors’ bull case. Since Q4 2020, the company has quickly scaled from just 172 stations to over 981 stations. What is NIO’s secret sauce?

Battery as a Service (BaaS)

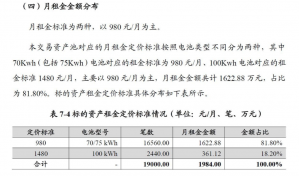

Building upon its Battery Swapping business, NIO introduced “Battery-as-a-Service” to give customers the option to purchase a car without the battery. This structure lowers the total price of the car by at least 70,000 RMB and is supposed to improve EV adoption. Through the program, users can then lease the battery from the BaaS provider, paying 980 RMB-1,480 RMB per month or 11,760 RMB-17,680 RMB annually, depending on the capacity of the batteries rented.

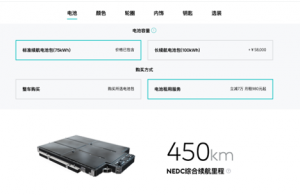

Below are screenshots from the NIO app which show the reduction in the upfront price and subscription pricing when users opt to rent using BaaS. Our conversation with the salesperson in NIO’s EV center also confirmed these two monthly rental prices under the 70/75kWh battery and 100kWh battery selection, respectively.

Source: NIO App

Given the synergies between Battery Swapping and BaaS, we were puzzled to see NIO spin off the BaaS business as an unconsolidated entity where they have to share economics with other investors. However, after a deeper investigation, the answer appears clear. NIO spun-off Wuhan Weineng to help artificially boost its battery swapping business and overall performance.

According to NIO’s filings, Weineng is the entity that owns the batteries used in the BaaS business and is responsible for managing the subscriptions. Thus, when a user subscribes to the BaaS program, Weineng is the recipient of all subscription payments. Where does Weineng get the batteries it provides? None other than NIO…

“Under the BaaS, we sell a battery to Wuhan Weineng Battery Asset Co., Ltd., or the Battery Asset Company, and the user subscribes for the usage of the battery from the Battery Asset Company.“

Since Weineng Battery was formed in August 2020, NIO has found it to be a reliable and growing stream of revenue. In just four months of operating in 2020, NIO generated 290 million RMB from sales to Weineng. Despite this quick start, revenue attributable to the entity ballooned even further in 2021 to 4.14 billion RMB representing ~11% of overall 2021 revenue.

The arrangement between Weineng and NIO has helped them in three ways:

- Pulling forward several years of revenue to help meet ambitious estimates

- Providing a willing counterparty to sell more batteries than their required network needs

- Shifting depreciation costs off their financial statements

Never Stop Pulling: How NIO is Pulling Forward Future Revenues Using Wuhan Weineng

If Weineng did not exist, NIO would have to recognize subscription revenue from customers over the lifetime of their subscription. Luckily for NIO, they don’t have to wait… Consider a 70K RMB sale. Normally it would take NIO approximately 7 years (inflation-adjusted) to generate the full subscription revenue, but with Weineng, they can recognize the revenue immediately.

In other words, NIO can pull forward approximately 7 years of recurring revenue and recognize it immediately to artificially boost revenue growth without incurring any additional costs.

We were able to retrieve Weineng Battery’s prospectus for an Asset-Backed Financing which revealed key information about its subscriptions. As of September 30, 2021, 19,000 users are serviced under the BaaS service agreement, 18% of which are subscribed to the 100kWh battery BaaS service and 82% to the 70-75kWh battery.

Source: Weineng’s ABN Prospectus

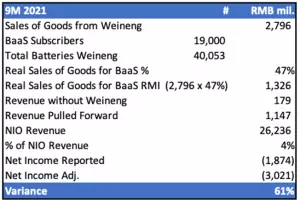

Using these numbers, we can determine what NIO’s financials would look like if Weineng did not exist. Contrary to the 2,796 million RMB in revenue reported, NIO would have received roughly 19.84 million RMB per month, or approximately 179 million RMB for the 9 months ending 2021 (~239 million RMB annualized for 2021).

Although Weineng never filed any updates to their 2021 Q3 numbers, the analysis in this report is still very relevant and valid. As of today, NIO is still offering BaaS to its consumers, and Weineng continues to operate as an unconsolidated entity.

Below is a screenshot of NIO’s current offering.

Source: NIO

Through the Weineng scheme, NIO has pulled forward over 1.147 billion RMB in revenue resulting in an equal improvement in reported earnings. We estimate NIO’s true net income for the period to be a loss of 3.02 billion RMB.

The following chart shows how we derived these figures, with a few conditions:

- As we will show, we believe only the 19,000 batteries corresponding to Weineng’s 19,000 service users can be considered real Instead, Weineng holds total batteries more than double this number. We will deal with these surplus batteries in the next section and show readers why we believe NIO has been further inflating revenue by overselling batteries to this counterparty.

