Read below or open PDF version

- Ceres Power Holdings plc is a UK developer of solid oxide electrolyzer cell (SOEC) and solid oxide fuel cell (SOFC) technology for use in distributed power systems. We believe the company is hiding a flawed business model with abysmally small revenue potential behind a façade of big-name announcements and lofty projections.

- Our research shows that Ceres has a history of ambitious partnerships and unrealistic projections that keeps repeating. Past partnerships with Bosch, Nissan or Honda were loudly announced but failed miserably. Past ambitious revenue projections were also quietly removed from investor presentations.

- Based on our expert interviews as well as the company’s own past commentary, we found that revenue potential is only a fraction of what investors believe.

- Earlier this year, Ceres stock price skyrocketed on the announcement that Doosan Fuel Cell finally started mass producing and commercializing their fuel cell stacks and systems using Ceres’ solid oxide fuel cell (SOFC) technology. We found that Doosan is already struggling to find customers for its current 50MW manufacturing capacity.

- More than four months after mass production began, Doosan has a single 9MW order for their SOFC product, and it comes from a related party. According to experts and Ceres’ own marketing materials, we estimate a 9MW order will only generate up to a minuscule $1.35 million in gross margin for Ceres. Doosan stated that they do not expect any new order this year and that results are already falling short of expectations.

- Ceres recently signed a new manufacturing agreement with WeiChai, which holds 19.50% of Ceres’ shares. It is one among multiple JVs, agreements and products that WeiChai and Ceres developed together and failed. WeiChai even deemed the announcement as “routine business”, not material enough to warrant an announcement on the Hong Kong stock exchange.

- A core issue in Ceres’ business model is that it shifts all product R&D, industrialization, and capital requirements onto partners, a strategy that has failed for over a decade. This sits alongside other flaws, including the technology’s reliability, maintenance and serviceability challenges, limited market size, and total dependence on licensees. Ceres has never generated material royalty revenue and, in our view, will not do so in the foreseeable future. The business survives on one-off licensing and engineering fees.

- In conclusion we believe that Ceres is a flawed business model as a public company. The announcements that catapulted Ceres’ market cap by hundreds of millions GBP will likely turn out to yield only minuscule earnings as the stock fades away into obscurity.

Introduction

Ceres Power Holdings plc is a UK developer of solid oxide electrolyzer cell (SOEC) and solid oxide fuel cell (SOFC) technology for use in distributed power systems. Founded in 2001, it is headquartered at Horsham in the UK.

Ceres Power’s stock price is up more than 250% since their partner Doosan Fuel Cell announced the start of its SOFC systems in their new 50MW factory using Ceres’ technology in July 2025. Since then, Ceres Power only signed a new manufacturing agreement with their long-standing partner and biggest shareholder WeiChai, with whom they failed multiple times to bring joint products to market since 2018.

Based on our research, we believe investors are misled by Ceres’ projections given the near-future prospects and the multiple past failures of Ceres partnerships.

For example, we found evidence that Doosan’s “mass production start” since July 2025 suffers a very slow take-off and interest in SOFC products, as Doosan Fuel Cell only currently secured a 9 MW supply contract with a related-party. According to our research, this should at best generate $1.5 million in royalties for Ceres, a small prize for a 10+ year struggle to reach commercialization stage.

We get a “déjà vu” impression about this situation, as Ceres has announced dozens of partnerships with global companies to commercialize a product with Ceres’ technology. The vast majority of these partnerships vanished without much communication from the company.

