- We believe KULR Technology Group, Inc. (NYSE: KULR) is just a fancy PR machine trying to impress gullible investors with little business success and a dim future ahead.

- The most recent earnings, presented as a “record revenue year and quarter,” are hiding a disastrous quarter marked by declining sales in products and services. The results were inflated by pulling forward millions of dollars in revenue from the recent licensing agreements, even though the payments will be made over the next three to five years. The biggest one, which allowed the company to pull forward $1.66 million, was signed two days before the end of the year 2024 and won’t see full payment until December 2029.

- We uncovered multiple occasions where KULR’s management projected enormous revenue opportunities and goals, sometimes suggesting a 100x revenue increase after a few years, only for the actual results to fall far short. In reality, KULR has consistently missed all its projections by at least 50%.

- Management touted deals like a 500 MWh battery supply from a “tier one manufacturer”, claiming hundreds of millions in potential revenue. Yet, two and a half years later, there’s very little concrete evidence of these partnerships delivering meaningful financial returns.

- Despite the management’s claim of a massive sales pipeline, strong brand recognition, and year-over-year customer growth, the company ended Q4 2024 with only ten customers, a decline of more than 70% to Q3 2024.

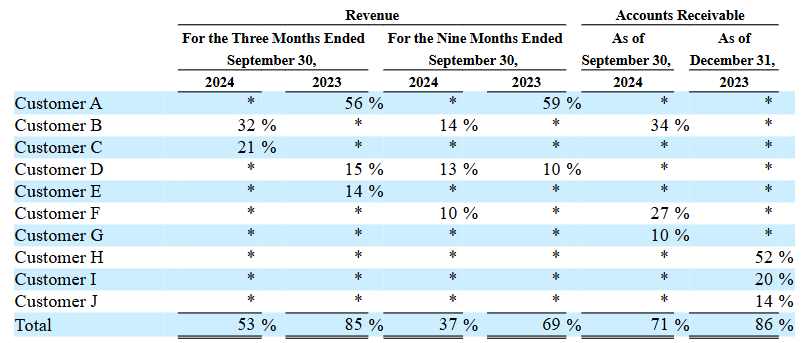

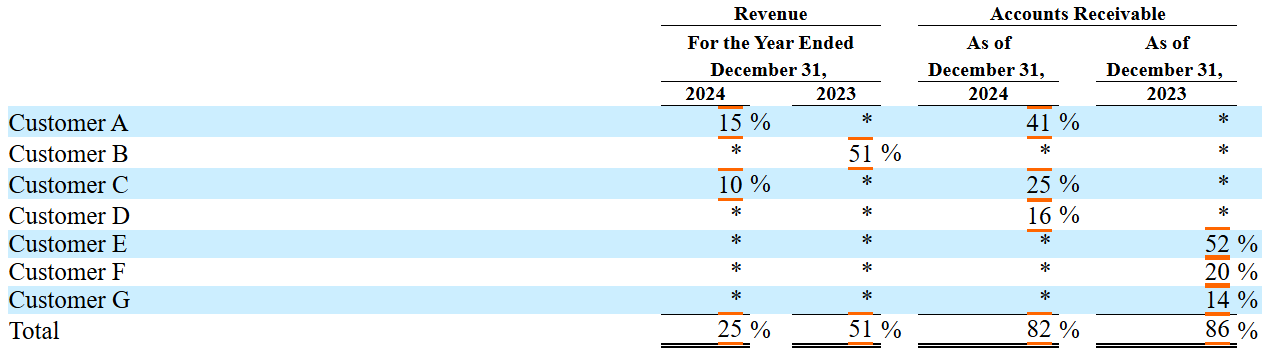

- For the three months ending September 30, 2024, two customers accounted for the majority of the company’s revenue. For the three months ending December 31, 2024, a single customer accounted for approximately 50% of the company’s revenue. Even worse, these three different customers are different from the three other customers that represented 95% of the total revenue for 2023. This underscores another major issue in KULR’s core business: its struggle to retain customers.

- The low revenue per customer indicates that even those who try KULR’s products don’t seem to stick around, casting doubt on claims of widespread demand and organic brand growth.

- We often hear about KULR’s “long-standing relationships” with the DoD and NASA, but one look at actual contract records paints a different picture. The biggest DoD payouts tend to be small subawards (subcontract awarded by DoD contractor)—mere fragments of larger deals.

- In 2024, the total amounts for awards and subawards publicly available on government databases were only $97,500 and $1,075,000, respectively, with a combined total of $3,3680,000 since the first award. Specifically for NASA, publicly available data reveal a mere total of $1.7 million in awards since the first award was granted.

- While the company frequently cites “major” DoD and NASA collaborations, these government contracts appear sporadic and relatively modest, contradicting the lofty revenue forecasts the management shares in public statements. The biggest contract is an extension with the U.S. army for a total amount of $2.4 million. This contract’s data is not publicly available. The other contracts were either announced without any revenue projection or with much smaller ones.

- We identified a similar pattern with contracts from non-governmental organizations, including Lockheed Martin. KULR has been awarded a $500,000 initial order with “future considerations up to the multi-million-dollar amount over the next year (2023)”. Additionally, at the end of 2023, KULR announced a follow-on contract from Lockheed Martin with a revenue potential exceeding $8 million and consistent demand over the next few years. However, as of March 2025, only $187,000 in contracts have been awarded to the company.

- The ongoing discrepancy between claimed “game-changing” contracts and the reality of small, infrequent payouts casts serious doubt about KULR’s habit to issue eye-catching press releases without delivering matching financial results.

- We notice the same behavior with “partnerships” announced by KULR. Although not being directly disclosed as revenue-generating opportunities, they are usually announced with charming buzzwords. By digging deeper into them, we found that most of these partnerships are ridiculously insignificant and only reveal the company’s desperation to appear relevant to investors through fancy PR.

- Our interviews with former employees were damning and confirmed all our suspicions. From fluff PRs, unsellable products, to lack of attractiveness, customer retention, and business scalability, we have little hope for the company’s future.

- Recent marketing moves from the company, such as a doubling of revenue projection for 2025, a future partnership in robotics and AI, and the purchase of bitcoins, appear to us as the regular meaningless PR acrobatics to keep the stock price afloat.

Introduction

KULR Technology Group, Inc, founded in 2013 and based in San Diego, California, specializes in developing and commercializing thermal management technologies for electronics, batteries, and other components. The company’s product offerings include lithium-ion battery thermal runaway shields, automated battery cell screening and test systems, fiber thermal interface materials, and phase change material heat sinks. These technologies are utilized in applications such as electric vehicles, energy storage, battery recycling transportation, cloud computing, and 5G communication devices. KULR’s solutions aim to enhance safety and efficiency in energy storage and thermal management systems. The company is publicly traded on the NYSE American exchange under the ticker symbol KULR. We think the company has been vastly overpromising and underdelivering to investors, and despite its recent stock price boom, does not have a promising future.

Record Quarter or Disastrous Quarter Embellished by Accounting Shenanigans?

On March 27th, KULR posted their Fourth Quarter and Full-Year 2024 Financial Results, which they proudly called a “record revenue quarter and year.” However, despite these claims, the company used several misleading statements and accounting practices to mask a troubling quarter.

The truth lies in the details of the 10-K filing, and was completely hidden from the financials press release from the company. Everything starts from the agreement for the CF Cathode that was signed with a Japanese customer on December 29th, 2024, just three days before the quarter ended:

“The CF Cathode Agreement contains a significant financing component. Therefore, the Company immediately recognized revenue in an amount equal to the present value ($ 1,658,451) of the $ 1,800,000 license fee, using the prevailing interest rate in the relevant market (prime rate) of 7.5%.”

This agreement is a licensing agreement where the Japanese customer agreed to pay $1,800,000 to KULR over five years with installments of an initial $300,000 in February 2025 and consecutively $150,000 each quarter until December 2029.

To save its quarter and full-year results, KULR decided to recognize the entirety of the revenue tied to the agreement in 2024, signing the deal only two days before the end of the year.

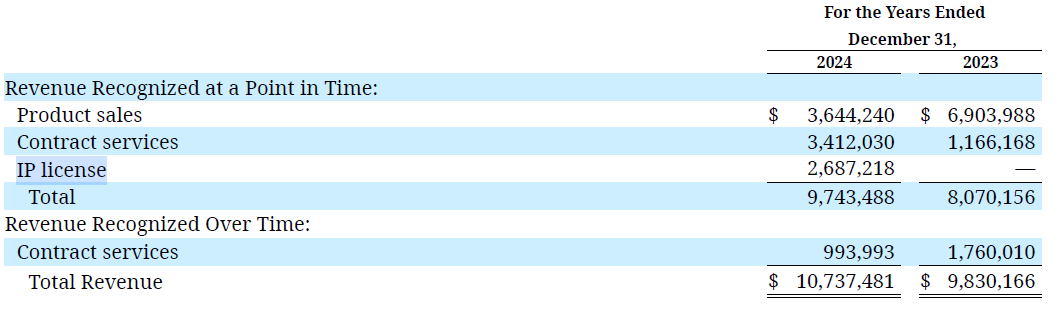

In other words, without recognizing the full value of the 5-year contract into this year, revenue would have only been $1.71 million, reflecting a decrease of approximately 27% from last year’s figure of $2,333,851, and a decline of 46% when compared to the previous quarter’s revenue of $3,185,778.