- We define revenue that has been “pulled-forward” as any revenue beyond what NIO would have received in the first year of subscriptions had it consolidated Weineng as a subsidiary.

- NIO has grown the top-line absent the incremental costs that would be associated with real revenue. This is because regardless of the arrangement, NIO would have paid and bought batteries to operate its BaaS business. Thus these financial costs are already baked into NIO’s financials.

Source: company filings, Grizzly analysis

The arrangement with Weineng helped NIO inflate its revenue for 9 months ending September 2021 by almost 4%. which directly flowed into its bottom line; NIO’s adjusted net loss should be ~61% larger than the reported figure.

In the next section, we show how NIO took advantage of this scheme to sell batteries in excess of what is required by the BaaS business and inflate revenue.

How NIO has been Oversupplying Wuhan Weineng

We believe NIO intentionally oversupplied Weineng with batteries. By calculating the battery requirements of the BaaS network, we show the quantities supplied by NIO far exceed justifiable amounts.

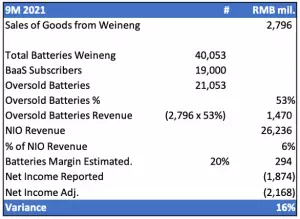

According to the Weineng Battery’s ABN Prospectus, up to September 2021, Weineng had 40,053 batteries.

“截至2020年末及 2021年 9月末, 武汉蔚能 持有 BaaS电池资产数量 分别为4,115块和 40,053块,业务规模明显增长。”

Translation:

“As of year-end 2020 and 9 months ending Sep 2021, Wuhan Weineng possesses 4,115 and 40,053 batteries respectively. The operation is rapidly growing.”

– Source: Weineng Battery ABN Prospectus

Recall there were only 19,000 users who had subscribed to the BaaS program as of September 30, 2021, implying an excess of 21,053 batteries. Assuming the same 20-80 mix between 75kwh and 100kwh batteries, we can deduce that inundating Weineng with batteries helped NIO report 1.47 billion RMB in additional revenue and 294 million RMB in additional net income. The below chart shows the math behind this conclusion.

One of the key assumptions embedded in our analysis is that the battery margins are approximately 20%. We believe this is a conservative estimate as it is consistent with the margin of an entire vehicle and batteries are a cost center for all vehicles.

Source: company filings, Grizzly analysis

While we do not have inventory numbers from Weineng beyond September 2021, we can show that NIO continued this scheme into Q4 2021. Dividing NIO’s Weineng sales of 2,796M RMB over 40,053 batteries gives us an average selling price of ~70K RMB. We also know that for FY2021, NIO sold 4,138M RMB for the full year, implying revenue of 1,342M RMB for Q4 2021.

Using our average selling price, this would imply that in Q4 2021, NIO sold another ~19,000 batteries to Weineng, further increasing its battery inventory by almost 50%.

Bulls might argue Weineng purchased these excess batteries to smooth out operations but as we are about to show:

- Weineng buys battery packs from NIO on a back-to-back, implying that battery sales should match subscriber numbers

- Low utilization at battery stations negates excess batteries needs

NIO Battery Sales to Weineng Should Match Subscriber Numbers

NIO states in its most recent 20-F that it sells batteries to Weineng on a back-to-back basis, at the same time as when a NIO customer subscribes to BaaS and purchases their car without a battery. NIO then recognizes the sale when the vehicle (together with a “subscriber battery”) is delivered to the customer, at which point the control is transferred to Weineng.

This implies that when a BaaS subscriber purchases a car, Weineng buys 1 battery corresponding to this sale. After delivery of the car, this battery is “owned” by Weineng and becomes a part of Weineng’s assets.

Operationally, NIO does not differentiate Weineng batteries from NIO batteries at their swapping stations. NIO does not restrict BaaS users to only Weineng-owned batteries when they come to swapping stations to perform battery swaps, nor do they restrict non-BaaS users from only accessing NIO-owned batteries. The lack of such restrictions is important because it nullifies the need for NIO to sell excess batteries to Weineng for logistical reasons.

We sent our investigator to visit a NIO car center, where he had a conversation with a NIO salesman about BaaS. Our investigator also took a test drive and conducted a battery swap. We discovered that there is no distinction between BaaS and non-BaaS batteries. The only distinction the salesman made was that there are two types of batteries, that is short-range battery and the long-range battery. We were told by the salesman that users could swap for both batteries if they want.

Interview Transcript [paraphrased]

Q (investigator): The long-range battery [BaaS Program] could not swap for a short-range battery?

A: (NIO salesman): All the battery pack is the same size, and they are just different in terms of energy density.

