Read below or open PDF version

- Electro Optic Systems Holdings Ltd (ASX: EOS) is an Australian developer and manufacturer of advanced electro-optic systems, including remote weapon systems, surveillance and fire control systems for military customers. EOS’s stock price doubled in mid-December 2025 on the back of the announcement of a major contract with an anonymous Korean counterpart. Investors see this contract not only as validation, but also as a major contributor to EOS’ revenue growth going forward.

- While investors are speculating about the identity of the big Korean counterpart to this contract, we found proof in local Korean media articles that the counterpart is a company called “Goldrone Co., Ltd”.

- A closer look at Goldrone makes us believe that the contract announcement is intentionally misleading and utterly unrealistic. Goldrone is a tiny agricultural drone company that seems to lack the resources to buy US$80 million worth of products and services from EOS.

- Our research into Goldrone shows that:

- Revenue peaked at US$476,000 in 2018 while incurring a US$400,000 net loss.

- The company seems to have only three employees and operates out of a restaurant complex.

- Goldrone business activity and announcements have died down over the years after multiple failures, leaving the impression of a currently defunct business.

- Goldrone is currently attempting to raise around US$343,000 to stay afloat.

- We find the statements that EOS made in the investor call dedicated to the new Korean contract announcements aggressively misleading, and sometimes bordering on outright lies.

- Amongst other things EOS management stated on the investor call regarding the acquisition that “in most defense deals, the counterpart does not want to be nominated” and that “for the time being, they asked us to keep silent, keep it confidential and we respect it”. Goldrone is neither a defense company nor does Goldrone appear to be coy about the agreement, as Goldrone itself made a detailed public announcement about this contract and it was covered in local Korean media.

- EOS was previously investigated and recently fined by Australian regulators for shoddy disclosures. EOS seems to have been under pressure to deliver tangible progress to investors and EOS sold its apparently only profitable business unit in 2024 and losses are mounting.

- Our research in the acquisition of MARSS by EOS in January 2026 uncovers a multitude of issues. We believe management has lied about past revenues and is misrepresenting the economic opportunity of this acquisition.

- We find the sizable contract announcements of EOS during 2025 highly questionable and management’s statements about them misleading.

- In conclusion, we see a dishonest management team that will soon fail under the pressure of its own lies and worsening financials.

Content

Introduction

Electro Optic Systems Holdings Limited (EOS), listed on the Australian Securities Exchange (ASX: EOS), specializes in designing, manufacturing, and exporting electro-optic systems for the global defense and space domains.

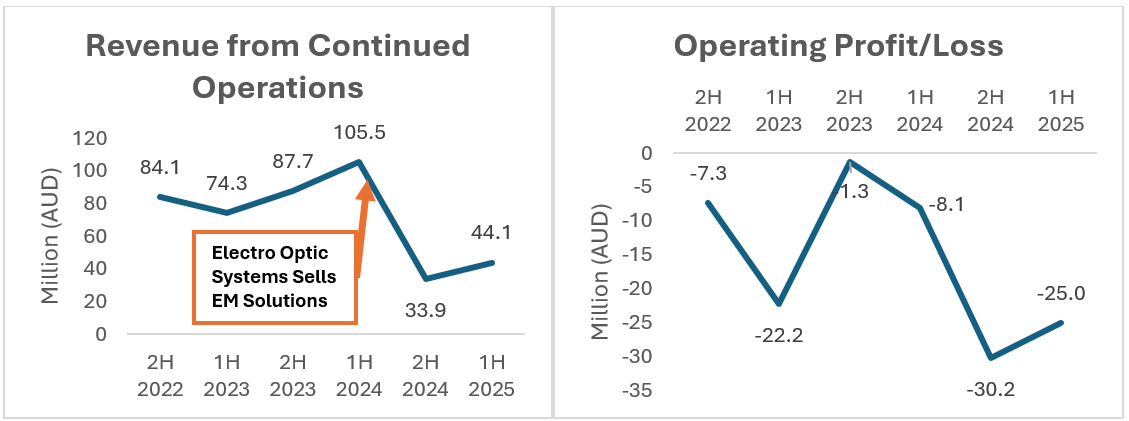

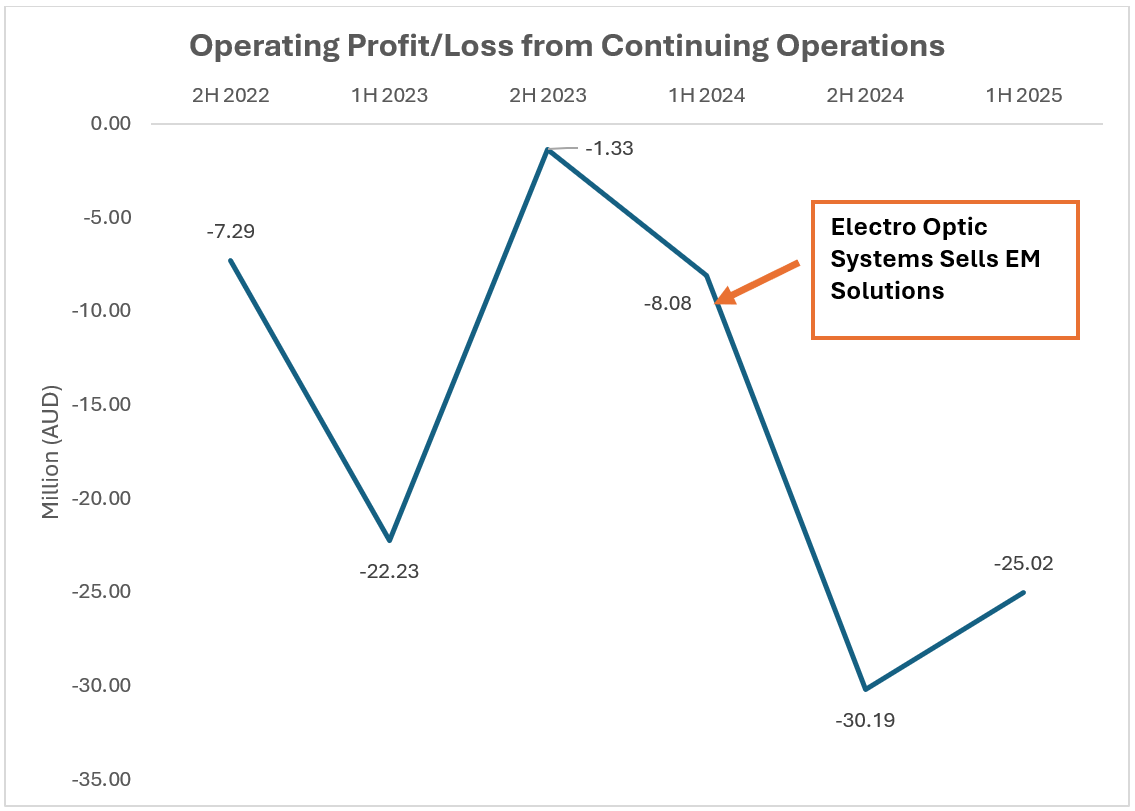

EOS financials have seen mounting pressure since EOS sold its only profitable business unit “EM Solutions” in 2024.

