- Pony AI Inc. (Nasdaq: PONY) is a hyped robotaxi company that went public in November 2024. Recent rumors around interest by former Uber CEO Travis Kalanick in PONY’s U.S. business have driven excitement around the company.

- Our research, including on-the-ground testing in one of the major cities in China and expert interviews, indicates that PONY has, in fact, very little to offer and is more akin to a smoke and mirrors show.

- There are serious allegations from an apparent insider that PONY actively falsified data for the algorithm of its self-driving software. Management is allegedly aware of the issue and was covering it up. We find this reckless and dangerous, especially for a company that develops autonomous driving software.

- While PONY likes to portray itself as an international player, the reality is that the company’s permit to conduct autonomous vehicle testing without a driver in California was revoked a few years ago after a crash. Pony had a similar incident in May 2025 in China, which reportedly led to the temporary suspension of the service in that district. It appears that PONY currently only has a permit to conduct autonomous vehicle testing with a driver in the U.S.

- We tested the company’s robotaxis in available districts in China. Based on our experience, it appears PONY has the least pick-up spots, longest waiting time, and overall worse customer experience than the industry leader there. In our opinion, PONY is clearly losing against Chinese peers such as Baidu Apollo and WeRide.

- Expert interviews confirm the issues we saw in our on-the-ground due diligence. PONY is lacking data, a high-definition map, and would need enormous funding and time to catch up with peers, according to industry experts.

- The economics of PONY currently appear dire. Financials worsened after the IPO and the company heavily relies on its related-party transactions. A big portion of PONY’s total revenue comes from an entity directly related to the Chinese military.

- PONY’s close ties to the Chinese Government caused Senators to call for a delisting of PONY from U.S. stock exchanges. We think these issues themselves make a potential acquisition of the U.S. business difficult despite management claiming a separation of the U.S. and Chinese businesses.

- PONY is trading at record valuations, and the recent expiration of the lock-up restrictions is poised to put pressure on the company’s share price.

Introduction

Pony.ai Inc. (Nasdaq: PONY) is a China-based autonomous vehicle (AV) technology company specializing in software deployment and maintenance, vehicle integration, and road-testing services for original equipment manufacturers (OEMs) and transportation network operators. In 2018, they launched PonyPilot—an autonomous ride-hailing service that enabled users to book robotaxi rides in Guangzhou.

Pony.ai made early inroads into the U.S. market, securing a 3-month autonomous vehicle testing permit in California as far back as 2018. However, by late 2021 the California DMV suspended a driverless testing permit for Pony.ai after a vehicle hit a road center divider and a traffic sign in Fremont after turning right. The incident also prompted an investigation by the NHTSA, culminating in a formal recall.

PONY likes to tout its international business and advanced software. In June 2025, The New York Times first reported that former Uber CEO Travis Kalanick is allegedly interested in purchasing PONY’s U.S. business with Uber potentially financially backing the transaction.

After extensive research including testing of AV services in China, expert interviews, and consultation with former employees, we believe that PONY is in fact a dishonest company with severe issues that is currently losing the AV race against better funded competition. With the recent expiration of lock-up restrictions, we believe PONY will see mounting pressure on its business and its stock.

Praying for a Buyout

In June 2025, the New York Times reported that Uber and its previous CEO Travis Kalanick might be in talks to help fund his acquisition of PONY’s U.S. subsidiary. The article stated the company “has permits to operate robot taxis and trucks in the United States and China.” The report does not mention the specific valuation of PONY’s U.S. subsidiary and states that the “talks are preliminary.”

We have seen unfounded excitement around buyout rumors before, recently in Sigma Lithium Corporation which we criticized in a critical report in March 2023. We believe a transaction is in this case not only ill-advised for Uber and Travis Kalanick, but also unlikely to positively surprise investors if it indeed happens.

First of all, PONY’s license to conduct autonomous vehicle testing without a driver in California has been revoked by the California Department of Motor Vehicles after a crash a few years ago. Currently it only holds a license to conduct autonomous vehicle testing with a driver. Therefore, we do not believe the statement in the article that the company “has permits to operate robot taxis and trucks in the United States and China” is entirely correct.