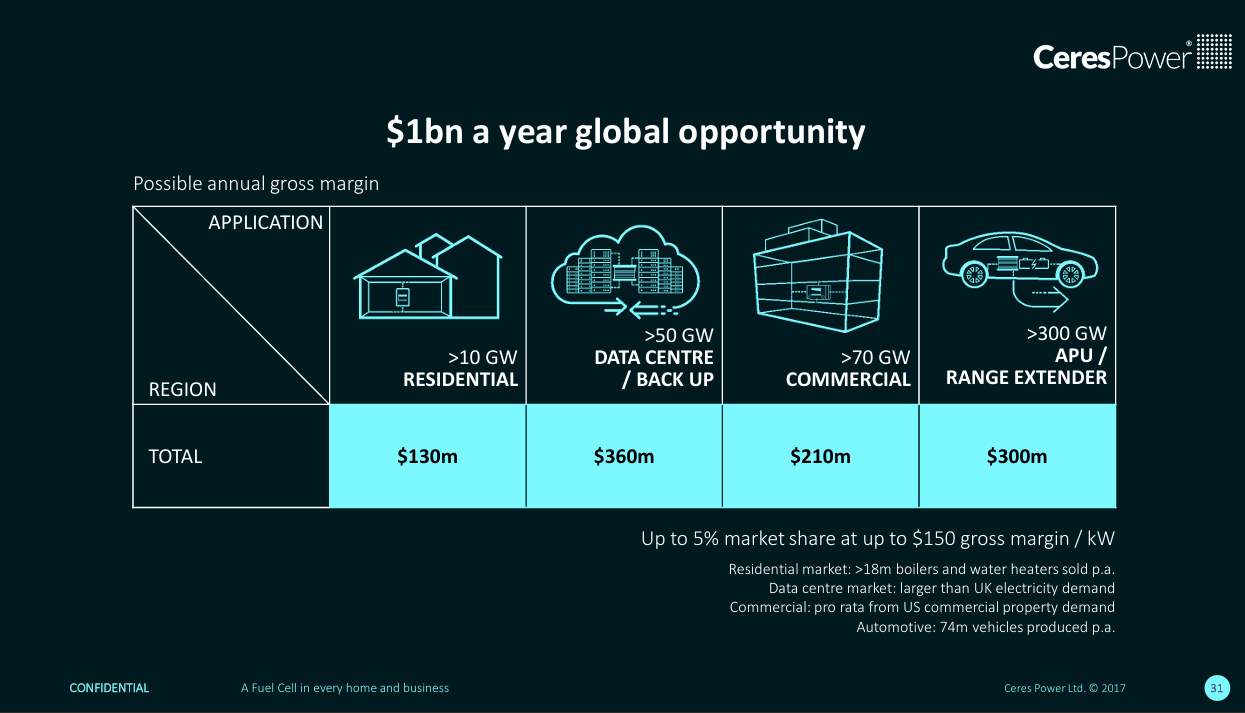

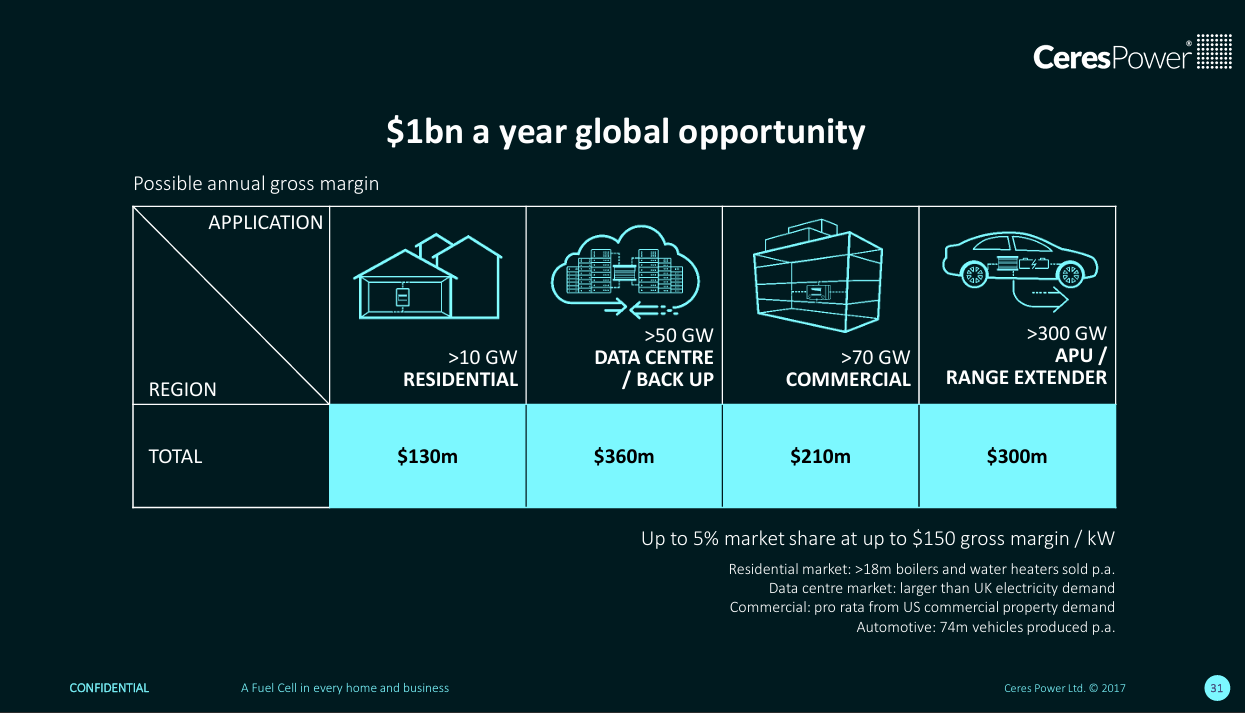

We find since vanished projections from Ceres’ 2022 Annual Report to “reach multi GWs by 2030” ridiculous and frankly, misleading. As far back as 2016, the company touted that possible annual gross margin for Ceres’ licensing model was around $1 billion annually. 9 years later, the company still has not generated any significant royalties.

In conclusion we think that Ceres’ licensing business model is deeply flawed. The company essentially shifts all the risk to its licensees while relying entirely on them to commercialize a new product. The capital required to bring a product from the IP acquisition to a potential commercialization is enormous, while the TAM of both the SOFC and SOEC technologies are small, despite being relatively old technologies. We are afraid investors will find themselves once again sorely disappointed by the results exciting sounding partnerships will deliver.

In this report we first examine the most recently announced deal with Doosan that has now reached commercial stage, but will unfortunately soon reveal to investors the abysmal customer interest and minimal revenue potential associated with Ceres’ technology.

Content

Doosan Fuel Cell, the First Partner to Bring a Product to Mass Production in More Than a Decade Suffers Slow Take-Off