Source: Compiled from company sources/filings

Luckily for EOS, the company was able to secure an US$80 million contract with an anonymous Korean counterpart, which EOS proudly announced on December 15th, 2025. Investors seemed ecstatic as EOS stock price went up 50% on the two days following the announcement and approximately 100% over the next three weeks.

The identity of the Korean counterpart has been subject to investor speculation and was never officially disclosed by EOS. We identified the Korean counterpart as Goldrone Co., Ltd, a tiny company that seems to completely lack the resources to fulfill such an agreement. In light of our findings, we conclude that the Korean contract is but a smoke and mirrors show to mislead investors.

This is not the first time that EOS seems to have been dishonest as they were recently fined by Australian regulators over disclosure matters.

We also question the latest acquisition announced in January 2026 which is deserving of further scrutiny by investors and regulators.

The Big Bogus Korean Contract

On December 15th, 2025, Electro Optic Systems Holdings Limited (ASX:EOS) entered into “a US$80 million conditional high energy laser contract” with a mysterious Korean counterparty. This announcement, along with the investor call specifically held for it, supposedly came with other material and game-changing future opportunities for EOS.

EOS did not disclose any information about the Korean counterpart, despite being one of, if not, their most important contract at the moment, and despite direct investor inquiries during the Investor Call of December 16th, 2025. EOS implies that they cannot disclose the counterpart because of the sensitive nature of the defense industry. EOS’ stock price went up 50% on the following two days and 100% over the next three weeks.

We identified the counterparty through local Korean media articles as being “Goldrone Co., Ltd.” or “골드론” in Korean, a small agricultural drone company. We expose via a forensic in-depth analysis of Goldrone’s public filings, history, locations of operations, product portfolio, customer relations, intellectual property and shareholder complaints that this counterparty seems completely unable to satisfy such a contract.

A Korean local media called “Enewstoday” covered the contract signing and published an article on the same day as the announcement, along with a picture of what appears to be the signing ceremony. The picture shows EOS’ CEO and Goldrone’s CEO shaking hands.

Source: enewstoday.co.kr

Goldrone itself published an official notice on their website, shedding more light on the contract with EOS, and confirming that Goldrone is indeed the single counterpart to this transaction. The notice also contains a schedule for the future collaboration process with EOS, which matches with what EOS disclosed, confirming that it is indeed the US$80 million contract mentioned earlier. The following is the translation of selected passages from Goldrone’s official notice:

- “As a result, our company, in cooperation with the UAE defense-specialized company Calidus, has achieved a meaningful outcome of signing, with Australia’s world-class defense company EOS, the nation’s first contract for technology transfer and production of a 100-kW laser drone air defense system.”

- “Key steps of the project:

– On-site inspection and consultation of EOS’s production facilities in Singapore (2025.12.19. ~ 12.21)

– Proceeded with procedures for the establishment of affiliates and overseas subsidiaries (2026.1 ~ 2026.3)

– Preparation for global business structure and phased contract execution (2026.2 ~ 2026.4)

– Discussions on business cooperation with major countries such as North America, the Middle East, and Japan (2026.4 ~ 2026.6)”

Who Is Goldrone?

Goldrone is a small Korean agricultural drone company based in Jeollanam-do, a southern, rural region of Korea. Goldrone does not appear to be a defense-related company in any way, but the company develops and manufactures drones for agriculture purposes. They make “handmade” drones, sometimes in partnership with Korean universities.

We could not identify any R&D or manufacturing centers. Goldrone does not have industrial manufacturing capabilities, which stands in contrast to EOS statement during the Investor Call that the Korean counterparty is “an Industrial Player”. According to multiple local information providers, basing their estimates on the “National Information & Credit Evaluation” (NICE Group) as well as the National Pension Service and the company’s disclosure, Goldrone only has 3 employees.

Source: Goldrone website.

Note: As described by the company, the drones are for agricultural purposes. (Translated from Korean)

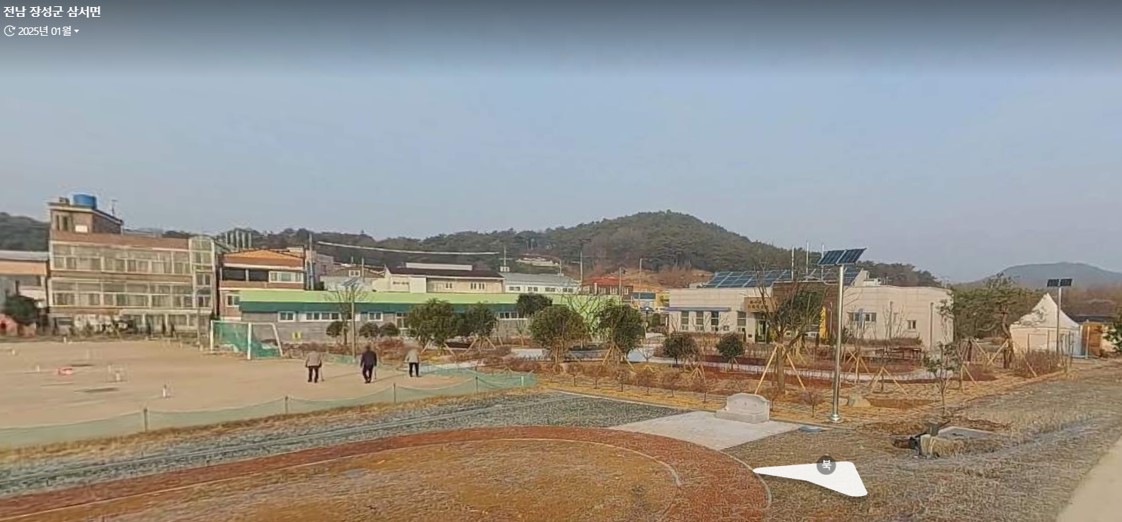

According to Goldrone’s website and filings, their headquarters’ address is: “1134 Haesam-ro, Samseo-myeon, Jangseong-gun, Jeollanam-do (2nd floor)”, which is in a two-story building above a random restaurant. Goldrone seems to hold annual meetings and sometimes Memorandum of Understanding (MoUs) signage in a small room, which we believe is located above this restaurant.