The currently existing U.S. operations of PONY are tiny. According to the company’s annual report, it only generated $321K in revenues from the U.S. in 2023 and $604K in 2024. PONY’s entire business had a negative free cash flow of over $120m in 2024 and is in dire need of funding to realize its ambitions. In terms of PONY’s mileage on the road in California, according to the website of the California DMV, the company only had about 51.6K autonomous miles from December 2023 to November 2024.

Uber’s interest should not be overinterpreted either. Uber has stated that it has a platform strategy that involves partnering with a range of AV companies.

While PONY announces many strategic partnerships in different countries, you can only access their AV service in China where it seems to lose the race against competitors.

Without a driverless testing permit in the U.S., or any meaningful operations or financials, the value in acquiring a U.S. business would mostly lie in the technology, especially the software Pony has developed. Here is where we uncover possibly the most concerning issues. Allegedly, PONY not only falsified data for its AV software, but management was also aware of the issues and was actively covering them up.

The second big issue with the technology is in our opinion PONY’s proximity to the Chinese Government. PONY is a Chinese company, and a PLA affiliated company is in fact PONY’s biggest customer and supporter. PONY allegedly forked the source code of its technology in 2022, and therefore the AV technology developed over the past 2 years was developed in the United States, not China. We distrust this statement and apparently the leading U.S. government voices agree with us. Chairman Moolenaar of the House Select Committee on China and Chairman Rick Scott of the Senate Committee on Aging sent a letter to Securities and Exchange Commission (SEC) Chairman Paul Atkins urging the Commission to begin delisting Chinese companies that pose serious national security and investor protection risks. The letter explicitly mentioned PONY as checking all 3 boxes in terms of military-civilian fusion, forced labor, and party branch affiliation.

Given these issues and other problems we raise in this report, we believe a transaction as portrayed by the New York Times article is not only unwise, but also unlikely to ever happen.

Alleged Company Insider Exposes PONY’s Data Falsification and Other Issues

Our research led us to a Chinese website where an apparent company employee posted in 2023 very concrete allegations exposing that PONY’s autonomous driving technology involves data falsification and other issues. The text below is the paraphrased translation from the original Chinese posting.

“Recently, many WeChat public accounts have been reposting PR articles from Pony.ai, which are practically hyping up their IPO using language that borders on deceptive advertising. I’ve had enough and decided to expose some of the truths behind Pony.ai.

Straight to the point:

1) The technical manager responsible for path planning algorithms at Pony.ai was exposed by a colleague for data falsification. Rather than addressing the issue, senior management tried to delay and cover it up, even going so far as to use the investigation as a way to identify the whistleblower. Pony.ai itself doesn’t even know the real safety statistics of its algorithm. Despite knowing the algorithm is unreliable, they still continued real-world vehicle operations, completely disregarding passenger safety and seriously endangering public safety.

2) The so-called L4 business that Pony.ai promoted in fundraising rounds before Series D was never feasible. They had already abandoned the L4 commercialization path, which has inherent technical flaws. Even achieving scalable L3 is difficult. With weak productization capabilities, they have no competitive edge in the highly competitive L2 market. Without the L4 business, it’s questionable whether they’re even worth a fraction of their D-round valuation of 8.5 billion. The valuation is grossly inflated, making it virtually impossible to raise more capital. Given how fast the autonomous driving industry burns cash, this spells a dead end. Management likely already knows the IPO may fail, and amid a deep economic downturn, they are just trying to help senior executives and employees cash out by buying back shares.

3) The IPO hype is all smoke and mirrors. Pony.ai’s PR claims “large-scale operation of fully driverless autonomous vehicles in busy urban areas of Beijing and Guangzhou.” The truth is, they can only operate in places like Beijing’s Yizhuang and Guangzhou’s Nansha, where there’s barely any traffic. Even deploying the same algorithm in another similarly low-traffic area would take over a year of tuning. So forget about “large-scale operation” in “busy urban areas.” For a company that claims to be technically driven, Pony.ai plays word games just like education-tech companies that rely solely on marketing. They even claim their “BEV perception algorithm” and “game-theory interactive planning algorithm” are self-developed and original. This is like a Chinese EV manufacturer claiming to have invented the electric vehicle. In reality, Pony.ai just follows top-tier company Waymo. When Waymo publishes a new method in a paper, they copy it—and even their replications are full of errors. Their tech lags Waymo by at least three years. Even Waymo’s technical director admits that the current tech stack can’t achieve large-scale deployment in busy cities.