Though it was not detailed in the 10-K filing, the product revenue and service revenue for Q4 2024 were $1.13 million and $0.58 million, respectively. Compared to the same period last year, as highlighted in the company’s press release, this represents a decrease of approximately 22% in product revenue and 34% in service revenue.

The licensing deals are the sole reason the gross margins improved to 64% year over year, although it was down from Q3 2024 which had a gross margin of 70.85%. As disclosed by the company, the cost of revenue for the licensing agreements is negligible, which is considerably boosting the overall gross margins number.

Note that the whole earnings call and earnings release were focused on a comparison between Q4 2024 and Q4 2023, with very little focus on the full year 2024. This was a clever way, and the only way, for the company to post somewhat “impressive” and “positive” numbers, as the comparison quarter over quarter would have looked much less impressive.

We notice the same pattern in Q3 2024, when the company announced another licensing agreement with another Japanese customer with a minimum royalty fee of minimum $600,000 over the three following years:

“Therefore, the Company immediately recognized revenue in an amount equal to the present value ($528,767) of the $600,000 minimum royalty to be received, using the prevailing interest rate in the relevant market (prime rate) of 8.0%. Royalty fees above the minimum amount will be recognized when and if amounts become probable and estimable.”

The company recognized approximately $2.14 million in revenue that instead should be spread out over the next three to five years. If the revenue had not been pulled forward, the actual revenue figures for 2024 would have been $8,600,263, about 20% lower than what the company reported. Rather than achieving a “record year” with a growth of roughly 9%—a figure that is already underwhelming—the company would have faced a significant decline in revenue of around 13%, amounting to $1,230,000.

Such accounting shenanigans are a huge red flag. Considering the other issues, we uncover and present in this report, we urge investors to proceed with caution, as we find the company is all-around misleading.

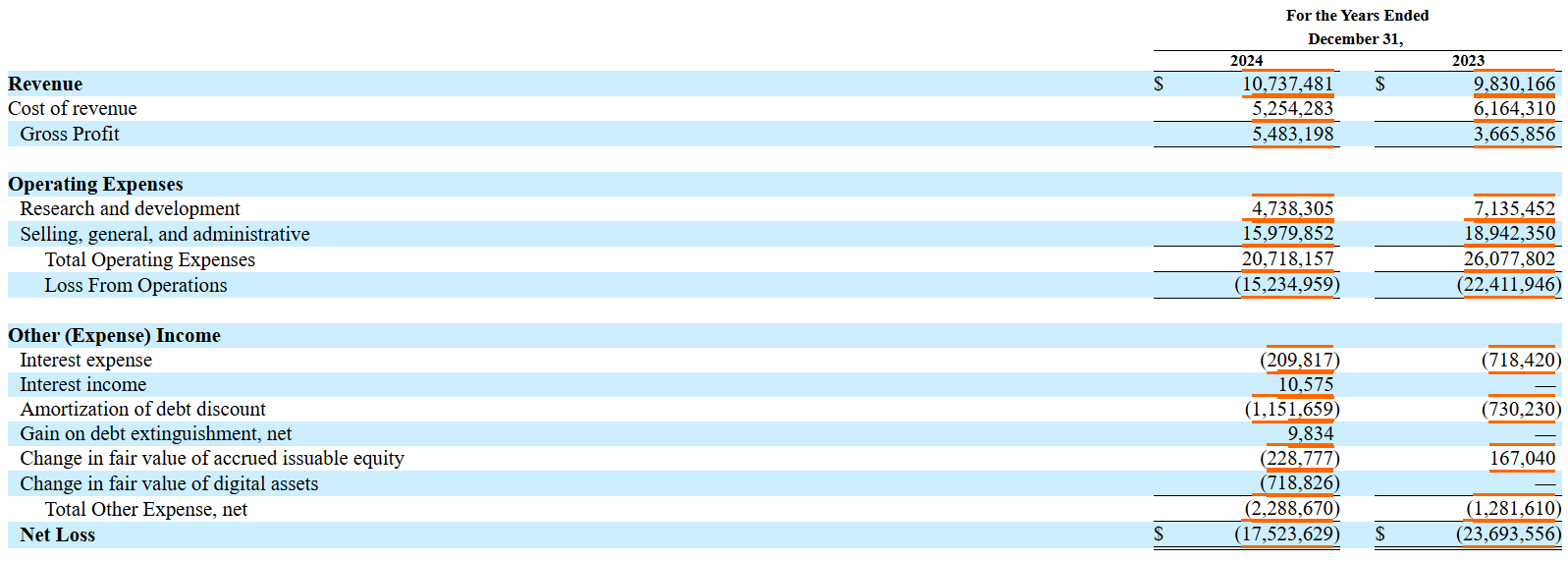

“For the years ended December 31, 2024 and 2023, R&D expenses were $4,738,305 and $7,135,452, respectively, representing a decrease of $2,397,147 or 34%.

The decrease was comprised primarily of $2,193,643 of engineering labor and other costs charged that were reduced or redeployed to revenue-generating activities and were charged to costs of revenue, $784,827 related to a planned decrease in R&D consulting services.”

The core business of the company is already crumbling. Indeed, with such a decline in R&D expenses as well as product revenue, it appears clear that the company does not have much hope for its future operations. Although it is putting out all these misleading press releases about commercial partnerships and agreements, real numbers and actions speak louder than words and promises.

KULR Has Repeatedly Overpromised and Underdelivered

A company issuing frequent press releases during a period of “meme hype” and significant stock price appreciation is typically a red flag, often indicating desperation. This appears to be the case with KULR, which has published no fewer than 11 press releases in the past three months.

Many of these announcements highlight contracts and partnerships with various branches of the U.S. Department of Defense (DoD) or other major industry players. However, the company has become increasingly opaque in its disclosures, withholding the identities of certain partners and providing only vague details about contract values.

Our research indicates that KULR, which has historically attracted investors with highly unrealistic projections and revenue potential, continues to overstate its prospects while showing minimal growth in its underlying business.

KULR Has Missed All of Its Past Projections

In early 2022—specifically during the Q1 2022 earnings call—KULR’s CEO, Michael Mo, announced that the company had secured $55 million in capital for “two key initiatives.” The primary objective was to obtain over 500 MWh of battery cell supply from “tier one battery manufacturers,” later revealed to be “Molicel,” in anticipation of rapidly growing demand in key end markets, including Storage and E-mobility. At the time, the CEO stated:

“KULR will provide total system solutions to specific high value energy storage and e-mobility applications. With a total top line revenue potential of between $250 million to $350 million.”

When this was announced, KULR had just concluded the year 2021 with approximately $2.4 million in revenue, suggesting that these new initiatives could potentially increase revenue by 100 times at the minimum—seemingly a major opportunity for investors.

When analysts asked how much capital these supply commitments would ultimately require, management’s response remained vague. A few weeks later, the company disclosed a partnership with “Molicel,” indicating an initial order of 75 MWh of Li-ion battery cells and plans to purchase 700 MWh in total. At that time, KULR reiterated its belief that the corresponding revenue opportunity could now exceed $350 million.

Following this press release, little additional information was provided about the partnership. The latest direct reference to this initiative and its “potential” is found in the 2022 10-K, which largely repeats the content of the initial press release:

“Through our partnership with MoliCel, KULR has access to best-in-class Li-ion battery cells with high power and energy to build battery modules with the highest safety ratings. As part of the strategic relationship, KULR has access to over 700MWh of battery energy capacity to further accelerate its production and supply chain localization initiatives within North America. Securing this MoliCel battery cell supply accelerates our ability to provide total solutions to high value customer applications with revenue potential that could exceed $350 million annually in five years.”

Over two and a half years later, this substantial revenue has yet to materialize even a small portion of what has been announced. Unfortunately for investors, this was far from being the only instance of inflated and unrealizable projections. A few quarters following that first announcement, during the Q4 2022 earnings call, shortly after the launch of their new product named “KULR ONE,” management stated:

“Since the launch of the product in January, KULR ONE has half a dozen development engagements with electrical vehicles, DoD applications, electric aviation and charging infrastructure customers. We expect KULR ONE to have the revenue opportunity of over $200 million by 2026.”

and

“We expect to achieve over $100 million in revenue for KULR ONE design solutions over the next 3 years, as we continue to gain traction with large OEM customers and their products begin to ramp in volume.”

Moreover, management projected that this new product would generate approximately $10 million in revenue for 2023, largely based on a U.S. Army contract that appeared to have boosted the company’s optimism. However, the total revenue for 2023 ended up being approximately $9.8 million, and only slightly above $10.7 million for 2024.