Q: So the short-range battery could also swap for a long-range battery.

A: Right. Your short-range battery can also swap for a long-range battery.

We further confirmed that there is no differentiation by looking through the NIO app. For example, the below screenshot shows a battery-swapping station in Beijing. After selecting this swapping station, a user was not asked by the app if he/she is a BaaS subscriber or not. It directly shows how many batteries are available in this station. In this case, it shows there are 13 batteries in total and 13 batteries are available for swapping.

The NIO app also shows more details of the available batteries. There are two choices for the batteries, one is called a standard range (short-range) battery (70/75kWh) and a long-range battery (100kWh). If we click the battery section, it will show that this station has 8 short-range batteries and 5 long-range batteries. No differentiation of NIO battery vs Weineng battery, nor BaaS battery vs Non-BaaS batteries were made.

Source: NIO App

Since BaaS users can tap into NIO’s network of batteries, regardless of whether they are owned by Weineng, Weineng doesn’t have much of a need to maintain excess batteries. Thus the number of batteries owned by Weineng should correspond to the number of subscribers.

However, as of September 30, 2021, Weineng had 19,000 subscribers under the agreement but held 40,053 batteries in inventory.

From both an operational and structural standpoint, Weineng has no need for any excess batteries. Therefore this evidence leads us to believe that NIO has oversupplied Weineng by up to 21,053 batteries as of Q3 2021 to boost its financials.

Site Visits and App Analysis Reflect Low Utilizations in Select Locations

Furthermore, our due diligence team observed some of the stations during the busiest hours and saw little-to-no traffic. Our observation makes us believe that these battery swapping stations likely have very low utilization negating such expansive inventories.

Source: physical NIO battery-swapping stations

We supplemented our physical diligence with an analysis of the NIO App. This analysis provided us with several data points such as batteries available and people in line. From these available metrics, we were able to calculate battery utilization.

We observed 25 of these stations at 2-hour intervals and found NIO’s battery swapping stations had a weighted average utilization of just 39%. Note that we deliberately avoided parts of China that are under a very strict “COVID-Zero” policy (For example, Shanghai was completely shut down and all stations had 0% utilization during our observation window. We did not choose to include that in our analysis). The low utilization further strengthens our belief that Weineng does not have a need for excess batteries at these stations, indicating that NIO likely oversupplied Weineng by up to 21,053 batteries.

Of course, when you purchase thousands of batteries, physical storage is required. To our amazement, however, after searching for months we were unable to identify or locate Weineng’s storage facilities. Our team also consulted employees from numerous battery swapping stations but we were not able to obtain any knowledge of where the batteries could be stored. Weineng’s prospectus also neglected disclosure on battery storage (i.e. 99% of Weineng’s fixed assets are batteries). At best, this leads us to believe many of these excess batteries remain in NIO storage facilities.

Accounting Magic: Shifting Depreciation Costs

Another benefit of creating the Weineng Battery entity is that NIO can realize enormous depreciation savings. According to NIO’s 2020 20F, the useful life of Charging & Battery Swapping Infrastructure and Equipment (including batteries) is 5 years. Strangely, NIO recently changed the useful life to 5-8 years, meaning batteries on the balance sheet depreciate by ~15% per year.

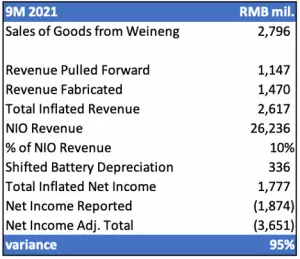

Recall NIO’s sales to Weineng for the 9 months ending September 2021 were 2.8 billion RMB. We believe almost all of these sales of goods are comprised of battery sales. Assuming 20% margins on this revenue, this would imply that NIO collectively shifted assets that cost 2.25 billion RMB off their balance sheet for the period. This means that these batteries will save NIO up to 336 million RMB for 9 months ending September 2021 in depreciation costs which directly impacts (and inflates) the company’s bottom line.

Coupled with the revenue inflation outlined in previous sections, we estimate Weineng Battery alone can artificially improve NIO’s bottom line by over 3 billion RMB. As of the 9 months ending September 2021, NIO’s reported a net loss of 1.874 billion RMB. Without all these accounting shenanigans, NIO’s net loss would nearly double to 3.690 billion RMB!

Source: company filings, Grizzly analysis

Not only is NIO able to recognize 2.6 billion RMB in additional revenues from the BaaS business (which would otherwise not exist if NIO consolidated it) but they are also able to shift costs and expenses associated with the battery swapping business off-balance sheet. By doing so, NIO has fooled Wall Street and investors with reported financial performance that is detached from the business’ reality.