4) The company culture is toxic. Management enables incompetence and pushes out talented employees. Many capable people have left, while those who remain are often unqualified and unethical. These people manipulate data and shift blame to others to protect their own interests. Even when exposed by colleagues, they face no consequences because management has formed its own self-serving interest group.

Supplementary Note (2023-01-18 12:05 +8:00):

I just received an email from Pony.ai’s legal counsel accusing me of “misrepresent to the public” “without evidentiary basis and fact,” also citing confidentiality clauses and threatening legal action. I replied all my statements are either based on sufficient evidence/facts, or based on publicly known information about autonomous driving technologies, shared as personal opinion, or self-derived general statement based on personal conversation with industry leader. All my technical comments about autonomous driving are things that anyone with experience in the field and who has contact with the VC community can easily conclude.

To avoid confusion, I add the following clarifications:

1) Data falsification refers to internal data falsification—plainly, deceiving colleagues to get one’s algorithm deployed. Before I reported this to Pony.ai’s executive Tiancheng Lou, senior leadership either didn’t know or pretended not to know. After reporting, HR replied with an email stating they are investigating, but there’s solid evidence they never conducted a real investigation.

2) “L4 business is unviable” refers to all domestic L4 companies. With their current heavily rely on rule approaches, it’s impossible to scale. This is not aimed solely at Pony.ai. I never worked in their planning team and don’t care what specific methods they use. What I do know is that Pony.ai CTO Lou is a “rule-based true believer”. He previously had a disagreement on direction with Andrew Ng while at Baidu—this was told to me by a former Baidu Apollo executive.

3) Pony.ai also accused me misrepresent to the public that the company has copied and infringed on Waymo’s technology. But in the autonomous driving field, the widely known fact is: most papers come from Waymo Research. When people see some good models, they would use them. I merely stated a basic fact. Pony.ai’s legal team twisted it into me claiming they “copied and infringed on Waymo’s technology,” which I never said. Anyone with basic understanding would take it this way. If reproducing a published paper constitutes “copied and infringed on Waymo’s technology, does that mean Waymo could go around suing every self-driving company and academic group out there? Waymo could sue every AV company and academic lab on the planet. As for the statement regarding the “Waymo tech director” —again, that’s based on my personal conversation with industry leader and a personal opinion based on public knowledge of AV tech paths and situations.

I also want to publicly warn Pony.ai. Do not use legal action as threats and intentionally twist my statements. If you infringe upon my legal rights, I will pursue personal legal action against the individuals responsible under the law.”

These allegations are in our opinion credible and extremely concerning. Autonomous driving can be extremely dangerous, as faulty software may cause crashes and potentially cost lives. We believe that while thankfully nobody has gotten seriously injured yet, PONY’s at best sloppy treatment of its software has already led to incidents and the revocation of one of the company’s most valuable licenses in the U.S.

Move Fast and Break Things – The Wrong Attitude in Autonomous Driving

PONY tried the autonomous test drive in the U.S. before, however, its driverless testing permit was reportedly suspended by the California Department of Motor Vehicles in 2021.

“The crash occurred in Fremont on Oct. 28 when one of Pony.ai’s fleet of 10 Hyundai Kona test vehicles collided with a lane divider and street sign after turning right. No one was injured, and no other vehicles were involved. As was the case for several months, the Kona was being trialed without a human safety operator.

Pony.ai’s driverless testing permit was subsequently suspended by the California Department of Motor Vehicles, and an inquiry was launched by the NHTSA. The investigation concluded that a software defect was to blame, and the Toyota-backed start-up was informed. It admitted that a planning system diagnostic check ‘could generate a “false positive” indication of a geolocation mismatch’ in very rare circumstances, and updated the software on the vehicle that crashed, as well as two others.”

According to this report from TechCrunch, PONY “paused its driverless pilot fleet in California six months after it was approved by local regulators to test autonomous vehicles without a human safety driver. “

Following the driverless testing permit suspension, “The California Department of Motor Vehicles revoked Pony.ai’s permit to test its autonomous vehicle technology with a driver on Tuesday for failing to monitor the driving records of the safety drivers on its testing permit,” according to the report in May 2022 from TechCrunch.