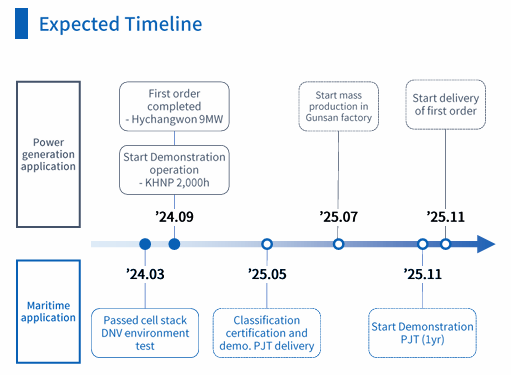

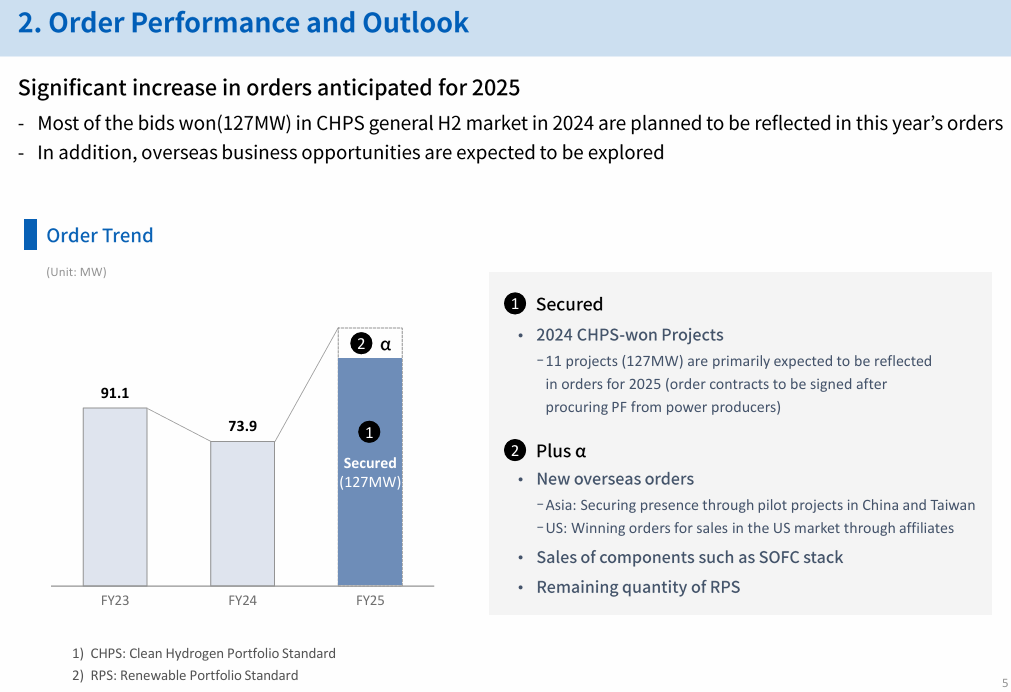

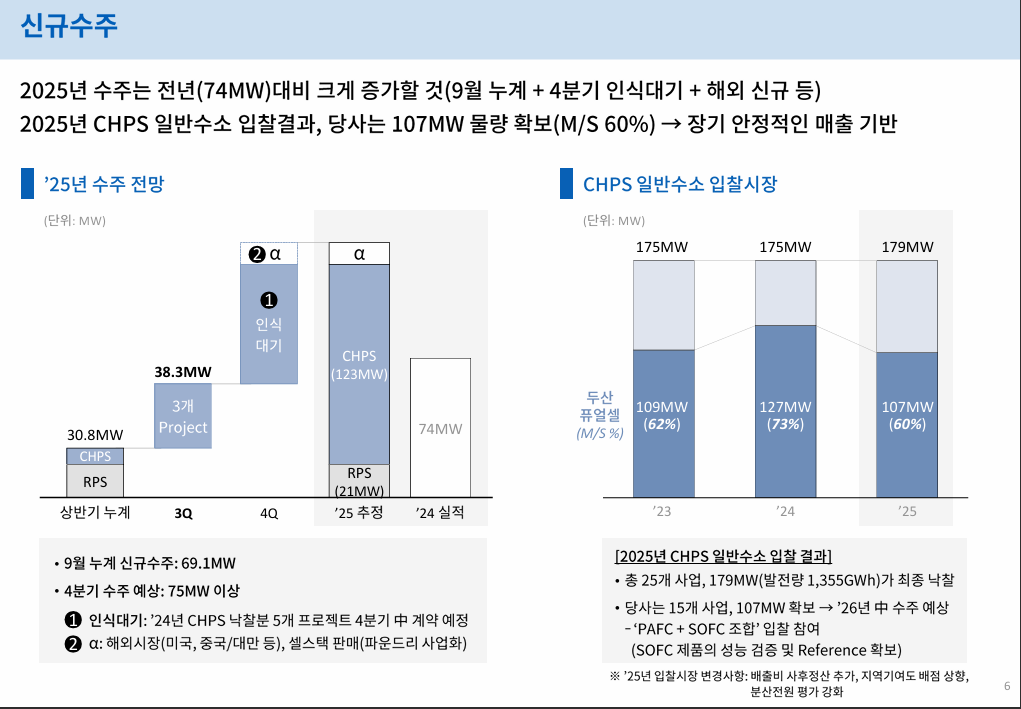

In July 2025, Doosan Fuel Cell announced that mass production of their stack cells had begun using Ceres’ technology. This represents a significant milestone for Ceres as this is the first time, after more than a decade of consistent failures, that it finally reaches royalty revenue generation. This comes more than 6 years after Doosan and Ceres signed a collaboration and licensing agreement to develop SOFC power systems. The capacity of Doosan’s new manufacturing facility is 50MW. However, our research shows that 4 months following that announcement that sent Ceres’ stock price through the roof, Doosan only received a 9MW order from a related-party in September 2024. Worse yet, in their Q3 2025 presentation, Doosan clearly shows that it is not expecting any additional order for 2025, and that the volume of SOFC product sold should also remain similar in 2026, with very little traction. Korean medias pointed out the disappointing quarter that did not meet analysts’ expectations.

Ceres’ royalty outlook from Doosan is objectively weak, and the evidence across disclosures, Korean filings, bid results, and Doosan’s own Q3 investor materials makes this increasingly clear that it will likely continue to stay. Doosan is the only mass-manufacturing partner currently capable of producing SOFC systems based on Ceres’ technology, meaning Ceres is entirely dependent on Doosan for near-term and also their very first royalties. Yet Doosan has no visible commercial SOFC demand, no confirmed third-party SOFC customers, and has only started delivering SOFC stacks to one related-party SPV “Hychangwon Fuell Cell Project” in November 2025, which provides no meaningful signal of market traction or future royalty volume.

Source: Doosan’s Q3 2025 Presentation

Doosan’s 2025 order-intake forecast shows zero secured SOFC MW (9MW order being from September 2024), all expected orders are CHPS and RPS programs (Korean government programs) that use their legacy PAFC fuel cells. The 107MW contracts Doosan won in 2025 are effectively 100% PAFC, with SOFC playing no commercial role.