NIO Maintains Effective Control: Top Weineng Managers Are Current NIO Executives

Within its 2021 20-F Risk Factors, NIO states that they have limited control over Weineng Battery.

However, within the same filing, NIO states that:

“The Group, as a major shareholder of the Battery Asset Company, is entitled to appoint one out of nine directors in the Battery Asset Company’s board of directors and can exercise significant influence over the Battery Asset Company. Therefore, the investment in the Battery Asset Company is accounted for using the equity method of accounting”

Based on this conflicting disclosure, NIO investors might be confused as to how much control NIO actually has over Weineng. Executing the scheme we have detailed in this report would require NIO to exercise significant control over Weineng. Our research indicates that is exactly the case.

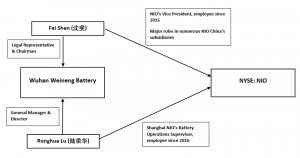

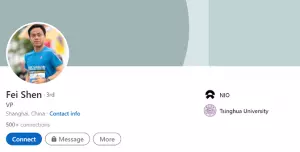

According to Qichacha, a well-known corporate due diligence platform, Weineng Battery’s Chairman and legal representative, Fei Shen, and general manager and Director, Ronghua Lu, are both NIO employees.

Source: Qichacha

We believe these two individuals lead Weineng Battery’s daily operations and material business decisions licensing them to effectively exercise control over the company.

Our research also found that both Fei Shen and Ronghua Lu continue to hold executive roles at NIO while they are at Weineng.

Source: Qichacha, LinkedIn, Grizzly Analysis

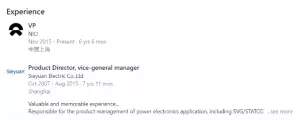

Fei Shen

According to Fei Shen’s Linkedin profile, he currently is a Vice President for NIO, a position he has held since November 2015.

Source: LinkedIn

Fei Shen also shows up in the corporate records of numerous subsidiaries of “NIO China”, of which NIO owns over 90% equity interest. The table below lists some of these companies with Fei Shen’s corresponding positions.

Ronghua Lu

According to Ronghua Lu’s LinkedIn profile, he has been working for NIO since March 2016 and currently is the battery operation supervisor for one of NIO’s main subsidiaries, “Shanghai NIO”.

Source: LinkedIn

There is also an online article that suggests that Ronghua Lu joined NIO in 2016.

“陆荣华2016年入职蔚来,分配的工作之一就是做车电分离的规划,但一开始阻力是很大的。”

“Since Ronghua Lu joined NIO in 2016, one of [his] assigned works is to draw a plan on the separation between the EV and the battery, but there was big resistance in the beginning.”

Some of NIO’s top leadership also holding executive positions at Wuhan Weineng is a major conflict of interest which explains the ease with which NIO has been able to orchestrate the scheme. We think NIO’s control over Weineng provides further support for our belief that Weineng is merely a tool for NIO’s financial shenanigans.

NIO is a “Vehicle” that is Used to Enrich the Local Chinese Government and Insiders

On top of financial trickery, we believe NIO has been using its status as a public company to enrich its local Chinese government shareholders.

Mind-Boggling NIO China Redemptions

In April 2020, NIO announced that it entered into definitive agreements for investments in NIO China with a group of investors (collectively, the “Strategic Investors”) led by Hefei City Construction and Investment Holding (Group) Co., Ltd., CMG-SDIC Capital Co., Ltd., and Anhui Provincial Emerging Industry Investment Co., Ltd. These investors injected ~7 billion RMB into NIO China for a 24.1% stake in the entity.

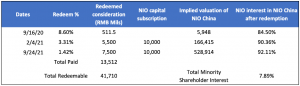

Since then, NIO has redeemed these minority shareholders on three separate occasions. The details are listed in the below table.

Source: multiple news outlets

Local Chinese governments or related entities have already collected 13.5 billion RMB from NIO. Based on the most recent valuation of NIO China, the local government can collect another 41.7 billion RMB from NIO if the company purchases the rest of the government’s 7.87% stake in NIO China.

This is concerning because NIO has historically burned cash and had to dilute shareholders to fund its operations. After coming public in the US, NIO raised 10.9B USD but spent over 2 billion USD on these redemptions. If the local government decides to redeem more, NIO would need another 6.7 billion USD to repurchase, and as of December 31, 2021, the company had 8.2B USD of cash and short-term investments.

Throughout these redemptions, NIO China’s valuation has mysteriously multiplied. Between September 2020 and February 2021, the implied valuation of NIO China jumped approximately 28 times, and after 7 months into 2021, NIO China’s implied valuation further increased another 3x. Within just one year, NIO China’s valuation increased almost 89x.