Therefore, in late 2021 and then 2022, PONY lost both of its driverless and driver-present autonomous driving permits in California, which is a testimony of PONY’s lack of technology and safety control. However, the company’s permit for driver-present autonomous vehicle testing was reinstated in December 2022. This permit is not particularly special or valuable as there are about 30 companies with a permit to do driver-present autonomous vehicle testing in California. Only 6 companies have a permit to conduct driverless autonomous vehicle testing and only Mercedes-Benz, Nuro Inc, and Waymo LLC currently have permits to deploy autonomous vehicles.

As recent as May 13th this year, it was reported in China that a driverless pilot testing car ran into issues and stopped on the road. Then it caught fire by itself when it was processed by the employees. The picture below is from the media report.

Source: finance.sina.com

Chinese media reported that days after this incident, PONY suspended the robotaxi services in the Yizhuang district in the city of Beijing.

We suspect the collisions, and the followed removal of permit is due to PONY’s inferior technology. The company’s current active AV related permit in the U.S. is a dime in a dozen and not particularly valuable, in our opinion. But even in places where PONY does offer AV services to customers, its sloppy approach and inferior technology show.

PONY is Miles Behind Competitors

There are only a few select regions in the world where a customer can access PONY’s AV services. Those regions are mainly located in China. We sent our China due diligence team to gather data on the ground. We tested PONY’s AV service in one of the major cities. We compared the experience with Pony.ai’s competitors WeRide and Baidu Apollo in the same city.

Pony.ai Mobile App

Our experience shows PONY in the last place in many important aspects:

- PONY seems to have the least available spots to get on its robotaxi as compared to Baidu Apollo and WeRide (Note: customers need to go to pre-designated places/spots to get on and get off the robotaxi provided by these companies).

- Customers need to wait for the longest time for PONY’s robotaxi, as compared to WeRide and Baidu Apollo. For example, our team waited on average over 20 mins for PONY’s rides, whereas we waited approximately 10 mins for WeRide’s rides and about 5 mins for Baidu Apollo’s rides. We suspect the main reason for the long wait time is that competitors have more robotaxis in service.

- Baidu Apollo overall has the best comfort and experience as compared to the other two robotaxi service providers. Their vehicles are relatively new and have multiple brands. In addition, certain vehicle also has AI audio interaction technology, which is a plus for customer experience.

In summary, we were not impressed with our experience with PONY’s AV service and see competitors in the clear lead when it comes to customer experience and availability. Although this is just one of the major cities, we suspect the situation to be similar in other cities as well.

Industry Experts See PONY’s Technology as Severely Lacking

We consulted with industry experts and compared available technologies in the marketplace. Experts point out severe issues with PONY that competitors are able to solve.

Not only does PONY seemingly have the fewest pick-up spots and the longest wait time, experts in the industry also point out the severe issues such as lack of high-definition map and source of fundings.

“On Baidu’s side, from a foundational technology perspective, Baidu has its own high-definition map from its own business group. They have their own high-definition map in place. This is the first foundational difference—Pony doesn’t have this.

Secondly, so far from an AI point of view, Baidu has a big model—essentially, different models to support different AI applications, including in the automotive industry. Baidu has big-model technology. They have also been testing for a longer time. Their testing duration is much longer and much larger than Pony AI’s. They test more, which allows them to gain more experience and gather more bad cases to improve upon. This is different because Pony started later than Baidu, and also because there are fewer robo-taxi vehicles available in the market. I think this is an important difference.”

One sentiment that was mirrored throughout the interviews is that PONY is currently really more akin to a start-up that needs enormous funding to hope to catch up and eventually compete with much better funded peers.

“Everybody knows that. Very, very expensive. I don’t know if you know, but it costs a lot of money every single day to keep these operations running. Zoox is lucky to be partnered with Amazon”

“I don’t envy anyone who is burning a lot of cash and not making a lot of cash.”

The experts’ critical perspective on PONY stands in stark contrast to PONY’s own self-assessment. PONY’s CTO stated in an interview in China that he sees PONY at the same level as Waymo and Baidu while all other players are supposedly two and a half years behind. To our amusement, the CFO of WeRide responded to the statements of PONY’s CTO in a WeChat moment.

Translation:

“Curious how a company that had its U.S. license revoked after a crash, and caught fire in Beijing after hitting a curb, still has the nerve to diss another company that has deployed far more vehicles and achieved much broader real-world operations. How can it claim to be two and a half years ahead of others? Here’s a tip for our industry peer: instead of signing MOUs all over the world just to call yourself a “global company,” try following WeRide’s example — actually get dozens of vehicles on the road and running before making such claims.”