Source: Naver Maps, Streetview from October 2023

Source: Naver Maps

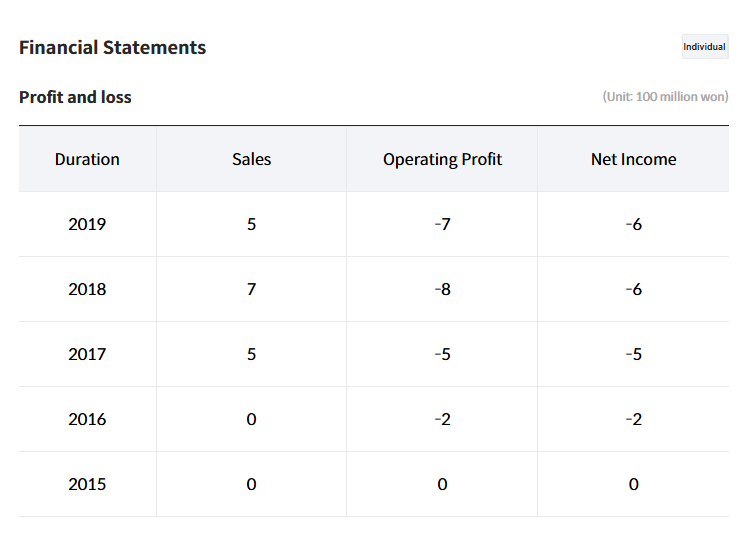

Goldrone is also a small company in terms of revenue. According to Seoul Exchange data (an Over-The-Counter exchange for unlisted companies), which also provides data for private companies, Goldrone’s revenue peaked in 2018, with only US$476,000 (₩700,000,000) in revenue, while incurring a loss of over US$400,000 (₩600,000,000).

Note: (Translated from Korean)

It seems to us that Goldrone has essentially stopped doing business since 2019. One quote we notice on the Seoul exchange website is “Trading will resume once the audit report for the previous fiscal year is confirmed”, which explains why the data ends in 2019, and strengthens our beliefs that Goldrone is currently almost idle.

It appears that, in 2019, Goldrone seized its previous drone certification and training activity, which we estimate has been material in terms of revenue for the company. Goldrone used to operate the training business behind the headquarters, in a small building with a training field as shown in the screenshot below:

Source: http://dronelicense.co.kr/ (Goldrone’s former drone certification website, which now appears to be inaccessible)

Enrollments for training classes were so low that the business seized to offer courses in 2019. The building now appears to be vacant, the Goldrone sign is gone, and the field is now used by the community to play “Gateball”.

Source: NaverMaps, StreetView from October 2023

Source: KakaoMap, Image from 2025

Source: KakaoMap, Image from 2025.

Note: 삼서면게이트볼장 = “Samseomyeon Gateball Field”

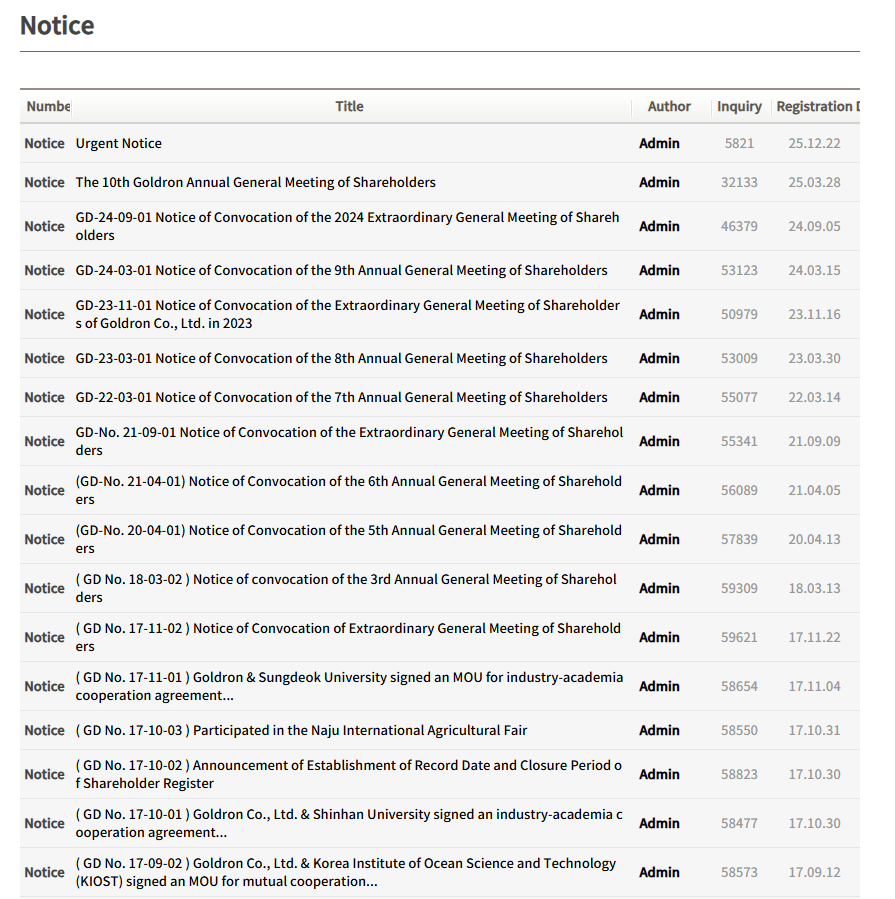

We also looked at Goldrone’s PR publications, and it appears that the company was actively growing its operations until 2018, engaging in partnerships with universities and small government programs/institutions. In the next few years, until 2020, we only observe few meaningless MoUs signing with local authorities or small companies. In 2024, Goldrone partnered with Plana, a small hybrid eVTOL startup, but nothing material came out of this partnership either, and it can only be found in local Korean news.

After 2017, the only official PR publications were for the annual mandatory shareholders meeting, until the announcement with EOS.

Source: Goldrone website

According to their own notice, Goldrone is trying to raise ₩500,000,000 (1,000,000 x ₩500 per share), equivalent to US$343,000 to go forward and finance the US$80 million contract with EOS. How is a company needing to raise US$343,000 suitable for an US$80 million contract and supposedly big future opportunities that investors value in the hundreds of millions?