Source: Doosan’s Q3 2025 English Presentation

Source: Doosan’s Q3 2025 Korean Presentation

Furthermore, the near-term outlook for SOFC deployment has worsened further following the Korean government’s cancellation of the 2025 Clean-Hydrogen Power Scheme (CHPS) bidding round, which had represented one of the few credible demand channels through which Doosan could have attempted to introduce its new SOFC product. Even before the cancellation, Doosan was only positioning SOFC as a supporting technology within mixed PAFC+SOFC bids, primarily to secure references rather than to win meaningful standalone orders. With CHPS now suspended, this validation pathway has closed, and the company is left with no obvious route to early commercial SOFC volume. As a result, the already-limited pipeline for SOFC deployments has deteriorated further, pushing out any realistic prospect of material royalties flowing to Ceres and amplifying the execution risk surrounding the entire SOFC commercialization cycle.

Combined with Doosan’s publicly disclosed SOFC poor initial yields, higher unit processing costs, and inventory NRV adjustments, the commercial rollout is clearly delayed and financially strained.

The Doosan Deal Reveals That Revenue Potential Is actually Tiny

For estimating royalties from Doosan’s 9 MW SOFC contract, we based our pricing assumptions on publicly available benchmarks for SOFC system costs, because Doosan has disclosed no commercial pricing for its Ceres-related SOFC line. The U.S. Department of Energy (DOE) sets a long-term SOFC system cost target of $900 per kW for commercial-scale deployment, this is the lowest credible benchmark and assumes future cost optimization (Source: Solid Oxide Fuel Cells | Department of Energy). Independent industry assessments hint at commercial pricing closer to $1,200 per kW, while several technical papers and research-gate module surveys note that early-stage commercial SOFC systems can range far higher, often $4,000–8,000 per kW, depending on stack technology, support materials, and low production volumes (although very unlikely for Doosan). We reach the following range of hypothetical amounts:

- Low case: 9,000 kW × US$900/kW ≈ $8.1m

- Base case: 9,000 kW × US$1,200/kW ≈ $10.8m

- High case: 9,000 kW × US$4,000–8,000/kW ≈ $36–72m

Applying standard industrial-technology royalty ranges of 2-5% to these values yields a royalty range of roughly $0.16m to $3.6m for a 9MW project. Given the project is with Hychangwon, a related party created for Doosan’s own deployment, the real amount could be even lower.

We found that in 2016 Ceres’ Annual Report showcased projected gross margin at up to $150 gross margin/kW. Applying this to the 9MW would yield $1.35 million in royalties for Ceres, in line with our assumptions. Given that this is a “best-case” scenario given by the company 9 years ago, we assume that it is in reality lower than this.

Source: Ceres Experience 2016

In April 2025, a MoU was signed between Doosan Fuel Cell and Samchully explicitly referenced SOFC deployment and “mid-/low-temperature SOFC commercialization”. But the current situation with Samchully reinforces the view that Ceres should not expect meaningful near-term SOFC royalties from Doosan. The large ₩1.07 trillion set of contracts that Samchully signed with Doosan in August did not mention SOFC at all. Instead, those contracts were described only as generic “fuel-cell system supply” for by-product hydrogen plants, the type of projects historically dominated by Doosan’s PAFC systems. The absence of any SOFC reference in the final binding contracts strongly suggests that the earlier SOFC-focused MoU has been delayed, deprioritized, or effectively abandoned, with Samchully choosing proven PAFC systems for its commercial roll-out. If Doosan could not convert its most public SOFC MoU into actual SOFC orders with a long-standing partner like Samchully, this implies real-world customer reluctance, technology-readiness issues, or economic disadvantages for SOFC. For Ceres, this means one of the only SOFC commercial pathways has stalled, and the royalty pipeline expected from Doosan’s partner network remains thin to non-existent.

Doosan expects no SOFC-related growth in 2026, as shown in the screenshot below.

Source: Doosan’s Q3 2025 English Presentation

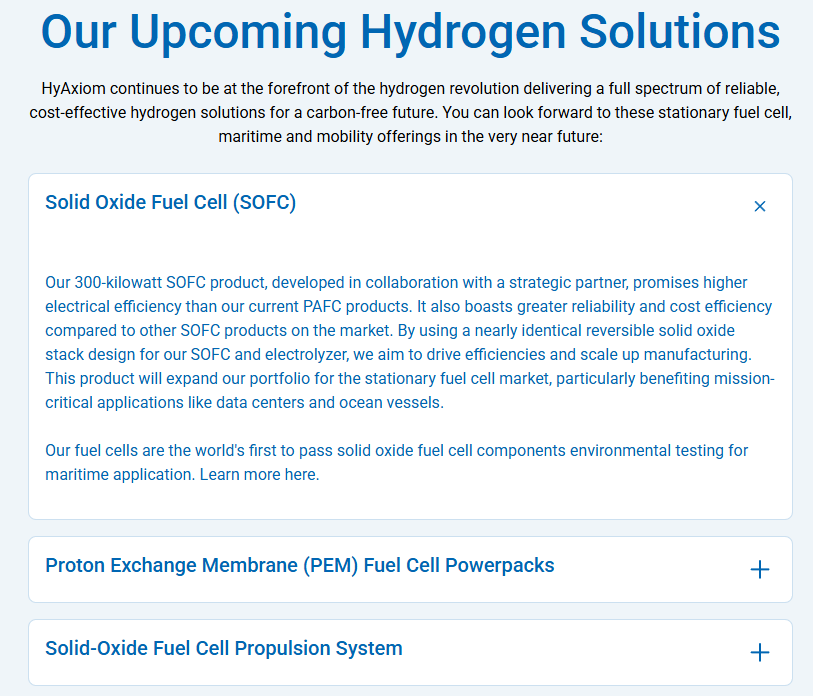

Doosan also operates a subsidiary that is in charge of all its business outside of Korea: “HyAxiom”. On their website, it is highlighted that the SOFC products are “upcoming”, meaning it is not yet available outside of Korea and is most probably still pending local validation first.

Source: HyAxiom.com

When comparing Doosan Fuel Cell’s Q3 2025 Consolidated and Unconsolidated income statement (with and without HyAxiom), we see no difference in revenue and a slight difference in operating expenses, suggesting that the subsidiary is essentially idle.