WeRide’s CFO is obviously a competitor so her statements should be taken with a grain of salt. But we agree that everything she says in her comeback is correct. PONY’s license did get revoked due to an incident in California, and its robotaxi did hit the curb and caught fire, which led to the temporary suspension of the company’s robotaxi service in that district.

PONY is Too Close and Dependent on the Chinese Government

According to the press release, on May 5, 2025, Chairman Moolenaar of the House Select Committee on China and Chairman Rick Scott of the Senate Committee on Aging sent a letter to Securities and Exchange Commission (SEC) Chairman Paul Atkins urging the Commission to begin delisting Chinese companies that pose serious national security and investor protection risks.

The letter states that PONY checked 3 boxes in terms of military-civilian fusion, forced labor, and party branch.

The letter goes into more details to explain why PONY is included in this list.

-

- Pony AI Inc.

“Pony AI develops autonomous driving technology while maintaining partnerships with Chinese military-linked entities. State-owned GAC Group, which has documented ties to corruption, 60 military procurement, 61 and forced labor in Xinjiang,62 holds an ownership stake with veto power over Pony’s key decisions. 63 Pony formed two specific joint ventures: one with SANY Heavy Industry,64 a defense contractor developing military unmanned equipment,65 and another with Sinotrans,66 a state-owned military logistics provider.67 These ventures are postured to support PRC military logistics in a potential conflict with the United States. The Pentagon designated Pony’s LiDAR supplier, Hesai, as a Chinese military company in 2023.68 Pony also partners with Robosense in a military-civil fusion project with blacklisted Beihang University to develop unmanned systems for military logistics networks.69 Pony has an embedded CCP branch and is prominently featured in CCP publications as a model enterprise advancing “new productive forces,” with its Guangzhou operations highlighted by Party-state media as aligned with national priorities in autonomous driving and industrial innovation.70”

According to this report’s introduction, PONY’s partner Sinotrans is directly tied to the People’s Liberation Army (PLA), China’s military.

“Sinotrans, now under China Merchants Group, is directly tied to PLA logistics. Its subsidiaries carry out military transport missions, support naval operations, and have been praised by PLA departments for meeting national defense standards. See Conor M. Kennedy, China Maritime Report No. 4: Civil Transport in PLA Power Projection, China Maritime Studies Institute, U.S. Naval War College 9, 13–14 (Dec. 2019), https://digital-commons.usnwc.edu/cgi/viewcontent.cgi?article=1003&context=cmsi-maritime-reports.”

PONY itself describes Sinotrans Limited (“Sinotrans”) as a related party because Sinotrans is the non-controlling shareholder of Cyantron, which is 51% owned by PONY.

Sinotrans is also the main revenue driver of PONY. Sinotrans’ share of revenue contribution increased over the past few years. For example, in 2022, revenues from Sinotrans accounted for 31.0% of the total revenues. In 2024, the revenue percentage coming from Sinotrans increased already to 40.9%.

Source: 2024 Annual Report

It appears the revenue from Sinotrans is from the robotruck business unit and it is safe to say that, without the incremental revenues from Sinotrans, PONY’s total revenues in 2024 would have declined compared to 2023.

The table below summarizes the business breakdown of the company from 2022 to 2024. It is very obvious that PONY’s robotruck services unit now accounts for more than half of its total revenues, which is mainly driven by the revenues from PLA affiliate Sinotrans.

Source: 2024 Annual Report

Another point worth noting is that the highly touted robotaxi business has seen a decline in terms of revenues from 2022 to 2024, and as of 2024, it accounts for less than 10% of total revenues.

In addition, we found the company has not been straightforward about its relationship with Hesai Group. Hesai is a Chinese Lidar company that is considered a security risk by the U.S. government due to its ties to Chinese military companies.

On April 23, 2025, PONY announced that it unveiled the 7th-generation robotaxi lineup. However, there is no mention of the LiDAR provider Hesai in its press release.

“Continuous design optimizations have also reduced a total amount of 70% bill-of-materials (“BOM”) costs, among which with 80% decrease in autonomous driving computation (“ADC”) and 68% cut in solid-state LiDAR, in each case compared to its predecessor.”