As NIO China has reached higher valuations, the Chinese government has extracted more money from NIO via the US Equity market. We believe this might be facilitated by early financing the local government provided to NIO called the ‘Gambling Agreement’. As NIO China’s valuation continues to increase, NIO must pay even more to the Chinese government. Without steady cash flow, this will come at the expense of US shareholders.

Undisclosed Gambling Agreement between NIO and the Chinese Local Government

The media recently reported that in 2020 when NIO was receiving the 7 billion RMB capital injection from the Chinese local government from the city of Hefei. At this time there was an additional ‘Gambling Agreement’ between NIO and the Hefei city government where:

- 蔚来中国在收到投资后的48个月内提交IPO,并在60个月内完成上市;股东要求蔚来或者李斌赎回公司股份,不能导致蔚来汽车或蔚来中国的控制权发生变化;3.如果没有完成IPO,或控股权发生变化,李斌就要回购蔚来中国的股份,赎回价格为合肥战略投资者的投资总额,并以年利率8.5%计算利息;4.要求蔚来中国在2024年实现营收1200亿元。

Translation

- NIO needs to apply for IPO within 48 months, and complete the IPO process within 60 months;

- NIO and NIO China’s controlling shareholders should not change, and if it changes, the local government will require Bin Li to buy back all the shares;

- If the IPO was not completed on time or the company’s controlling status changes, Bin Li will be required to purchase back the total amount of the investment made by the local government with an interest rate of 8.5%;

- NIO needs to achieve 120 billion RMB in revenues in 2024.

This agreement puts pressure on NIO and poses a material risk to NIO’s shareholders. Although it only mentions that NIO would need to buy back the total amount of the investment from the local government at an 8.5% interest rate, there may be more terms under the table that could hurt NIO’s shareholders.

The agreement requires that NIO achieves 120 billion RMB in revenues by 2024. To meet these targets, NIO would need to post aggressive growth in the coming fiscal years. We believe this goal is simply unachievable through normal means, and think that both the government and NIO know this as well. Beyond satisfying Wall Street estimates, this ‘Gambling Agreement’ is likely another motive behind the financial shenanigans we have outlined involving Wuhan Weineng.

As stated in requirement 2, NIO’s controlling shareholders cannot change, meaning Bin Li likely has to find creative ways to monetize his stake and unlock value.

NIO’s Chairman Pledged the NIO’s User Trust to UBS in June 2021

In January 2019, Bin Li transferred an aggregate amount of 50 million ordinary shares, consisting of (i) 189,253 class A ordinary shares and (ii) 49,810,747 class C ordinary shares, to the newly established NIO User Trust.

The goal of the NIO User Trust was to build a deeper connection between the company and its users. According to filings, in 2019, the company adopted the NIO Users Trust Charter and established a User Council to discuss and advise the management and operation of the NIO Users Trust. NIO User Council members would be elected by the community of NIO Users. The company’s filings also state that:

“According to the articles of association of NIO Users Trust, incomes and proceeds derived from the trust assets shall be mainly used for the following purposes: (i) environmental protection and sustainable development, (ii) NIO Users community care projects, (iii) community activities promoting common growth of Users and other necessary projects, and (iv) operational expenses of the Users Trust”

Proceeds could be generated from investment returns, dividends, or pledging of such shares. Given the above promise, we think NIO shareholders and NIO Users would be surprised to find out that Bin Li has already pledged the NIO User Trust.

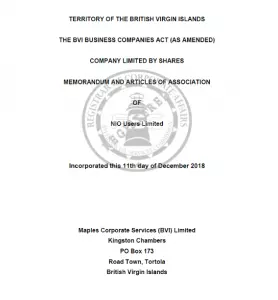

According to NIO’s 2021 20F, NIO User Limited is “a holding company controlled by NIO Users Trust, which is under the control of Mr. Bin Li” and its registered address is “Maples Corporate Services (BVI) Limited, Kingston Chambers, PO Box 173, Road Town, Tortola, British Virgin Islands.”

We were able to retrieve filings from the BVI that revealed that in June 2021, the NIO User Trust had already been pledged to UBS AG.

A document known as the Certificate of Change shows that NIO Users Limited was charged to UBS AG and the registration of charges was on June 28, 2021.

NIO Users Limited was incorporated on December 11, 2018, and its registered address is the same as what is disclosed in NIO’s 2021 20F.

We think Bin Lin intentionally neglected to provide public disclosure or media coverage around this pledge. Ironically, given the shares were pledged pursuant to the NIO User Charter and NIO User Council, Li appears to have violated the trust of the same individuals who believe in his vision.