Source: Doosan’s Q3 2025 English Presentation

This raises another red flag, as Doosan Fuel Cell explicitly stated that they would put more focus on the international market, more specifically the U.S.to boost their product’s adoption and revenue.

All of this leads to one unavoidable conclusion: Ceres has almost no royalty-bearing SOFC volume coming from Doosan, and the near-term outlook is still poor. Unless Doosan begins winning, and actually deploying SOFC projects with real external customers, Ceres’ royalty stream will remain negligible.

Ceres Power and Weichai Power: A Tumultuous Partnership Timeline

Initial Strategic Partnership and Equity Investment (2018)

The story starts in May 2018, Ceres announced a major strategic partnership with Chinese giant Weichai. Weichai agreed to invest up to £40 million in Ceres, taking an initial 10% equity stake (for ~£17m at 15.08p/share) with a path to 20% ownership pending further agreements. The deal was not just about equity: Weichai and Ceres also agreed to collaborate on SOFC technology for China’s commercial vehicle market, specifically a 30 kW fuel cell range extender system for electric buses. Weichai’s wide bus customer base in China (around 30,000 buses per year) made it an attractive partner for Ceres. Both parties envisioned that leveraging Weichai’s manufacturing might and market access could rapidly commercialize Ceres’ fuel cells in China’s fast-growing new energy vehicle sector. Importantly, the partnership included an explicit roadmap: joint technology transfer in 2018, a prototype fuel-cell bus demonstration by 2019, and multiple bus trials by 2020. These bold targets set high expectations on both sides.

By December 2018, Ceres and Weichai formally finalized their long-term collaboration, fleshing out detailed agreements. Weichai exercised its warrants to invest an additional £28 million at 164.5p/share, bringing its total stake to 20% (and total cash invested ~£48 million). In return, Ceres granted Weichai a system license to develop the promised 30 kW SOFC range extender for buses and a new joint development agreement (JDA) worth £9 million to fund continued product development. The partners also signed a Joint Venture (JV) Agreement laying the groundwork to establish a fuel cell manufacturing JV in Shandong, China once field trials succeeded. The JV was anticipated to launch around 2020, initially focusing on Chinese bus, commercial vehicle, and stationary power markets. Under the plan, Weichai would own 51% and Ceres 49% of the JV, with Ceres transferring its SOFC technology in stages for up to £30 million in fees and then earning royalties on future product sales.

Ceres touted the “scale-changing” potential of a Chinese manufacturing JV with Weichai, yet it led nowhere.

Early Progress: Prototype Bus and Field Trials (2019–2020)

In September 2019, Ceres and Weichai unveiled the world’s first SOFC-powered bus entering field trials in China. A prototype 30 kW fuel cell range extender system using Ceres’ SteelCell stacks that was integrated into a Chinese electric bus, as part of the initial validation phase. Following the prototype, the focus shifted to scaling up trials to a fleet of 10 buses, which the 2018 JDA had targeted for 2019 to 2020.

However, beyond the single prototype bus, concrete news on broader trials was scant. Ceres’ disclosures around that time hinted at delays: no China JV was launched in 2020 as originally anticipated, and revenue from the Weichai collaboration remained limited to development fees rather than any commercial product sales.

By mid-2020, the initial goal of SOFC bus commercialization had failed. China’s new energy bus market itself was evolving, with policy incentives shifting toward hydrogen fuel cell vehicles and batteries rather than range extenders running on CNG. In other words, the strategic rationale for Weichai to prioritize Ceres’ SOFC in buses diminished as zero-emission (hydrogen) alternatives gained favor.

Delays, Strategy Shifts, and a Third Partner Enters (2021–2022)

By late 2020 and into 2021, the China manufacturing JV had not materialized on schedule. Weichai expanded the scope to stationary power applications, leveraging SOFC for generators, data center power, etc. By 2021 Weichai had quietly developed larger SOFC systems based on Ceres’ tech, likely repurposing the know-how from the bus program. In early 2023 Weichai unveiled a 120kW stationary SOFC power system and obtained CE certification from TÜV SÜD (a European safety standard).

Additionally, Bosch had entered the picture as a key Ceres stakeholder (acquiring ~18% of Ceres by late 2020) and was also pursuing SOFC manufacturing in Europe.

In February 2022, Ceres, Weichai, and Bosch announced a non-binding agreement for a “three-way collaboration” in China, effectively revising the original JV plan. Under this proposal, two JVs would be formed:

- a System JV among Weichai, Bosch, and Ceres to develop and build complete SOFC power systems in China (for both mobile and stationary applications), with Weichai as majority owner and Ceres taking only ~10% stake. Bosch and Ceres would license their system technology into this venture and share royalties.

- a Stack Manufacturing JV between Bosch and Weichai to produce fuel cell stacks (Bosch’s planned 200 MW German SOFC factory would be mirrored by a Chinese facility). Bosch would own the majority of the stack JV, while Ceres would have no equity stake, instead earning royalties via Bosch’s extended manufacturing license for China.

Critically, this restructured deal aimed to “significantly strengthen” the China plan by adding Bosch’s heft and including stationary power in the product scope. Ceres stood to receive around £30 million in license fees over the next three years from these new JVs. Notably the same figure touted in 2018 for tech transfer, suggesting little to no increase in overall deal value.

The Joint Venture Falls Through (2023–2024)

Despite the grand plans, the three-way JV structure never reached fruition. Throughout 2022, progress on finalizing the JVs dragged on with no definitive closing. Then came a major blow: in early 2023, Bosch began reconsidering its SOFC strategy. By January 2024, Ceres finally conceded that it was “no longer able to conclude” the planned joint venture in its current form. In an update, Ceres bluntly stated it was “unlikely” the China JV would be completed. The collapse of the JV plan after nearly five years of announcements and extensions was a major strategic setback, halting Ceres’ primary route to the China market.