“I talked about I expect KULR ONE, the solutions platform, is expected to generate about $10 million in revenue for 2023 and have a strong revenue opportunity to, over the next few years, to be over $100 million. I think the Army contract is kind of an important milestone or a path to that revenue ramp.”

Funnily enough, even though their product revenue is down 47% year-over-year, during the latest earnings call for the year ended 2024, the CEO stated that:

“As you all know, we’ve been investing in our KULR ONE battery platform. We’re now reaping the benefits of that investment.”

As will be demonstrated later in this report, KULR’s contracts with the DoD—repeatedly cited as a key driver of future growth—have, at best, stagnated, with no clear signs of meaningful expansion besides a single contract with the U.S. Army that is already delayed.

We asked a former sales manager who confirmed our suspicions, saying that besides luring investors with unreachable objectives and projections, most of the time, the products were not even ready to begin with.

“There’s a lot of. It’s like random stuff that they would just say that will never work. But. Or like you said, they would say like, hey, we’re doing 100 million in this. We’re going to sell a bunch of safe cases. And then you would like, talked to them. He was like, yeah, safeguards are ready. It’s still not working or there’s no chance ever have it ready by then.”

Another reason for this is also the lack of clear direction and constant switch of focus by the company in its operations. KULR has constantly been changing its focus whether it is sector or products. One could argue that the company is evolving and pursuing the best opportunities, however, this would have resulted in a higher growth in revenue and opportunities, which is not the case. The former sales manager told us that KULR was constantly asking them to find customers in new sectors, without a clear focus.

“Yeah. So like that was what they would tell me. Like they would just kind of give you a different industry. But usually was anything, you know, battery related. And the rest were like government contracts that they had from a while ago. So if it wasn’t for the NASA connection there, I don’t know what Cooler. I don’t think cooler would be a business.”

The confusion was also about products that the sales team was allegedly not properly trained to sell:

“But KULR Vibe, when I was there, at least everyone on the sales team, we were like, what? You know, we were confused, like, what the hell are we selling? It was like a vibration reduction software, had nothing to do with batteries, nothing to do with anything apparently. Like, I think one of the executives knew a guy that started that business, and it wasn’t doing too well, so he bought it for cheap and then we started selling it.”

More Missed Projections and Unrealistic Guidance

In their third quarter of 2023 earnings call, KULR shared yet another optimistic outlook:

“Based on continued record quarterly growth and the broadening and deepening of our customer engagements across multiple market verticals, our sales funnel shows that our current 2024 revenue potential to be between $26 million and $34 million.”

In reality, the company ended up generating a little over $10.7 million in 2024, which is more than 60% below the projection mean given by management. Whether these projections were the result of overconfidence or something more deliberate remains open to debate. During their latest earnings call for the quarter of Q4 2024, management once again stated that they project to double their revenue in 2025, which would still be below their previous projection for 2024. We still do not believe that it will happen.

Finally, management is also prone to fail in achieving its breakeven targets, as illustrated by another statement from the beginning of 2024:

“We continue to work on growth. We continue to work on resource optimization. And I guess we—I think we have a good line of sight to having operational breakeven in we think, potentially in the second quarter of next year. Obviously, we’ll have to meet certain milestones, which I can’t guarantee we will, but we think that they’re very much possible based on what we see today and the revenue visibility, the pipeline, the various customer partnerships we have and certain initiatives that are in place.”

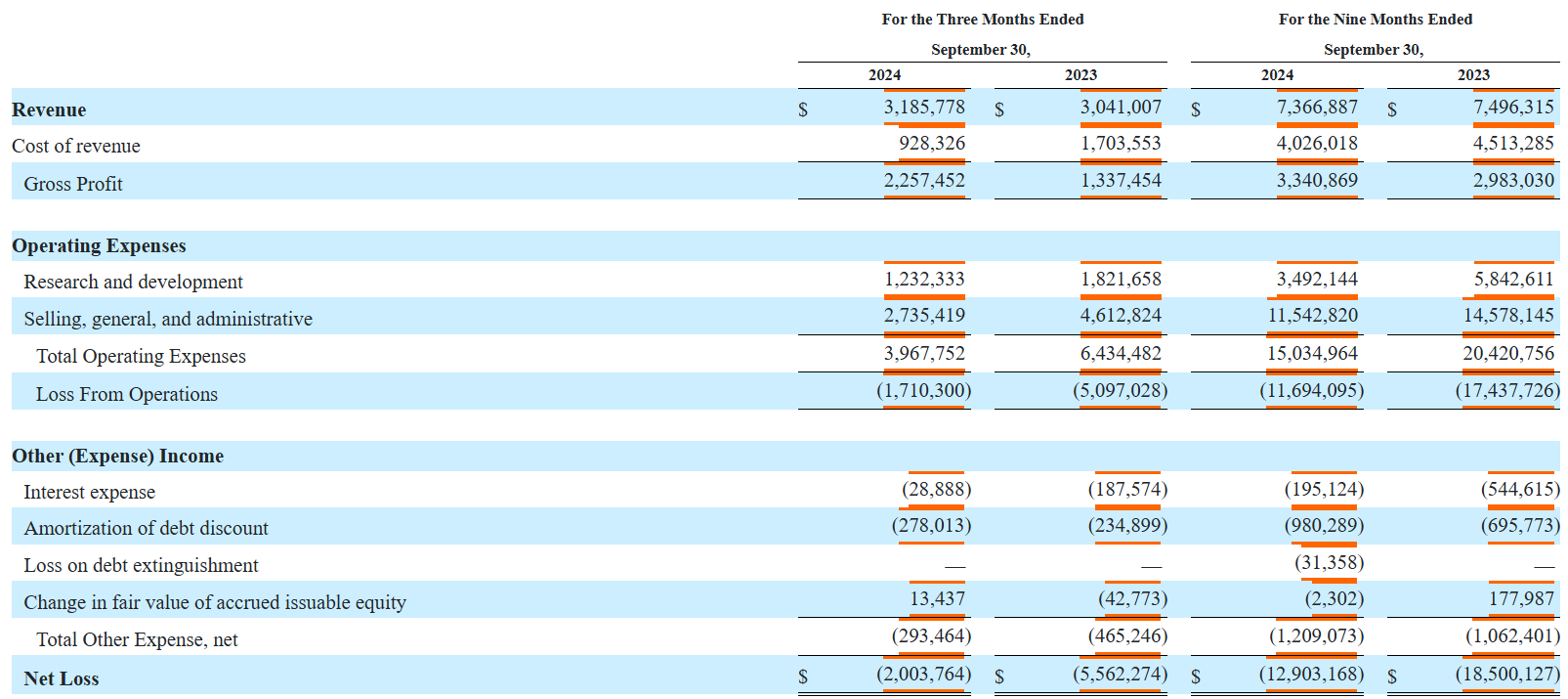

Note that as of Q4 2024, which is the latest available financial reporting period, KULR posted a $3.54 million loss from operations on $3.37 million total revenue.

One could argue that the company has been improving its financials year over year. However, the company is still currently in its growth phase which at that point, and with what promises management has been feeding to investors should be, should be exponential. The fact that the company is already cutting workforce and costs while its revenue has been stagnating year over year does not make us very hopeful for the future.

As we will show in the next section, not only did the anticipated revenue opportunities have not materialized, but the much-publicized customer interest has also not led to the expected growth.

KULR Struggles to Attract and Retain New Customers

Management has frequently emphasized that all their products generate significant customer engagement and interest. In 2022, during the Q2 earnings call, they reported customer interest across several verticals and noted a 30% increase in their active sales funnel. They also stated:

“(Significant Customer Interest) which amassed to a total of over 300 enterprise and government organizations in our sales pipeline…”

“We’re confident there will be the inevitable ramp in sales volume as we begin to recognize these customer engagements from a revenue standpoint over the coming quarters.”

“We already have multiple customer engagements in the pipeline as 3 purchase orders are expected to close in September 2022.”

However, KULR had only 36 paying customers in 2022, 53 in 2023 and 71 in 2024. This modest customer base also exhibited high revenue concentration: 87% of KULR’s 2022 revenue came from just three customers, and 60% of its 2023 revenue was generated by only two customers. In 2024, this number was reduced to 25%, which was again proudly announced by management during the Q4 2024 earnings call. However, what management did not disclose directly is that during the Q4 2024, KULR only got 6 product sales customers and 4 service revenue customers. Note that during Q3 2024, KULR had 20 product sales customers and 17 service revenue customers, which means that more than 70% of KULR’s customers from Q3 2024 did not follow up with new orders in Q4 2024. Again, management deliberately called this quarter a “record quarter” when it is quite a disaster. As we show in this section, former employees’ experiences in sales at KULR have been corroborating all our findings.