Not only should investors question Li’s trustworthiness, but they should be aware of the material risk to their investment associated with this same pledge. The company’s stock has fallen from ~$50 on the day of the pledge to ~$23. While the pledge ratio is not known, we can only imagine the stock being down 54% may lead to a margin call on these shares. Bin Li owns 177.7 million NIO shares or about 10.4% of the company. If UBS were to require Bin Li to post more collateral, shareholders would be exposed to the effects of a forced liquidation of the pledged shares in the open market.

Sadly, we were not surprised that Bin Li would put his shareholders at risk after reviewing his past companies, associations, and connections.

NIO Chairman and CEO, Bin Li’s Concerning Past is Full of Shady Connections and Shareholder Value Destruction

We dug deep into Bin Li’s past and our findings were concerning. We found that in the past Bin Li has worked closely with individuals involved in the Luckin Coffee fraud. He was also previously the Chairman and CEO of BITA (previously a US-listed co, which went private later), which was also the controlling shareholder of Yixin (currently an HK-listed co). He was also the Chairman of Mobike, a company that was accused of misappropriating over 600 billion RMB of user deposits. All of Bin Li’s past companies ended up destroying huge amounts of shareholder value.

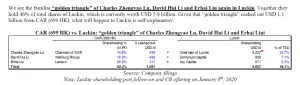

NIO’s Chairman and CEO, Bin Li, is Closely Associated with Joy Capital and Its Founding Partner, Erhai Liu, A Known Key Player in the Luckin Coffee Fraud.

We encourage our readers to read that anonymous research report on the company Luckin Coffee, which later admitted to financial fraud and was delisted by the stock exchange. That research report lists Joy Capital’s Erhai Liu as one of the “golden triangle” and a key player in this Luckin Coffee scandal.

Source: anonymous research report on Luckin Coffee

Considering Erhai Liu’s previous involvement in the Hong Kong-listed company CAR (HK.699) and U.S.-listed Luckin Coffee (OTC: LKNCY), we believe investors should be extremely cautious when a publicly listed company or management gets too close with Joy Capital and Erhai Liu.

Adding to our growing list of concerns, we found that NIO and its Chairman and CEO, Bin Li, have close ties with Joy Capital and Erhai Liu.

Below we summarize the previous connections between NIO/Bin Li and Joy Capital/Erhai Liu:

- Erhai Liu served as BITA’s board director since 2005 and independent director since 2011. BITA was always controlled by Bin Li.

- Erhai Liu was appointed as one of the independent directors for the special committee to evaluate BITA’s go-private transaction in September 2019

- Erhai Liu was reported to be an early investor of NIO and Mobike.

- NIO Capital and Joy Capital jointly invested up to $315 million in UXIN, whose shenanigans were exposed by a research report published by JCap.

From 2010 to 2020, Mr. Li served as Chairman of the Board at Bitauto Holdings Limited. BITA IPOd at $12 per ADS in 2010, and after rising to nearly $100 in 2014, the stock dramatically fell to the mid-10s in 2020. Eventually, the company was taken private at $16. Investors that were involved in the stock at a much higher price never will have the chance to recoup their losses.

According to media reports, the company failed because of poor strategic decisions. BITA relied heavily on external (internet) traffic and as costs increased, traffic declined. This led them to consistently generate losses from 2014 onwards. Upon establishing NIO and MoBike, Bin Li abandoned BITA and focused on these ventures.

Yixin 易鑫 Group

Yixin IPOd in the HK market in 2017 – where BITA had over 50% voting rights – and consolidated the company in its financials. Unfortunately, the stock reached its peak shortly after coming public with shares steadily declining ever since. The details of its downfall are not the focus of this report, but the lackluster performance since 2018 is worrying.

Mobike (摩拜单车)

Mobike was a private company and Mr. Li was Mobike’s Chairman. The company rode one of the hottest trends in China, bike-sharing, and aggressively tried to capture market share. To investor’s dismay, Mobike’s aggressive growth initiatives led to massive underutilization.

After burning substantial cash, Mobike was sold to Meituan, a public company in HK. The Chairman of Meituan was Mobike’s early investor, and also one of Meituan’s largest shareholders. Tencent was also one of the biggest shareholders of Mobike.

Free Money: NIO’s Chairman Using The Company for Interest-Free Loans

Another issue that we identified with Bin Li is that NIO granted interest-free loans to a company called Ningbo Meishan Bonded Port Area Weilan Investment Co., Ltd (“Ningbo Meishan”, Chinese name: 宁波梅山保税港区蔚兰投资有限公司).

![]()

Source: NIO filings

In the footnote of NIO’s 2020 20F, it is stated that:

“In 2017, the Company grant interest-free loans to Ningbo Meishen Bonded Port Area Weilan Investment Co., Ltd. As of December 31, 2020, the loans remain outstanding.”