A Pivot to Licensing – New Agreement in 2025

Having hit a wall with the joint venture approach, Ceres and Weichai recently opted for a simpler licensing arrangement. On November 5, 2025, Ceres announced it had signed a manufacturing license agreement granting Weichai rights to produce Ceres’ SOFC cells and stacks at a new facility in China. This deal explicitly targets stationary power applications such as prime or backup power for AI data centers, commercial buildings, and industrial sites, rather than the vehicle market. Ceres noted that this agreement “supersedes previous arrangements” with Weichai, effectively replacing the defunct JV plans with a direct license model.

Under the license, Weichai will set up production lines for the fuel cell stacks, while Ceres will supply certain key components and receive the typical mix of upfront fees, milestone payments, and ongoing royalties. Ceres touted this as a significant expansion of its manufacturing partnerships and highlighted the “multi-billion market opportunity” for stationary power in China as AI and industry drive demand for reliable, efficient generators.

Notably, Weichai’s reaction was subdued. Weichai’s management characterized the license as “routine business” and even stated the agreement “did not meet the disclosure threshold” for an announcement on the Hong Kong Stock Exchange. On the day the deal became public, Weichai’s stock fell ~7% which is a sign that investors saw it as having limited immediate upside for Weichai’s earnings. For Weichai, this license is just one puzzle piece in a much larger new-energy strategy, whereas for Ceres it is a central lifeline to finally access the Chinese market (albeit in reduced scope).

In conclusion, from inception to the present, the Ceres–Weichai partnership has been a rollercoaster of lofty promises, repeated delays, and strategic recalibrations, ultimately yielding a narrower outcome than originally envisioned. Investors should remain skeptical until they see tangible results: e.g. Weichai’s new SOFC factory actually ramping up and royalty streams flowing to Ceres rather than just optimistic press releases.

Bosch Partnership Failure

The Ceres-Bosch partnership, once a cornerstone of Ceres Power’s commercial narrative, ended abruptly in early 2025 after years of high-profile collaboration. Bosch had been a strategic investor and licensee since 2018, acquiring a nearly 18% stake and committing over €400 million to scale solid oxide fuel cell (SOFC) production using Ceres’s technology. The alliance was positioned as transformational, with Bosch aiming to build 200 MW of SOFC capacity and deploy distributed power systems across Europe. However, despite joint development milestones and limited pilot installations, Bosch ultimately terminated the relationship, citing “slower-than-expected market adoption”.

This exit not only removed a major revenue source and validation partner for Ceres, but also exposed the structural weakness in its asset-light model: full commercialization depends entirely on partner execution. Bosch’s decision underscores persistent demand uncertainty in the SOFC market, and raises broader questions about whether Ceres’s technology, though scientifically validated, is economically compelling at scale. While Ceres pivoted quickly to reinforce other partnerships, notably with Delta and Weichai, the Bosch exit represents a high-profile setback and highlights the inherent risks in relying on third parties for both commercialization and validation.

Bosch represents the biggest failure to date for Ceres, but is not the only one. From 2013 to 2023, besides Doosan and Weichai, virtually all Ceres partnerships and projections failed.

Other Failures With Past Projections (2013–2023)

In Ceres Power’s history, there’s been a consistent pattern: the company repeatedly trumpets new partnerships and agreements that ultimately yield nothing of commercial substance. From 2013 through 2023, Ceres announced deal after deal, each with optimistic projections of breakthroughs, only for these partnerships to fade away without delivering any product, revenue, or lasting collaboration. This narrative of hype followed by disappointment spans multiple years and high-profile partners, illustrating how Ceres’s projections have often proven misleading or overhyped in retrospect. Note that announcements from 2013 to 2017 are not easily accessible as Ceres conveniently made a new website in 2018 with the WeiChai’s partnership as its first press release. The prior website vanished from the web and is only accessible via Wayback Machine (www.cerespower.com).

2013: KD Navien, a Landmark Deal That Went Nowhere

In July 2013, Ceres unveiled what it called a “commercial and technical partnership” with South Korea’s largest boiler maker, KD Navien. This was heralded as Ceres’s first major commercial agreement under its new strategy, with plans for KD Navien to test Ceres’s 1 kW fuel cell module in Seoul and jointly design a micro-CHP (combined heat and power) system for the Korean market. Ceres’s chairman Alan Aubrey proclaimed KD Navien the “ideal partner” to integrate the SteelCell technology into Korea’s residential boiler market. The announcement even talked of an intended follow-on licensing deal for the manufacture and distribution of fuel cell products once initial trials succeeded. But despite these lofty promises, the KD Navien partnership quietly evaporated. Over a decade later, not a single commercial product or follow-up agreement emerged from this deal.

2016: A Flurry of Partnerships – All Hype, No Traction

After a few years of relative quiet, Ceres embarked on a flurry of partnership announcements. By the end of that year the company claimed six partners on its roster, including well-known names like Cummins, Nissan, and Honda. Each of these 2016 deals was touted as a significant step toward commercialization, yet each ultimately proved inconsequential.

Cummins (Data Centers): In September 2016, Ceres partnered with U.S. engine giant Cummins on a project to power data centers with fuel cells. Backed by nearly $5 million in funding from the U.S. Department of Energy, the collaboration aimed to develop a novel 5 kW solid oxide fuel cell system for high-efficiency, distributed power, to serve as backup or primary power for data centers. Ceres boasted that its “SteelCell” technology could revolutionize data center energy use, potentially cutting overall costs by more than 20% and reducing carbon emissions by roughly 49% if implemented at scale. CEO Phil Caldwell called it “a very exciting opportunity” to work with Cummins and the DOE on this application. Yet despite the fanfare, this partnership delivered nothing beyond a government-funded demonstration. No commercial product was ever announced as a result of the Cummins tie-up, and Cummins never integrated Ceres’s fuel cells into its data center power offerings.