On April 24, 2025, Hesai announced that it was selected as the primary lidar provider for PONY’s 7th-generation robotaxi:

“its long-range, automotive-grade AT128 lidar has been selected as the primary lidar solution for all three mass production models of the new seventh-generation Robotaxi unveiled by Pony AI Inc. (Nasdaq: PONY), a global leader in the large-scale commercialization of autonomous mobility. Each vehicle will be equipped with four Hesai’s AT128 lidar sensors, demonstrating Hesai’s critical role in enabling advanced autonomous driving capabilities.”

It appears that Hesai will continue to be PONY’s primary lidar provider going forward. This is another complicating factor that ties PONY even closer to the Chinese government.

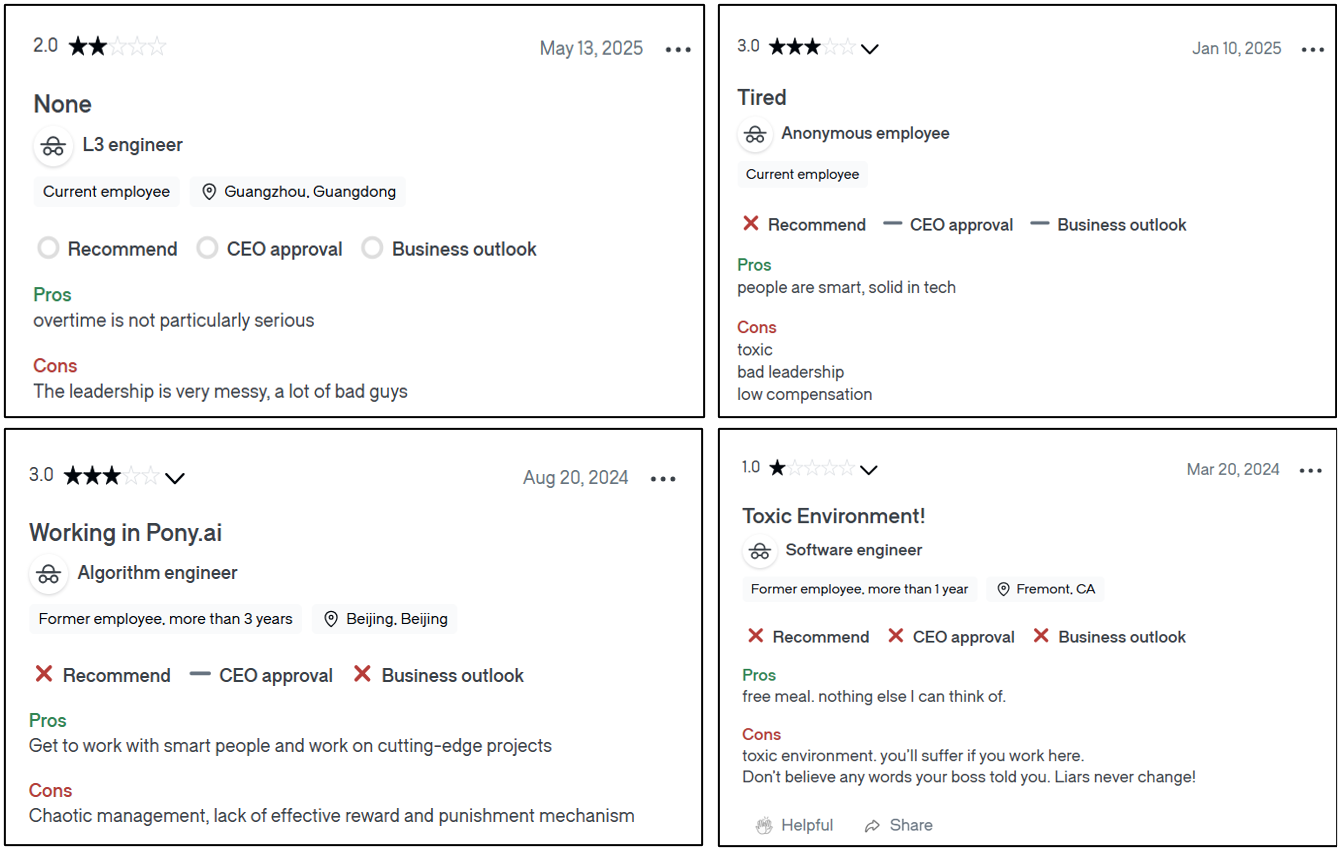

Former Employees Describe a Toxic Work Culture

We reviewed employee forums for the company. The feedback appears to be negative when it comes to management. This is an especially negative factor because a company in a quickly evolving industry like AV needs to attract and retain top talent to compete.