Despite these figures, management is continuously promoting the idea of strong brand recognition and customer demand. They even mentioned reducing marketing costs as well as not needing any additional prospecting initiatives from their end to engage with new customers:

“One of the things that we’ve been able to do is really cut some of our marketing costs. And the reason we’re able to do that is we’re starting to get very good brand recognition out in the industry. And we’re getting to a point now that we’re kind of full, if you know what I mean. We’re really not having to beat the doors down of other OEMs.” (Q3 2023 Earnings Call)

Yet, the most recent available data still shows a different reality. Although revenue concentration decreased somewhat over time, a few customers still represent a huge portion of KULR’s revenue, and these key customers never happen to be the same from quarter to quarter. Moreover, revenue per customer remains low, suggesting that customers who try KULR’s products may not be fully satisfied or sufficiently interested in continuing long-term engagements.

Again, formers that were directly involved in sales told us damning facts about the company. One of them was allegedly laid off along with other employees including the head of operations, for “lack of work available.” According to him, the reason was that KULR was not capable of taking on new business:

“Yeah, I could tell you why they let me go. And the reasoning they gave me was lack of work available to me. Yeah, so that was what they told me and I was in sales. I don’t know what that meant. My only job was just trying to bring in new business. So I don’t know how there was a lack of work available to me. It kind of made it seem like they didn’t have the operational know-how to even take on new business because, you know, projects, like I said, customer projects were delayed when I was there. Things were not being done on time. So that’s what I thought was like, hey, we can’t even, even if you guys did this, we wouldn’t be able to say yes to it.”

The mismatch between their hiring strategy and the reality of their business also shows weakness in the overall management of the company:

“Yeah, I mean that was happening only because when they hired me, they kept telling me how badly they needed someone. Like I went into the interview and then before I even got home and like drove home, they offered me the job. Like, we really need to start, like get going, really excited about this. And I only lasted like seven, seven months. And then they had no work for me to do. So they were a mess. And like I said, they had just let go of the head of operations. And the more I check on LinkedIn now, everyone I worked with there is gone. So I don’t know what’s going on.”

Combined with the rest of the business operations’ weaknesses that we mentioned, the reason why revenue decreases along with the poor customer retention appears clear, KULR deeply lacks efficiency and attractivity.

DoD Contracts Show Limited Enthusiasm From the Government

KULR has historically worked with various branches of the U.S. Department of Defense (DoD), even prior to its IPO. The company often highly publicizes these DoD contracts and highlights a longstanding relationship with NASA, as well as one recent substantial contract with the U.S. Army. However, publicly available data suggests that the DoD does not share the same level of enthusiasm. Indeed, prime contracts awarded by the DoD to KULR have been very limited, as shown by data from USASpending.gov.

Most of the recent revenue linked to DoD-related contracts has come from “Subawards,” which, in some instances, the company did not fully disclose as subawards but as direct contracts from the DoD. These subawards are subcontracting arrangements in which KULR is paid by a primary DoD contractor already working on a government project. Although subcontracts in large DoD projects can be worth tens of millions of dollars, KULR’s specific portions typically represent only a small fraction of the total contract value.

While management has expressed particular optimism about a recent expansion of its contract with the U.S. Army, the company once again appears to be presenting lofty projections. During the Q3 2023 Earnings Call, management stated:

“The prototype production likely start late 2024, into 2025. We started with Army on airborne and UPS applications… So once we can prove out the lithium-ion battery that we produce to them is safe and meets their energy needs, we believe the opportunity opens up from the current approximately $100 million opportunity for these applications to a much, much larger opportunity across the Army platform.”

Yet, comparing such statements with the available DoD data highlights a significant gap between management’s projections and the actual contract values.

According to a former employee, most of the recurring contracts come from the DoD, which, in itself, is not a bad thing. However, the fact that it is essentially failing to attract non-governmental customers from the many markets it has courted is worrying. Moreover, as the former also pointed out, what the company has been offering NASA is mostly battery screening, which is according to him hardly scalable:

“So, like they somehow land these big clients. But like you said, they don’t, they don’t land a lot of new customers and keep them around. Right. So I think they just kind of are really reliant on those big government contracts with NASA and Army and stuff like that. No, I don’t know how scalable that is like you said. But that’s what I would have old year when I left.”

“And so we, they did, they invested a lot of money in that like testing room machine thing to send NASA, you know, space grade batteries. But other than that, other repeat customers or. I didn’t see many.”

Moreover, the scalability and real opportunities that lie in that segment are vague, as we show in the next section, the actual amount of revenue derived from their main recurrent partner, NASA, is quite underwhelming.

Limited Results from NASA Contracts and Partnerships

For as long as its press releases go back, KULR has repeatedly touted its technology and commercial relationship with NASA.

In July 2024, the company announced its largest contract to date: an initial $400,000 order, with total orders potentially reaching $2 million over several quarters.

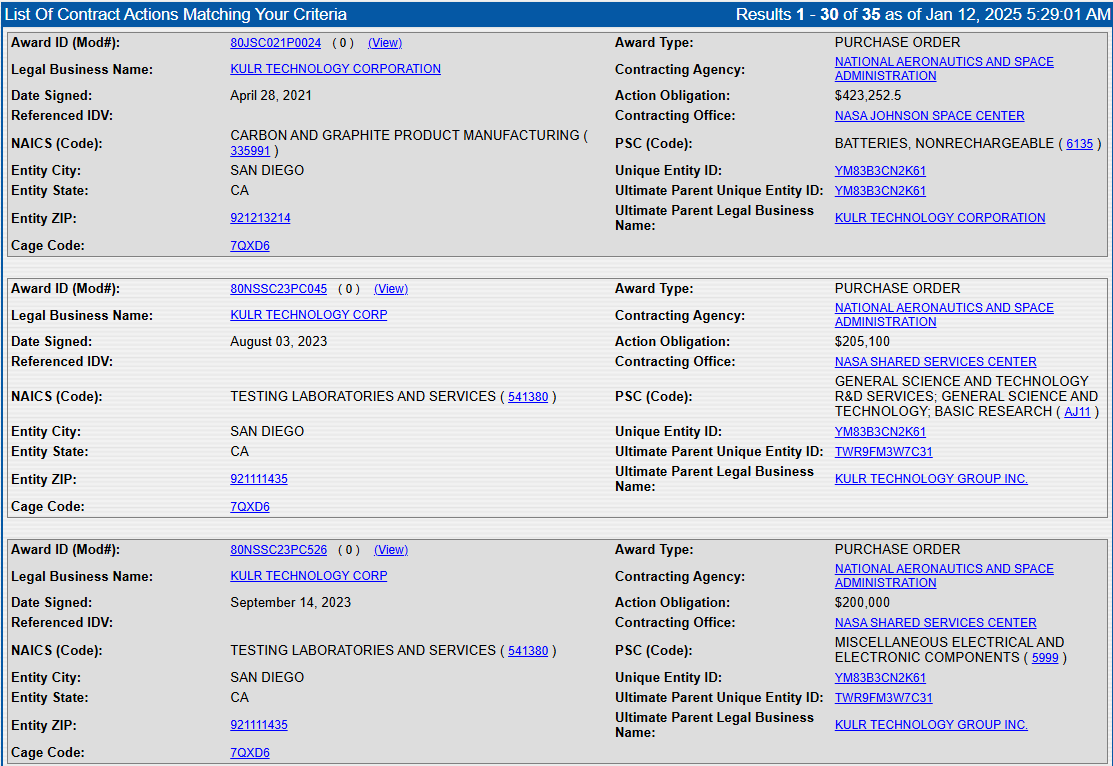

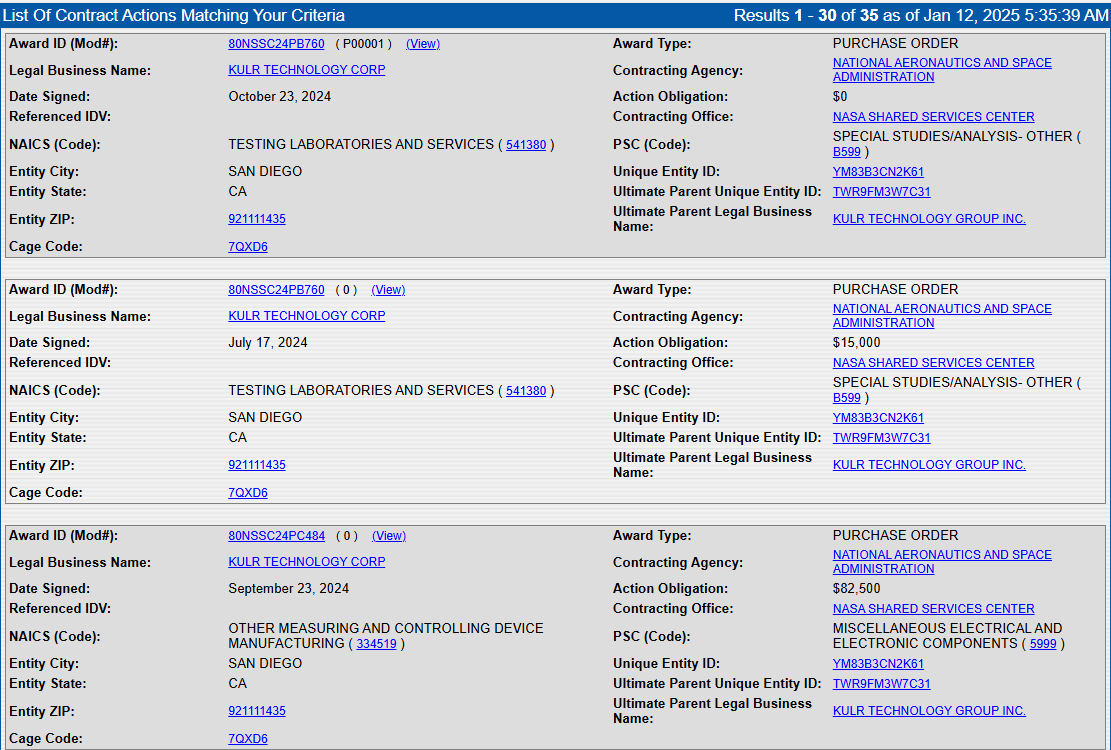

However, a review of current and historical NASA contracts reveals that none have produced substantial revenue or major achievements. Out of all contracts listed in the Federal Procurement Data System (FPDS), only five show an obligation (purchase order) exceeding $100,000. The largest is $423,252.50 in 2021, as seen in the corresponding records.