Nissan (EV Range Extenders): Around the same time, Ceres publicized a partnership with Nissan to develop fuel-cell range extenders for electric vehicles. In June 2016, Ceres announced it had “finalized all agreements” with Nissan Motor Manufacturing UK as part of an “Innovate UK–funded consortium” to develop an on-board solid oxide fuel cell stack for extending electric vehicle range. The company pitched this as a breakthrough to “significantly accelerate the take up of electric vehicles,” using Ceres’ “SteelCell” to enable longer-range, quick-refueling EVs while cutting emissions. But like the other deals, the Nissan collaboration was all talk and no tangible result. It was effectively a government-sponsored prototype effort, and once the initial demonstration was done, there was no indication that Nissan pursued the technology further. The venture did not yield any commercial EV product or follow-on contract with Nissan.

Honda (Joint Development Agreement): Ceres’s alliance with Honda followed a similar trajectory. In January 2016, Ceres signed a new two-year joint development agreement with Honda R&D Co. to jointly develop solid oxide fuel cell stacks using the “SteelCell” technology. Ceres touted the contract as a “deepening of the relationship” with Honda that even brought in a third-party manufacturer to evaluate future mass production scale-up of the “SteelCell” technology. The idea was that Honda’s continued involvement, building on an initial 2014 collaboration, could eventually lead to mass-produced fuel cell units for Honda’s product lines. At least, that was the hopeful projection. In reality, nothing of the sort materialized. The two-year Honda project came and went with no sign of any commercial follow-through. After it concluded in 2018, there were no announcements of Honda adopting Ceres’s stacks in any product or entering a licensing deal.

Unnamed “Global OEM” (Multi-kW CHP): At the end of the same year, Ceres revealed another agreement, this time with an unnamed “leading global OEM”, to develop a new multi-kilowatt combined heat-and-power product. The multi-year joint development license was supposed to enable the OEM partner to create a larger “SteelCell-based” CHP system for commercial and residential markets, with field trials planned and a target of eventual market launch. Under the agreement, Ceres would transfer its system technology to the OEM under a non-exclusive license, and the partner ostensibly had “a clear intention to develop and launch a product” using the “SteelCell: if the trials were successful. Phil Caldwell highlighted the deal as evidence that a major industry player saw value in the “SteelCell” platform. Ceres never disclosed the name of this OEM publicly, citing confidentiality. In hindsight, the opacity was a red flag: the hyped “go-to-market” CHP product never materialized. There is no sign that any field trial led to a commercial launch, nor that this unnamed manufacturer moved beyond the prototype stage.

2017: More Partners, Same Pattern

Ceres entered 2017 continuing its partnership-centric strategy, and still without any commercial success to show. In May 2017, the company announced a new two-year SOFC system JDA with one of its existing global partners, this time to develop residential power systems (home fuel cell units) based on the “SteelCell” technology again. The project was backed by about £0.7 million of government funding from “Innovate UK” to support advancing fuel cell solutions for home energy. Unfortunately, as became the norm for Ceres, this too led to nowhere substantive. After the two-year development period elapsed, no residential CHP product was ever brought to market.

Even in later years, this pattern continued. For example, in 2023 Ceres publicized a collaboration with Norway’s Alma Clean Power to develop an 80 kW marine fuel cell system. As of now, that partnership is only at the demonstration stage, with no evidence of commercial traction. Across all these cases, Ceres’s partnerships have amounted to little more than promotional news. The company repeatedly heralded “breakthrough” agreements and technological potential, but none of these alliances delivered any lasting value: no recurring revenue, no mass-market product, and no strategic follow-through.

The one partial exception was Ceres’s tie-up with Japan’s Miura Co., a boiler manufacturer, first announced in late 2016 as a joint development to launch a multi-kilowatt combined heat-and-power (CHP) fuel cell system. That partnership did eventually produce a tangible product, Miura unveiled a 4.2 kW solid oxide fuel cell CHP unit in 2019 as a result of this collaboration, making it the only early Ceres partnership to reach a commercial launch. However, even this “success” was marginal: the initial rollout was limited to field trials and a very small number of units (fewer than ten such systems were in operation by early 2020), with no sign of meaningful scale-up or lasting market impact. In short, while Miura stands out as the lone case from that era to produce an actual product, it ultimately did little to break the pattern of bold Ceres promises fizzling into underwhelming outcomes.

By the end of 2017, Ceres Power had amassed an impressive-sounding roster of partnerships and prototype projects, but not one had yielded a lasting commercial product, meaningful revenue, or an enduring OEM relationship. The company’s string of announcements between 2013 and 207 reveals a clear tendency to overpromise and underdeliver: each deal was touted as if it would be transformative, whether a “landmark” alliance or a collaboration with a “world-leading” OEM, yet each ultimately fizzled out. These serial disappointments highlight a consistent gap between Ceres’s promotional hype and the subsequent reality.

Below are a couple of examples of Ceres’ moonshot predictions which completely failed, while touting that they were “perfectly positioned to take a share of several multi-billion dollar markets”.

Source: The Global Opportunity – Ceres Power plc

Source: Ceres Experience 2016

Even though past results are not indicative of future performance, past and current indicators clearly show a tendency not to yield any results. To us, none of these failures are surprising, as we believe Ceres business model is deeply and fundamentally flawed, as we explain in the next section.

A Fundamentally Flawed Business Model

According to experts and former employees we interviewed, Ceres’ business model is fundamentally flawed on numerous fronts.

From the beginning, Ceres was described as a “university science project with no target market or commercial application” and also as a “hammer looking for nail”. Ceres has changed their business model entirely multiple times after the past ones failed miserably, lacking demand and feasibility. For example, their early commercial trial at residential CHP almost sent the company to bankruptcy, forcing the company to shift its focus entirely and commercially start from “zero”.

Another issue we mentioned earlier in this report and that was pointed out by multiple experts is the licensing business model. According to them, the licensing business model does not match the technology and its market for multiple reasons. The most important one is that the SOFC technology developed by Ceres is an advanced form of technology and therefore highly complex. After shifting the risk to the licensee that has to develop the system around the cells or the stacks, even though Ceres will provide engineering support to the licensee, it still bears an enormous amount of risk. Indeed, even though Ceres also offers system IP, the licensee still has to do the heavy work.