According to Qichacha, Ningbo Meishan was established in August 2016 with operations in investment consulting and management. Shareholder information shows that NIO’s Chairman, Bin Li owns 80% of Ningbo Meishan, making him a direct beneficiary of these interest-free loans.

Source: Qichacha

NIO’s 2021 20F stated that this loan was fully repaid in 2021. However, it also stated that in November 2021 NIO paid 50 million RMB to Ningbo Meishan to acquire certain equity interests in companies associated with NIO Capital.

“In 2017, we granted interest-free loans to Ningbo Meishan Bonded Port Area Weilan Investment Co., Ltd., a company controlled by our principal shareholders. The loan was fully repaid in 2021. In November 2021, we acquired from Ningbo Meishan Bonded Port Area Weilan Investment Co., Ltd., certain equity interests in companies associated with NIO Capital for RMB50.0 million.”

NIO did not disclose the details about this investment, but we think the sequence of events is very suspicious.

- NIO loans 50 million RMB to Ningbo Meishan (80% stake held by Bin Li) in 2017

- Ningbo Meishan, acquires a stake in an unknown investment fund for an undisclosed amount

- The loan remains outstanding for several years

- Then in November 2021, mysteriously, Ningbo Meishan transfer a 1.03% stake in this fund to NIO with a fair value of 68.5 million RMB

“In November 2021, the Group purchased an equity investment in an investment fund held by Ningbo Meishan Bonded Port Area Weilan Investment Co., Ltd. (“Weilan”), a company controlled by the principal shareholder (and Chief Executive Officer) of the Company (Note 26), with the total consideration of RMB50,000. As at the date of purchase, such investment was recorded at fair value of RMB68,535 with the excessive amount of RMB18,535 over the purchase consideration of RMB50,000 being recorded as an additional paid in capital contribution from the shareholder. The Group has ownership interest of 1.03% in this fund but has the ability to exercise significant influence over this funding its capacity as a member of its investment committee which determines the investment strategies and makes investment decisions for this fund. Therefore, the Group accounts for this investment under equity method.”

On paper, this equity stake helps NIO recoup its original 50 million loan, but shareholders have no disclosure on what this investment fund is, its strategies or any other information. We also do not know how the fair value has changed with it potentially declining markedly since November 2021.

What we think happened here is that NIO gave a vehicle owned by its chairman, 50 million RMB in “free-money” and investors should be concerned about what they received in return.

Conclusion

While NIO is a retail favorite and a popular stock for US investors seeking exposure to electric vehicle adoption in China, we believe the company is being propped up by financial shenanigans and is littered with corporate governance red flags.

NIO’s financials have been overstated through a scheme using an unconsolidated, related party.

Through oversupplying batteries to Weineng and pulling forward revenue, NIO has reported 2.6 billion RMB of inflated revenue for the 9-month ending September 2021 (~10% of its revenue for the period). Even worse, should have reported a net loss of 3.6B RMB for the period, which is double the loss that NIO actually reported.

In the background of this Valeant-style accounting, we believe NIO has enriched Chinese government entities and company insiders. The disclosed and undisclosed agreements NIO has with the Chinese government have already led to redemptions at outrageous valuations which are likely to continue in the future. By our estimates, NIO could still see another 6.7B USD in Chinese government redemptions, which would put a massive strain on its financial condition.

We retrieved documents from the British Virgin Islands that show Bin Li pledged NIO’s User Trust to UBS without any disclosure. Designed to increase the influence NIO users have over the company, Bin Li has used the User Trust for personal gain and exposed shareholders to a potential margin call-induced decline in the stock. With NIO’s shares losing more than half their value, this risk is becoming more and more serious.

ADDITIONAL RESEARCH CAN BE FOUND IN THE APPENDIX.

YOU CAN DOWNLOAD THIS REPORT HERE

Full Legal Disclaimer

***

IMPORTANT LEGAL DISCLAIMER

THIS REPORT AND ALL STATEMENTS CONTAINED HEREIN ARE THE OPINIONS OF GRIZZLY RESEARCH, AND ARE NOT STATEMENTS OF FACT.

Reports are based on generally available information, field research, inferences and deductions through Grizzly Research’s due diligence and analytical process. Our opinions are held in good faith, and we have based them upon publicly available facts and evidence collected and analyzed including our understanding of representations made by the management of the companies we analyze, all of which we set out in our research reports to support our opinions, all of which we set out herein. HOWEVER, THEY REMAIN OUR OPINIONS AND BELIEFS ONLY.

We conducted research and analysis based on public information in a manner than any person could have done if they had been interested in doing so. You can publicly access any piece of evidence cited in this report or that we relied on to write this report.

Grizzly Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use.