Per Seoul Exchange Data, Goldrone currently has 15,400,000 shares outstanding, at ₩500 per share, the company is worth a total of US$5,236,000, a fraction of the contract size and even of the initial deposit. We do not know how Goldrone intended to raise enough money to pay for the $18 million deposit due by the end of January 2026. Unsurprisingly, in their Q4 2025 update, EOS admitted that “the customer has indicated that further work is required to finalize the arrangements” and therefore now “believes this could be concluded in February or March 2026”.

In our opinion, this contract is nothing more than a fake PR piece, abused by EOS’ management to fuel the hype and inflate their stock price. Goldrone had essentially no material operations and/or operational growth since 2018 and is suddenly signing contracts worth tens of millions of dollars with EOS? This seems to us simply fraudulent.

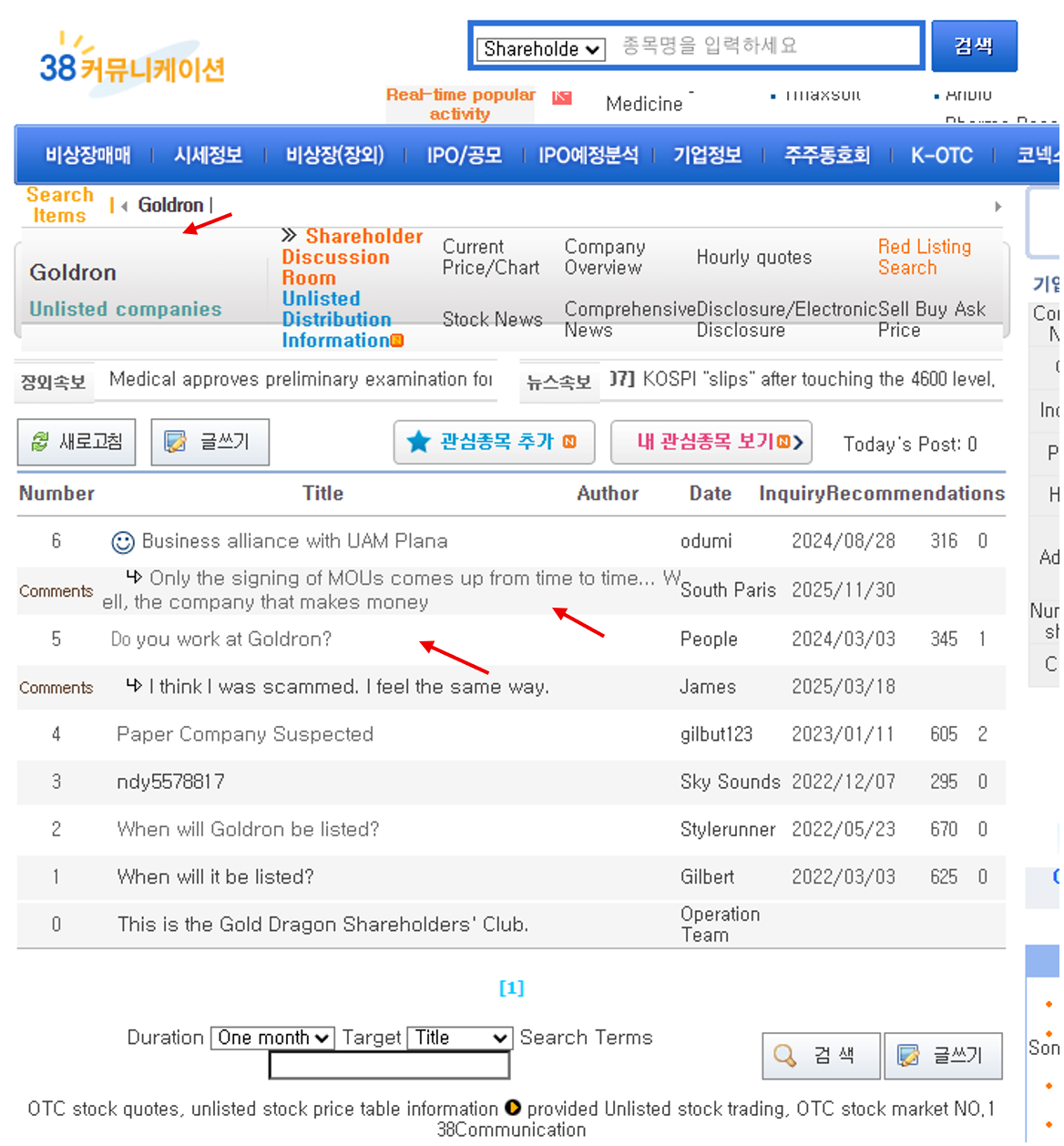

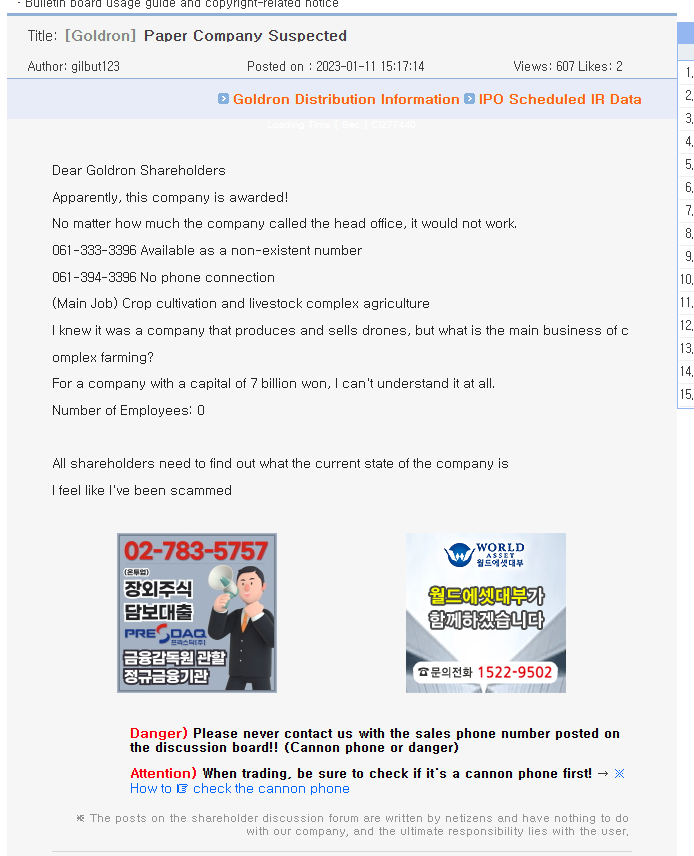

When looking into local Korean investing forums, we found testimonies of several of Goldrone’s shareholders who were confused about the situation and sought clarification. Some of them tried to call the company without any luck. We also tried to call the company’s number displayed on their website, but it is not even in service anymore.