Former employees called the management “chaotic”, “toxic”, and “bad”.

Source: Glassdoor

Source: Indeed

Worsening Financials Amidst Lock-Up Expiration and Sky-High Valuation Set the Stage for Disappointment

We think three factors will put pressure on the company and its stock in the short term.

First of all, the financials are worsening while capital needs are growing.

In the prospectus disclosed by the company, it shows that the company’s revenues for the first half of 2024 more than doubled from $12M to $24M, and the loss attributable to PONY narrowed from $69.4M to $51.3M in the first half of 2024. These are the financials PONY presented to investors just before its IPO. The trend looked encouraging at the time.

Source: sec.gov

Only a few months after its IPO, the company disclosed in its annual report for 2024 a different picture. Revenues for the full year 2024 were barely up y-o-y, with an increase from $71.9M in 2023 to $75.0 in 2024. In addition, the loss attributable to PONY is $274.1M for 2024, as compared to a loss of $124.8M in 2023. The financials of PONY worsened substantially post-IPO while capital needs continue to skyrocket.

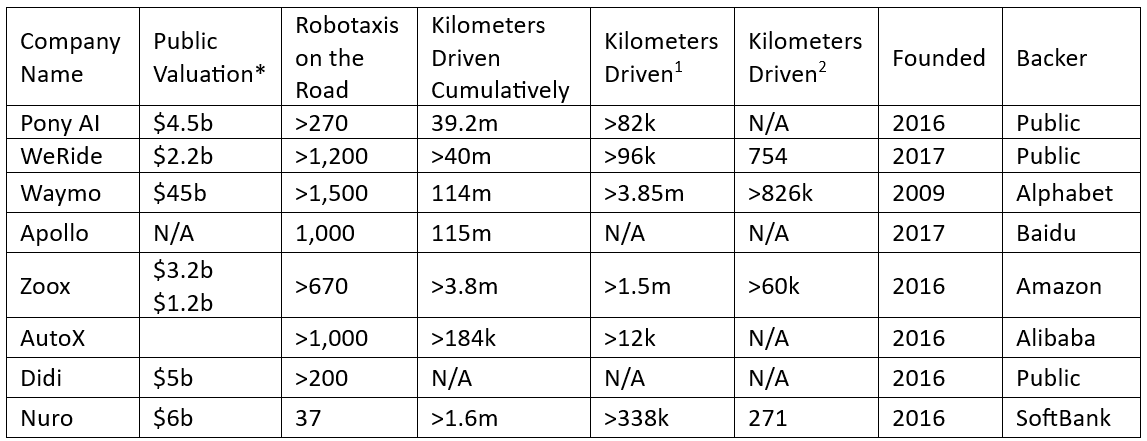

The second factor that we think will put near-term pressure on PONY is the company’s aggressive valuation. PONY’s P/S multiple is drastically higher than the peers in the autonomous driving sector while its growth is lagging peers.

*As of July 7th, 2025

1Total kilometers driven in 2024 with a driver in California

2Total kilometers driven in 2024 without a driver in California

Source: Media reports, companies’ filings, Grizzly’s analysis

The current run-up of the company’s stock is likely due to the hype in the robotaxi sector in general. However, investors should be aware that the robotaxi business accounted for less than 10% of PONY’s total revenues in 2024 and had a year-over-year decrease.

The third factor that we think will put pressure on PONY is the company’s lock-up expiration that passed on May 26th, 2025. Over 225 million shares of pre-IPO investors are now ready to be sold into the market, which will likely put pressure on the stock.

Conclusion

We think that PONY finds itself fundamentally in a difficult position with worsening financials, growing cash needs, and fierce competition that seems way ahead. PONY’s close ties to the Chinese government make any kind of acquisition very difficult from the investor’s perspective. But the most worrisome for a potential acquirer or an investor in PONY is the allegations of falsified data in combination with a history of crashes and limited permit to conduct autonomous vehicle testing outside of China. It would not be the first time that we find out that a Chinese company fakes data but in this industry consequences of such misbehavior are too severe.