We are entitled to our opinions and to the right to express such opinions in a public forum. We believe that the publication of our opinions and the underlying facts about the public companies we research is in the public interest, and that publication is justified due to the fact that public investors and the market are connected in a common interest in the true value and share price of the public companies we research. All expressions of opinion are subject to change without notice, Grizzly Research does not undertake a duty to update or supplement this report or any of the information contained herein.

Recipients of the research report are professional investors who are expected to make their own judgment as to any reliance that they place on the research report. You represent that you have sufficient investment sophistication to critically assess the information, analysis and opinion on this website.

You further agree that you will not communicate the contents of reports and other materials on this site to any other person unless that person has agreed to be bound by these Terms of Use. If you access this website, download or receive the contents of reports or other materials on this website on your own behalf, you agree to and shall be bound by these Terms of Use. If you access our website, download or receive the contents of reports or other materials on this website as an agent for any other person, you are binding your principal to these same Terms of Use.

AS OF THE PUBLICATION DATE OF GRIZZLY RESEARCH’S REPORT, CERTAIN GRIZZLY RESEARCH ASSOCIATED PERSONS (AS DEFINED HEREUNDER) (ALONG WITH OR THROUGH ITS MEMBERS, PARTNERS, AFFILIATES, EMPLOYEES, AND/OR CONSULTANTS), CLIENTS, AND INVESTORS, AND/OR THEIR CLIENTS AND INVESTORS HAVE A SHORT POSITION IN THE SECURITIES OF A COVERED ISSUER (AND OPTIONS, SWAPS, AND OTHER DERIVATIVES RELATED TO THESE SECURITIES), AND THEREFORE WILL REALIZE SIGNIFICANT GAINS IN THE EVENT THAT THE PRICES OF NIO INC’S SECURITIES DECLINE. GRIZZLY RESEARCH AND GRIZZLY RESEARCH ASSOCIATED PERSONS ARE LIKELY TO CONTINUE TO TRANSACT IN NIO INC’S SECURITIES FOR AN INDEFINITE PERIOD AFTER AN INITIAL REPORT ON A COVERED ISSUER, AND SUCH POSITION(S) MAY BE LONG, SHORT, OR NEUTRAL AT ANY TIME HEREAFTER REGARDLESS OF THEIR INITIAL POSITION(S) AND VIEWS AS STATED IN THE GRIZZLY RESEARCH’S RESEARCH. ONE OR MORE GRIZZLY RESEARCH ASSOCIATED PERSONS HAVE PROVIDED GRIZZLY RESEARCH WITH PUBLICLY AVAILABLE INFORMATION THAT GRIZZLY RESEARCH HAS INCLUDED IN THIS REPORT, FOLLOWING GRIZZLY RESEARCH’S INDEPENDENT DUE DILIGENCE. YOU SHOULD DO YOUR OWN RESEARCH AND DUE DILIGENCE BEFORE MAKING ANY INVESTMENT DECISION WITH RESPECT TO THE SECURITIES COVERED HEREIN. THE OPINIONS EXPRESSED IN THIS REPORT ARE NOT INVESTMENT ADVICE NOR SHOULD THEY BE CONSTRUED AS INVESTMENT ADVICE OR ANY RECOMMENDATION OF ANY KIND. FOLLOWING PUBLICATION OF THIS REPORT, WE MAY CONTINUE TRANSACTING IN THE SECURITIES COVERED THEREIN, AND WE MAY BE LONG, SHORT, OR NEUTRAL AT ANY TIME HEREAFTER REGARDLESS OF OUR INITIAL OPINION.

To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. Note that NIO Inc and insiders, agents, and legal representatives of NIO Inc and other entities mentioned herein may be in possession of material non-public information that may be relevant to the matters discussed herein. Do not presume that any person or company mentioned herein has reviewed our report prior to its publication.

This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction.

By downloading and opening this report you knowingly and independently agree: (i) that any dispute arising from your use of this report or viewing the material herein shall be governed by the laws of the State of New York, without regard to any conflict of law provisions;

(ii) to submit to the personal and exclusive jurisdiction of the superior courts located within the State of New York and waive your right to any other jurisdiction or applicable law, given that Grizzly Research is a Delaware limited liability company; and (iii) that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to use of this website or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred. The failure of Grizzly Research to exercise or enforce any right or provision of this disclaimer shall not constitute a waiver of this right or provision. If any provision of this disclaimer is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties’ intentions as reflected in the provision and rule that the other provisions of this disclaimer remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that the information on this website is copyrighted, and you therefore agree not to distribute this information (whether the downloaded file, copies/images/reproductions, or the link to these files) in any manner other than by providing the following link: http://GRIZZLYREPORTS.COM. If you have obtained research published by Grizzly Research in any manner other than by download from that link, you may not read such research without going to that link and agreeing to the Terms of Use on the Grizzly Research designated website.

***