Source: www.38.co.kr

Source: www.38.co.kr

Source: www.38.co.kr

In both the local Korean article and Goldrone’s notice, there is a mention of “Calidus” as an “introducer” between EOS and Goldrone. We looked deeper into this relationship to exclude the possibility that Calidus or another industrial player is financing the transaction in the background. We conclude that there is no active involvement of Calidus in this contract.

Calidus is a UAE defense company that has partnered with EOS in February 2025, the aim of this partnership is to help EOS manufacture their R500 RWS in the UAE. Calidus did not announce anything regarding the EOS-Goldrone agreement, whereas Calidus usually seems keen to announce new contracts. Calidus already has existing relationships with the Korean market. We believe that Calidus indeed made a simple introduction between EOS and Goldrone during a recent Korea/UAE defense event but has no involvement beyond this. It is also possible that their name is mentioned simply to add credibility to the announcement.

Calidus does not need a local partner like Goldrone, because it is already partnered with sizable Korean defense contractors, most notably LigNex1. The idea that a secret financing partner is behind Goldrone is also discredited by the numerous apparent falsehoods that EOS told investors about this contract as well as the fact that Goldrone is currently aiming to raise approximately US$343,000.

We Caught Management Red-Handed During the Investor Call

EOS management held a call on December 16th, 2025, to give more information about the new Korean contract. In light of our research, we find many statements by management to be gross misrepresentations, bordering on outright lies. Below are select highlights from the investor call we found especially misleading.

- The client is “an Industrial Partner”, and has evaluated all the international options but chose EOS. The first part is simply not true; the second part is highly doubtful.

- Thanks to this new contract, EOS claims it is now in a pole position for the future large procurement program in Korea. Management also added that “whenever there is a tender coming up in the future to have a great chance of winning this”. We find this a gross exaggeration.

- EOS management expects tenders to be for small batches (10, 20, 30 lasers) with a price of approximately A$45 to A$50 million for low-quantity orders and of approximately A$25 to A$30 million for higher-quantity orders. Here, management was touting possibilities of winning contracts in the multi-hundred million range from this counterpart, easily doubling their current backlog. We find this unrealistic.

- EOS’ Management also stated that they “will use the momentum of this contract to push to negotiations with a couple of other clients”. We believe potential clients will not be impressed when they learn about the identity of this counterpart.

- When EOS’ management was asked to give more details about the Korean counterpart, they stated that “in most defense deals, the counterpart does not want to be nominated” and that “For the time being, they asked us to keep silent, keep it confidential and we respect it”. This seems like an outright lie, given that the signing ceremony was covered by local news in Korea and that Goldrone itself made a special announcement about the contract.

We urge investors to listen to the Webinar Recording from December 16th, 2025 and judge in the light of our findings if this management team can be trusted.

The MARSS Acquisition, and More Questionable Statements From Management

On January 13th, 2026, EOS announced that it has entered into an agreement to acquire the MARSS group business, a Europe-based provider of command and control systems. The payment terms are as follows:

- Upfront cash payment of US$36m (~A$54m); plus

- Potential earnout amount of up to €20m for each €100m (or part thereof) of certain new MARSS third party contract orders (up to €500m) secured prior to the end of the earnout period. The earnout payment is capped at €100m (~A$174m), subject to adjustments and is payable in a combination of cash (capped at €20m) and EOS shares.

While management touted an immense opportunity arising from this acquisition during the call dedicated to the acquisition held on January 13th, 2026, they also made statements that we find to be completely void of sense. The statement that raised the most questions is from the CFO:

“MARSS has generated around 240 million EUR over 5 years”.