Surprisingly, the three contracts listed for fiscal year 2024 do not come close to the figures announced by KULR in July 2024. In fact, the company only received $15,000 in July 2024 for “Testing Laboratories and Services” and $82,500 in September 2024 for “Other Measuring and Controlling Device Manufacturing,” both far below the supposed multi-million-dollar order projections.

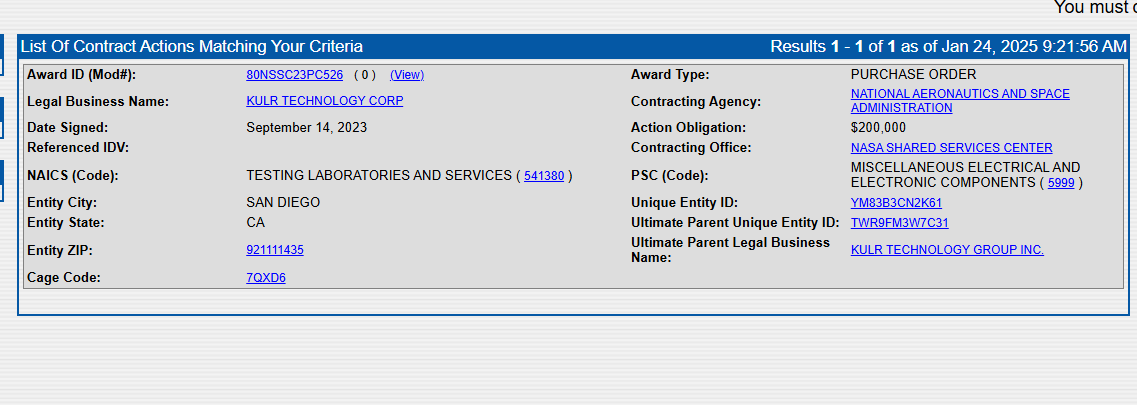

Another instance where KULR has been purposefully opaque in its disclosure with its contracts announcements can be found in a press release dated August 31, 2023. This press release announced a purchase order from NASA with mouth-watering numbers and statements including:

- Testing 10,000 LG Chem Lithium-Ion INR18650 M36T cells.

- Global battery cell testing market was valued at USD 5 billion in 2021 and is projected to reach USD 7 billion by 2030.

- KULR plans to expand its technology to support 21,700 cells by the end of the year.

- This partnership reinforces KULR’s role in aerospace energy management and battery safety.

The press release comes with a link to “SAM.gov” and gives some details about the order. However, it does not give many details compared to the FPDS database, an interesting choice from the company. Using the FPDS database, we find that this order is only “$200,000” total while the company is throwing around numbers such as “10,000 cells” ($20 cost per cell tested) and that the whole market for battery testing was valued at $5 billion in 2021. Again, KULR engages in opaque and misleading communications about its contracts while omitting important details that are publicly available information.

More Questionable Claims About Revenue Opportunities?

Subawards are no exceptions to the rule either, as shown with this announcement from October 4th, 2022:

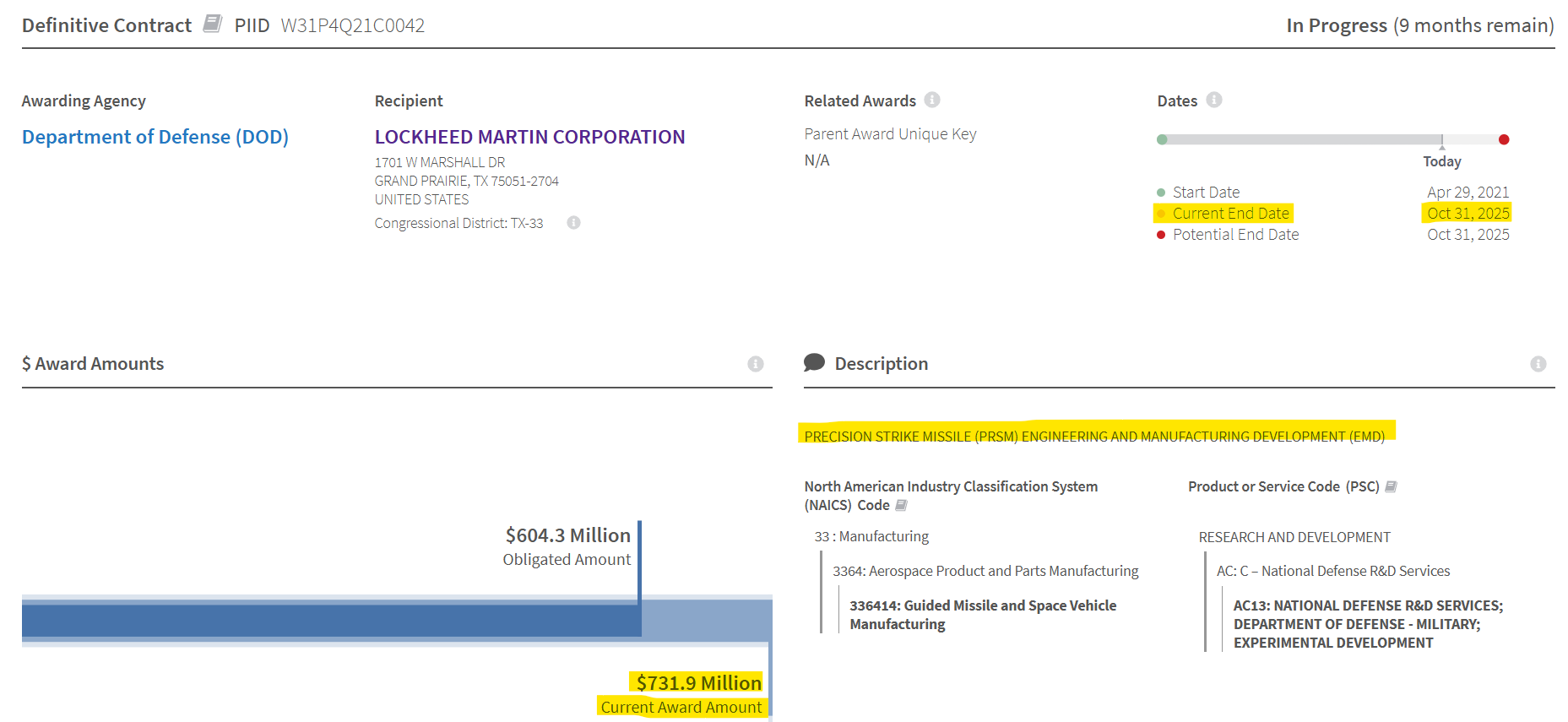

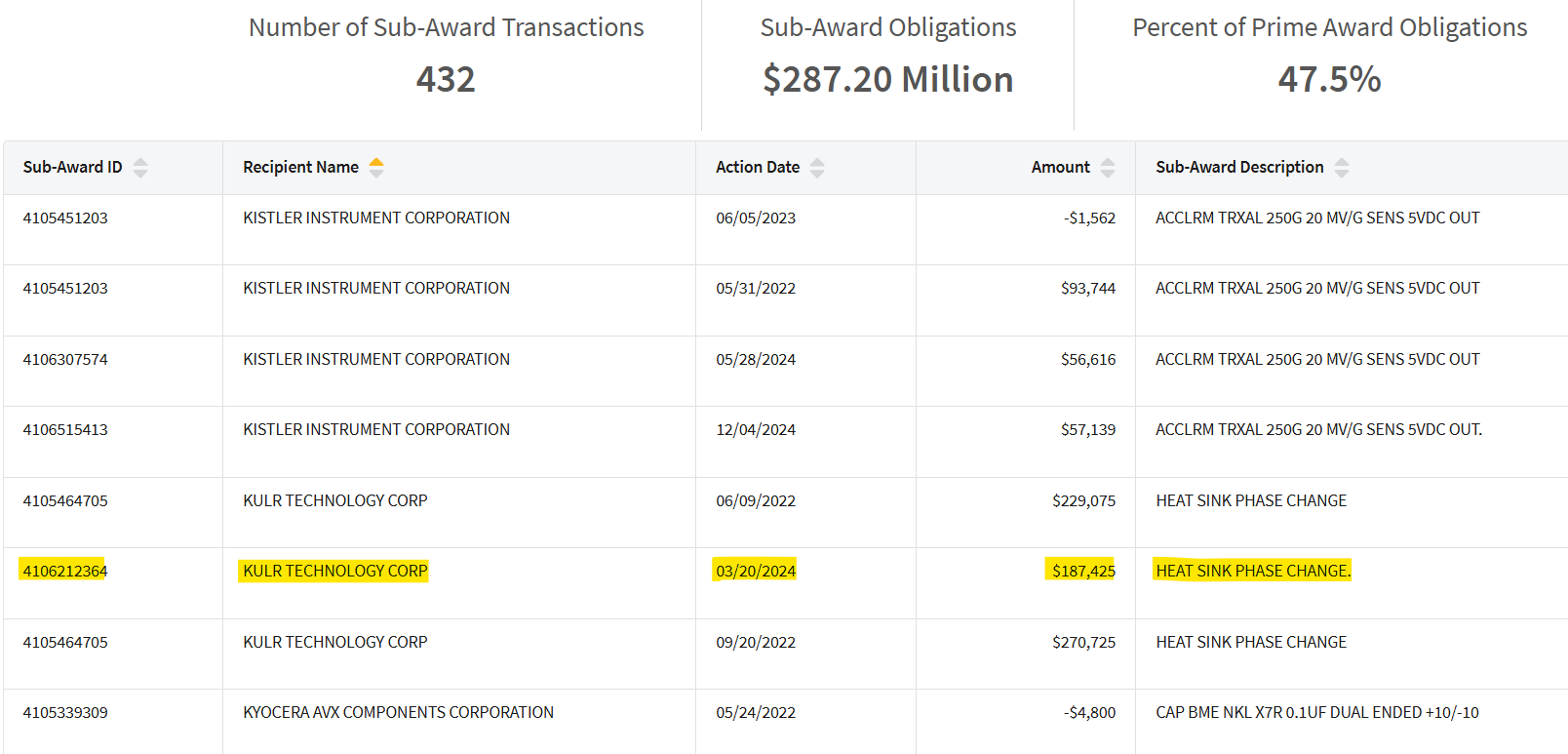

“It has received an initial deployment order totaling over $500,000 from a leading Department of Defense (DoD) contractor, with future considerations up to the multi-million-dollar amount over the next year. KULR’s technology will be utilized by the American manufacturer of spacecraft components and instruments for national defense, civil space and commercial space applications to support its Air-to-Air Missile shipping program.”

Since the announcement of what was described as a potentially substantial contract for KULR, only a single subaward amounting to just over $187,000 has been allocated to the company besides the $500,000 other two subawards that correspond to the initial order. The Department of Defense (DoD) contractor in question is “Lockheed Martin Corporation,” as indicated by various government databases. Despite KULR’s claim of a “potential for a multi-million-dollar deployment order to run through 2023,” the total funding received is still below $200,000 more than two years after the initial announcement.

Additionally, 432 subawards were issued under this program, which currently stands at $731.9 million. In contrast, KULR has managed to secure only a small fraction of these multi-million-dollar contracts, with its subawards largely overshadowed by others worth tens of millions of dollars.

Note: The other two subawards under this program total $499,800, which roughly corresponds to the initial order of “over $500,000.”

These apparent misrepresentations through high-profile press releases help explain why the company repeatedly misses its own revenue projections by more than 50%.

Most notably, since that press release, KULR has not received any additional awards or subawards related to missile programs, despite announcing a follow-on contract in November 2023 valued at over $8 million.

“Receipt of a follow-on contract from a leading Department of Defense (“DoD”) contractor for advanced thermal management systems in a next-generation air-to-air missile program. This contract signifies KULR’s expanding position in the defense sector as the Company anticipates consistent demand for its solutions through 2030, opening avenues for additional opportunities in similar fields. The multi-year follow-on engagement has an estimated total contract value to KULR of over $8 million.”

In our view, this announcement holds limited credibility considering the actual outcome of the contract it purportedly “follows on from” as well as the current lack of any order despite the company claiming that it anticipated a consistent demand from the contractor.

Fortunately for the company, which recently announced additional DoD contracts, most official award data remains undisclosed until 90 days after the award date. This delay may temporarily obscure the contract’s real value and terms.

Most of KULR’s Press Releases Are Only Fluff to Keep Investors Excited and Do Not Have Any Substance

Besides press releases that provide absolutely no substance, no revenue opportunities and only buzzwords that portray a situation where KULR has products adapted to every hot sector, such as AI and Space Batteries, we also notice a pattern where the counterparties of all these partnerships do not communicate in any way about it. It is always one-sided or with an insignificant partner.

As we mentioned earlier in this report, KULR has been posting an absurd number of press releases. Naturally, many of these are about partnerships on technology development and other collaborations. We question whether KULR can effectively manage its partnerships, given that its total workforce is only about 60 employees, which decreased in 2023 and 2024.

The formers we interviewed also shared our view of that misleading “communication” strategy, even admitting that besides the battery testing services, no product was really selling. This perfectly matches the company’s recent product segment decline of 54% during the past nine months.

“Yeah, I would say 90% of the products are fluff. It’s mostly just their testing services and their testing capabilities that are what people come to Cooler for. And they’re consulting, I guess like since we had all those NASA engineers, like a company designing battery cell would kind of come to us, test it with us, and then like, you know, we’d help them with like, you know, advice and stuff like that on their battery pack. But other than that, no products I could really remember selling that much of.”

Comparing the content of recently released PRs with the actual truth, and unsurprisingly, it is underwhelming to say the least.

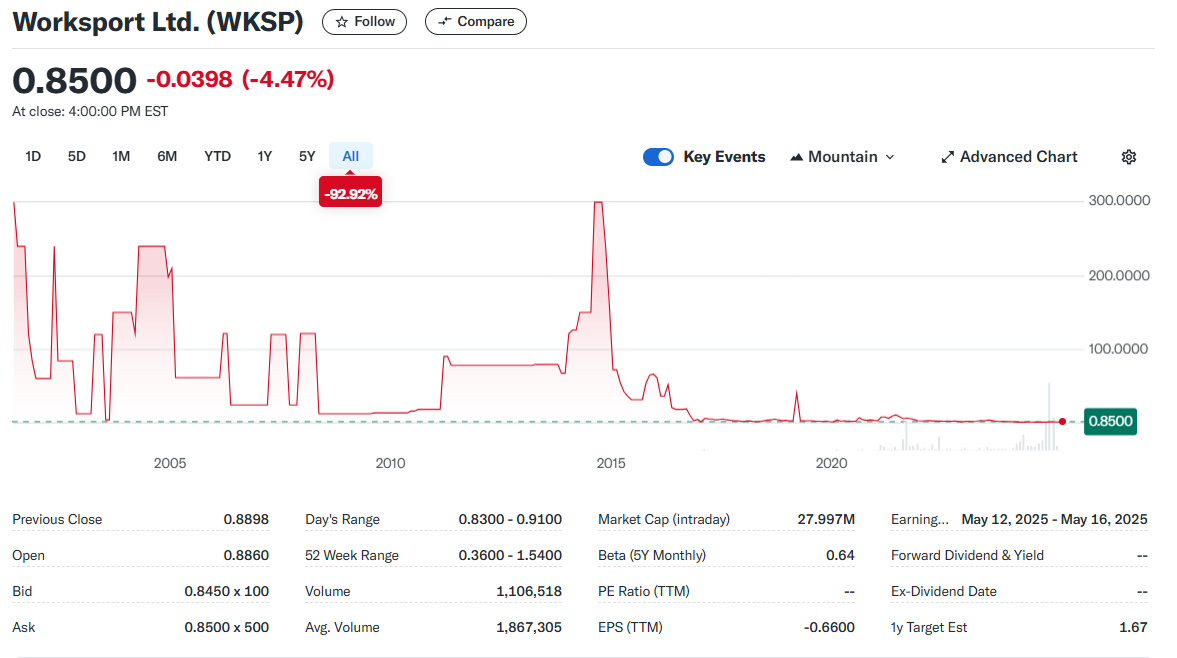

One of the most recent PRs issues by KULR is about a partnership between the company and “Worksport Ltd,” listed on the NASDAQ under the ticker $WKSP. Besides, once again, all the “opportunities” and buzzwords “AI,” we find that Worksport is in reality just a $16 million market cap company on the brink of bankruptcy.

Worksport stated in their latest 10-Q that:

“The Company has evaluated whether there are conditions and events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern within one year after the date the financial statements are issued. Still, certain factors indicate the existence of a material uncertainty that cast substantial doubt about the Company’s ability to continue as a going concern. The accompanying financial statements do not include any adjustments that might result from the outcome of this uncertainty. These adjustments could be material.” (source)

We do not see any added value from this partnership in the future, given the desperate position in which WKSP is found at the moment. Our best guess is that both companies agreed on a “partnership” without much hope to be able to release an additional fluffy PR that will benefit both of their stock prices only.