The licensee has to outlay the capital necessary for the additional research & development, testing, manufacturing and keeps the risk of the technology not being up to their standard, or the developed product not attaining the sufficient market success. Moreover, the systems built around Ceres’ technology might yield different/inconsistent performance that could disappoint. Everything mentioned here takes years to achieve, delaying royalties paid to Ceres as well as a risk of failure, which happened in most cases. On top of this, if everything successfully happens, the licensee still has to pay royalties to Ceres, which adds significant pressure to their margin and commercial prospects. All of these combined reveal a flawed business model, with heightened risks of delays and failures, as well as increased difficulty in finding new licensees. Ceres is essentially asking partners to accept technical, commercial, and financial risk.

Even though it is a known issue, highlighted by management themselves, it is still worth mentioning that the licensing business model bears the important risk of IP appropriation and/or stealing by licensees and other third parties. Even though the company has said to have put protection mechanisms in place, it is never truly a risk that is mitigable, and could severely impact the company’s ability to remain attractive to new customers, even if it is not observable on the surface.

More Fundamental Issues That Dwarf Ceres Potential

The addressable market itself is also an issue, as many experts pointed out, the SOFC market has been and is still relatively small compared to other technologies such as gas turbines or diesel generators. Even though the SOFC boasts higher performance and durability, it is currently unproven, lacks serviceability at scale and offers insufficient reliability guarantees. This reduces the appeal of the technology to various markets that are seeing exponential potential growth such as data centers.

Indeed, most experts agreed on the fact that, even though attractive, data centers do not constitute the “silver bullet” for Ceres technology. Indeed, research shows that Solid Oxide Fuel Cell (SOFC) inherently suffers from serious durability, degradation, and reliability issues: including thermal-stress, seal failure, and gradual material degradation under high-temperature operation which is specific to the technology. Data-center applications demand near-absolute uptime (five-nines uptime rule, 99.999%) and rapid response to load changes, but SOFC’s long start-up times, sensitivity to fuel quality or supply disruption, and complex maintenance undermines its suitability for such critical “always-on” environments. Compared to mature and well-understood diesel/gas generators or grid-tied power, SOFC lacks a proven track record of reliability at scale, making it much riskier as a primary data-center power source. Economies-of-scale and centralized generation further favor conventional power systems over modular, high-capex, maintenance-intensive SOFC installations. As a result, the idea that data centers are the “silver bullet” market for SOFC (and by extension for Ceres) appears structurally flawed and overly optimistic given current technical and market constraints.

Another fundamental issue is the inherent competition coming from smaller addressable markets. We believe that Ceres, once it has signed a licensee in a given country, has very minimal chance to find another licensee in the same country, drastically limiting its opportunities and also increasing the reliance on any licensee. As they are already competing with other SOFC/SOEC technologies, licensees cannot afford to compete with other companies that also develop their systems around Ceres’ technology as well. In other words, once Ceres signs a new licensee in a country, not only does it take years to achieve any results, but the results are entirely in the hands of the licensee.

And finally, most markets Ceres’ licensees are operating in are mostly subsidy-driven, following authorities/government directives. Therefore, not only is Ceres dependent on its licensees, but the licensees themselves are mostly dependent on their government directives.

The SOEC Market Bears the Same Issues

To add a few points on the SOEC licensees and prospects, it is very similar to the SOFC environment, but the risks are heavier for the licensees. Currently, Ceres has a few licensees and partners pursuing commercialization using Ceres technology which are Delta (dual licensee SOFC/SOEC, but currently prioritizing hydrogen related products, thus SOEC), Denso and Shell/Thermax. These licensees generated smaller license fees given the smaller SOEC market size and commercial prospects, estimated at less than $400 million globally in 2024. The company’s management admits it themselves, in their Annual 2024 report, they state that the SOEC market is immature and the Total Addressable Market is solely based on forecasts”. Therefore, the reluctancy from licensees or partners to invest capital in developing a product and bringing it to commercialization is high, and heavily depends on the market trajectory in the future. Not only is the business model around SOEC as flawed as SOFC’s, but it would yield smaller revenue for Ceres. We do not have much hope for this business segment either.

All these points reflect the complex and unfavorable situation that comes with Ceres’ business model and technology: overreliance on uncontrollable facts, competing with traditional technology, burdening licensees with significant risk and competing in a small market with an unproven technology.

Conclusion

In conclusion, our in-depth analysis of Ceres Power Holdings plc reveals a company ensnared in a cycle of overpromising and underdelivering, perpetuating investor illusions through a veneer of high-profile announcements and partnerships that rarely translate into sustainable value. From its historical pattern of ambitious collaborations with industry giants like Bosch, Nissan, and Honda, each heralded with fanfare only to dissolve without meaningful outcomes, to the consistent retraction of lofty revenue projections, Ceres has demonstrated an inability to convert technological promise into commercial reality.

Expert insights and the company’s own disclosures underscore that its revenue potential is dramatically overstated, constrained by partner dependencies, market adoption hurdles, and negligible royalty streams.

The recent developments with licensees such as Doosan Fuel Cell and Weichai further exemplify this flawed paradigm. Doosan’s mass production milestone, which propelled Ceres’ stock to new heights, has yielded only a solitary 9MW related-party order after months of operation, potentially generating a paltry $1.35 million in gross margin for Ceres amid admissions of underwhelming results and no anticipated new orders for the year. Similarly, the new manufacturing agreement with Weichai, a significant shareholder, appears as yet another iteration in a lineage of failed joint ventures, dismissed by Weichai itself as routine business unworthy of formal disclosure. This reliance on partners to shoulder the burdens of design, industrialization, and capital investment has sustained Ceres for over a decade on sporadic licensing and engineering fees alone, with no evidence of evolving into a royalty-driven powerhouse.

Ultimately, we believe Ceres embodies a fundamentally flawed business model unfit for a public company in its current form. The very announcements that have inflated its market capitalization by hundreds of millions are poised to evaporate into minuscule earnings. Investors would be wise to approach with caution, prioritizing substance over spectacle in this evolving energy landscape.