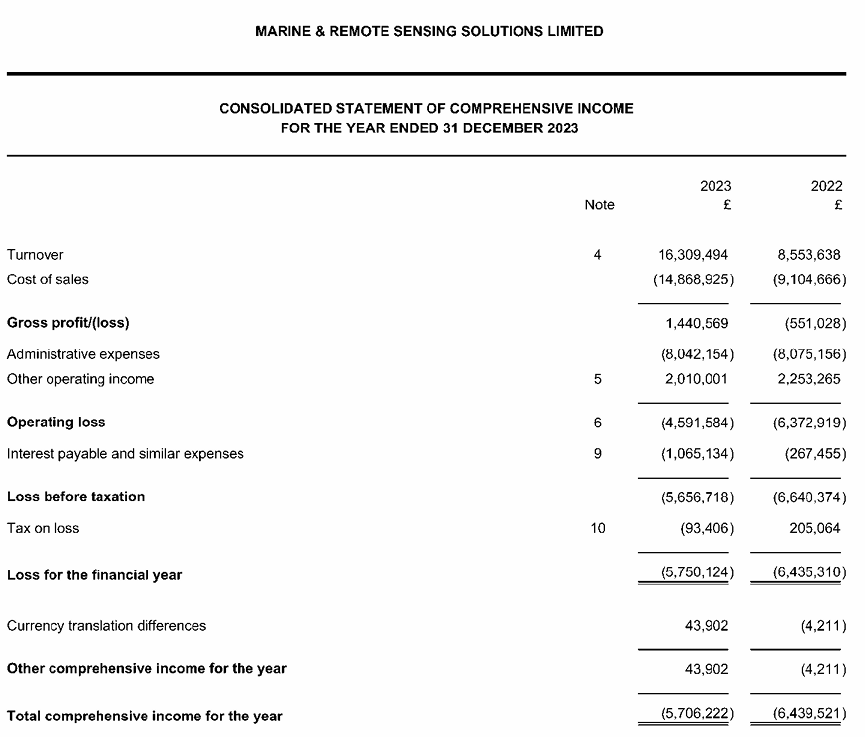

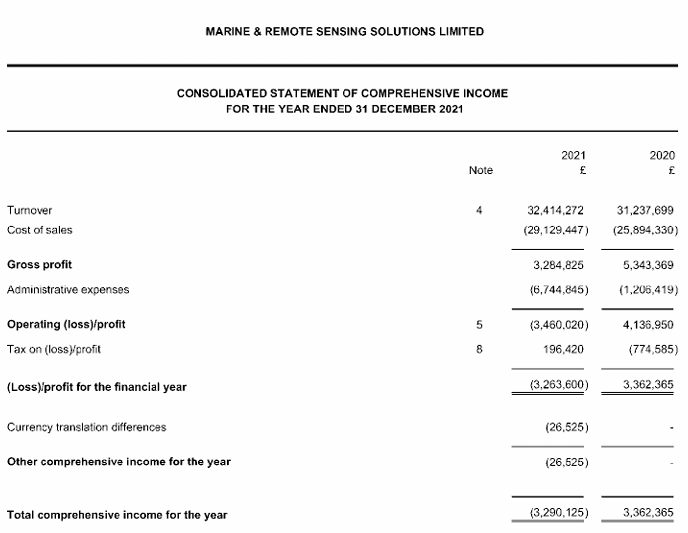

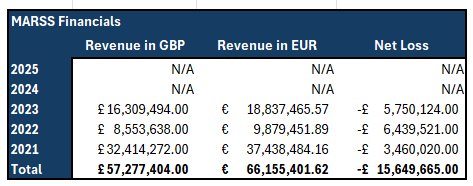

We found MARSS’ financials for their U.K. subsidiary which seems to be conducting all their operations, with reported revenue segments from the U.K. and “The rest of the world”. By reverse searching the name of MARSS’ CEO “Johannes Pinl”, we found MARSS’ “real name” which is “Marine & Remote Sensing Solutions”. Below are the screenshots for MARSS revenue for the years 2021, 2022 and 2023 (the other years are unavailable yet, the annual accounts for 2024 are overdue since the end of 2025).

Source: U.K. Companies House

Source: U.K. Companies House

By making a quick calculation, we clearly see that the statements around this acquisition do not make sense. If we consider that “240 million € over 5 years” is January 2021 to December 2025, and given that the company generated approximately 66 million € from 2021 to 2023, this implies that MARSS generated 174 million € in 2024 and 2025 combined, and therefore is experiencing an exploding growth.

Source: MARSS filings, Grizzly Analysis

As we can see from the filings above, the company has seen its revenue slashed almost 75% from 2021 to 2022, from 37.4 million € to 9.9 million € respectively. As the revenue for 2023 was 19 million €, even if the revenue doubled every year, it would not be enough to attain the number given by EOS CFO.

To make our point clear, MARSS would’ve had to post a gigantic growth over the last two years to attain those numbers. Funnily, it implies that MARSS 2025 revenue is likely higher than EOS’, while being acquired for 3% of EOS market cap. This begs the question, would a company that grew its revenue this much in the past couple of years agree to be bought for a mere 30.5 million €? (US$36 million). This simply does not make sense to us.

Moreover, in MARSS’ news feed, we do not see any announcement of big contracts or awards, which is in contrast with EOS management stating that MARSS got huge opportunities, while admitting that their backlog was actually “modest”. Besides receiving an LOI for a big project backed by UK Export Finance, MARSS did not disclose any new contract in 2025. MARSS usually eagerly issues press releases for its new contracts and their completion, even for smaller contracts like this US$4 million contract completed in 2024.

We believe management is misrepresenting the economic opportunities of this new acquisition to pump up the stock price.

EOS Under Pressure to Bring Good News to Investors

Back in November 2024, EOS announced that it would be selling its only profitable subsidiary called “EM Solutions” (EMS). The sale was completed for a total consideration of A$160 million on January 31, 2025. EOS stated that this transaction was a way for the company to raise capital so that they could execute their growth strategy as EMS was a non-core asset for them.

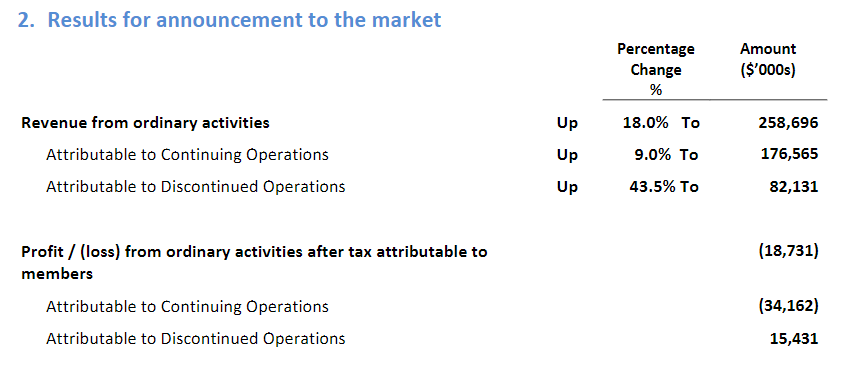

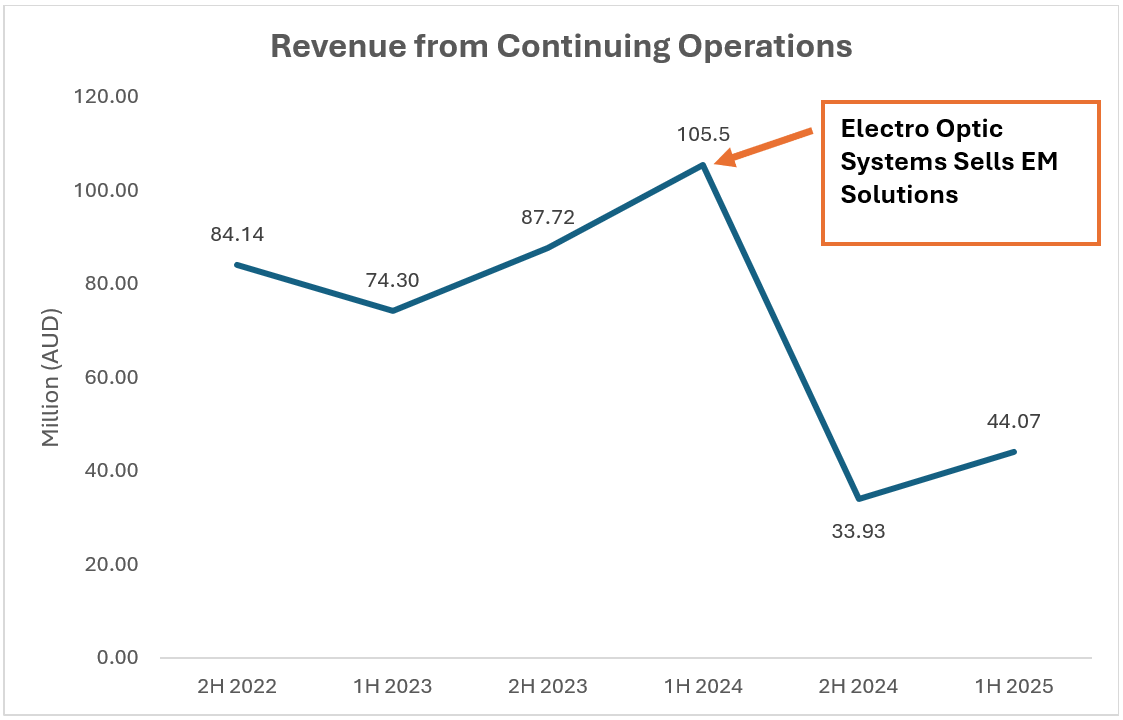

Though the company asserts that EMS was a non-core asset, the results post divestiture have implied that it was the asset that generated an outsized amount of revenue, growth and profitability for the company.