Another quote from one of our interviews with a former employee corroborates our suspicion of such a scheme, with one partnership that was announced in 2023 with Cirba, which is still displayed on KULR’s website as an important partner:

“And, but Like I said, that was like on our website being sold as if it was ready, but it was never ready when I was there. And I think we just did other work, like referral work with Cirba. Like that was it really. But I don’t think it was much.”

When it comes to surfing the hype wave and its buzzwords, KULR excels, but is still unable to add much substance to their business and financials through them. As the next few press releases and their analysis show:

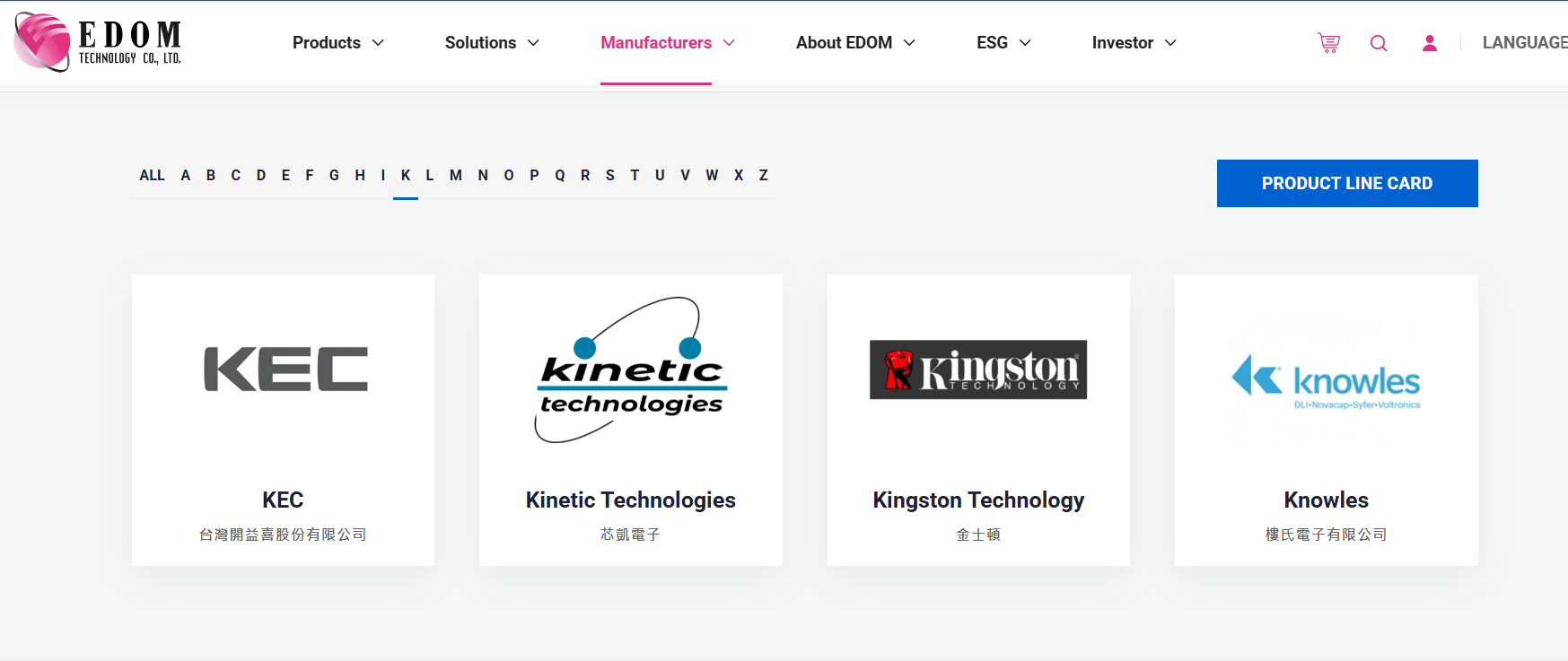

“(NYSE American: KULR) (the “Company” or “KULR”), a leader in advanced energy management platforms, today announced its strategic partnership with EDOM Technology (EDOM) (3048.TW), a long-standing NVIDIA Channel Partner and a premier integration and distribution company. This collaboration positions KULR to deliver its innovative KULR Xero Vibe™ (KXV) and KULR ONE product lines to Taiwan, a global epicenter of AI supply chain development, by leveraging its suite of energy management products and solutions to address the need for large-scale systems cooling within the AI ecosystem.

The partnership will enable KULR to service both server and edge computing devices within the AI supply chain while deploying its suite of energy management products and solutions to meet the needs of the entire AI ecosystem. By aligning with a strategic partner like EDOM, KULR is positioning itself to address the global surge in demand for AI infrastructure, fueled by initiatives like The Stargate Project making a recent $500 billion push to accelerate AI infrastructure expansion in the United States”

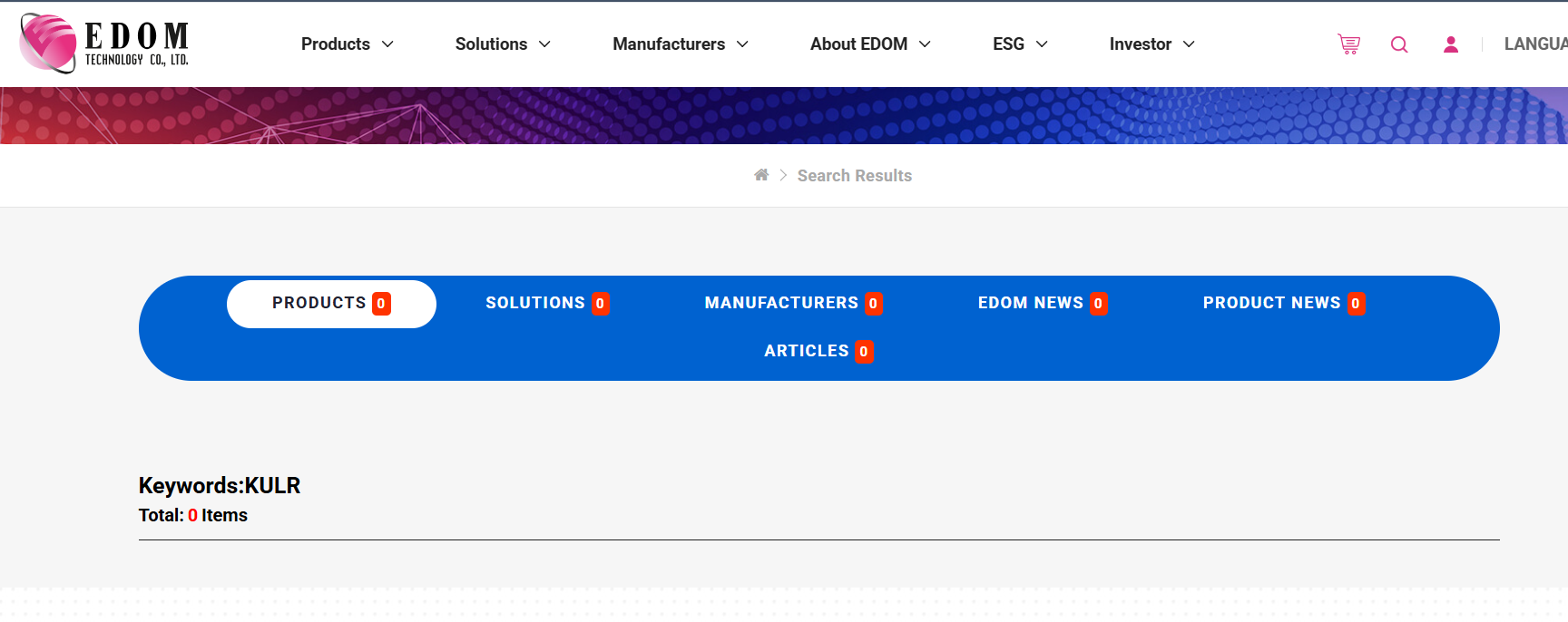

First, KULR is still to appear on EDOM’s website in their manufacturers section. EDOM already lists hundreds of manufacturers, including many other battery companies such as Enovix. Additionally, there are no PR about the partnership on EDOM’s side, despite many articles and news about their partnership and other events with their manufacturers.

Similarly, with this other PR: KULR Technology and Scripps Research Collaborate on Novel Pyrolytic Carbon Electrode Technology

“A global leader in carbon-based thermal management and battery safety solutions, has announced an innovative collaboration with the prestigious Scripps Research Institute’s Baran Lab. Together, the teams have developed a groundbreaking pyrolytic carbon (PC) electrode material, poised to transform synthetic organic electrochemistry.”