According to their full year 2024 financial results, the EOS only saw a 9% year-over-year increase in revenue from continuing operations, while EMS, saw an increase of 43.5%. It’s also revealed that EM Solutions was a profitable subsidiary, generating A$15.4 million in post-tax profit.

Source: Appendix 4E and 2024 Financial Report

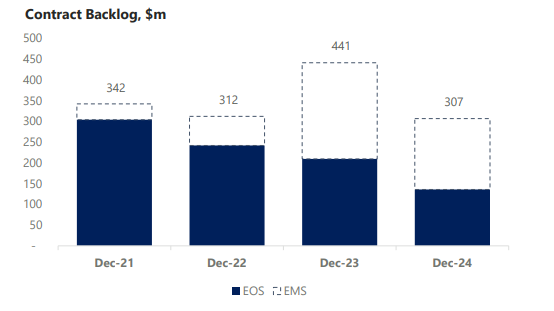

EMS was also a large portion of the company’s total backlog, in their full year 2024 results presentation they state that EMS contracted order book was A$171 million, counting for more than half of the A$307 million total contract backlog at the end of 2024.

Source: 2024 Full Year Results

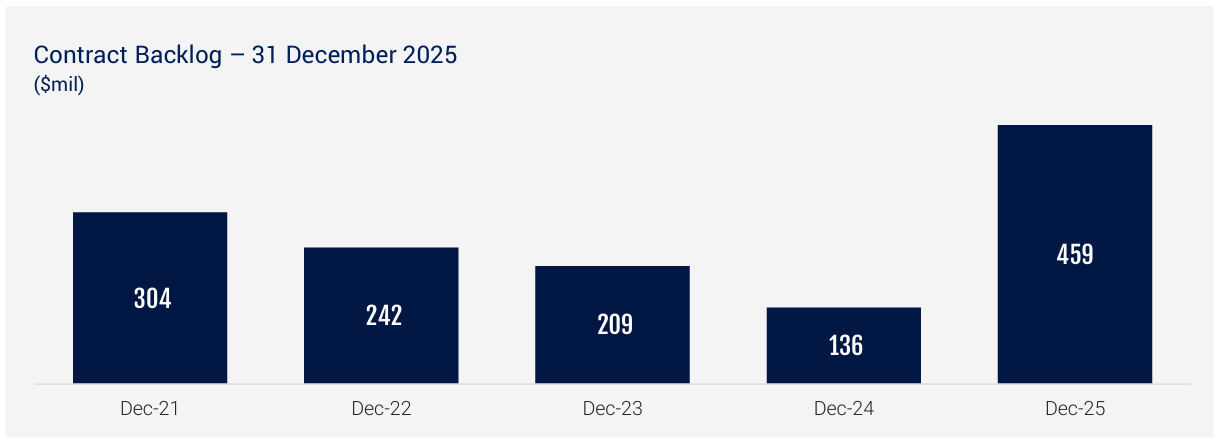

When comparing this to EOS’ latest updated backlog from their fourth quarter update, we can see that EOS has now barely exceeded their 2023 stated backlog.

Source: Quarterly Activity Report and Appendix 4C – December 2025

Debt Payback

The company used a portion of EMS sale proceeds to pay back their debt, which became current during that same period worth roughly A$61.1 million. We believe the timeline of these events is not a coincidence and simply the company had to find a way to pay back the debt facility, having to pay it back in full in the next 10 months.

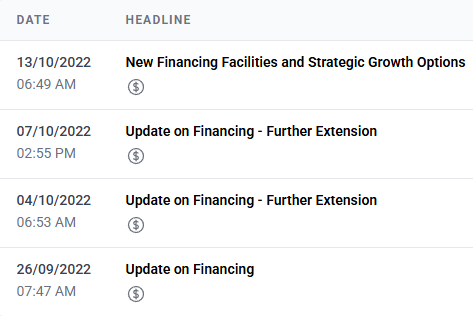

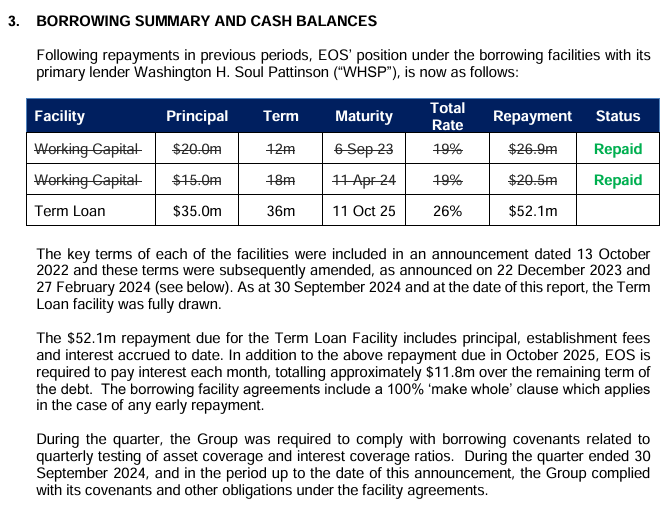

In October 2022, EOS finalized multiple borrowing facilities with Washington H. Soul Pattinson (WHPS) with aggressive terms, the biggest one bearing interests of a whopping 26%. On top of this, EOS issued 4.68% of their total shares outstanding to WHPS for free, taking WHSP’s total shareholding to 9.95% of EOS’ issued share capital at the time. EOS was also required to maintain financial covenants that it struggled to reach at multiple occasions, reducing the flexibility in how they were doing business.

Source: EOS website

During the Q3 2024, after repaying two of the three facilities, EOS was left with the biggest borrow facility amounting to A$52.1 million and due for repayment around 10 months later. On top of this, EOS had to pay a total of A$11.8 million in interest until the repayment date.

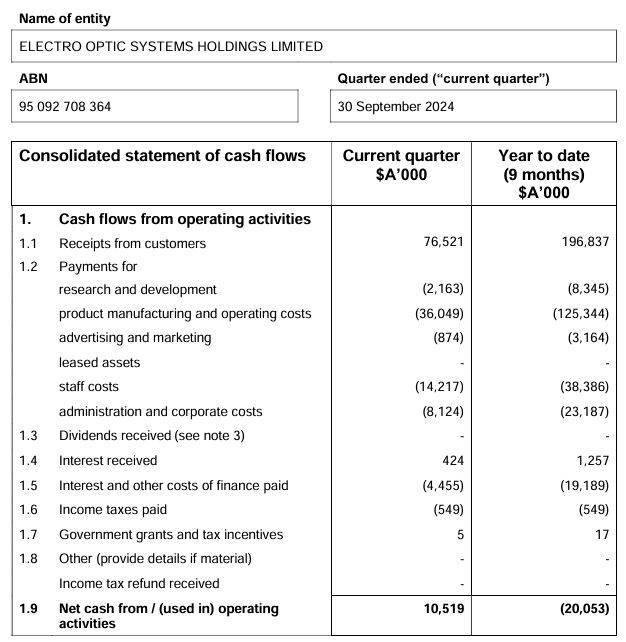

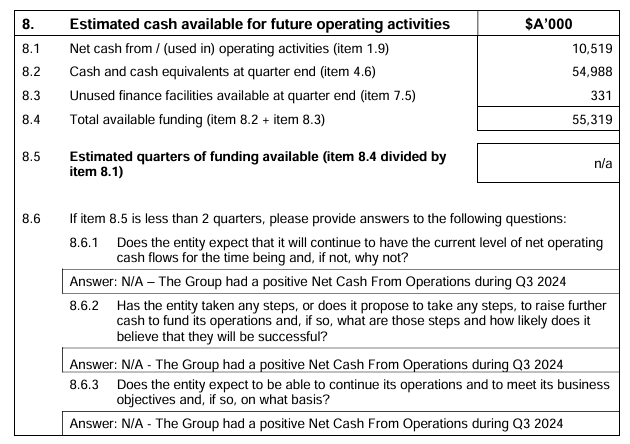

At the end of this same quarter, EOS had cash and cash equivalents of A$55.3 million, and had no other financing available, meaning that there was massive insolvency risk hanging over the company. EOS generated a negative A$20 million operating cash flow during the 9 months from January 2024 to September 2024, which left no room for execution and operational mistakes. At the same time, EOS stock price was around A$1.50, restraining the company from raising capital without triggering heavy dilution for its existing shareholders. The company was left with few options, one of them being the sale of some of its assets.

Source: Filing for Quarter Ended 30 September 2024

Source: Filing for Quarter Ended 30 September 2024

We believe that, at the time, EMS was the only “interesting option” for buyers, being profitable, growing and having a substantial backlog. EOS Management calling EMS a “non-core asset” appears to have been an excuse to mask the desperate situation they were in.

While we do not criticize the decision to sell EMS, we want to point out that this has put EOS in a delicate post-sale situation where they had to develop their remaining business segments quickly and garner investor interest in accessing financing options.

Post-EM Solutions Divestiture

Following the divesture of EMS, the company immediately looks materially worse as they lost the only profitable segment. In the full-year 2024 results, the company posted a A$30 million loss from continuing operations for the second half of 2024, the largest loss since the June 2022 semi-annual.

This trend continued in June 2025 as seen in the semi-annual report, where the company reported A$44 million revenue from continuing operations, down 58% year over year. Additionally, operating loss saw another drop to -A$25.02 million and the net income attributable to continuing operations cratered to -A$44.2 million.

Source: Grizzly Analysis, compiled from company sources/filings

Source: Grizzly Analysis, compiled from company sources/filings

The company is still incurring heavy losses, and the cash flow for the twelve months ending December 31, 2025, has been disappointing. EOS stock price rose to an ATH of A$10.42 in October 2025, after the company announced new contracts, only to fall back to around A$4.50 after releasing disappointing earnings for Q3 2025.

The bogus Korean contract appeared as a savior, pushing the stock price from around A$5 to a recent new ATH of A$11.20, reversing the fall. We would not be surprised to see a capital raise coming soon which further explains the need for EOS to increase its stock price.

Disclosures Around Other Major Contracts Signed in 2025 Also Show Red Flags

After discovering the truth around the Korean contract, we took a fresh look at the other important contracts signed by EOS in 2025 and what the company discloses.

The A$53 million contract customer has not been named, it is a “turnkey naval shipyard related systems integrated company” from Europe. Delivery is expected to occur during 2025 and 2026. Even though it could remain unnamed for legitimate reasons, we are naturally suspicious of the opacity around this customer identity.

The A$125 million contract from the Dutch government has been touted by EOS as a “game-changing contract” for them and even for the whole industry. However, we believe EOS has not been entirely transparent with its investors. While the contract was confirmed by the Dutch Government, we learn from their disclosure that this project aims to “build a prototype” which is expected to be delivered in 2028. There is no mention of it being a prototype in any of EOS press releases. We find this information quite crucial. In one of the interviews he gave following the signing, EOS’ CEO even states:

“Schwer highlights this contract as the first operational deployment of such a high-powered laser globally, moving beyond prototypes to real-world use.”

Given our previous findings, we view these misleading statements as red flags, given the continuity of misrepresentations by management.

The A$108 million contract is a sub-award from Hanwha Defense Australia who is the prime contractor for the Australian Government. It includes delivery of RWS, plus spare parts, training, documentation, and “other items” during 2025, 2026 and 2027, but as mentioned in the Q4 2025 update, it will primarily be fulfilled during 2026 and 2027.

These contracts cover most of the backlog (A$404 million with the remaining initial backlog), the other small contracts announced during the fourth quarter of 2025 are also expected to be delivered over multiple years. While there is nothing alarming about them on the surface, the opacity and misleading statements of EOS around them raise red flags.

Similarly, we found that management very often engages in aggressive promotion of their capabilities, opportunities and achievements. During the countless interviews that the CEO gave to media and webinars around signing of contracts, EOS is almost always portrayed as the marquis of the defense sector, with almost all major governments being “very interested” to work with EOS. The most outrageous statement we could find comes from an interview with the CEO from December 2025:

” We also won by a wide margin at the US Army’s most prestigious live-fire exercise in April of this year. Subsequently, we received a contract from the US Army, which will likely make us their preferred C-UAS standard solution. The US combat vehicle fleet will be equipped with an EOS R400 Slinger in a semi-autonomous special configuration.”

We could not find any evidence that backs up this statement beyond EOS’ own announcements. This kind of repeated aggressive statement should be cautiously viewed by investors.

Conclusion

We conclude that EOS is run by an untrustworthy management team. The financial situation looks dire, and therefore the company is under pressure to paint a rosier picture and get the stock to a high valuation. It seems that they have resorted to fraudulent tactics to pump up the stock price.

In the light of our findings, the new Korean contract does not look like validation. On the contrary, we believe it exposes a management team so desperate to push out good news that they are willing to lie to their investors.