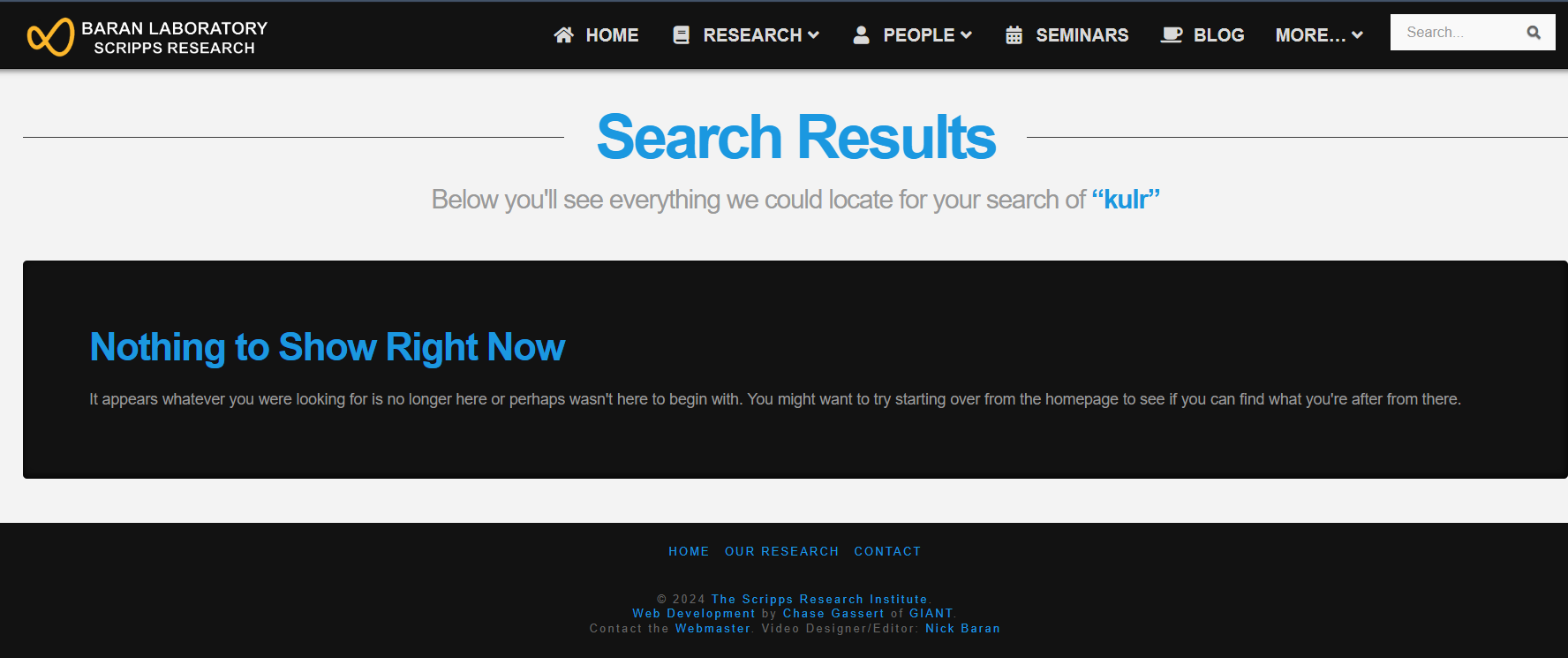

Despite being a small research laboratory with less than 40 people and an actively updated website, we do not find any trace of that collaboration with KULR on their website. To us, this is another sign of an insignificant and fluffy press release.

But KULR sometimes pushes the fake narrative a little too far, as shown with this recent press release announcing “the signing of a multi-million-dollar licensing agreement with a new technology partner (“Licensee”) to enable advanced carbon fiber cathode applications for nuclear reactor systems in Japan.”

The counterpart is most probably Company | EX-Fusion / en which is a startup and does not have any real product at the moment besides a non-approved design and a few partnerships. They raised a total of $12 million to date:

“OSAKA, Japan—(PRNewswire)—EX-Fusion announced today the close of an over-subscribed $1.8 billion yen seed-round investment designed to accelerate the commercial development of laser fusion technology. EX-Fusion has raised 130 million yen to date, and this latest financing will bring the total amount raised to 1.93 billion yen.”

Even though the terms of their licensing agreement might match whatever they announced in the press release, it is highly deceptive as the company will see no revenue for many years, if that startup ever gets to the stage where they’d need KULR technology. Moreover, that licensing agreement would surely need the commercialization of the startup’s product to be a huge success to attain the “multi-million-dollar” revenue mark for KULR. This adds another thick layer of uncertainty and delay. The lack of transparency about the timeline is deliberate, as without providing it, investors are probably believing that revenue will be imminent.

KULR’s Recent “Bitcoin Strategy”: A Desperate Attempt to Maintain Hype?

In our opinion, KULR’s move toward a Bitcoin strategy signals another major red flag as it looks to jump to the next hype investment theme. Beyond the superficial appeal of cryptocurrency, this decision places the company’s already essential “surplus” cash (arguably vital to ongoing operations) at considerable risk, as the purchase was made near Bitcoin’s peak price. As of April 3rd, 2025, the company is sitting on approximately $9,770,000 in unrealized loss, or around 15% of its total bitcoin purchase so far.

The positioning of the company towards its Bitcoin holdings strengthens our beliefs that it is nothing more than a stunt to attract new gullible retail investors and get into the radar of investors wanting exposure to bitcoin via the stock market. As the CFO stated during the latest earnings call:

“We believe our Bitcoin Holdings will account for meaningful shareholder value over the long term. We don’t anticipate using our BTC holdings to meet normal course working capital funding and think we’ll have available cash on hand to meet those needs.”

Given the rate at which the company is burning cash, we could assume that the company will further dilute investors in the future to keep the operations going as most of its cash is now used in the “long-term bitcoin strategy”.

However, this also underlines a huge lack of growth opportunities for the company. Besides the word salad and bitcoin cope lesson that management used to avoid clearly answering analysts’ worries about such a huge potential cash lock-up, it appears clear that KULR has currently no plan or opportunities to acquire or invest in its business to boost its growth.

“So, our strategy is to be a long-term holder of BTC, Bitcoin, and we do not see a scenario today cause us to change that strategy.”

The sudden commitment to bitcoin expanding to bitcoin mining does not help the cause:

“Additionally, on March 7, 2025, the Company entered into a sixty-day Machine Lease Agreement with a bitcoin mining services company to operate 2,500 S-19 bitcoin mining machines on KULR’s behalf, at a total lease cost of $850,000.”

This goes beyond the initial “90% in surplus cash” as the company is effectively spending cash to get additional bitcoin via operational expenses. Given what we exposed earlier and the current operational situation of the company, we believe this to be a last resort trick in order to divert investors’ attention from the truth.

Note that the company heavily diluted its investor base by a gigantic 49% from December 2023 to March 2025. This was mostly due to its huge market offerings during the year 2024 and the period from January 2, 2025, to March 27, 2025, with a total of 94,168,827 shares issued for total gross proceeds of $113,034,988. In simple terms, the company almost doubled its share count from December 2023 to today.

We find odd that the company allocates so much cash to its strategy, without any foreseeable future plans to expand its operations, while one of their risk factors reads as follows:

“We have limited experience manufacturing our products. We have established small-scale commercial or pilot-scale production facilities for our carbon-based thermal management products, but these facilities do not have the existing production capacity to produce sufficient quantities of materials for us to reach sustainable sales levels. At present, we rely on outsourced partners to produce high volume products. In order to develop internal capacity to produce much higher volumes, it will be necessary to produce multiples of existing processes or engineer new production processes in some cases. We have begun building up the scale of our automated battery cell facilities in our leased facility in San Diego but there is no guarantee that we will be able to economically scale-up our production processes to the levels required. If we are unable to scale-up our production processes and facilities to support sustainable sales levels, the Company may be forced to curtail or cease operations.”

Note that “building up the scale of their facility” is a mere upgrade from its current state and would need significant capex in order to be relevant and substantial. However, we believe that the company simply does not have the demand for this kind of “sales levels”. The fact that sales have crumbled coupled with the fact that their total sales team is less than 10 employees, as disclosed by the company in the latest earnings call, and what the former employees told us gives us confidence in our observations and judgement.

Conclusion

KULR has consistently issued upbeat press releases, forecasting significant revenue opportunities and emphasizing crucial partnerships, notably with the Department of Defense and NASA. However, the data shows a persistent trend of underperformance relative to these public announcements. Despite management’s assertions of a growing sales pipeline, the company’s actual customer base remains small, highly concentrated, and vulnerable to attrition. Most of the revenue related to the DoD appears to come from subcontracts, which only account for a small portion of the total program value. This raises doubts about KULR’s claims of securing multi-million-dollar orders in the near future.

Additionally, the company’s venture into Bitcoin—a strategy often linked to financially struggling organizations seeking quick speculative profits—further complicates concerns about resource allocation and long-term sustainability.

Overall, these findings present a picture of a company that has yet to show meaningful commercial progress or transparent, sustainable growth. Investors should pay close attention to the disparity between KULR’s public statements and its reported financial performance when evaluating the company’s future prospects.